The Trump administration’s cuts to federal science funding threaten the U.S.’s innovation pipeline, which relies heavily on federally supported research at universities and labs. In this article in the Silicon Valley Business Journal, Dr. Jeff Welser, Chairman of the Bay Area Science and Innovation Consortium (BASIC), and Sean Randolph, Senior Director of the Institute, provide insight into how science and technology will be greatly impacted as a result of these new federal policies.

The Trump administration’s cuts to federal science funding threaten the U.S.’s innovation pipeline, which relies heavily on federally supported research at universities and labs. In this article in the Silicon Valley Business Journal, Dr. Jeff Welser, Chairman of the Bay Area Science and Innovation Consortium (BASIC), and Sean Randolph, Senior Director of the Institute, provide insight into how science and technology will be greatly impacted as a result of these new federal policies.

Recent political and economic decisions, particularly tariffs, have strained relationships with allies like Canada, Mexico, Australia, and European countries, causing diplomatic fallout and economic uncertainty. In this article on Medium.com, Sean Randolph, Senior Director of the Institute, reflects on the declining strength of U.S. global alliances and emphasizes the long-term impacts of dismantling institutions and relationships.

AI is fueling economic recovery in the Bay Area. Chinese AI startup DeepSeek’s open-source R1 model has raised concerns about AI investment, but its energy-efficient and low-cost innovations could accelerate AI adoption. In this San Francisco Business Times article, Sean Randolph, Senior Director of the Institute, highlights how AI’s growing impact across industries, combined with California’s emphasis on workforce training and innovation, will help the region maintain its leadership in the sector.

The Biden’s administration’s support for electric vehicles (EV’s), including tax incentives and funding for charging infrastructure, is being rolled back. In this article in the Silicon Valley Business Journal, Sean Randolph, Senior Director of the Institute, discusses the potential negative impact of the current overhaul of U.S. government policies on the competitiveness of the U.S. electrical vehicle industry.

As a new year begins the San Francisco/Silicon Valley Bay Area’s economy remains consistent with patterns over 2023 and 2022: a mixed story of slow progress in addressing underlying structural challenges, combined with resurgent innovation at the research and business levels. In this article in the Times of India, Sean Randolph, Senior Director of the Institute, details high-level takeaways for the future of the Bay Area’s economy as the regions continues to recover from the pandemic.

The Trump presidency will reshape the United States relationship with the rest of the world. Changes from the current administration will be abrupt, with a long list of campaign promises revolving around ending the war in Ukraine, immigration reform, tariffs, and much more. In this article in the Silicon Valley Business Journal, Sean Randolph, Senior Director of the Institute, puts aside the strategic issues and details early takeaways on the economic side of the incumbent administration.

The worldwide shift of production is fully underway as companies with global operations diversify their sourcing and work to manage risk. A trend for several years, this has become a flow. A less hospitable environment in China and tensions in US-China relations are a driver, but so is the need to reduce dependence on any one country (a problem laid bare by China’s pandemic shutdowns) and a desire to bring production closer to home. In this article in the Silicon Valley Business Journal, Sean Randolph, Senior Director of the Institute, details the three prime destinations for production for the U.S. which include India, Mexico, and Southeast Asia.

As Mexico’s strategic importance to the U.S. grows, its newly elected president, Claudia Sheinbaum, has an opportunity to deepen the economic relationship and with-it prosperity in both countries. In this article in the Silicon Valley Business Journal, Sean Randolph, Senior Director of the Institute, details the vision and what the future can hold between the two nations and the greater North America.

The Asian Pacific Economic Cooperation (APEC) conference was a pivotal event for the Bay Area and San Francisco. With the City in the world spotlight for the first time since the founding of the United Nations in 1945, San Francisco was given the prime opportunity to showcase its strengths and change the doom-loop media narrative. At APEC’s Biden-Xi summit President Xi hailed “the San Francisco Vision” as a reset in the relationship. In this article in the Silicon Valley Business Journal, Sean Randolph, Senior Director of the Institute, describes the vision and what the future can hold between the two nations.

The Asian Pacific Economic Cooperation (APEC) conference that recently concluded was a pivotal event for the Bay Area and San Francisco. With the City in the world spotlight for the first time since the founding of the United Nations in 1945, San Francisco was given the prime opportunity to showcase its strengths and change the doom-loop media narrative. In this article in the Silicon Valley Business Journal, Sean Randolph, Senior Director of the Institute, discusses how the APEC conference all played out.

The significance of India technology innovation and capacity has been growing tremendously, with Silicon Valley at the heart of that change. In this video, Sean Randolph, Senior Director of the Institute, recorded this program with the India Dialog program at Stanford, sponsored by the India Institute of Competitiveness and Stanford’s US-Asia Technology Management Center to discuss the connections of the Bay Area with India.

September 20, 2023

With the recent collapse of Silicon Valley Bank, most would say that the bank is dead and gone, however, SVB is very much alive and open for business. In this article in the Silicon Valley Business Journal, Sean Randolph, Senior Director of the Institute, discusses the changes and ongoing operations at SVB, which is good news for the Silicon Valley and the Bay Area.

June’s meeting between U.S. President Biden and India’s Prime Minister Modi advanced the U.S.-India connection to a new level. While the relationship falls short of an actual alliance and India and the U.S. may often differ, the alignment of national interests continues to deepen. In this article in the Times of India, Sean Randolph, Senior Director of the Institute, discusses the scope and breadth of cooperative agreements, mostly centered around technology, which has played an increasingly important role in the relationship

Europe and the United States are allies, collaborators — and competitors. Today, it is increasingly important that Europe and the United States look beyond competition to align their policies and capabilities around shared strategic goals. In this article in the SF Business Times, Sean Randolph, Senior Director of the Institute, examines these connections and details why Europe and the U.S. don’t see eye-to-eye on technology regulation, which is ultimately hurting both

India’s economic ties to the San Francisco/Silicon Bay Area are continuing to grow, led by the dramatic acceleration of India’s digital economy, the maturing and growth of its startup environment and the deepening geostrategic alignment between India and the U.S. In this article in the Silicon Valley Business Journal, Sean Randolph, Senior Director of the Institute, examines these connections and one of the greatest economic opportunities of the next decade.

India’s economic ties to the San Francisco/Silicon Bay Area are continuing to grow, led by reform and growth in India, Silicon Valley’s global reach, and geostrategic alignment between India and the US. These ties have been building for some time. What’s new, however, is the acceleration. In this article in the SF Business Times, Sean Randolph, Senior Director of the Institute, examines these connections and the broad range of opportunities in fintech, edtech, pharmaceuticals, healthtech, renewable energy, electrical vehicles, semiconductors, smart infrastructure, and space.

As part of the United States’ 2023 Asia-Pacific Economic Cooperation (APEC) Host Year, San Francisco will host APEC’s Economic Leaders Week and the CEO Summit in November 2023. The meetings will enable meaningful engagement on open trade and investment, resilience, economic inclusion, sustainable economic growth and digital transformation across the Asia-Pacific. In this article in the SF Business Times, Sean Randolph, Senior Director of the Institute, examines the opportunity for San Francisco to rehabilitate its global image.

U.S.-China tensions, supply chain vulnerabilities, reshoring, and other trends present a window of opportunity for North America. In this article in the SF Business Times, Sean Randolph, Senior Director of the Institute, examines the potential for North America if the U.S., Canada and Mexico can seize it.

With the City of San Francisco’s recovery lagging behind other major U.S. cities, could an innovation hub in downtown San Francisco be modeled after a Canadian city? In particular, Toronto? In this article in the SF Business Times, Jim Wunderman, President and CEO of the Bay Area, and Sean Randolph, Senior Director of the Institute, examine the possibilities and feasibilities of converting the City into an official innovation hub.

Between extended economic shutdowns to combat the COVID-19 pandemic, work-from-home policies employed by Bay Area businesses, and a sharp reduction in travel, the region’s downtown cores have experienced a hollowing out of economic activity. As the region recovers, it has become clear that the pandemic has permanently changed how and where people work, how businesses think about their location decisions, and where households choose to live. These effects appear to be most visible in expensive coastal regions, including the San Francisco Bay Area.

To evaluate and track key indicators of economic recovery in the Bay Area, the Bay Area Council Economic Institute and CBRE’s Tech Insights Center are partnering on a three-year, three-part series of interactive reports. The first part of this analysis, published below, tracks jobs, people, investment, economic activity, and affordability measured by 1) an economic index tracking recovery across the nation’s 25 largest regions, and 2) a deeper dive into our region’s economic recovery.

Regional Economic Recovery Index

To better understand how our region fared compared to peer regions, we scored metropolitan statistical areas (MSAs) on 15 different datapoints across 5 different metrics: Jobs, People, Investment, EconomicActivity, and Affordability. Twenty-five regions were selected based on the size of their 2020 regional gross domestic product (GDP), a typical measure of the size of a region’s economy. For a full list of regions and their GDPs, and a detailed list of metrics that went into the index, check out our data and methodology section.

Each region was scored by taking percentile ranks (wherein 0 is the lowest rank, 100 is the highest) of 14 different metrics. Austin scored 100 in the People category, meaning it had the highest rate of both population growth and labor force growth, the two metrics in that category. San Diego, San Jose, San Francisco, and Los Angeles all scored the lowest because they experienced the greatest population and labor force losses given their pre-pandemic levels.

Austin, Texas ranked first across the 25 regions in our study, scoring an average of 92.8 (out of 100) across the 15 metrics we evaluated. Within these metrics, it ranked first (100/100) on 10 metrics: job growth, “knowledge worker” growth, growth in job postings, growth in “computer and mathematical” job postings, population growth, labor force growth, net absorption, new housing units per capita, sales tax revenue growth, and air travel growth. These figures speak to the dramatic resilience and growth Austin, and Texas as a whole, experienced during the pandemic, while coastal cities like San Francisco and New York continue to suffer losses.

For questions about this project, please contact Abby Raisz, Research Manager at the Bay Area Council Economic Institute at araisz@bayareacouncil.org.

Check out the topic areas:

Jobs

People

Costs

Economic Activity

Investment

What’s Next

December 21, 2022

The highlights:

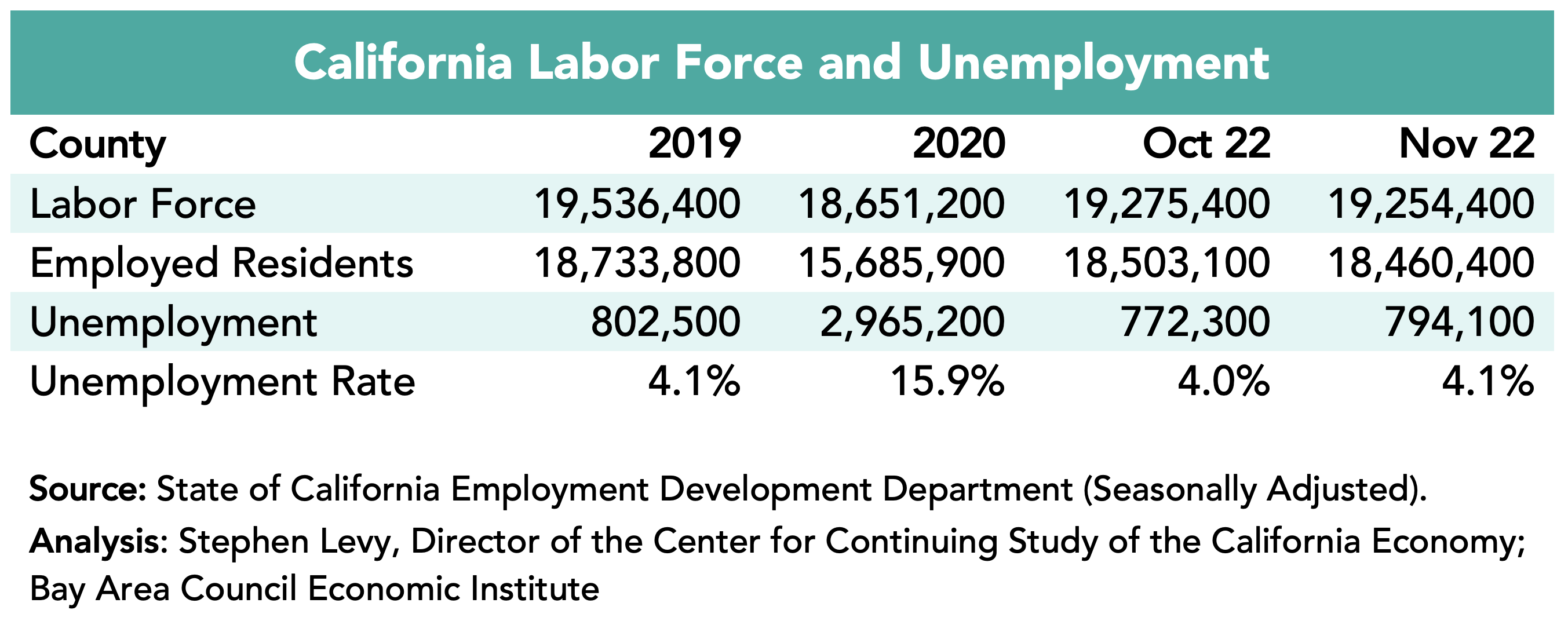

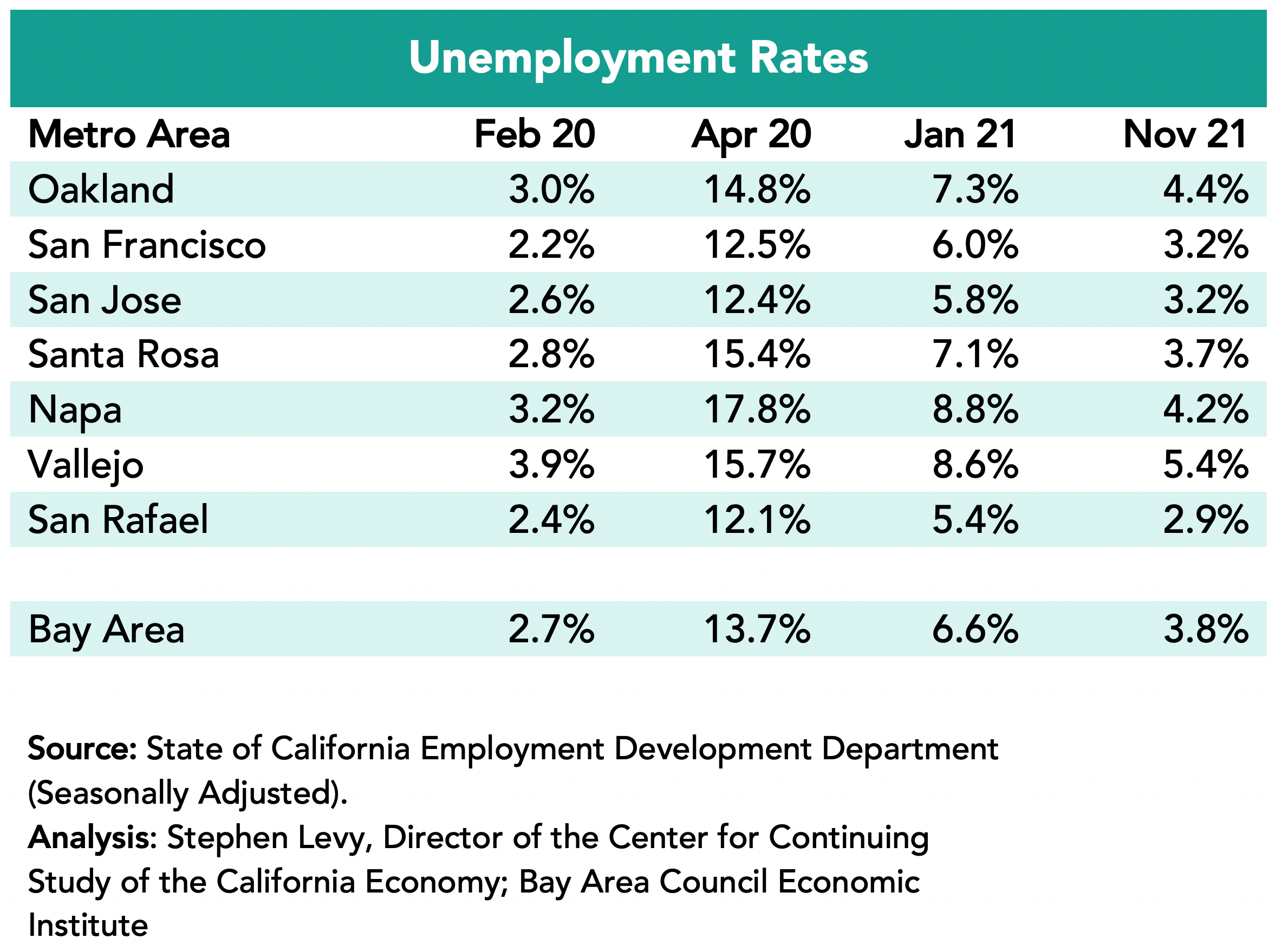

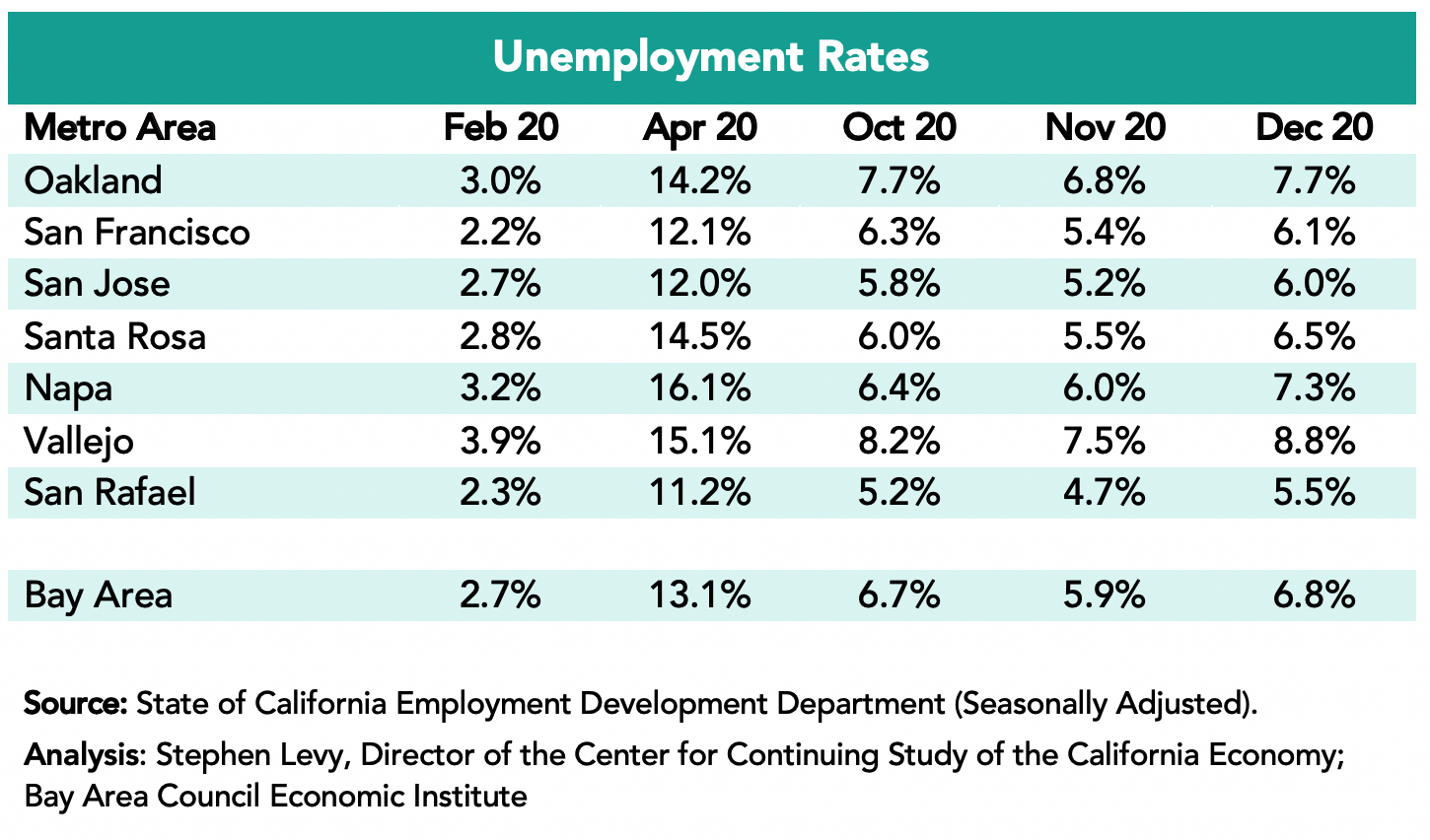

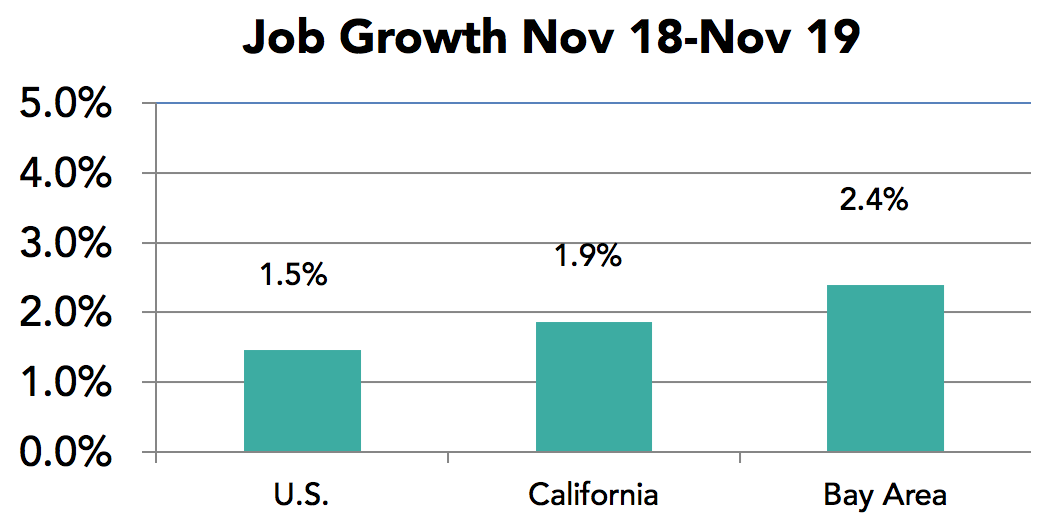

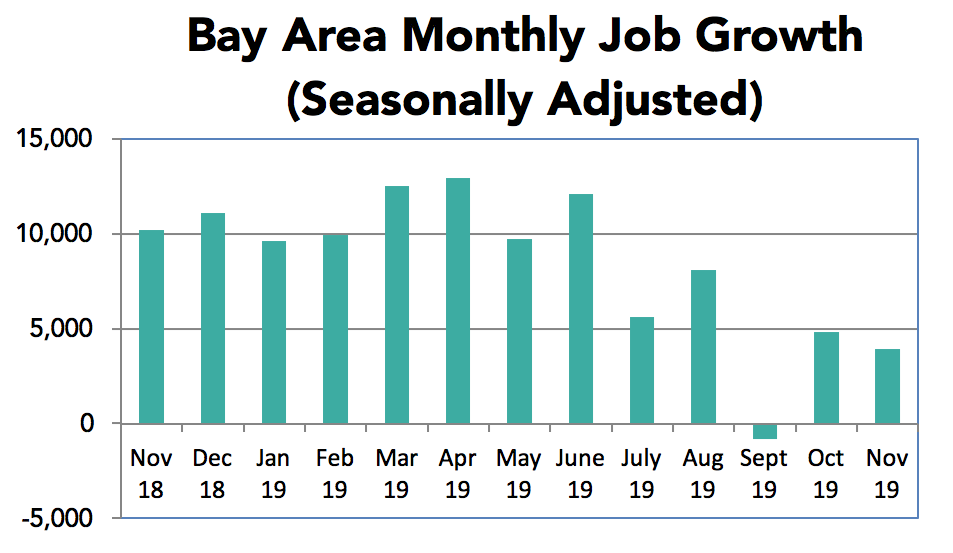

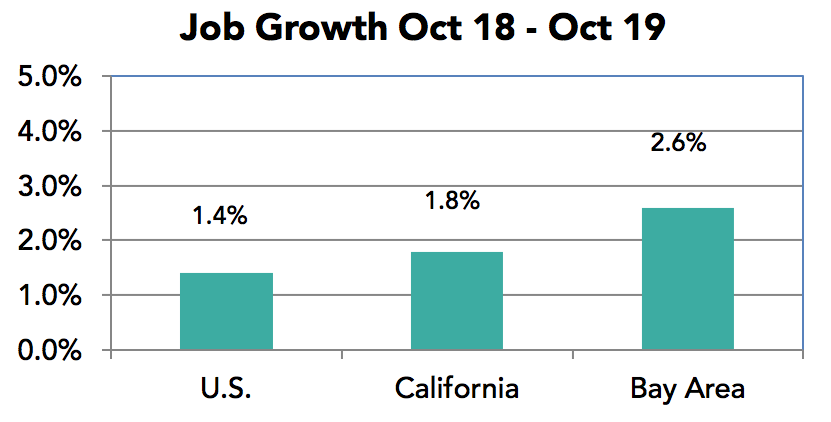

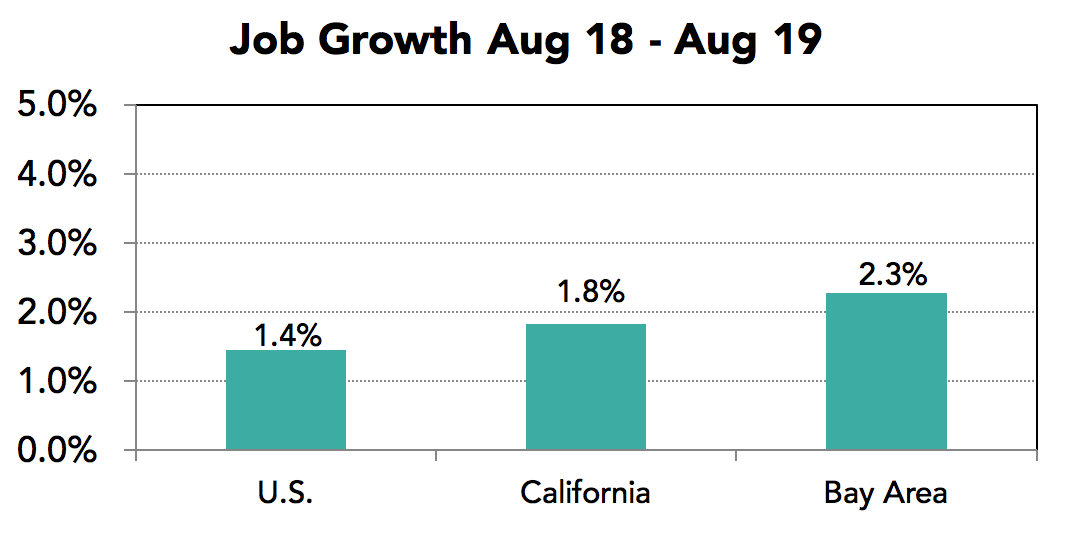

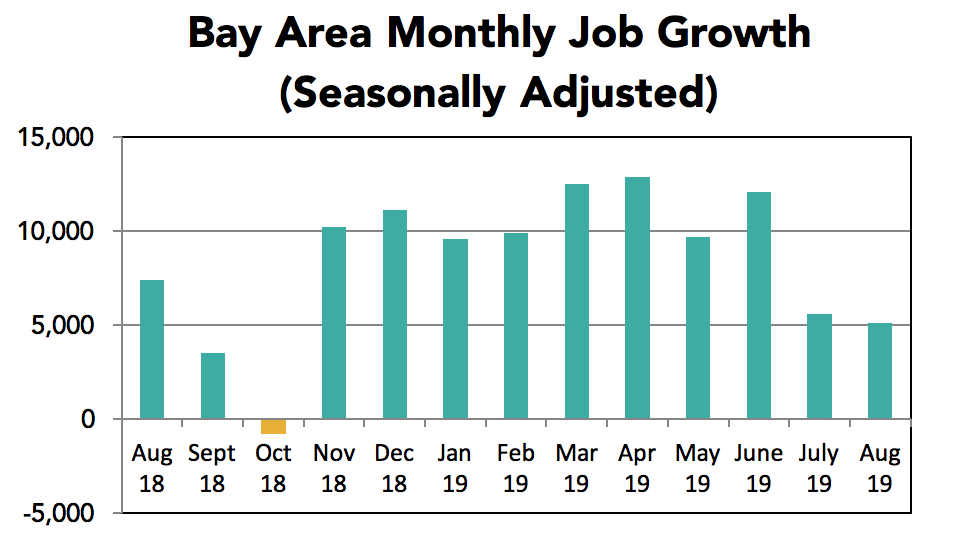

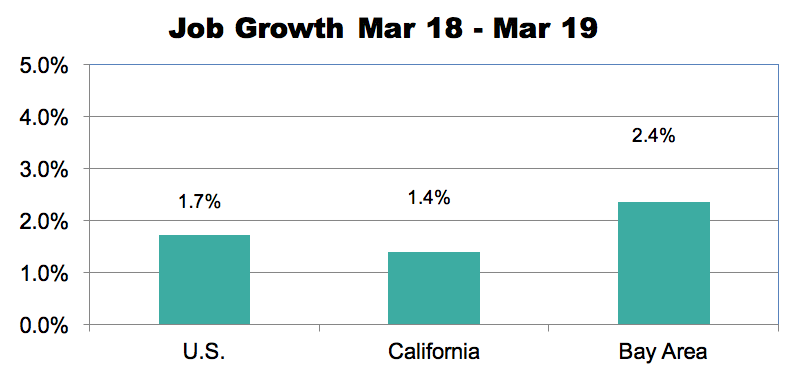

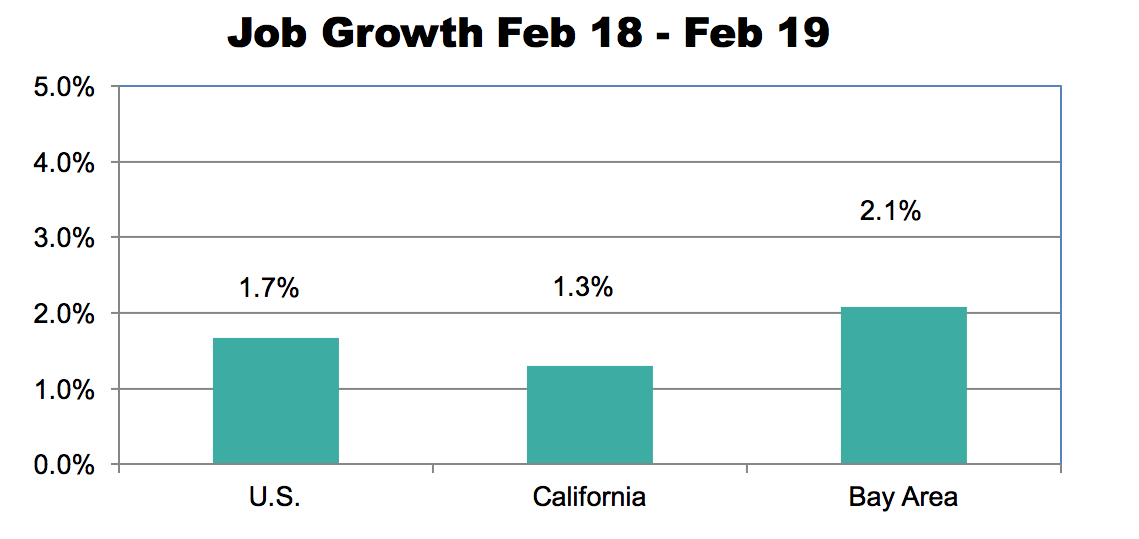

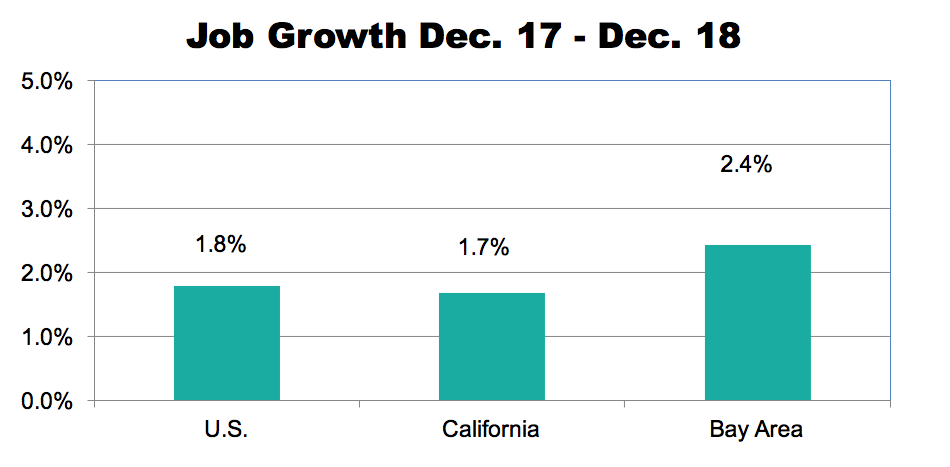

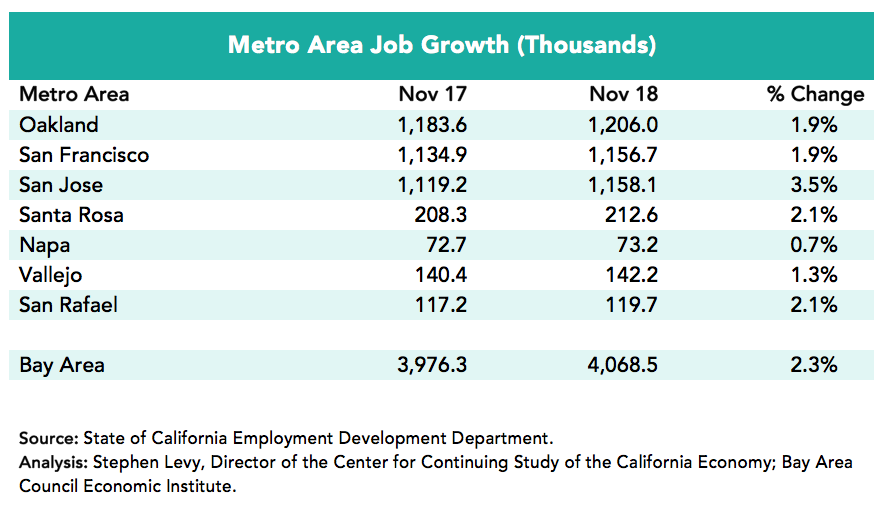

• The Bay Area added 7,400 jobs in November. The household survey, on the other hand, showed rising unemployment rates and a drop in the region’s workforce.

• Both the region and state showed conflicting trends between the jobs survey (up) and the household survey with rising unemployment and a decline in the labor force.

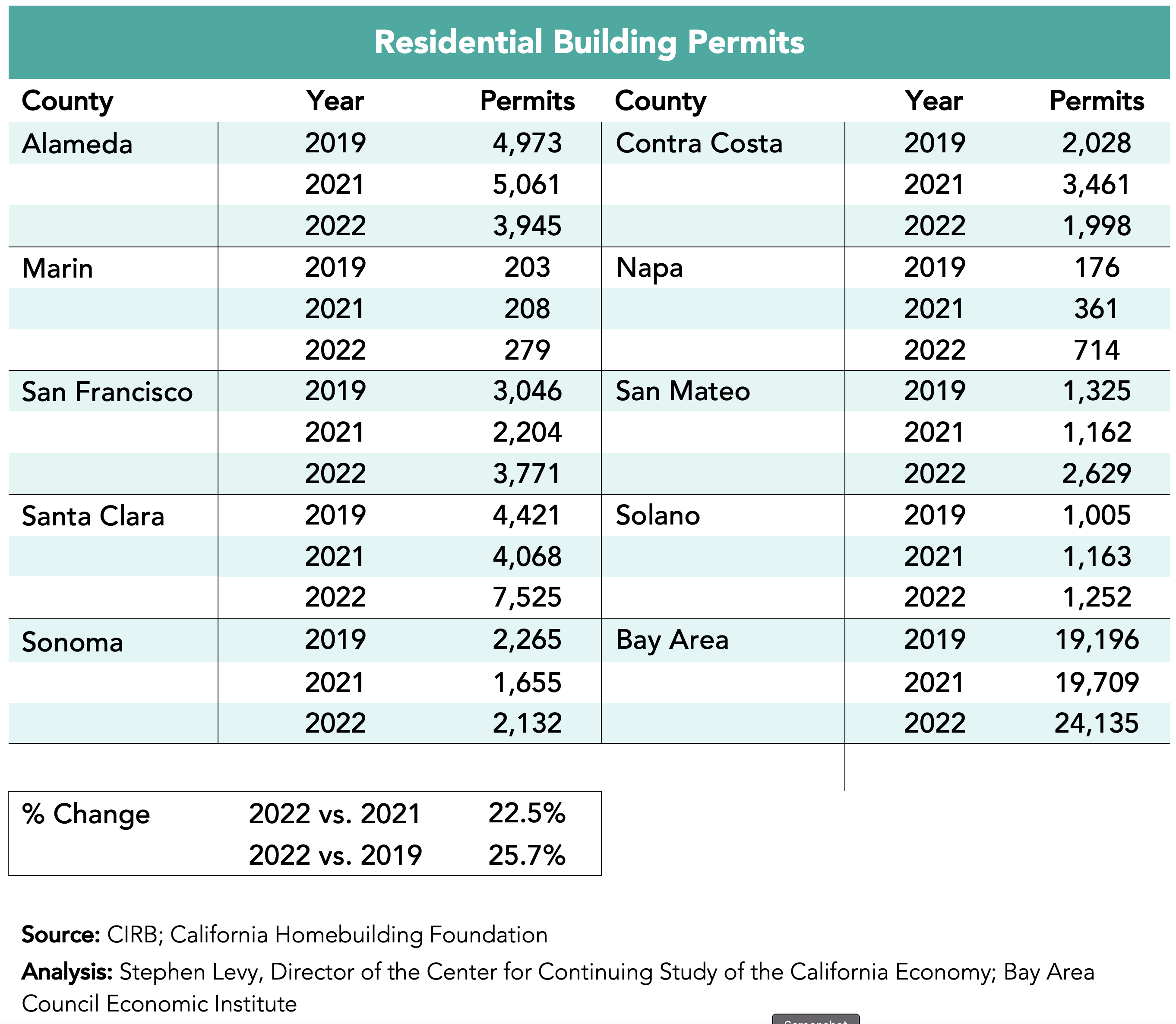

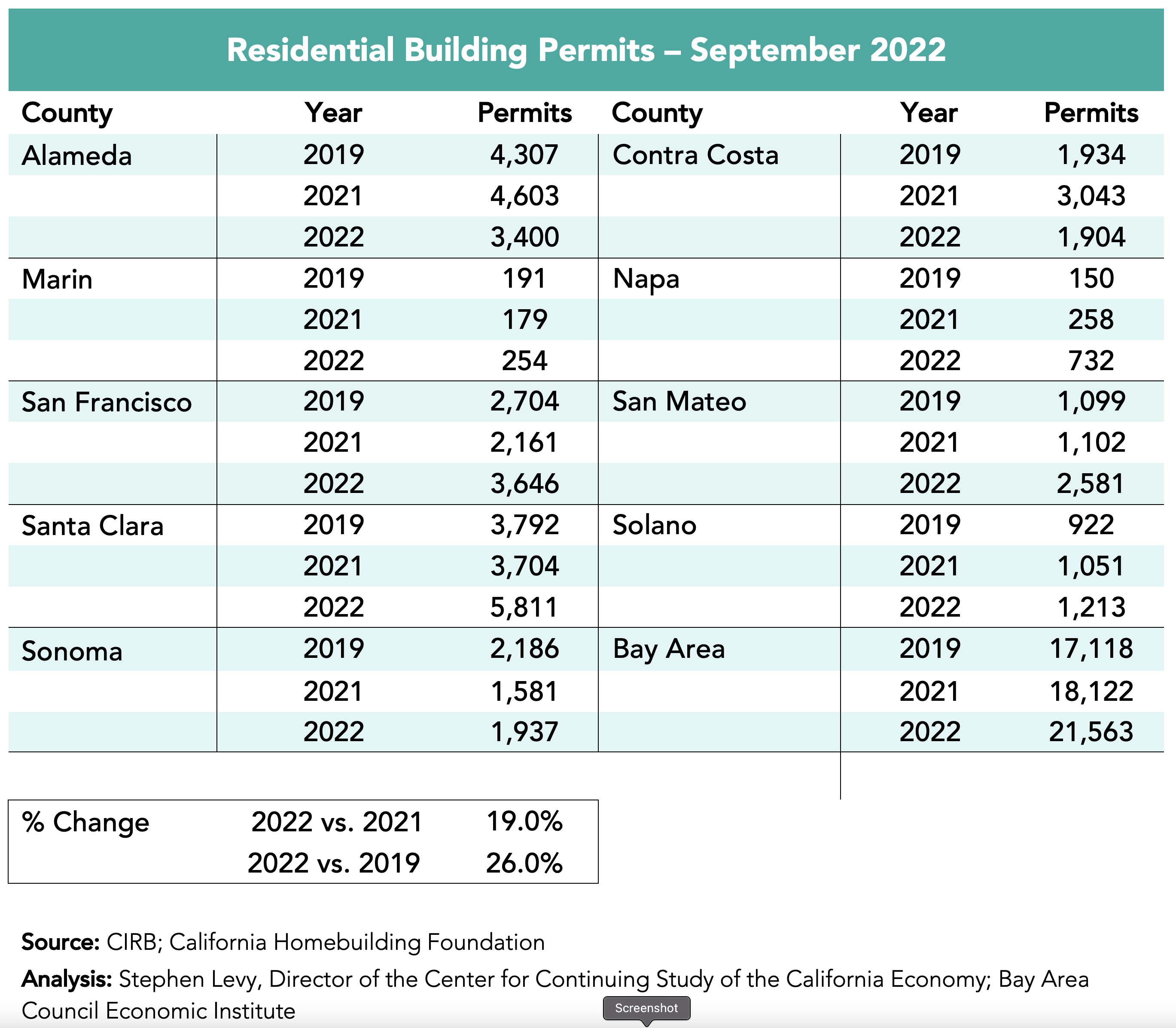

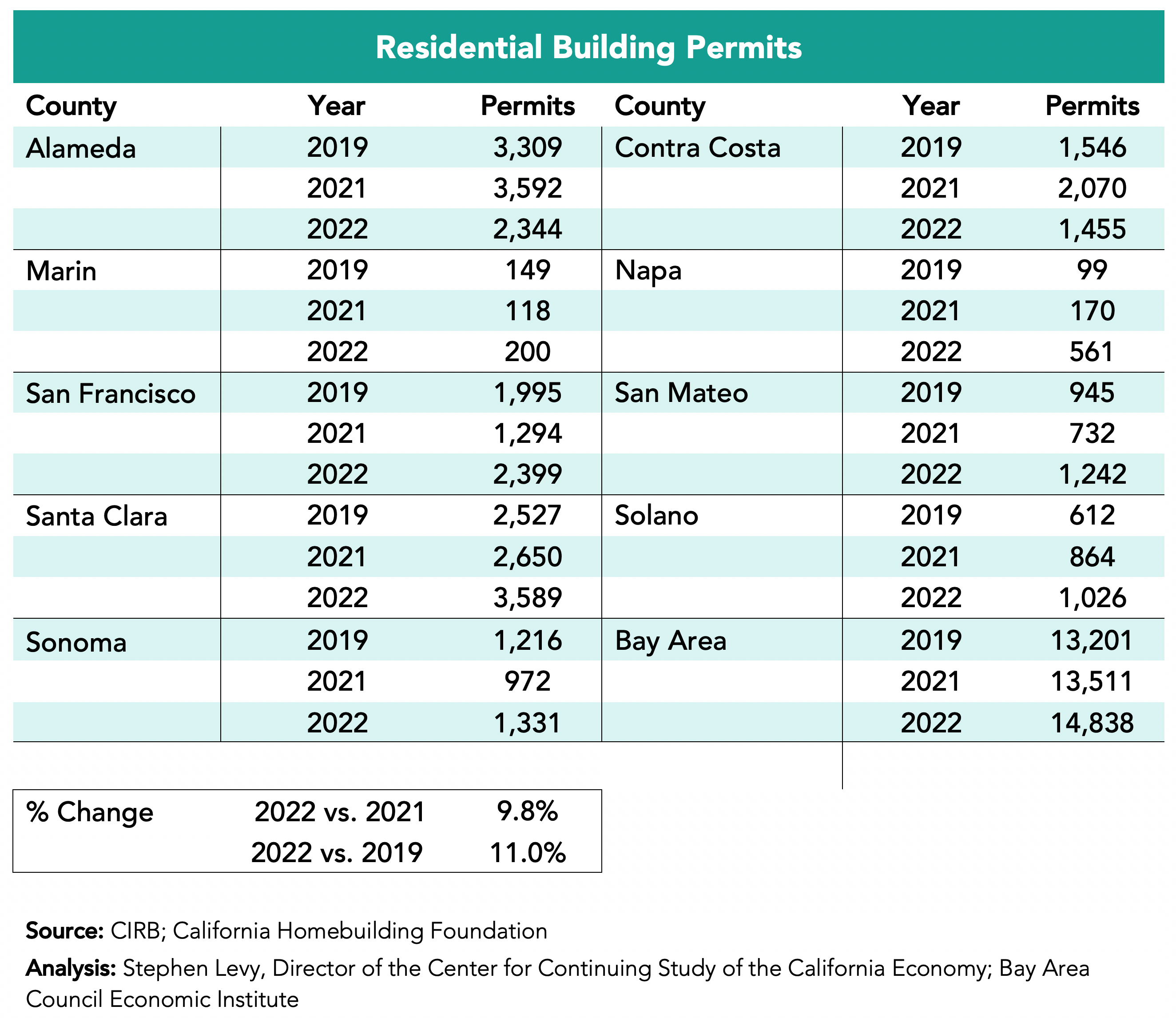

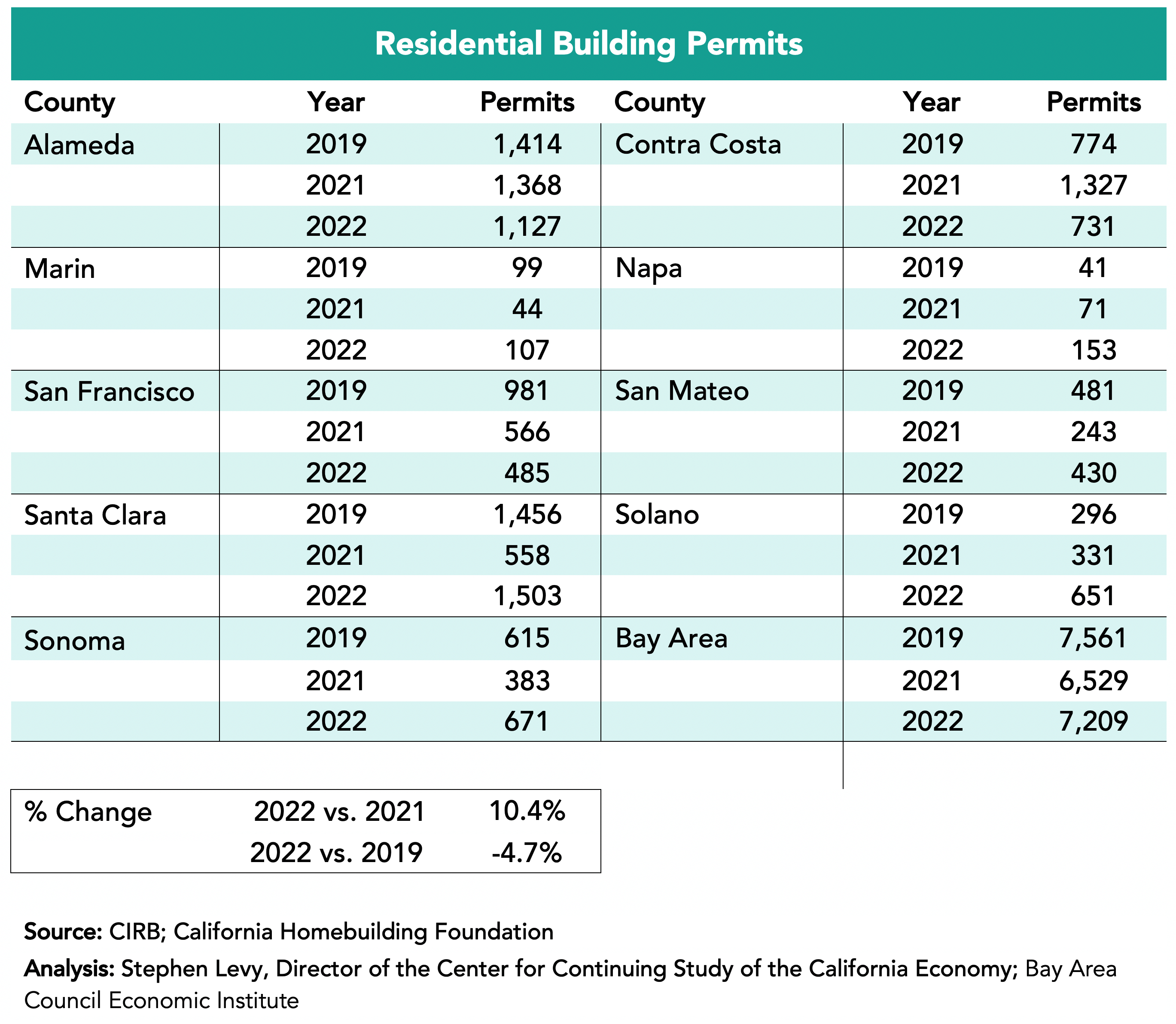

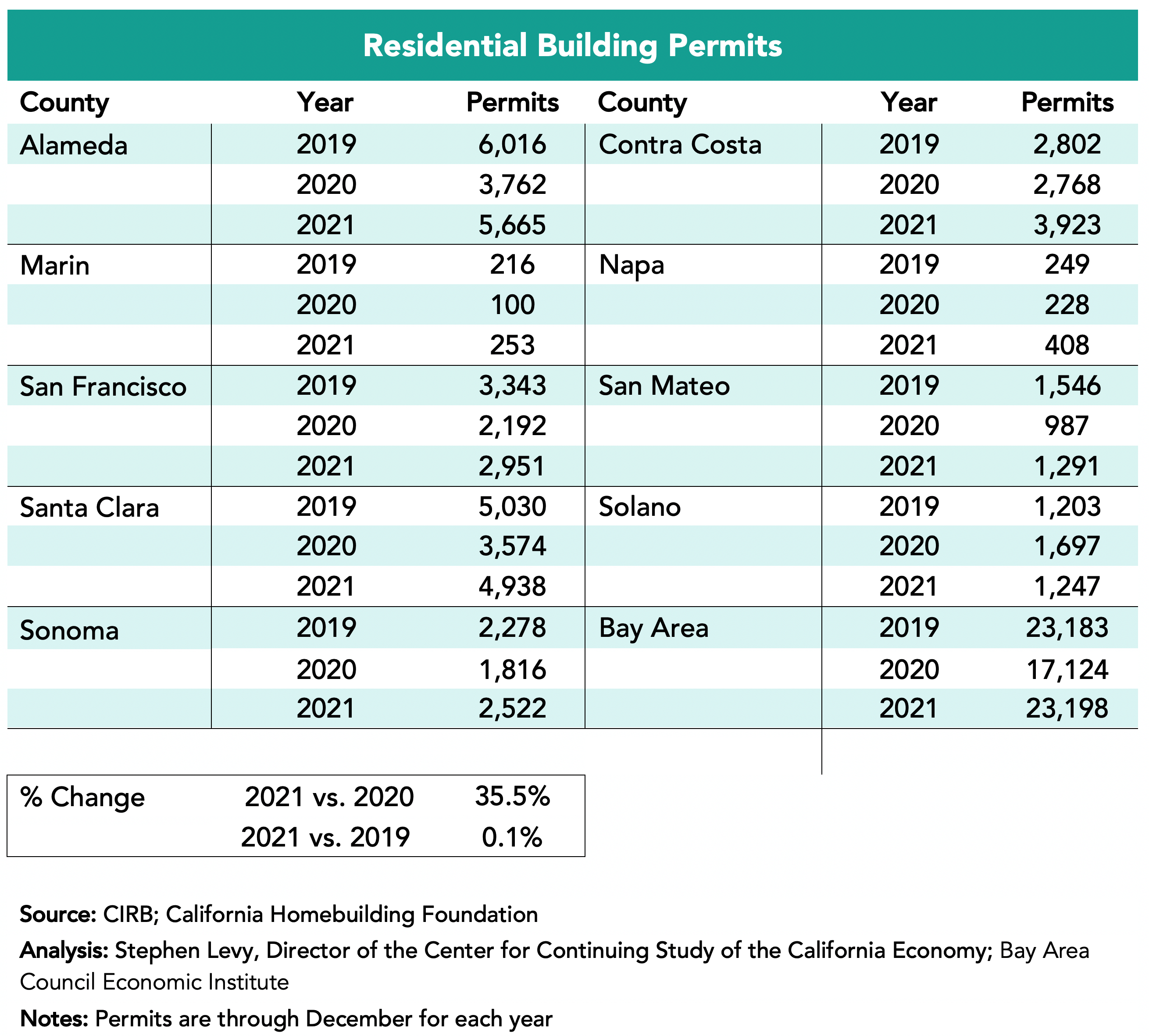

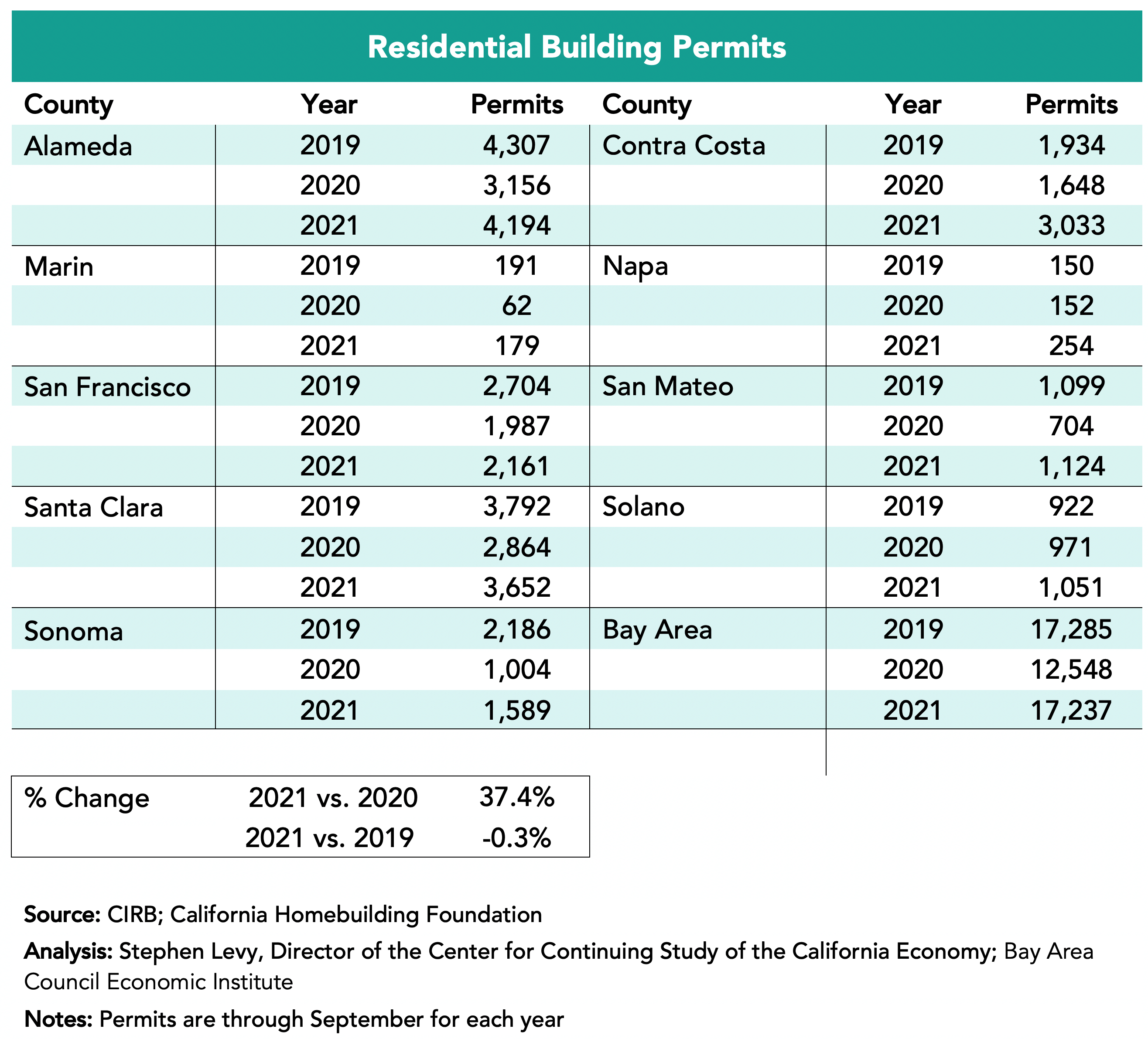

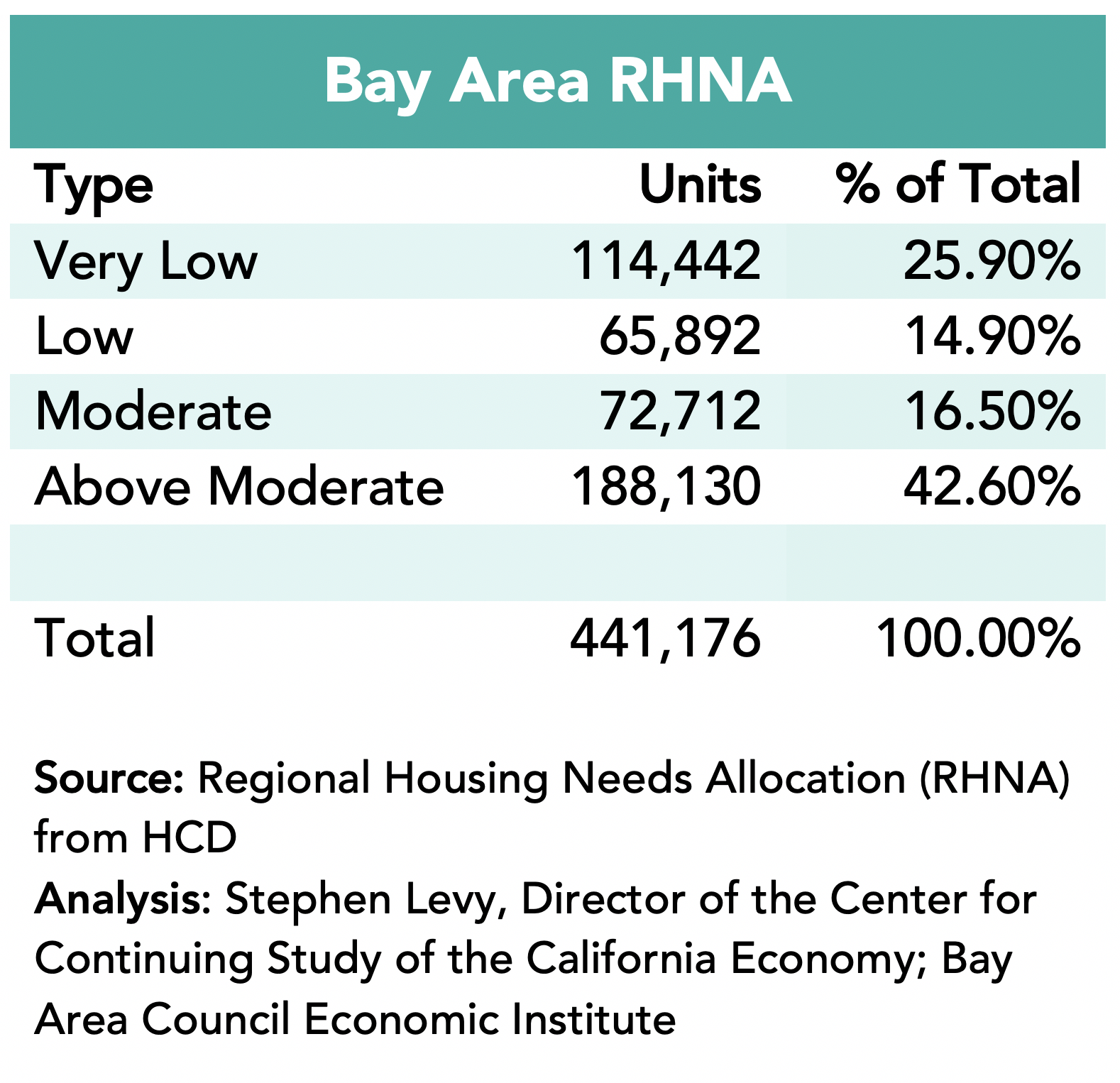

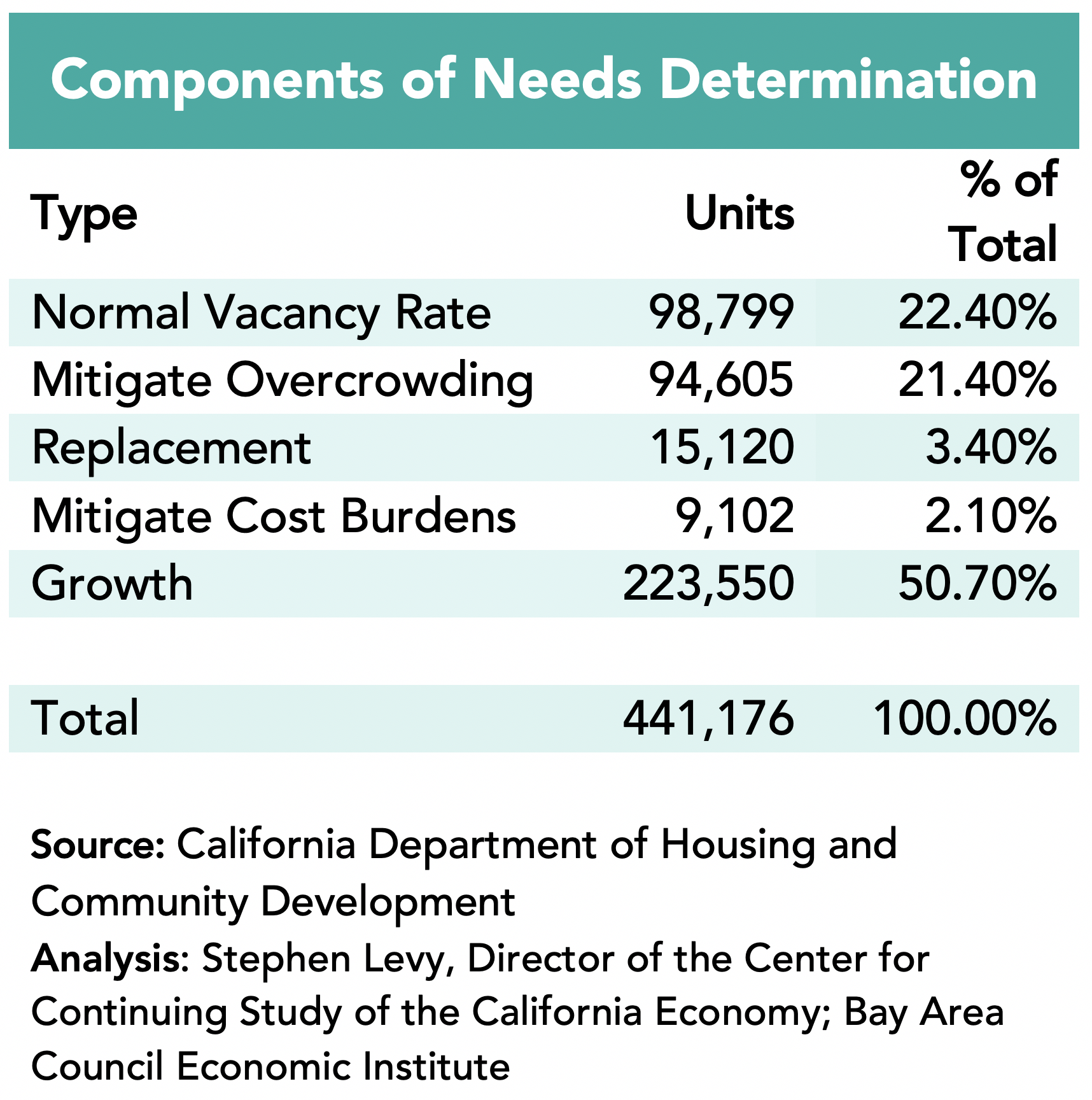

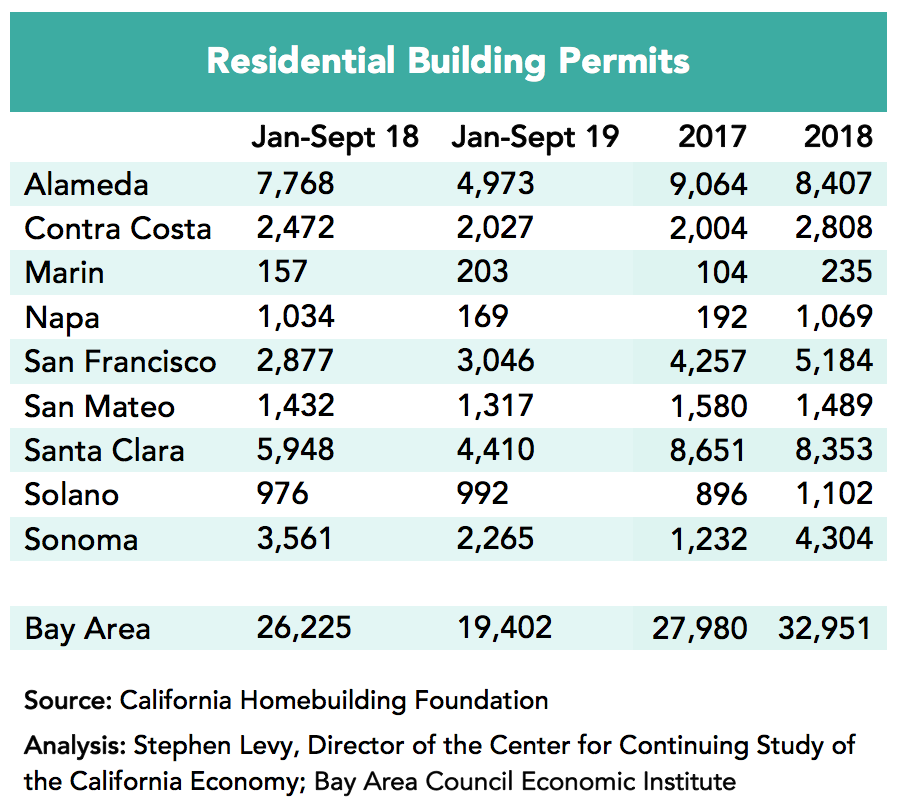

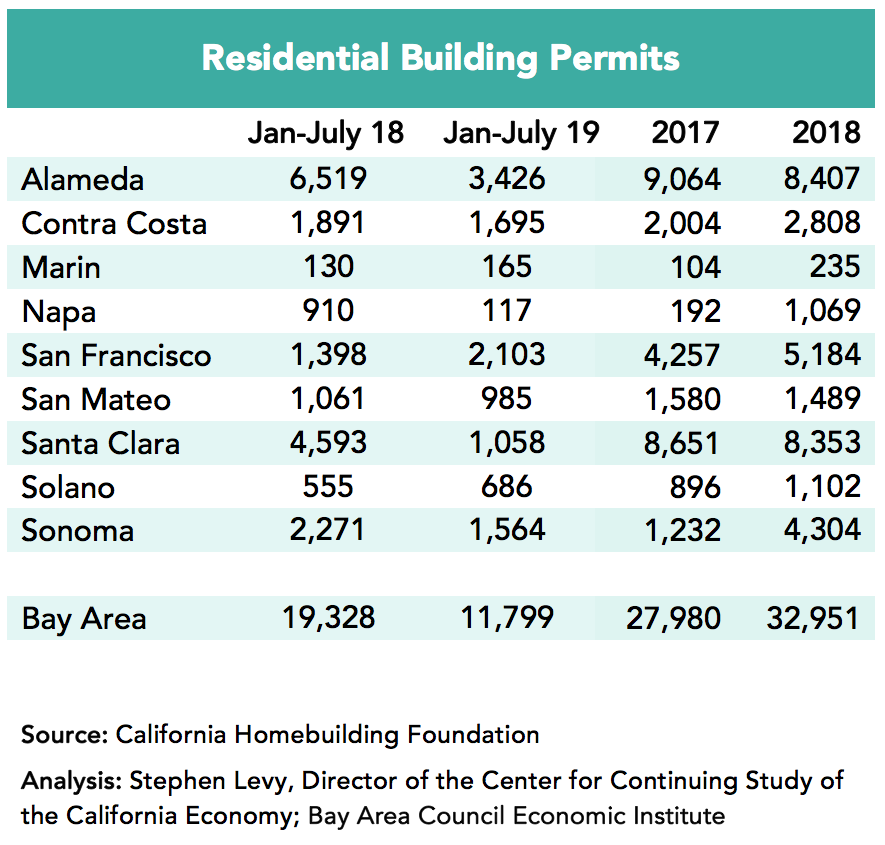

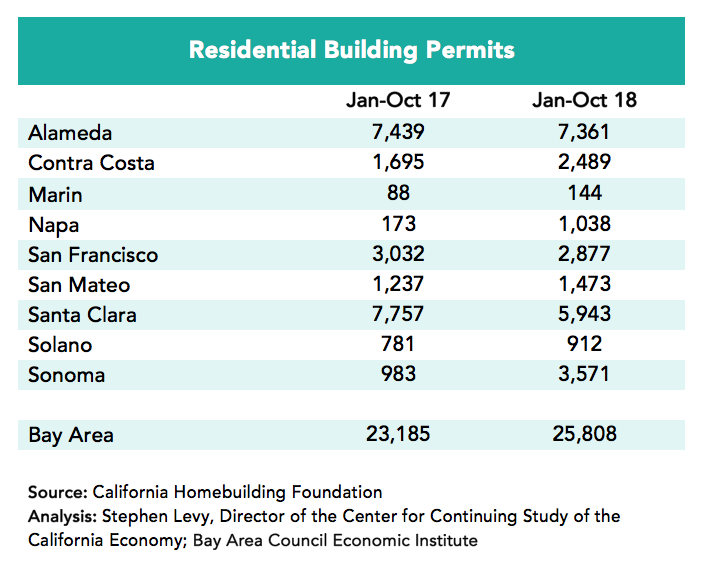

• Housing permits for the first ten months of the year surpassed both 2021 and 2019 levels though still well below the region’s new RHNA targets

• Bay Area GDP surged in 2021 with gains throughout the region with growth faster than all states and the nation.

• The challenges of high inflation and interest rates remain as well the Bay Area challenges of housing, transportation and supporting competitiveness.

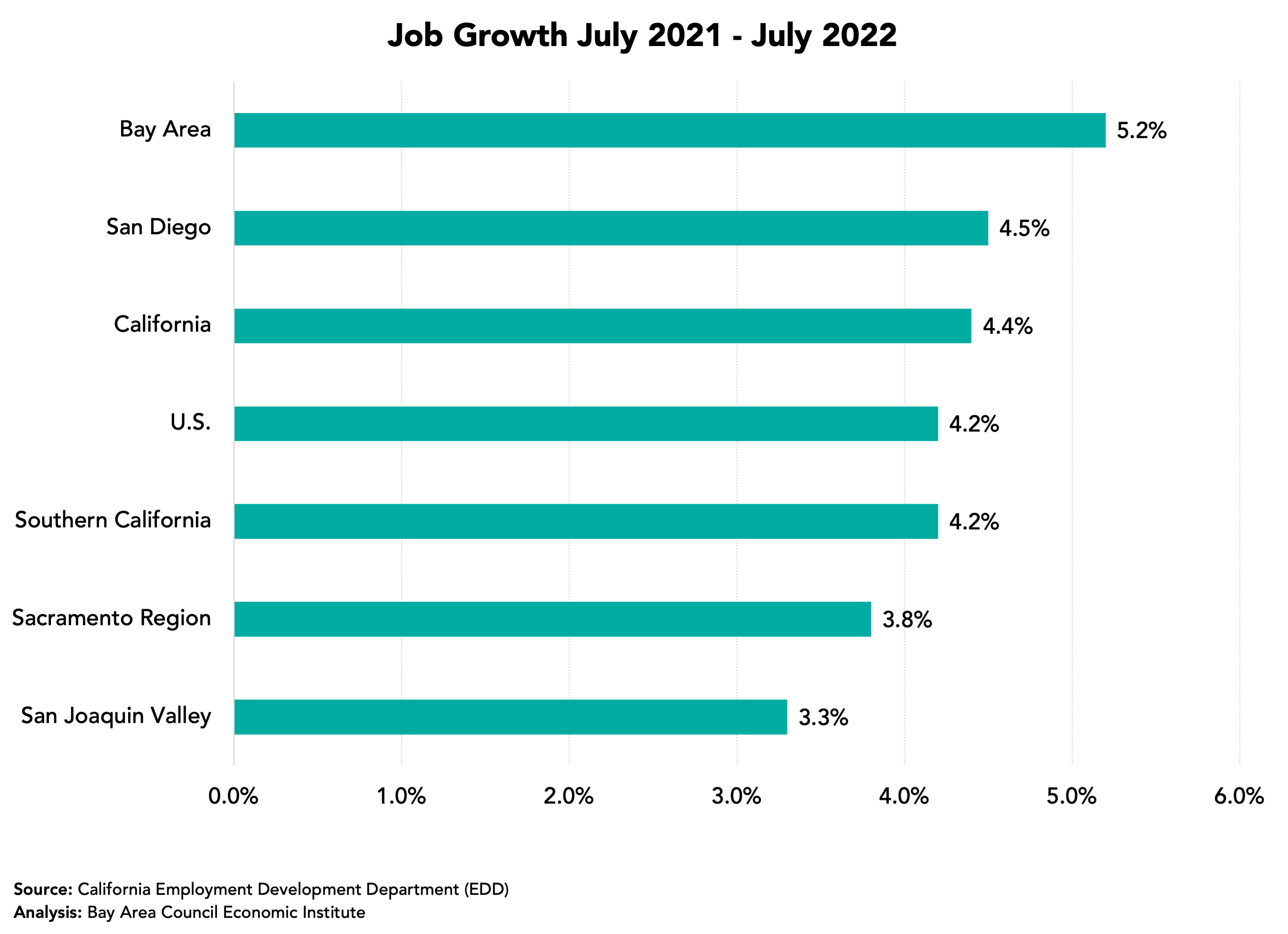

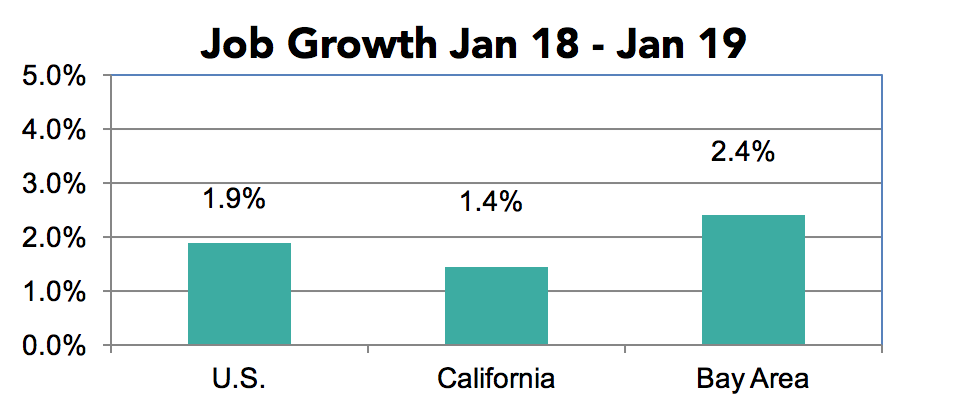

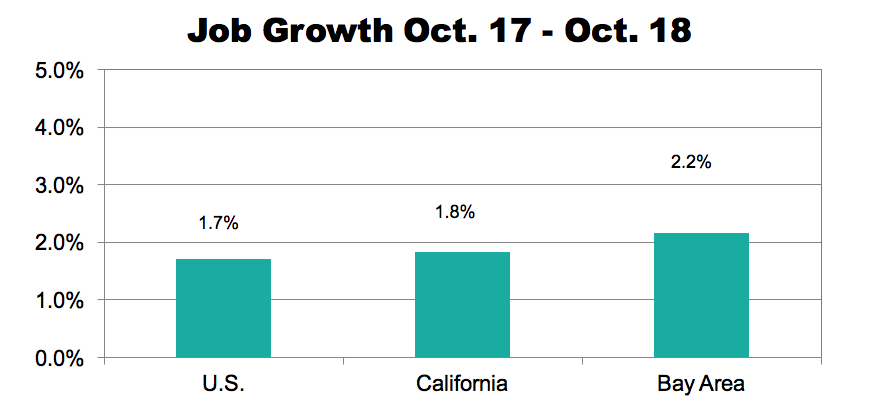

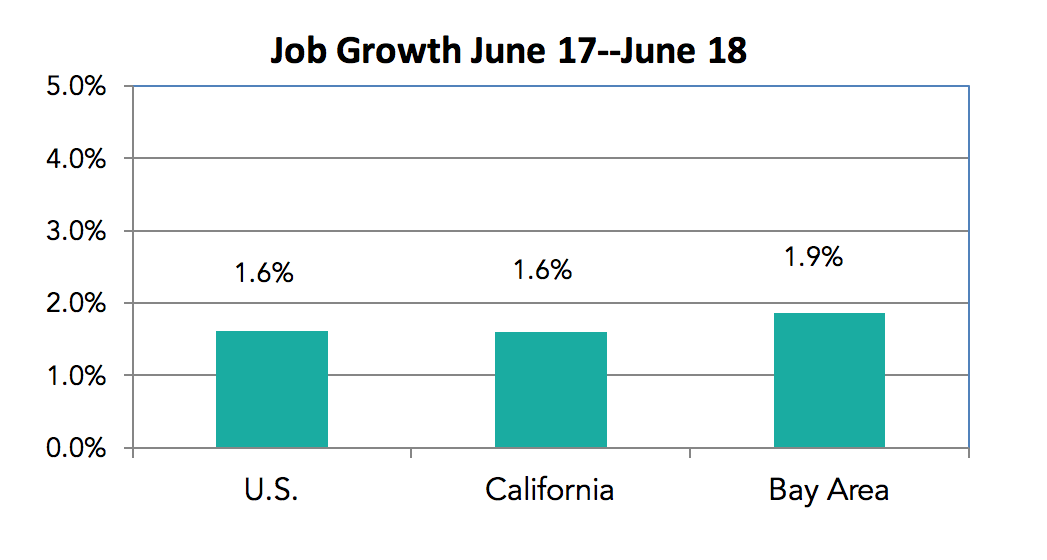

Even with the Recent Slowdown the Bay Area and State Posted Above Average Job Growth During the Past 12 Months

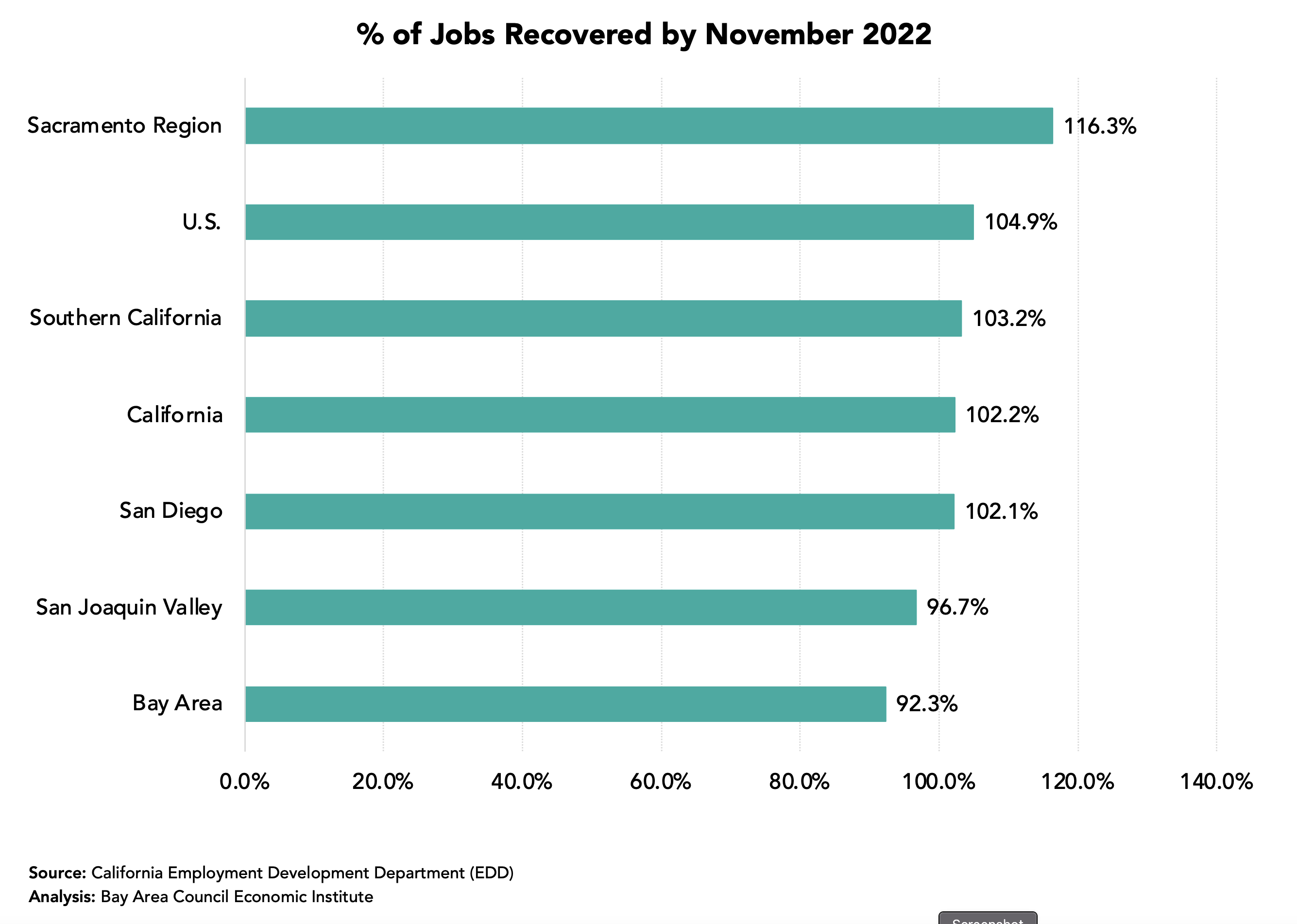

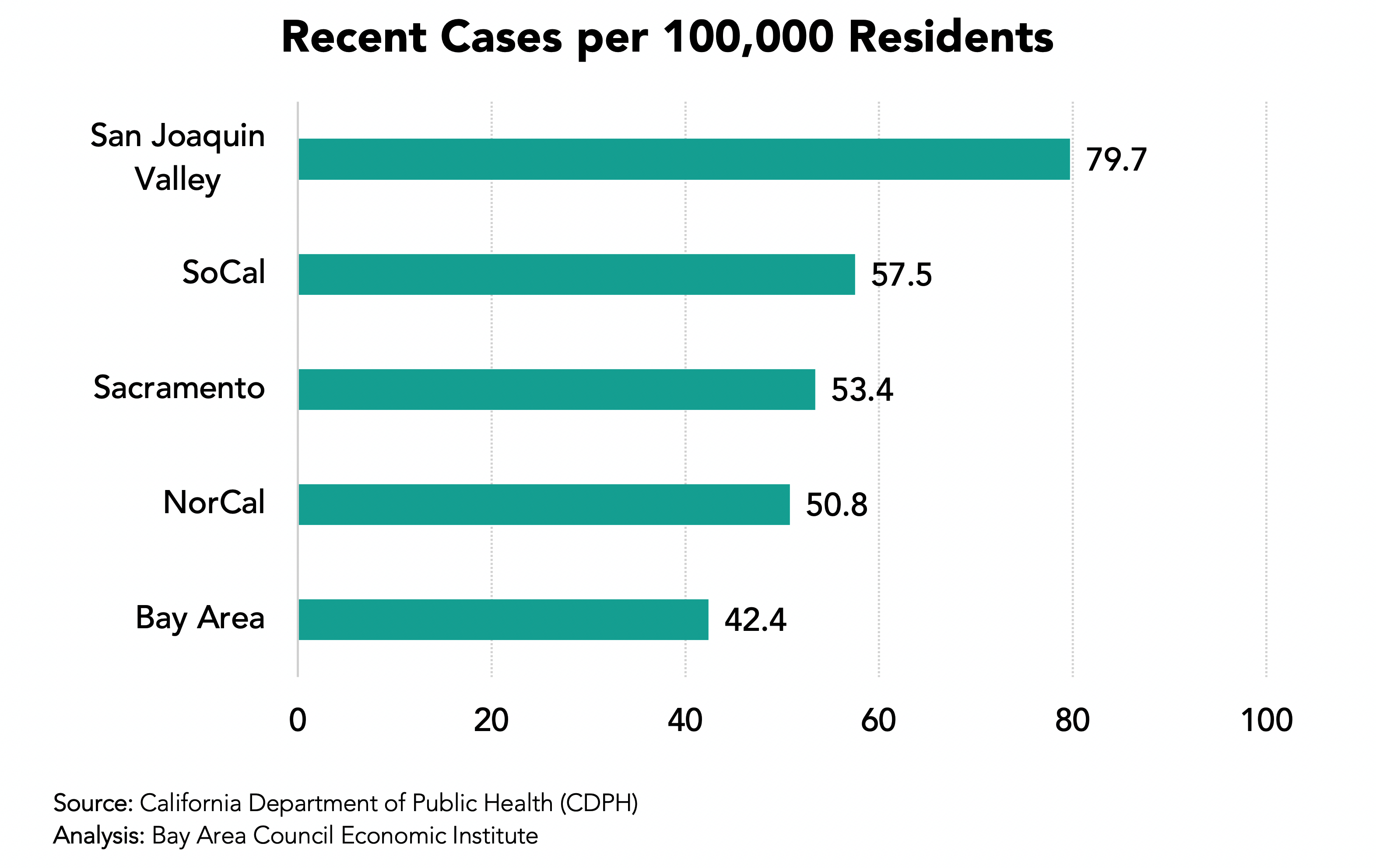

All regions in the state except the San Joaquin Valley outpaced the nation in job growth during the past 12 months led by the Southern California and the Bay Area followed by the Sacramento region.

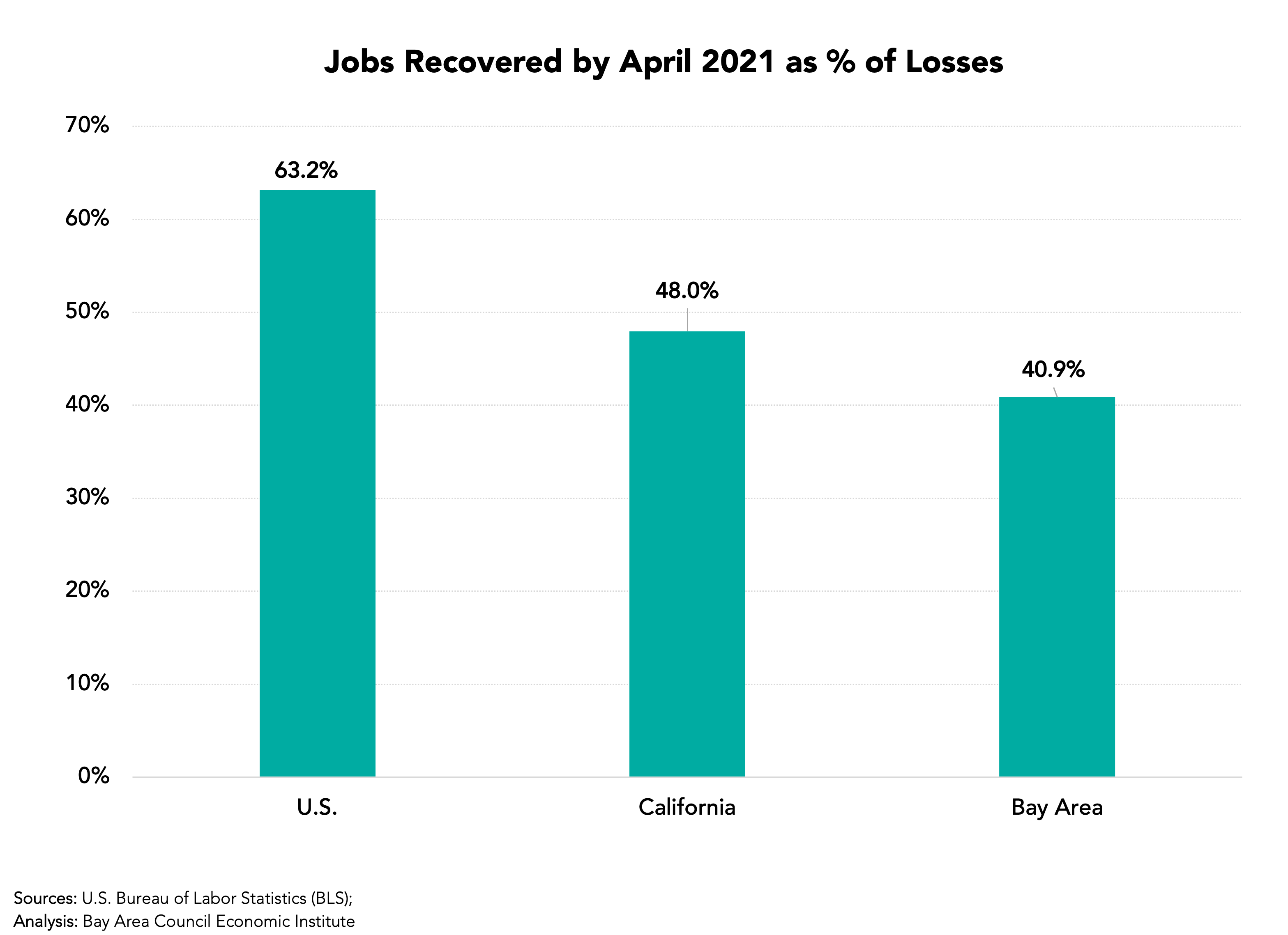

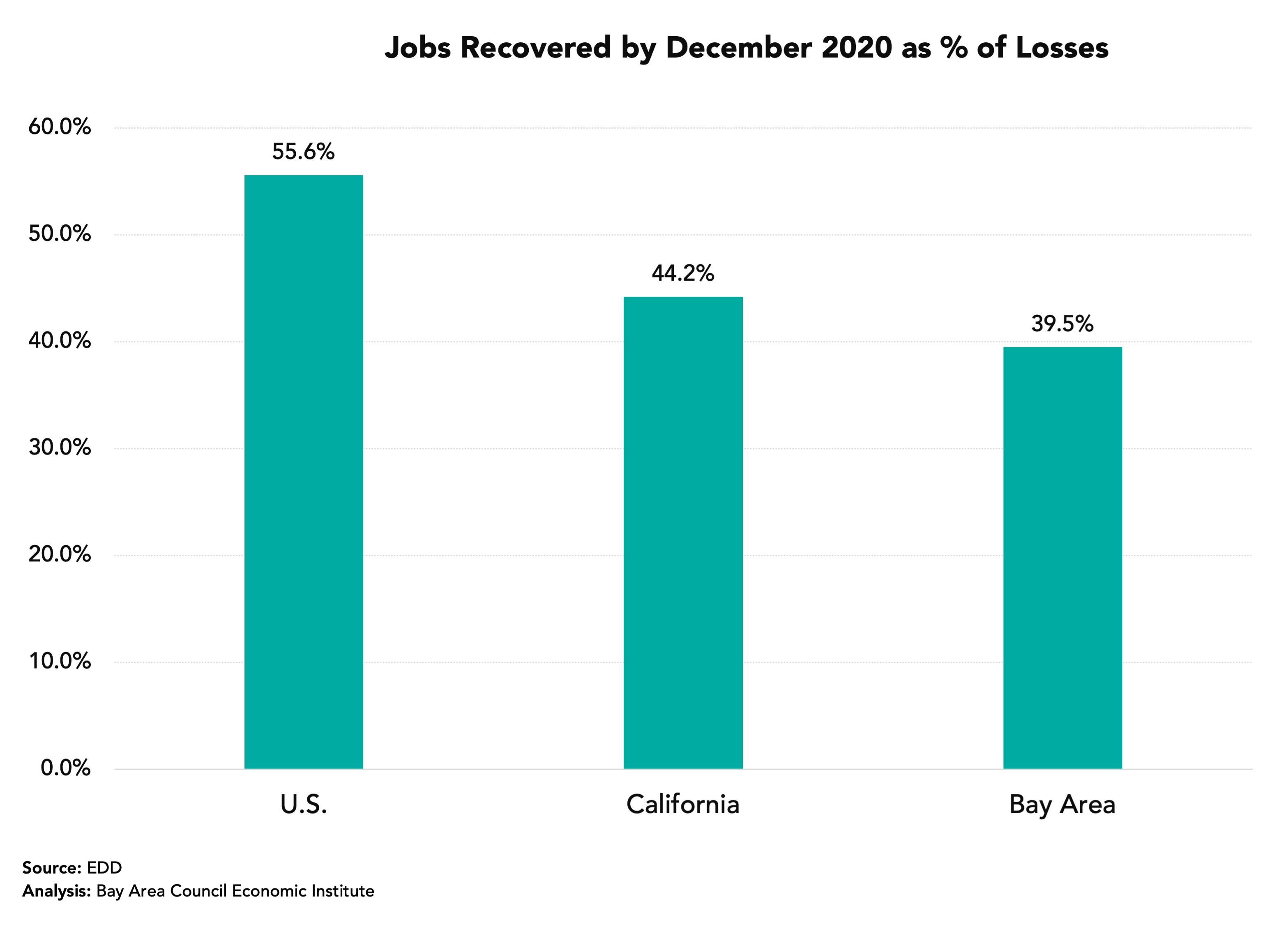

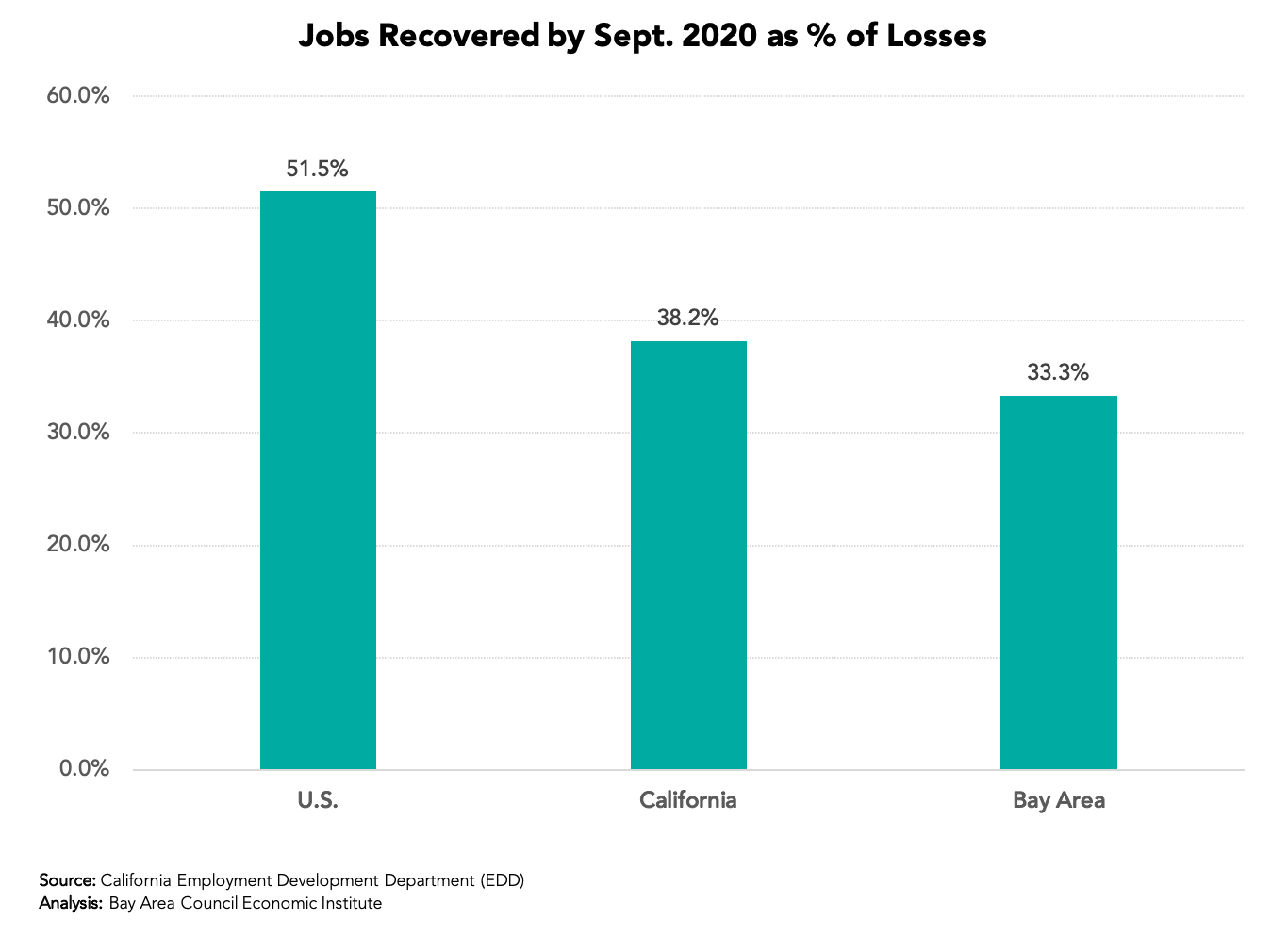

The chart below gets wide media attention and focuses on our region’s below-average job recovery rate. It is accurate and shows the better U.S. and California data. But look at the chart above to see the Bay Area catching up.

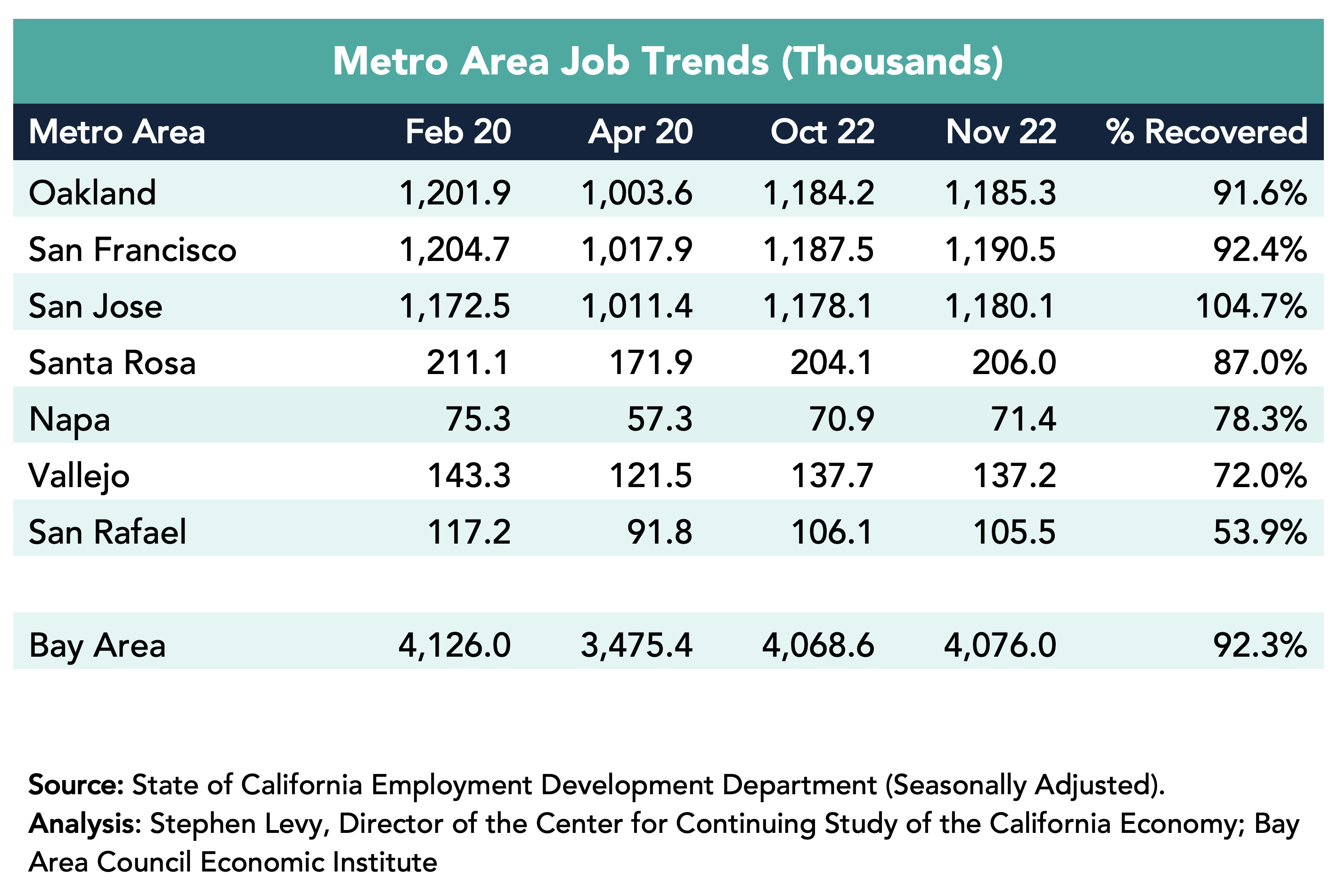

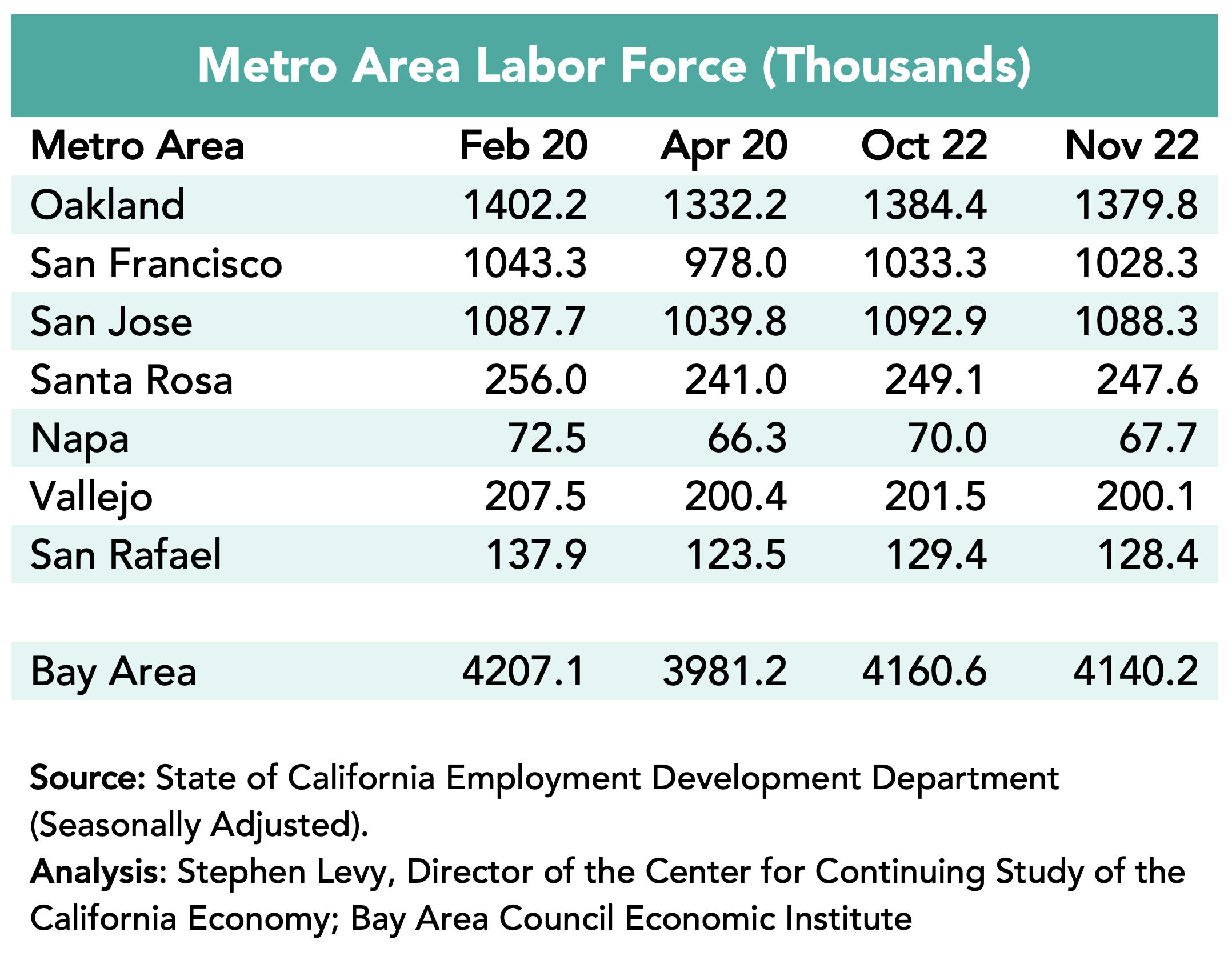

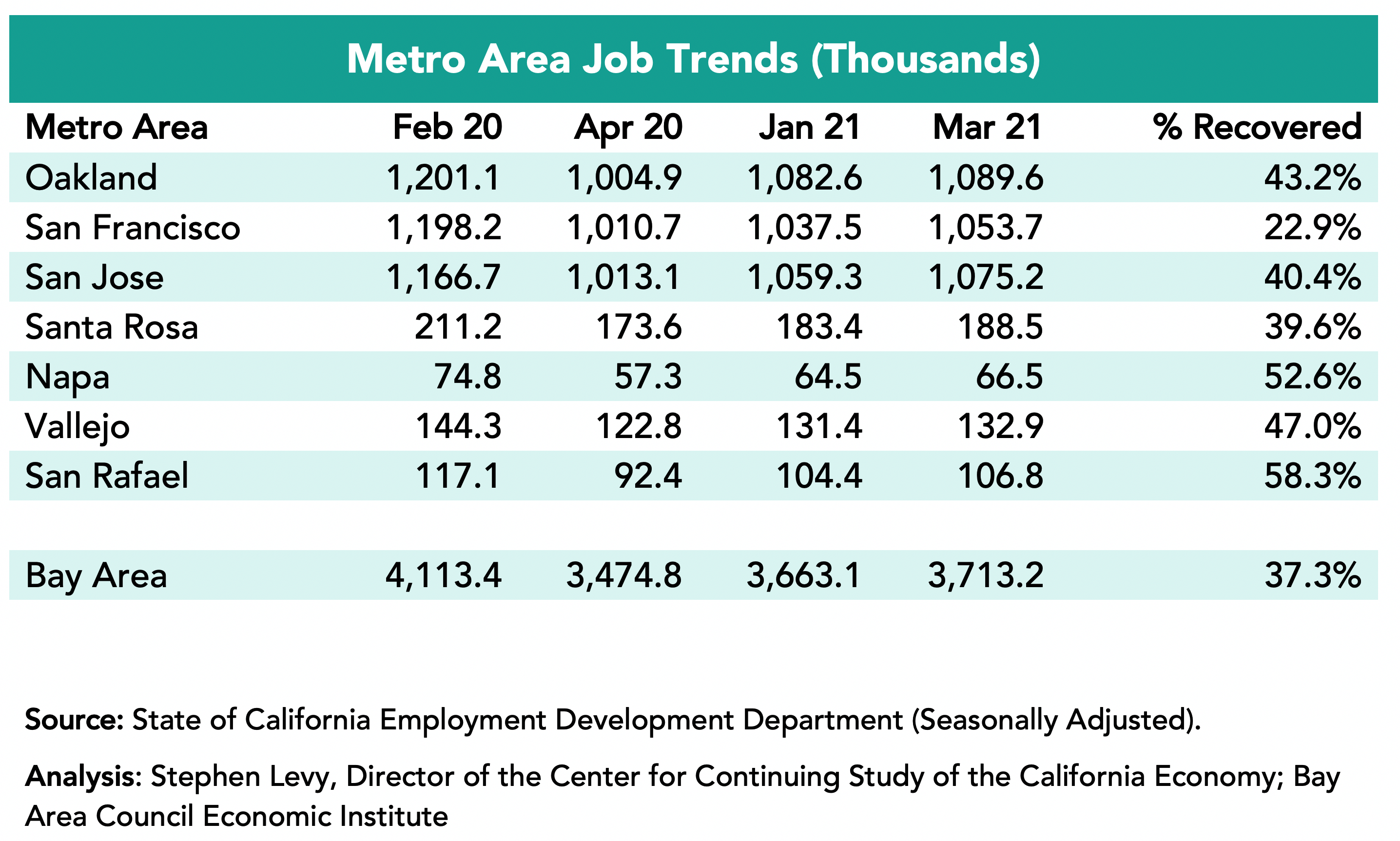

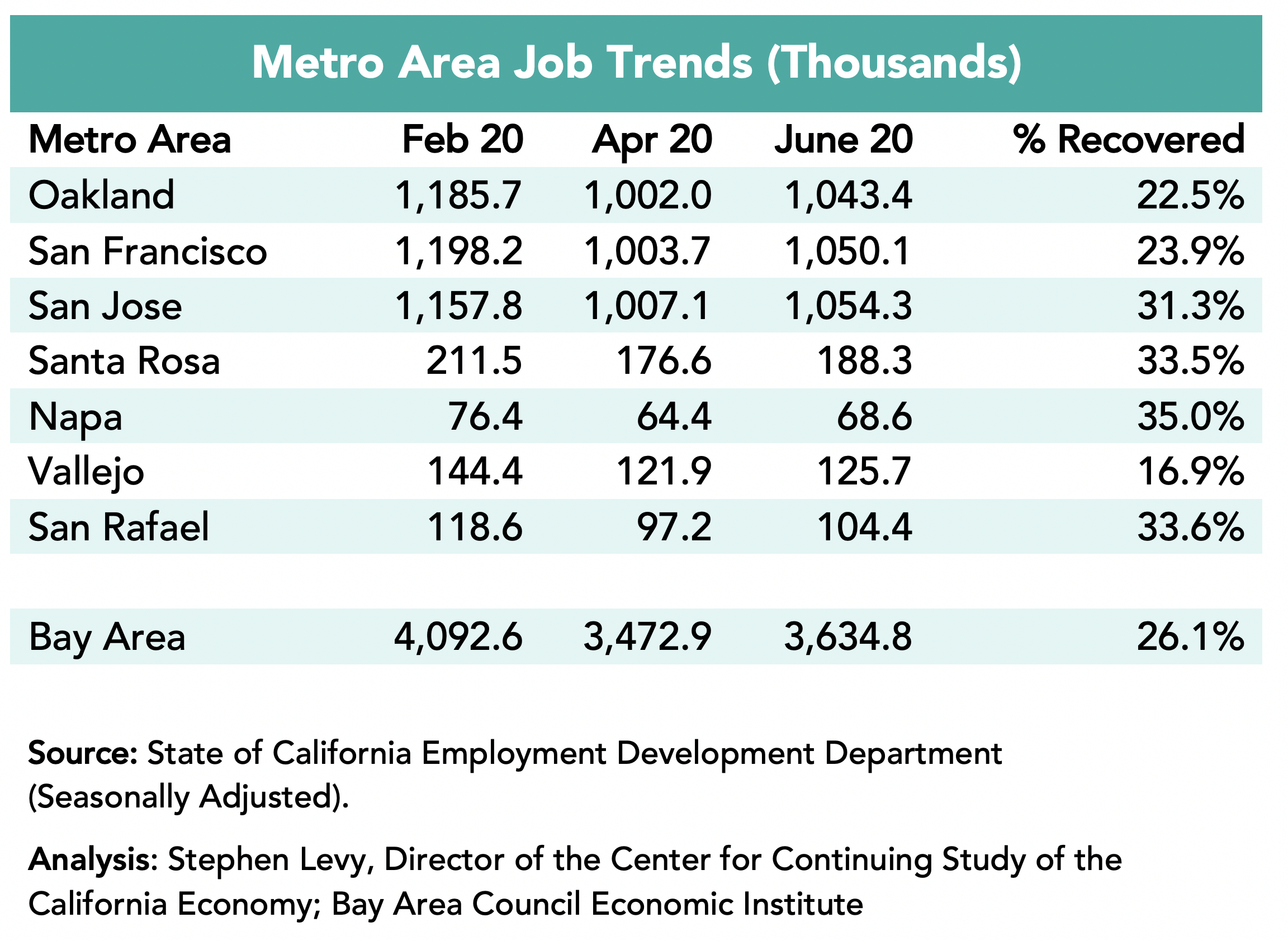

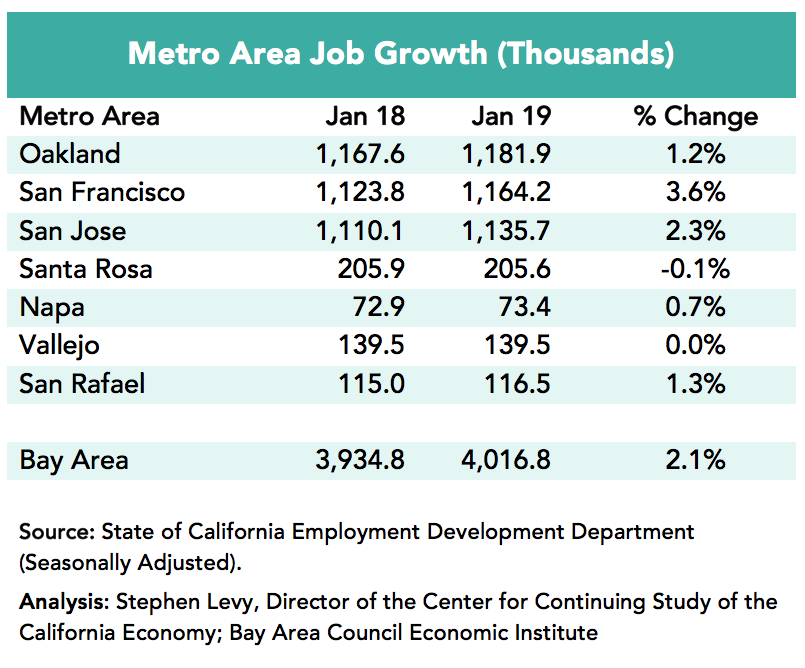

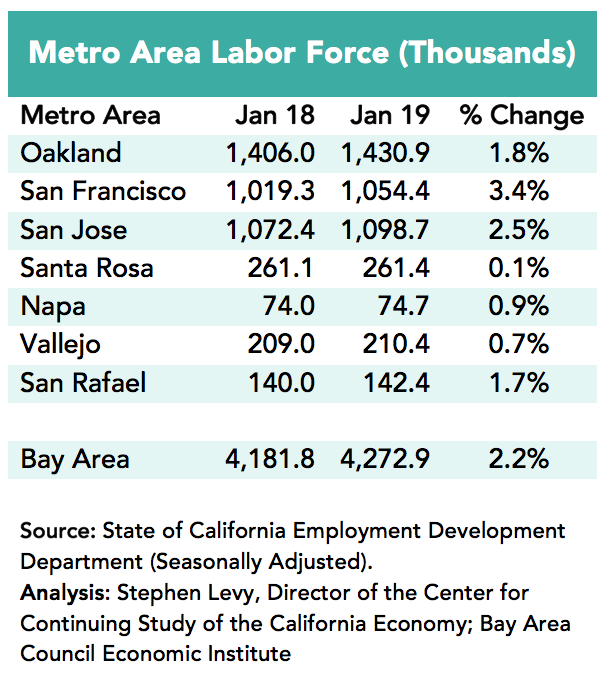

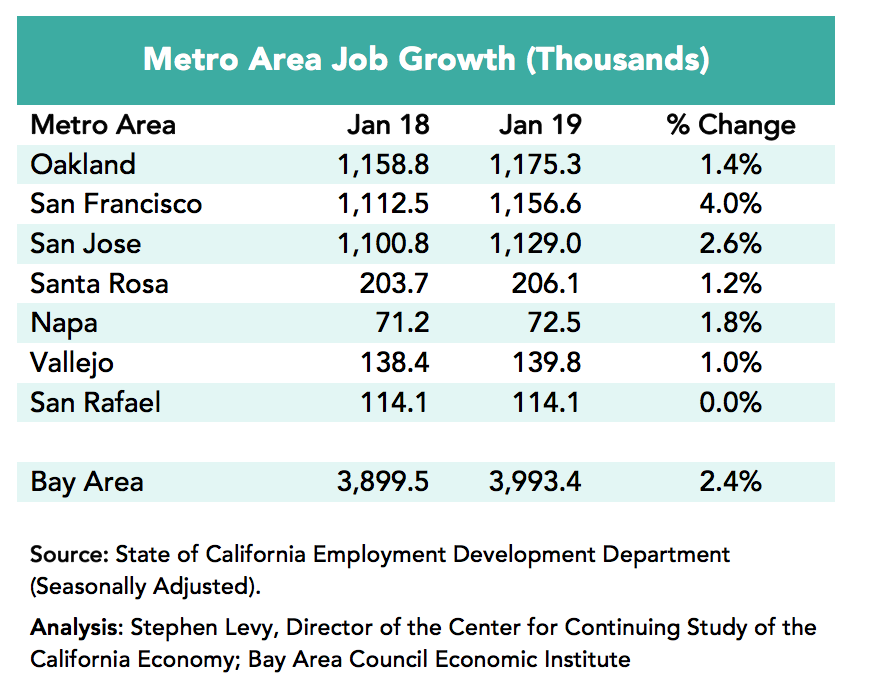

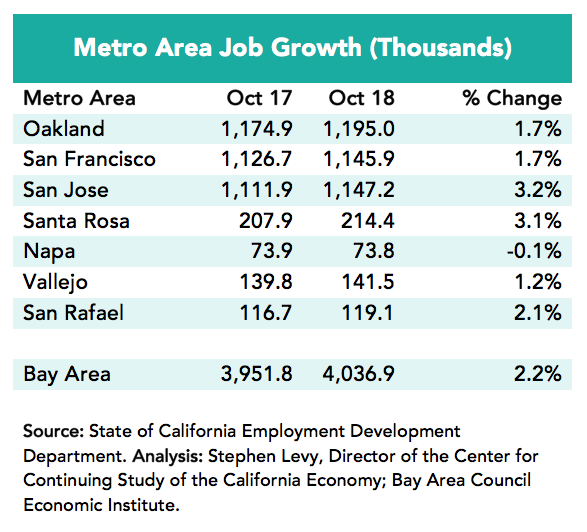

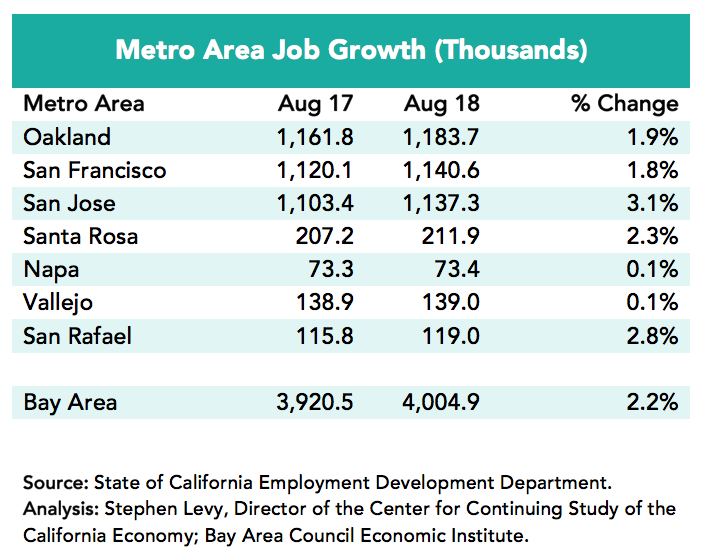

Payroll Job Growth Shows the San Jose Metro Area Leads the Region

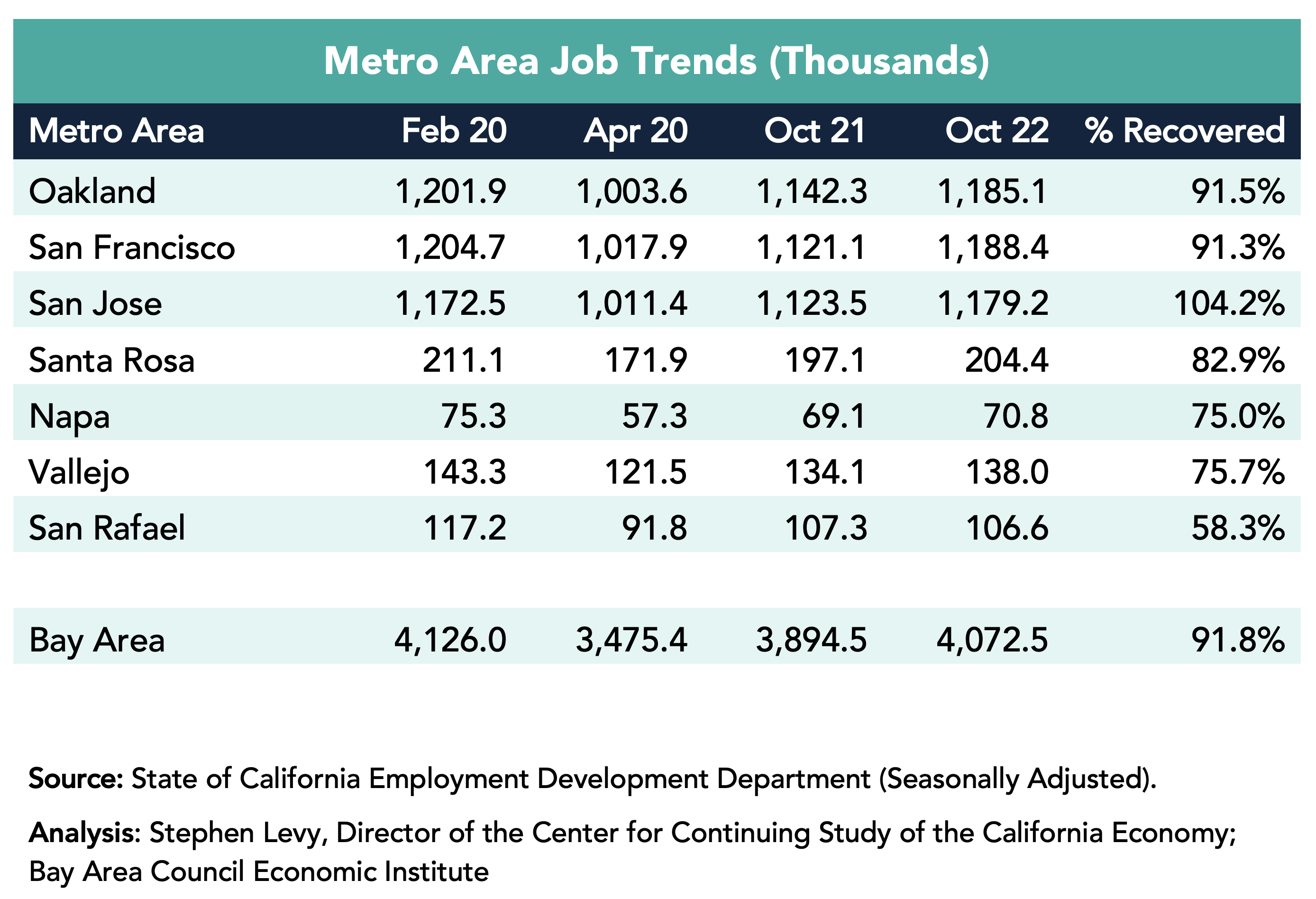

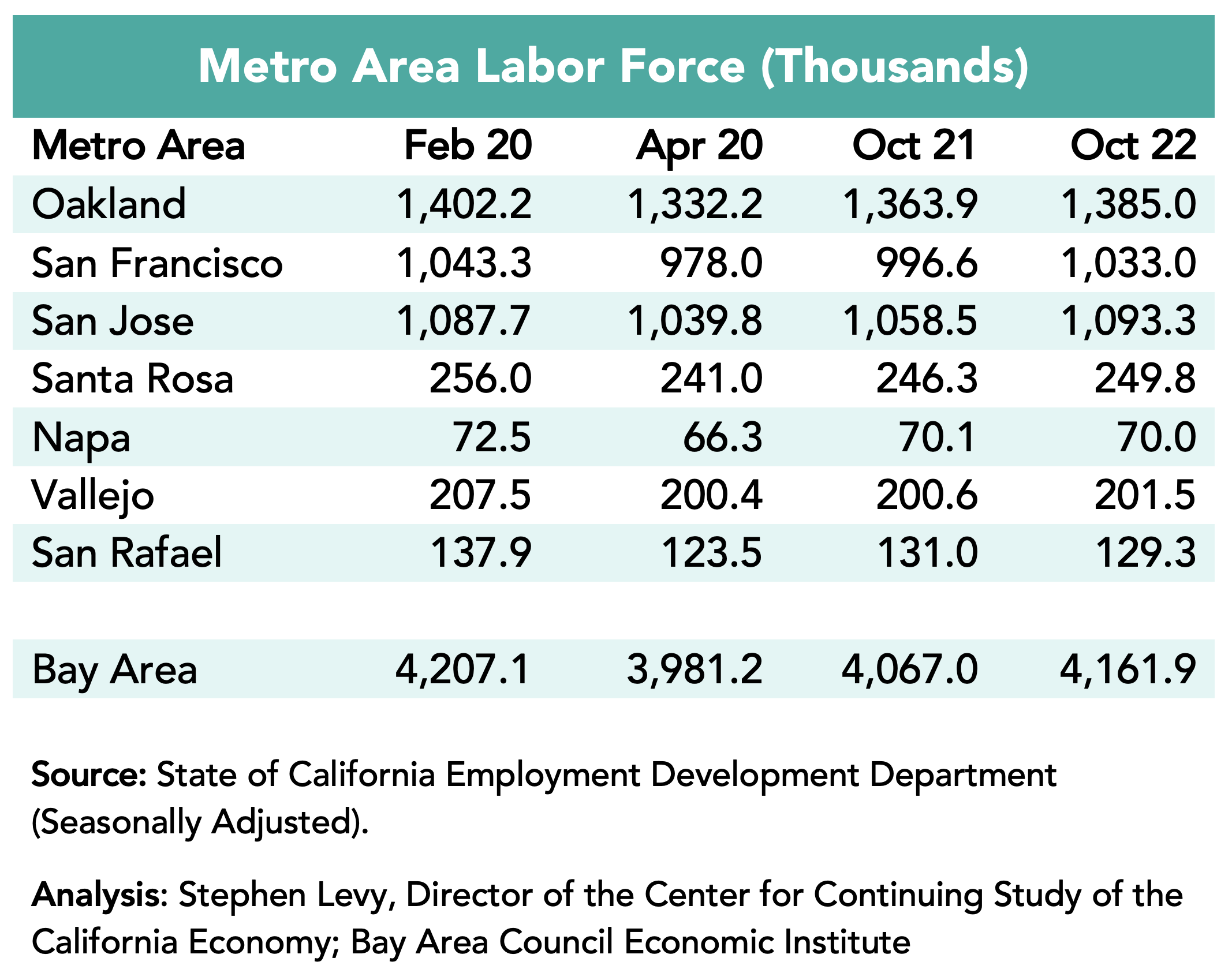

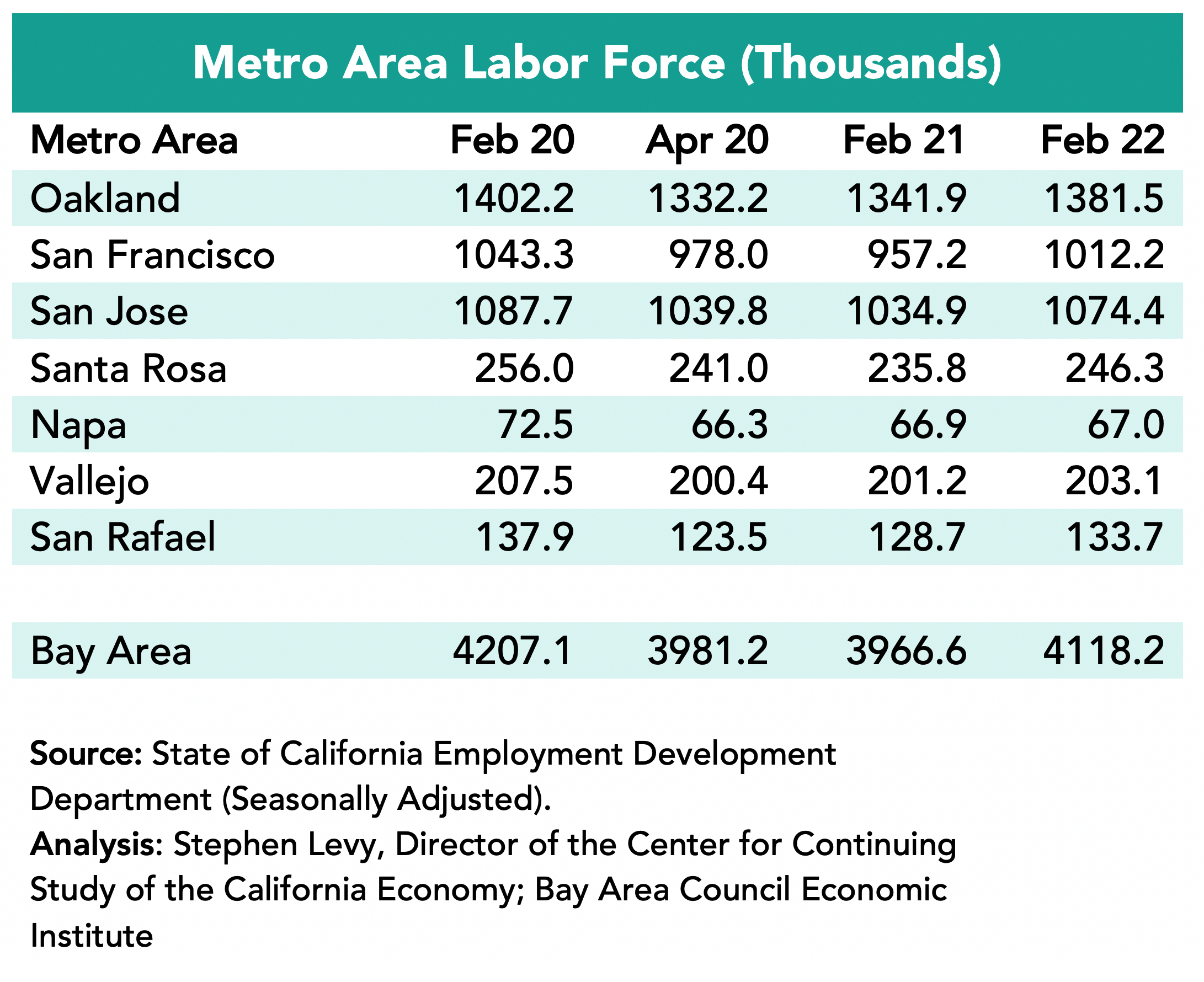

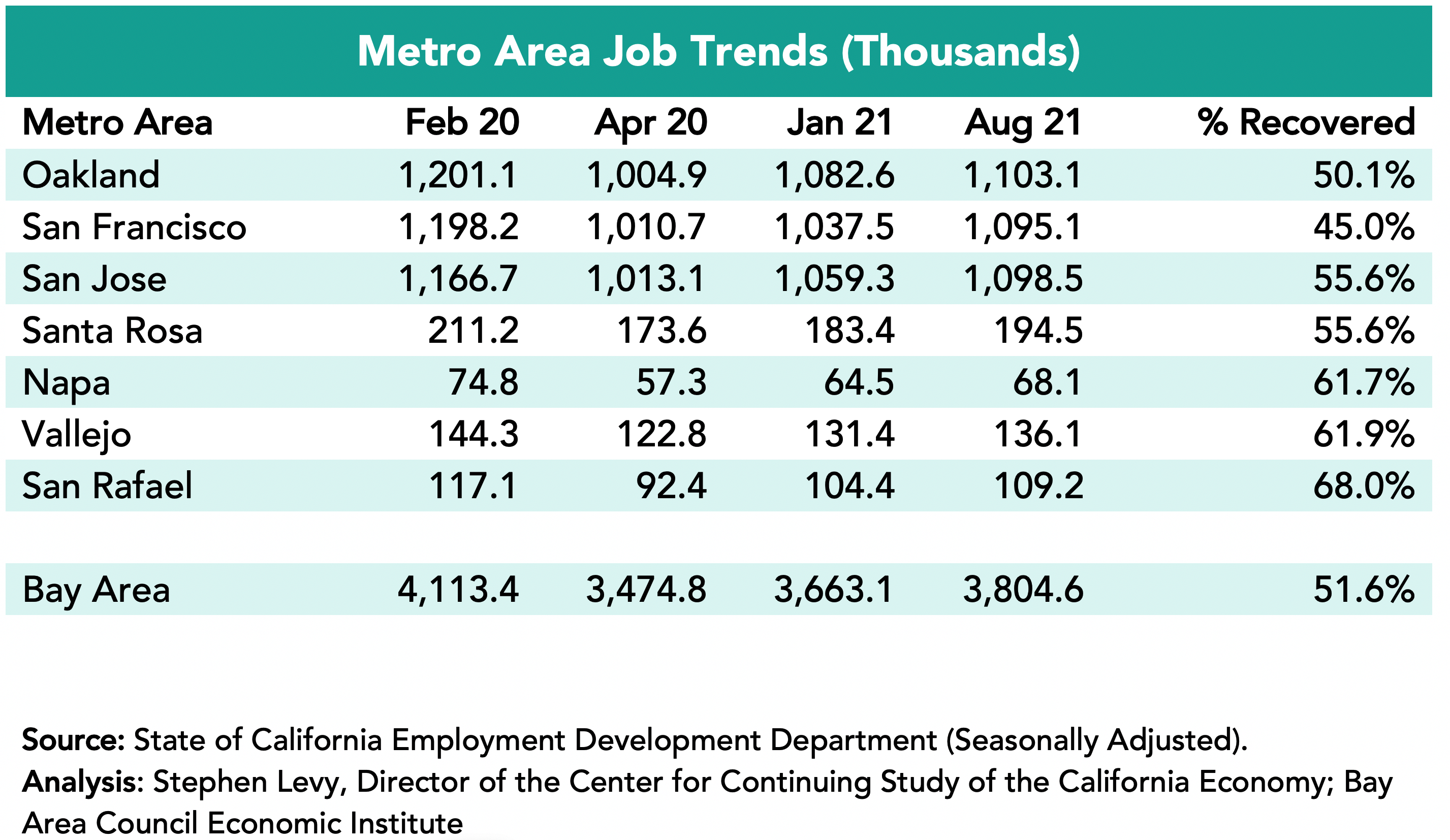

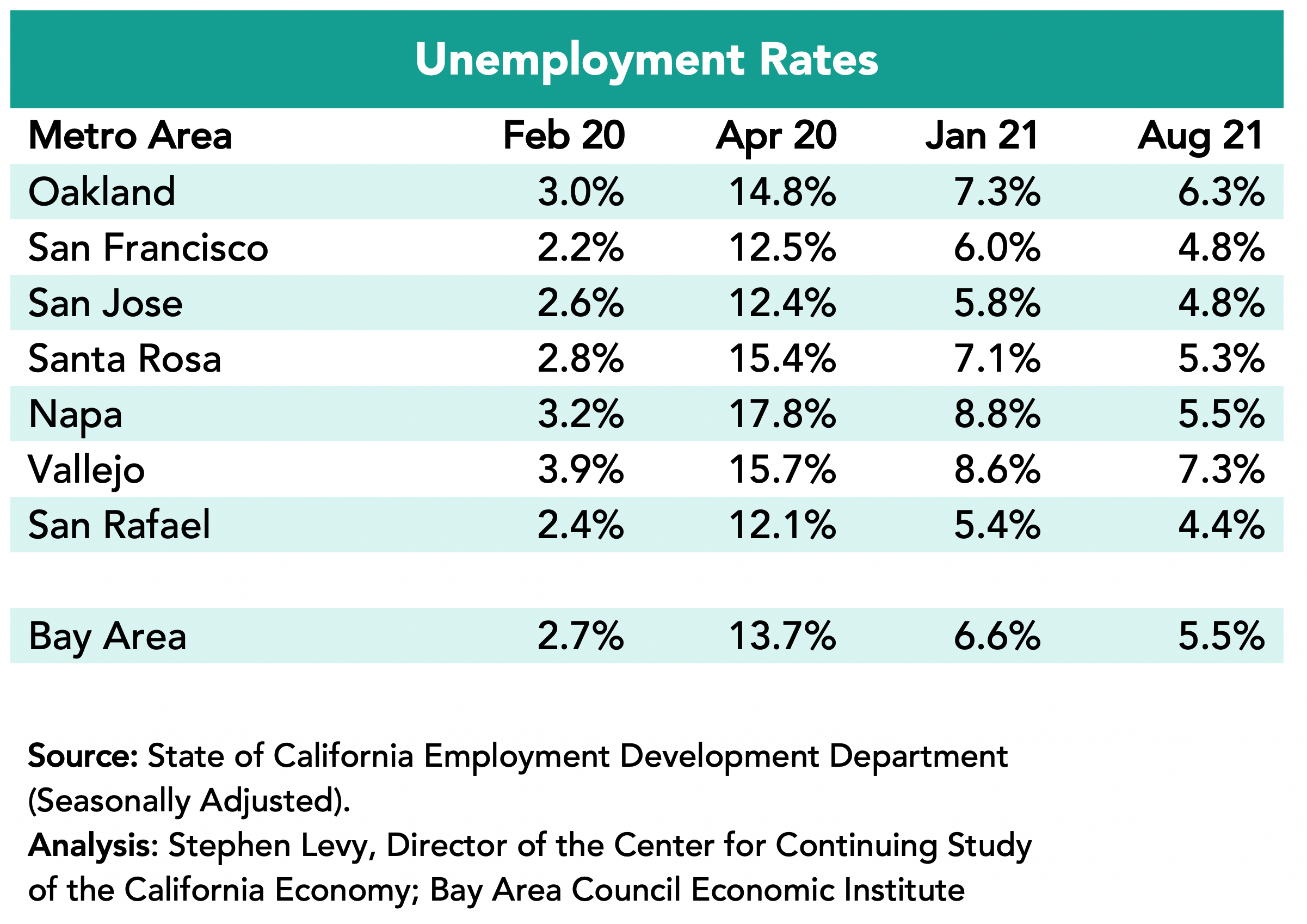

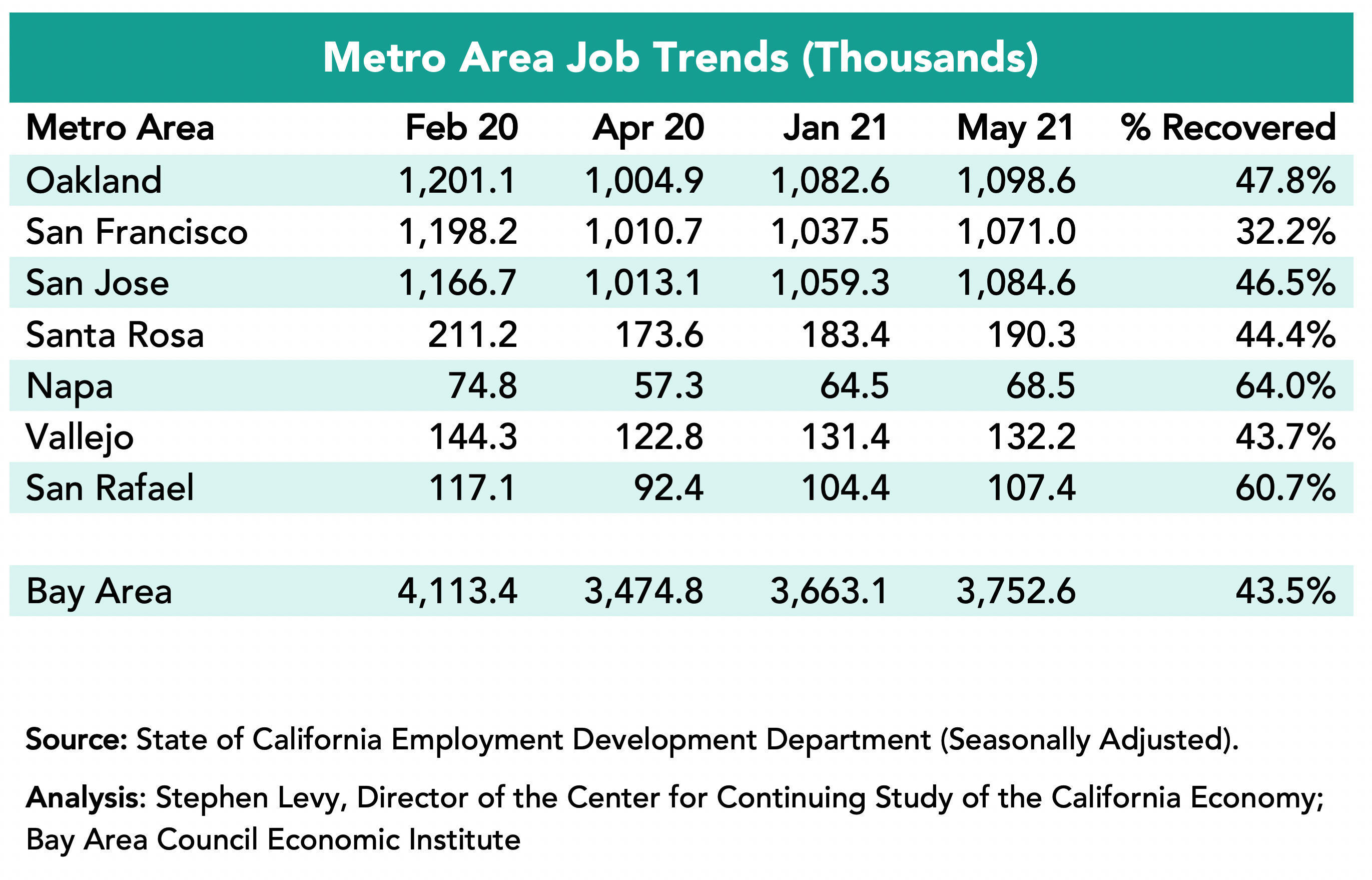

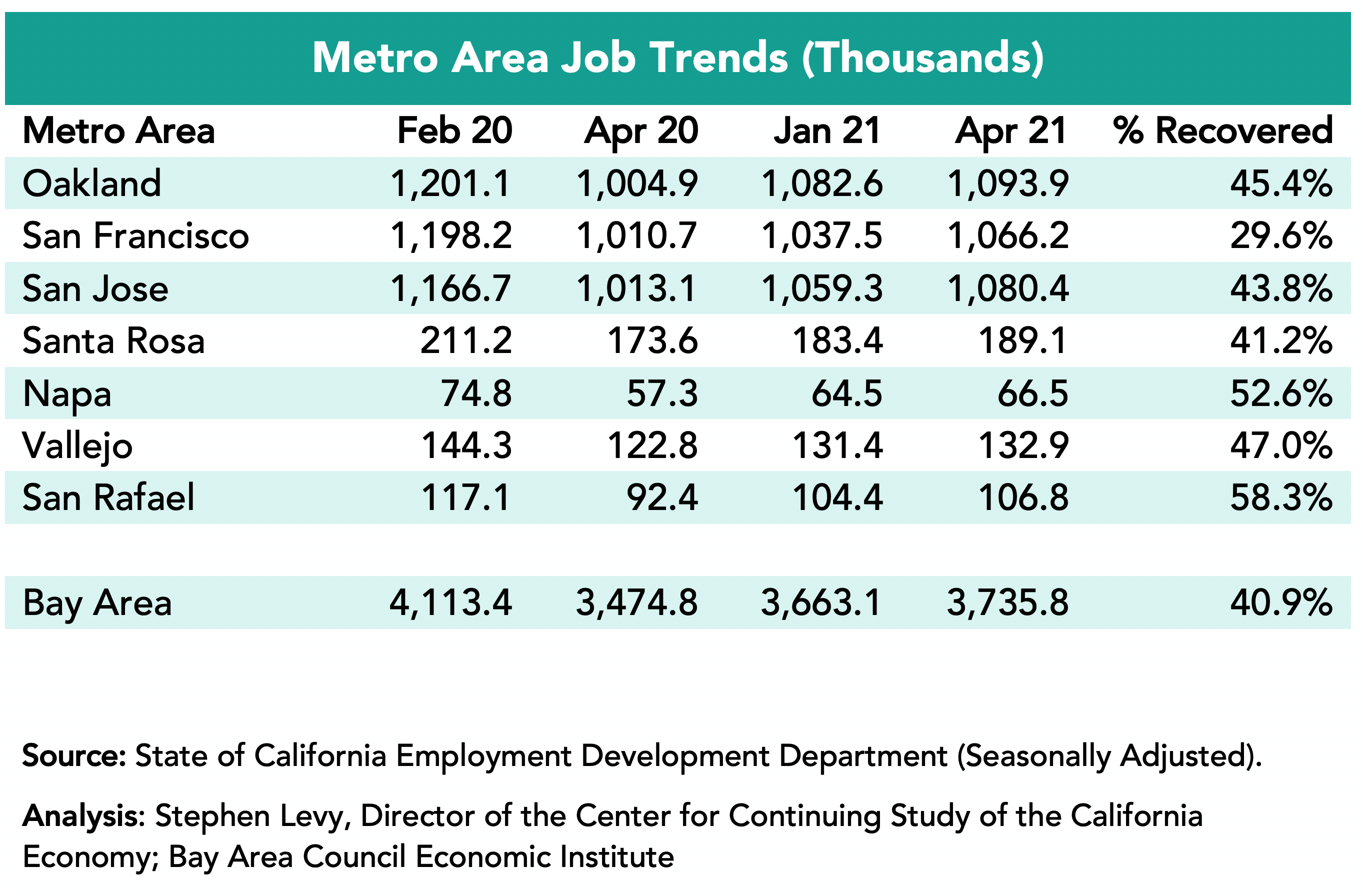

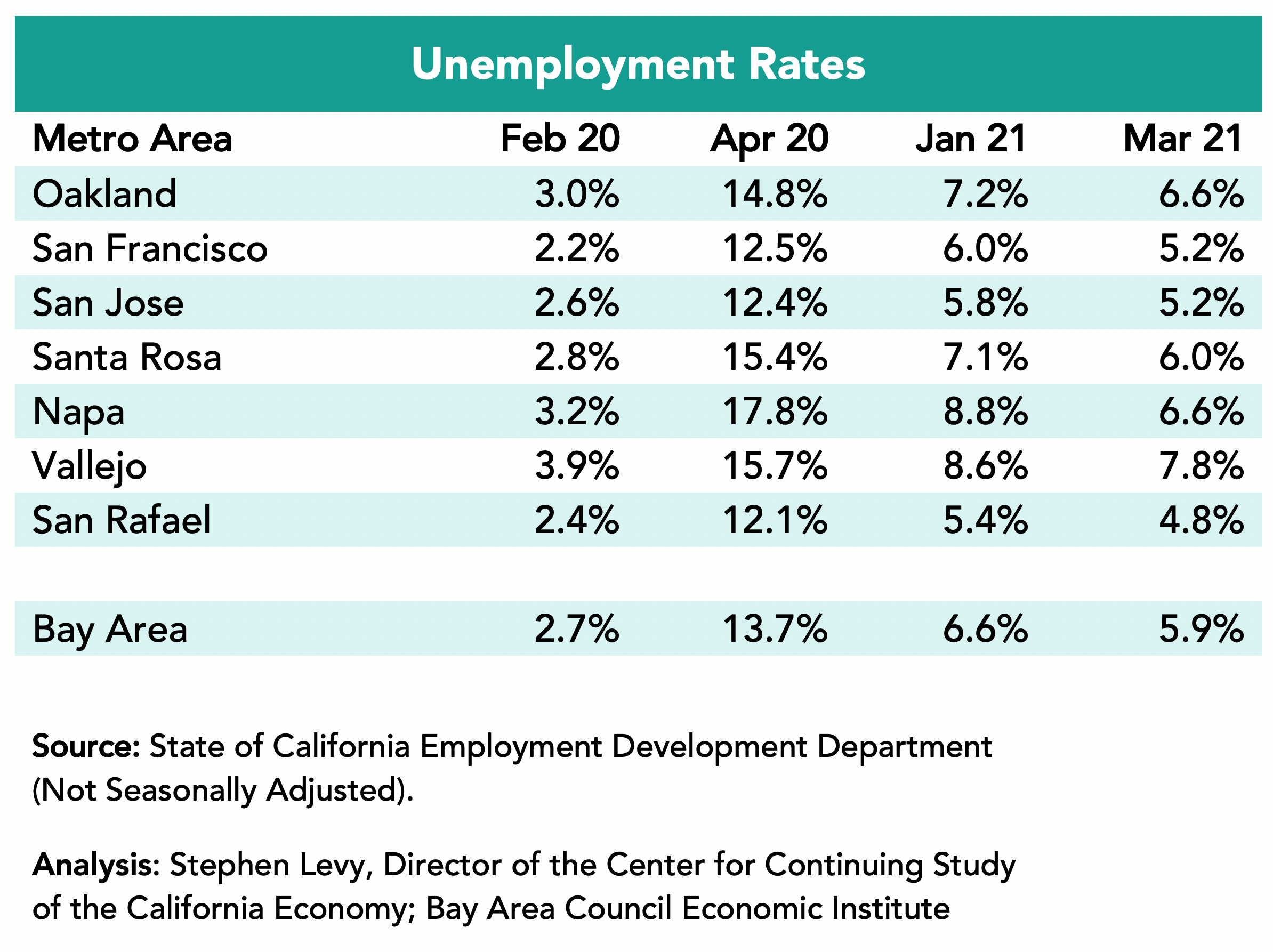

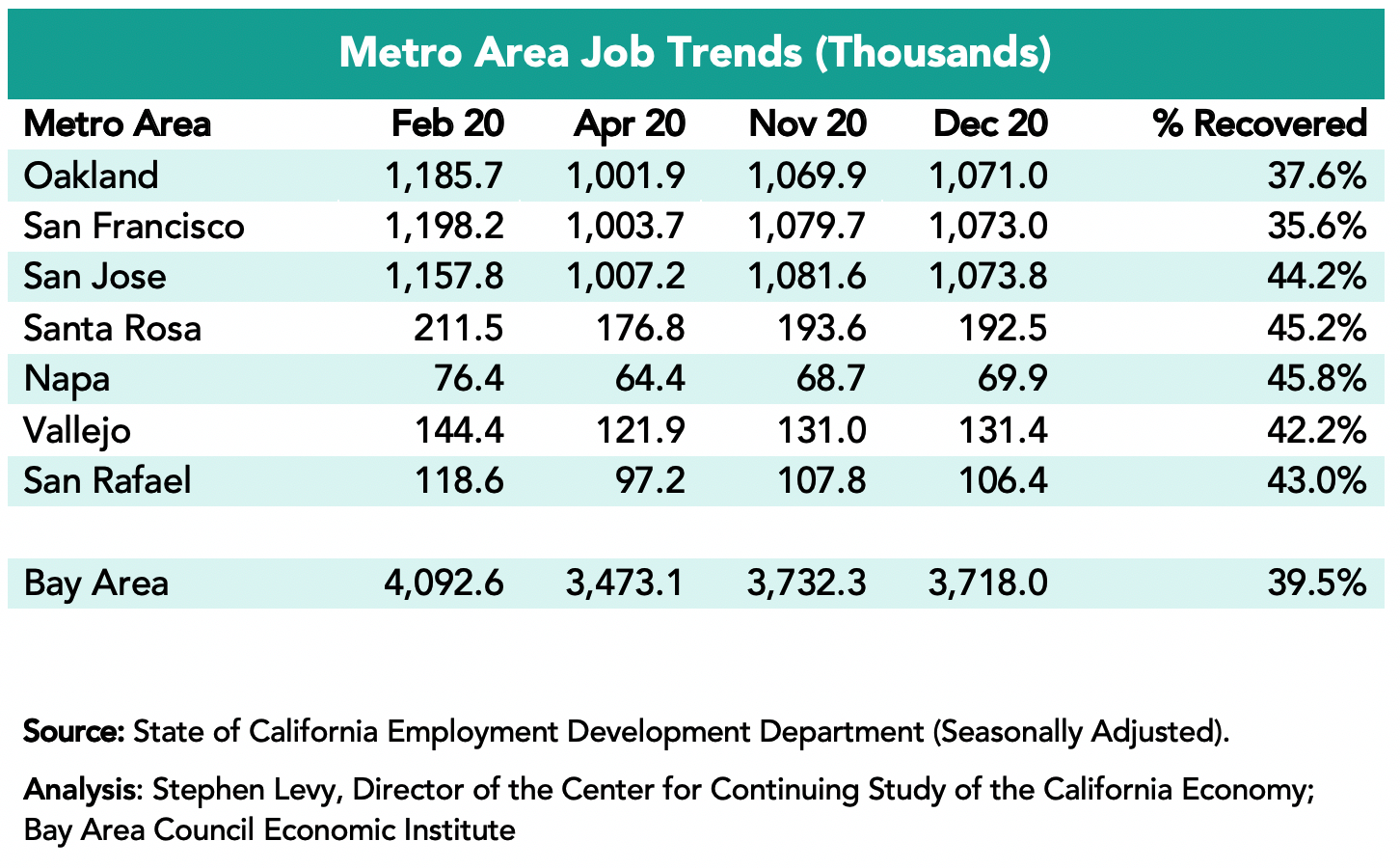

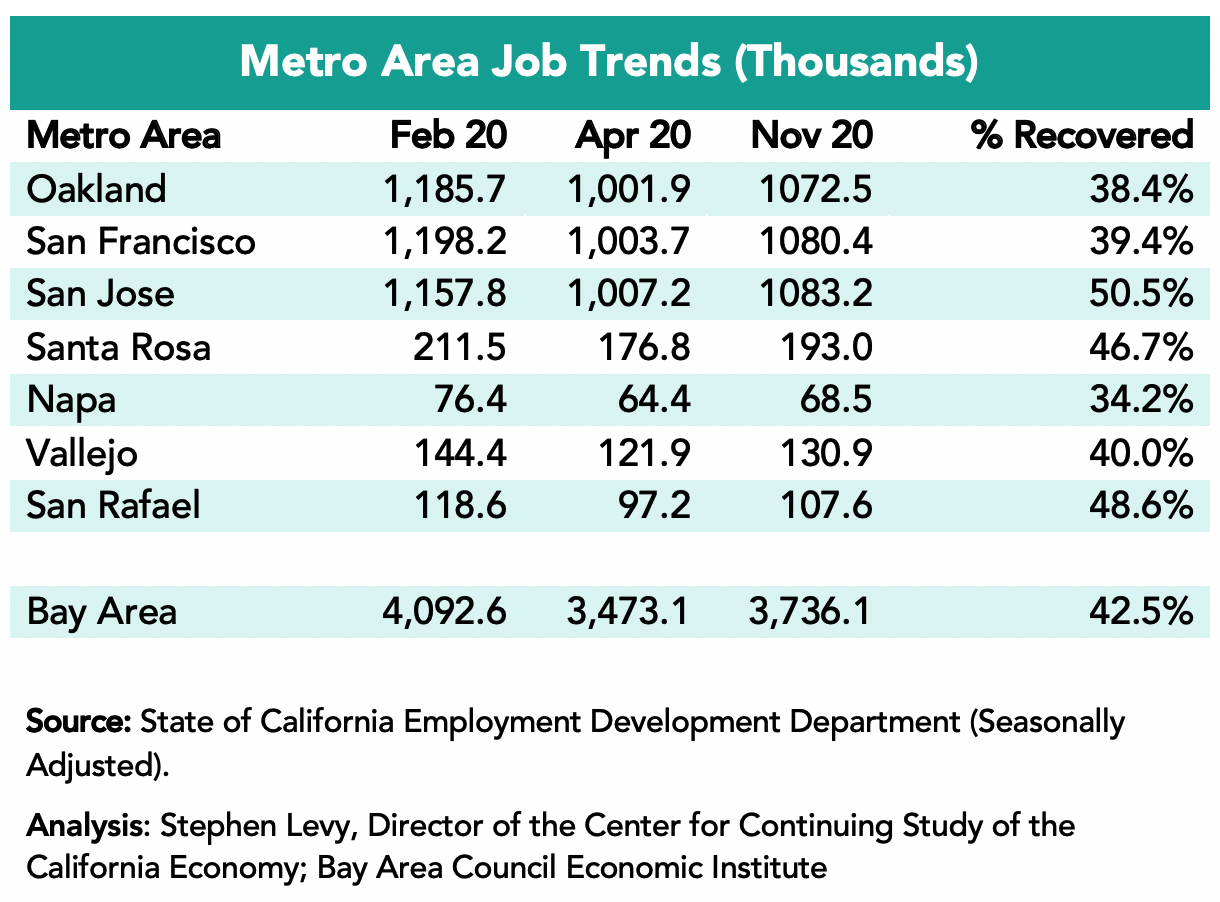

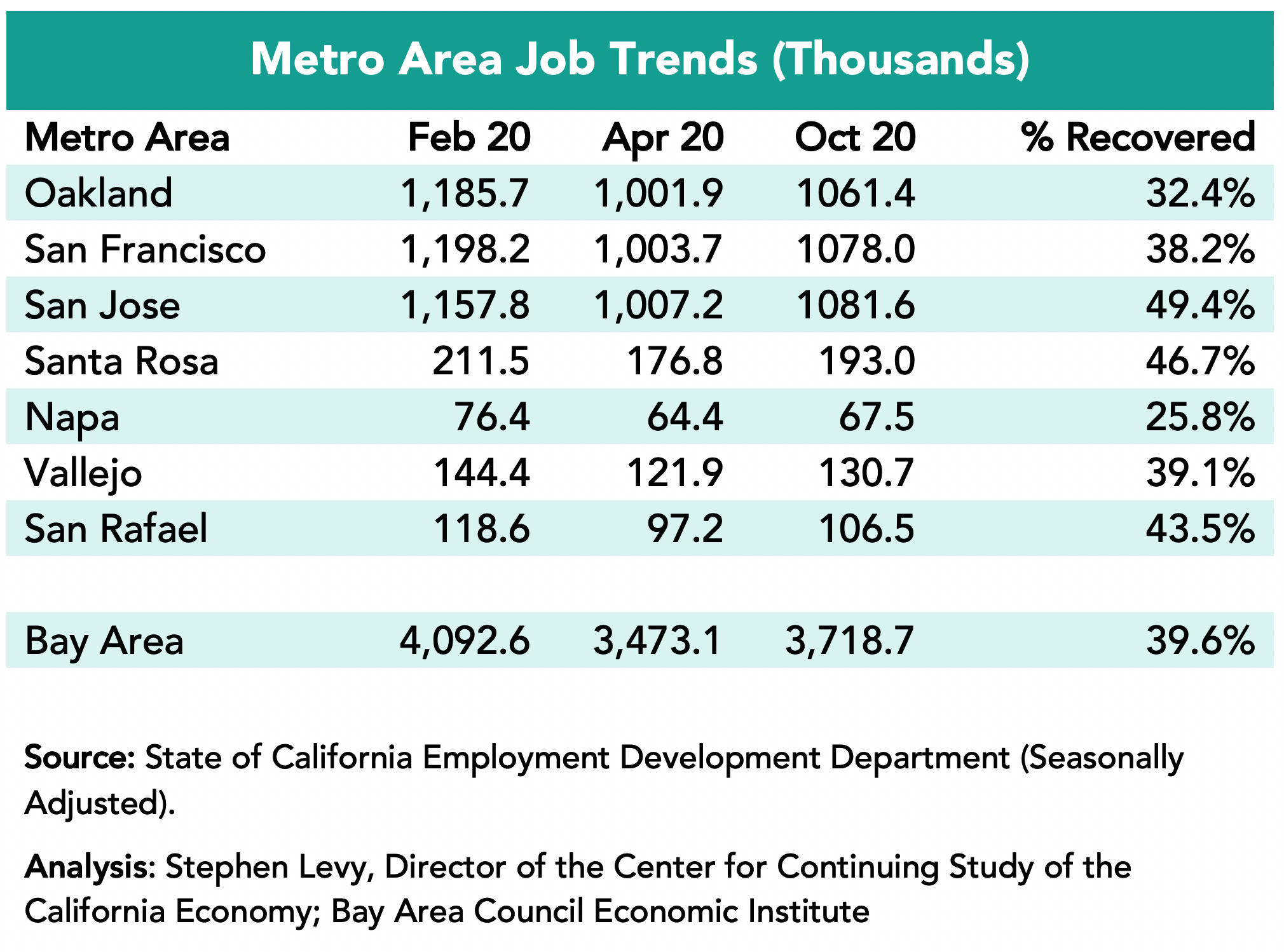

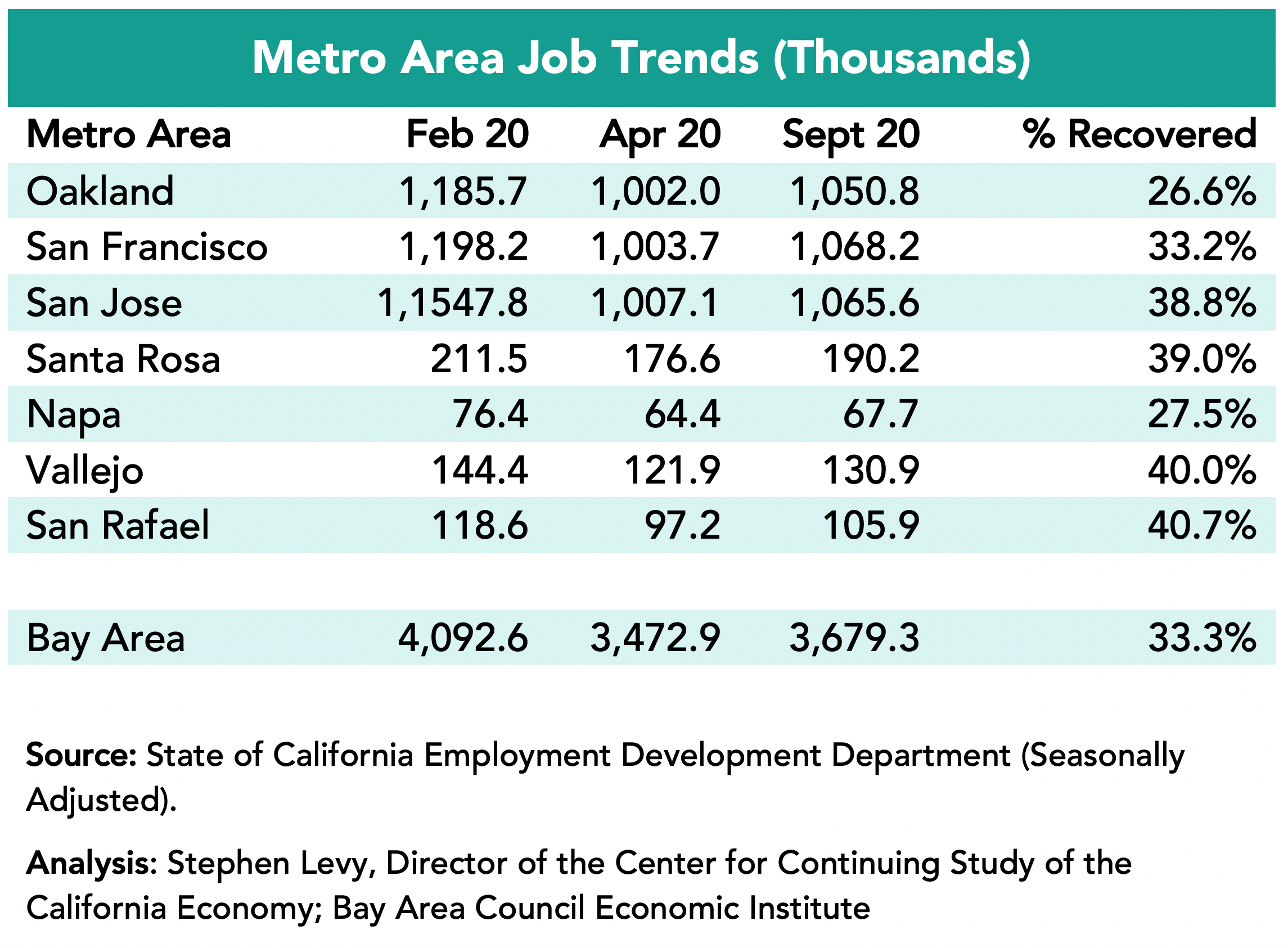

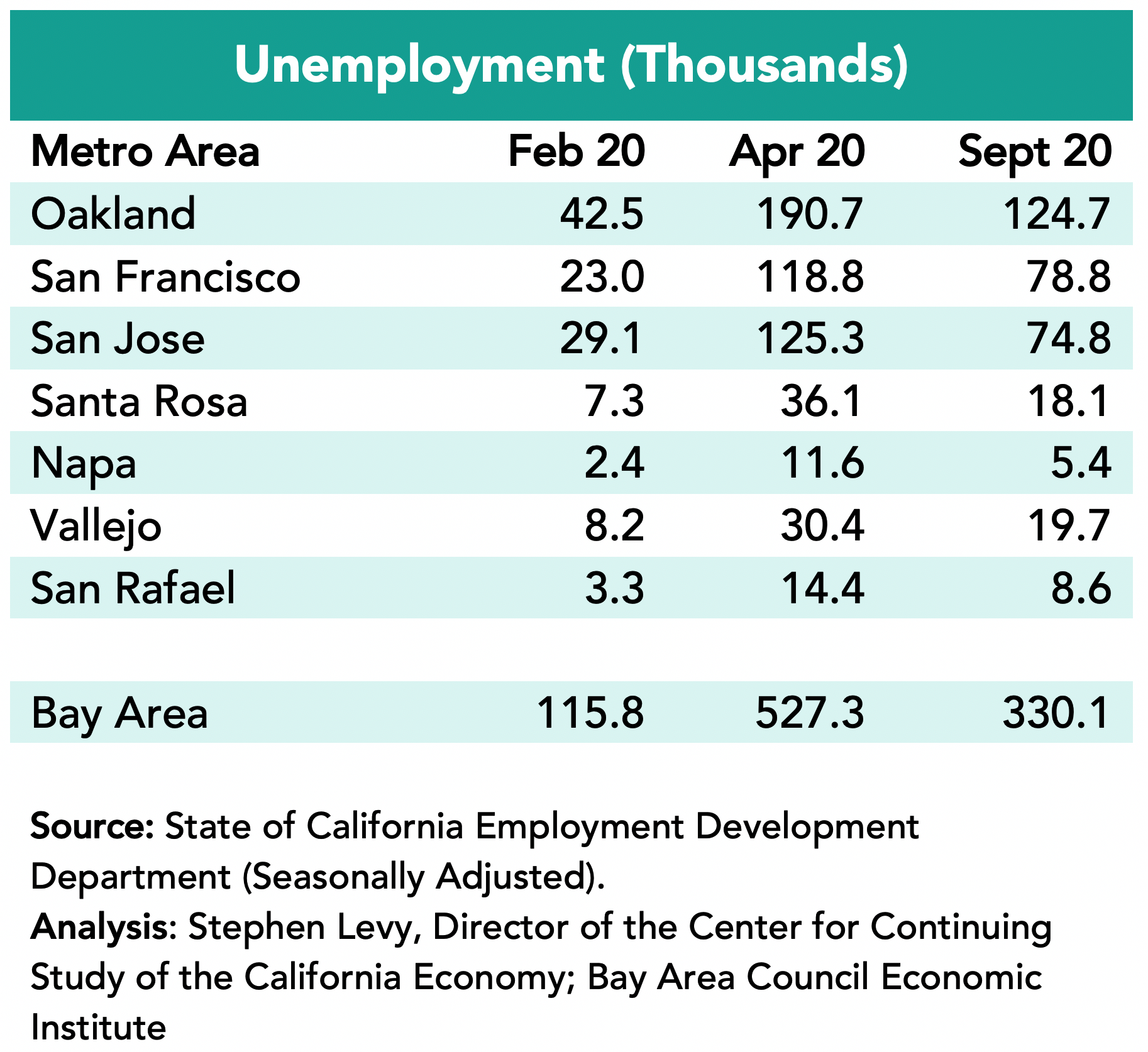

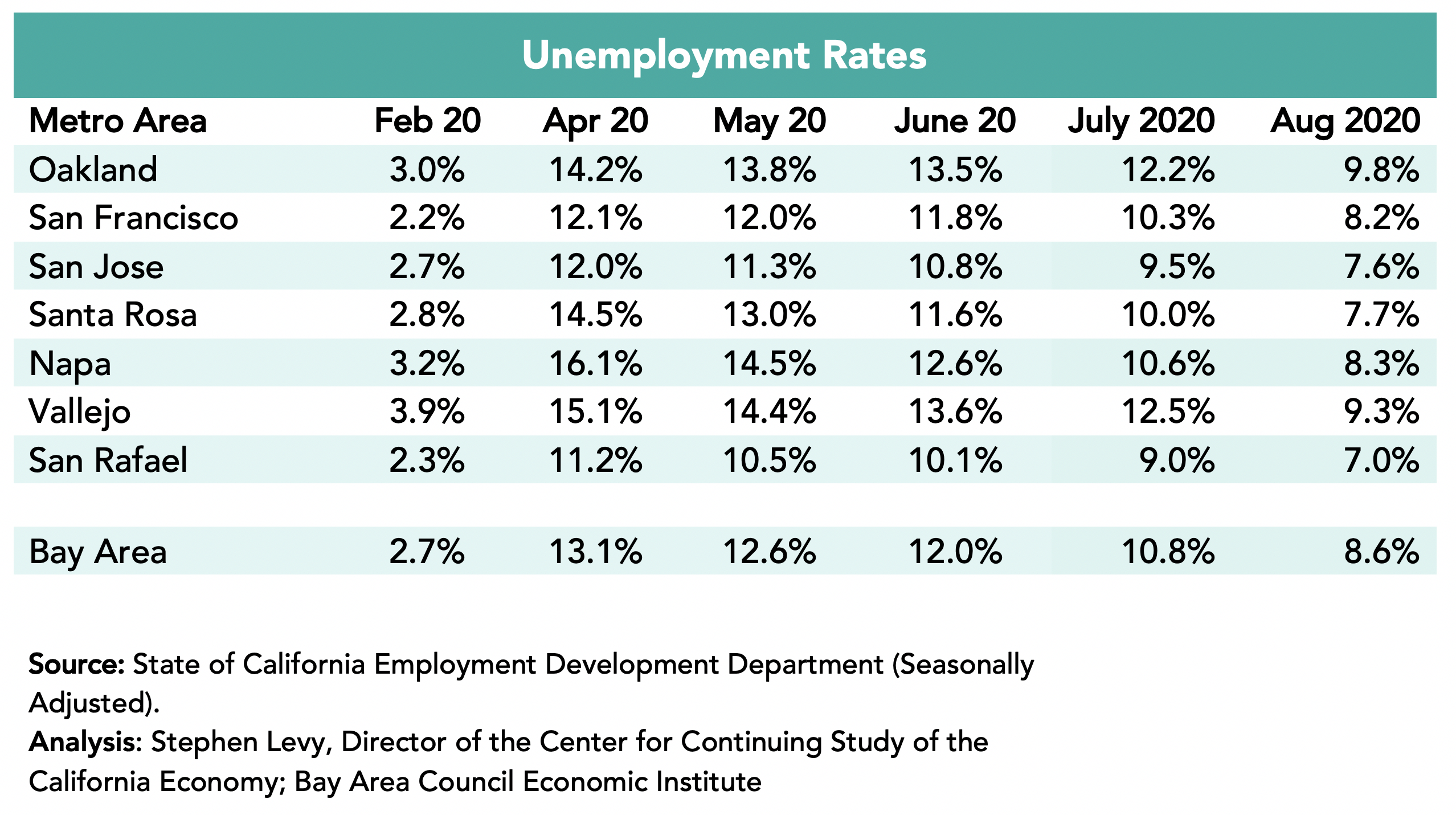

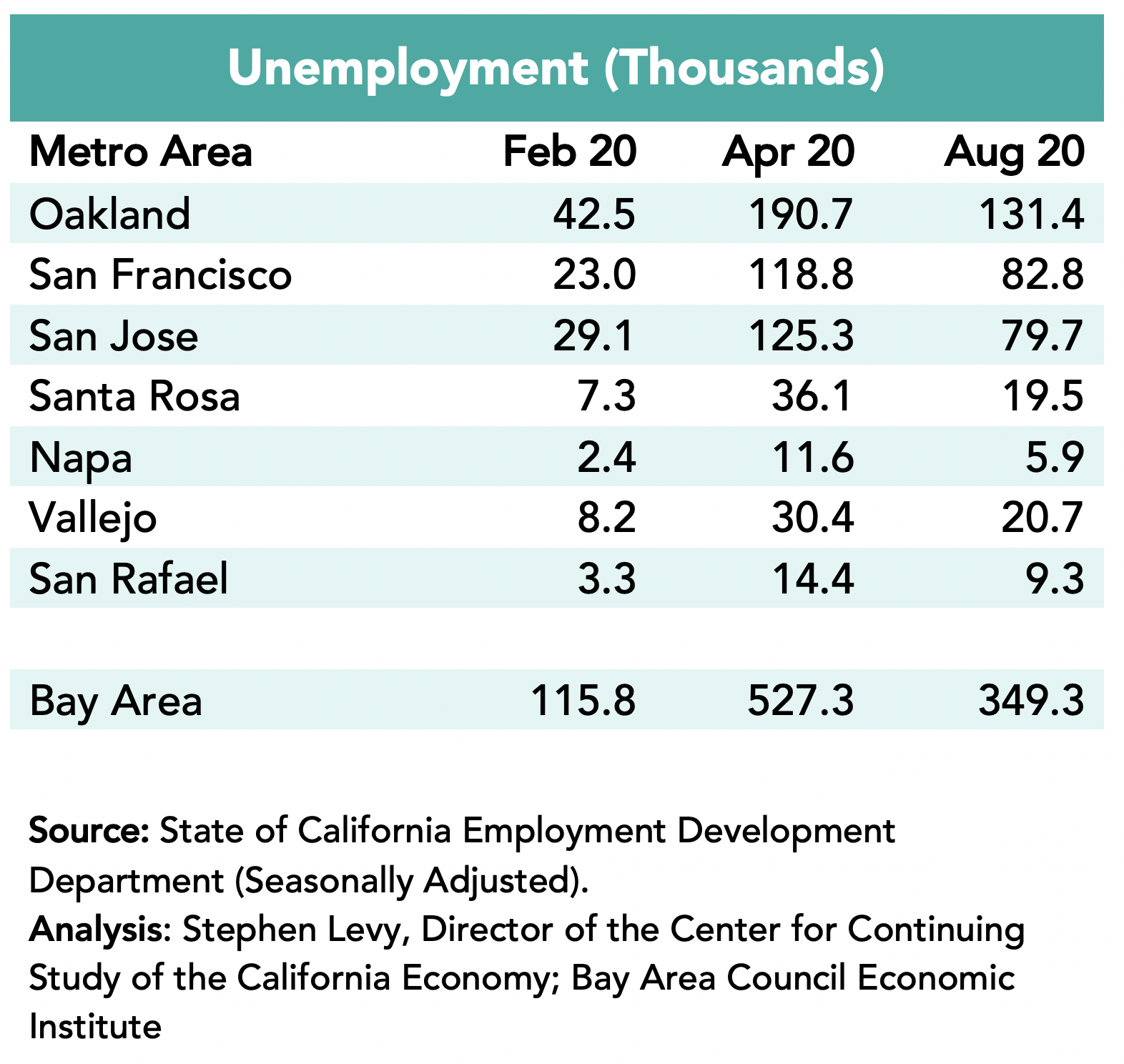

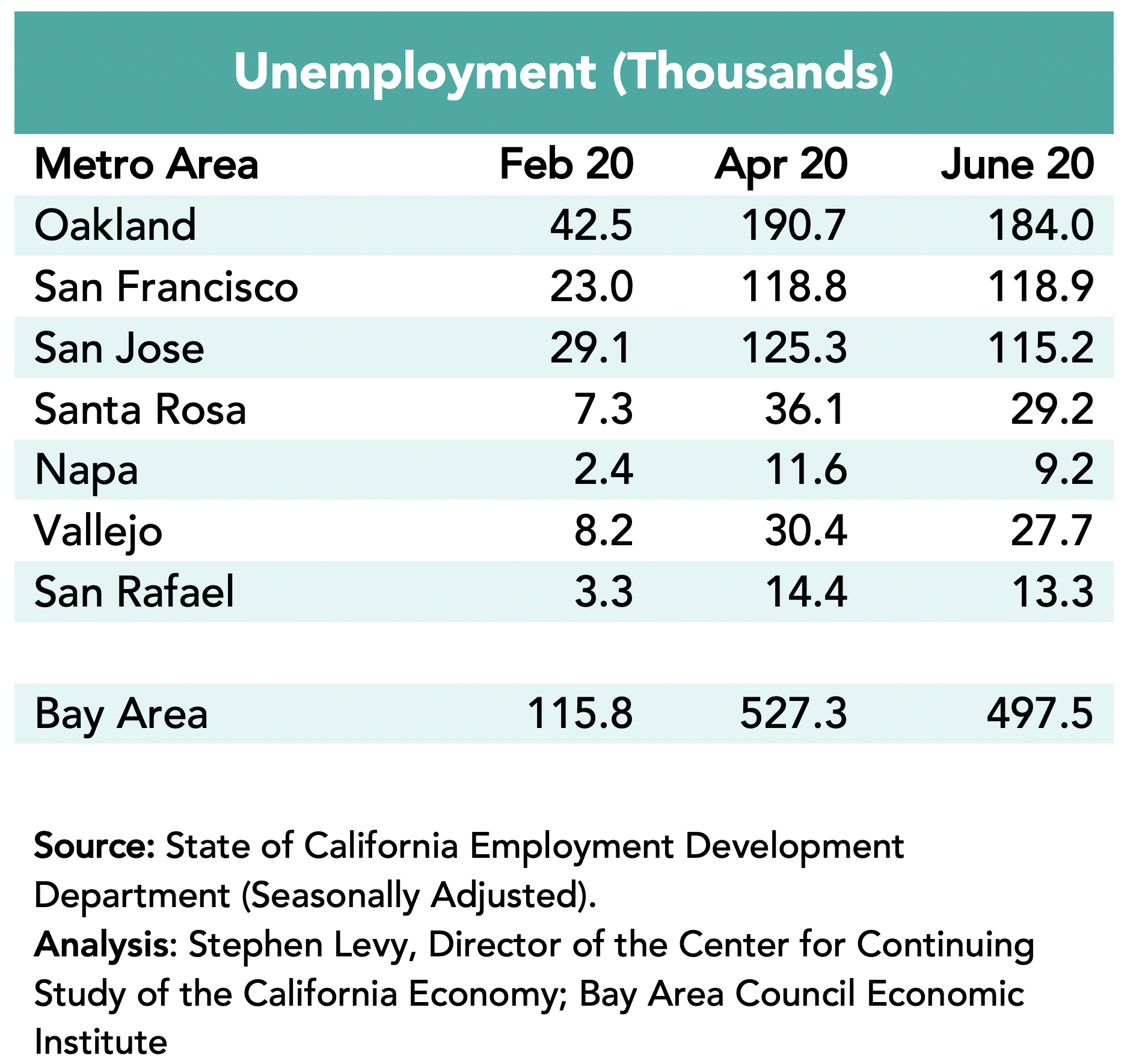

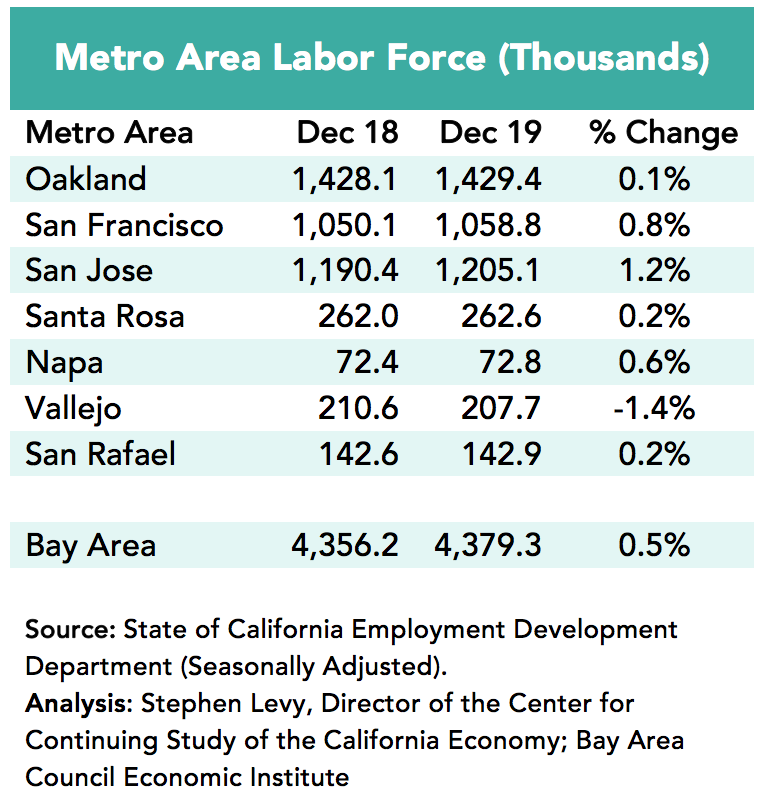

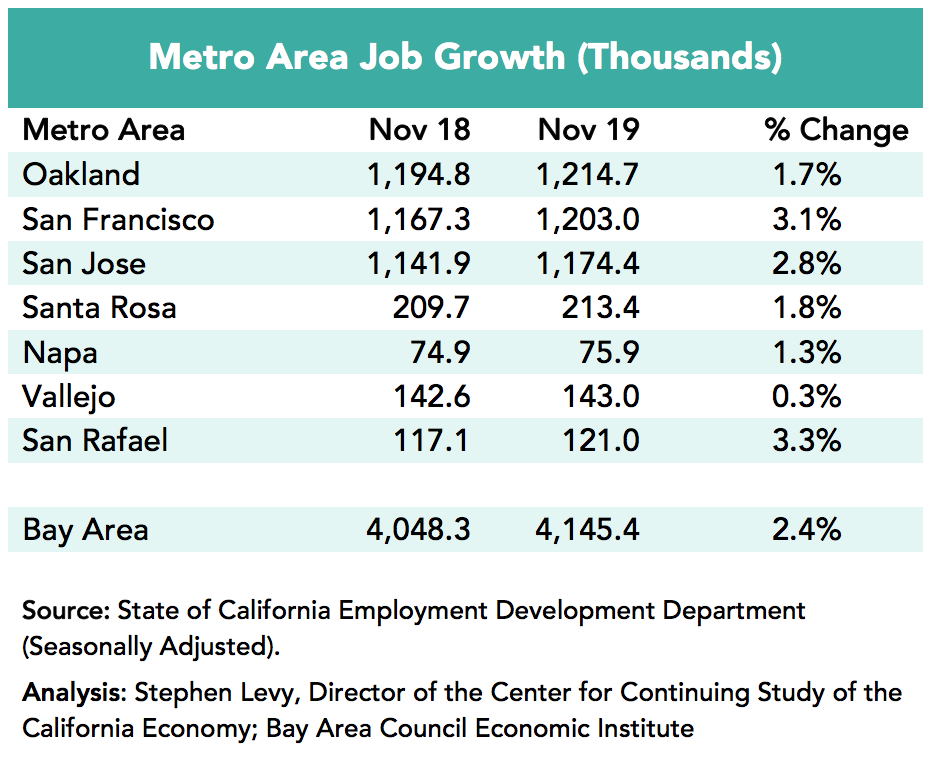

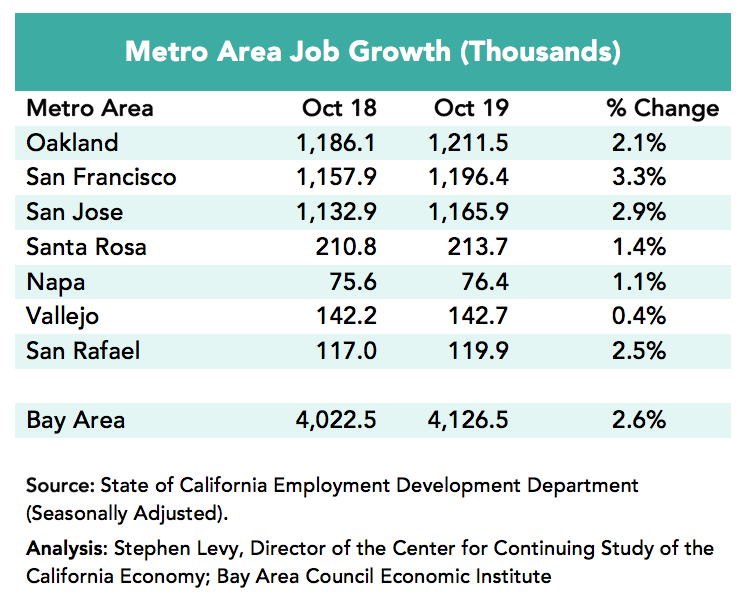

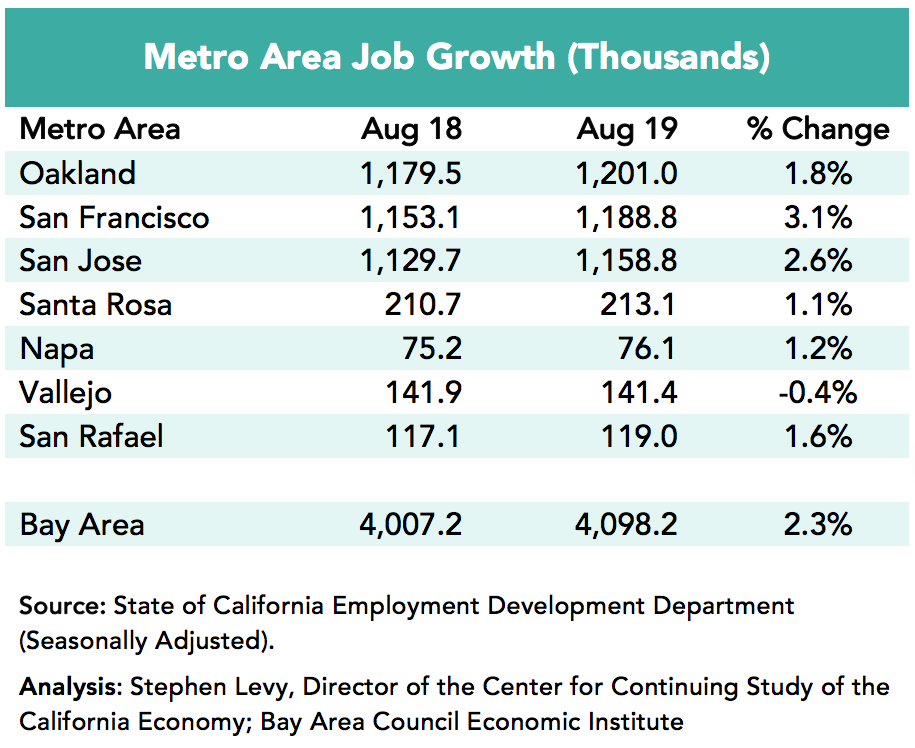

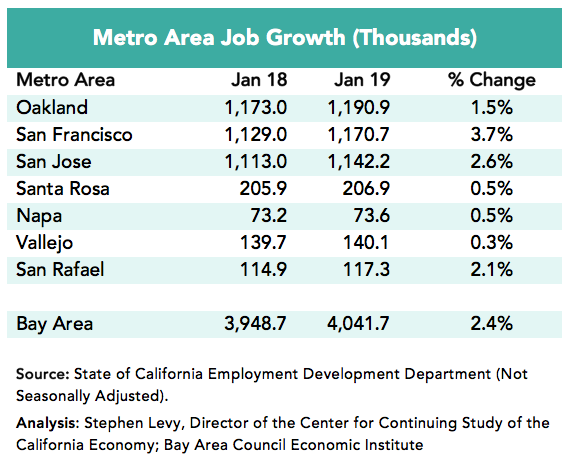

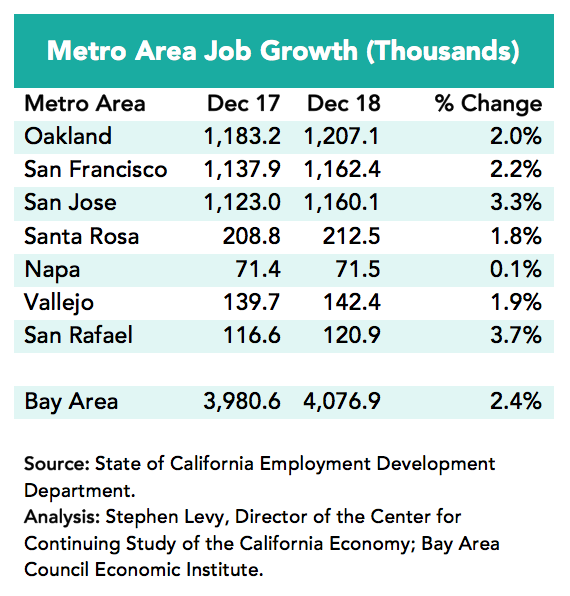

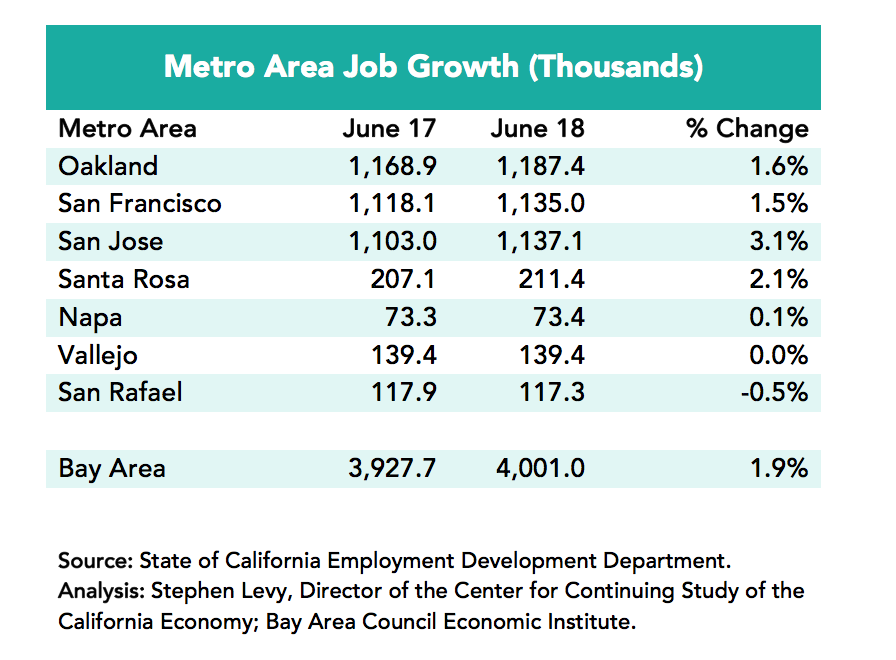

Though growth has slowed in recent months, the Bay Area added 165,000 jobs in the past year (+4.2%) led by a gain of 62,300 in the San Francisco metro area though SF has recovered just 92.4.3% of the jobs lost between February and April 2020. The San Jose metro area added 53,200 jobs and by October 2022 had recovered 104.7% of the payroll jobs lost between February and April 2020. The Oakland metro area added 39,000 jobs during the past year. Other metro areas have been slower to recover lost jobs.

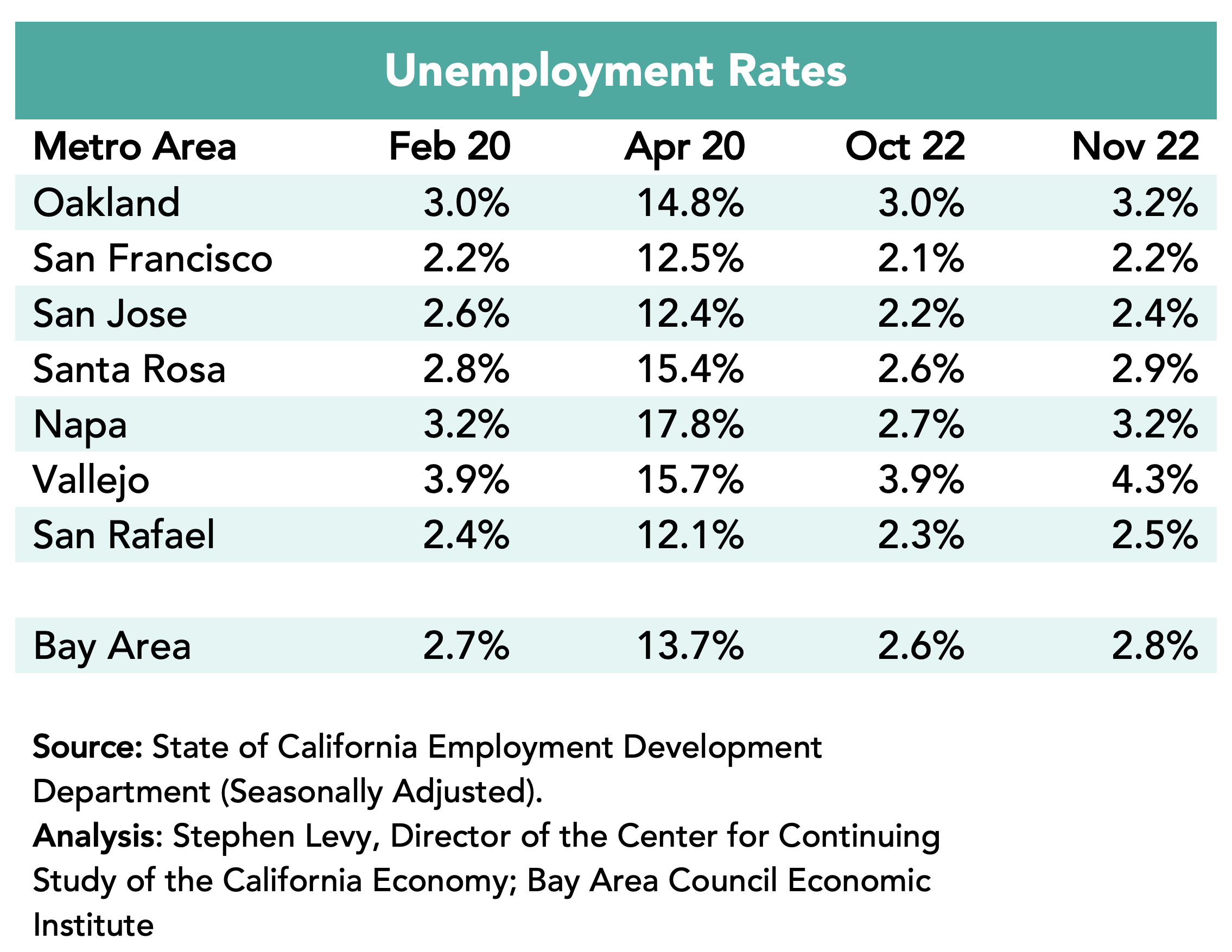

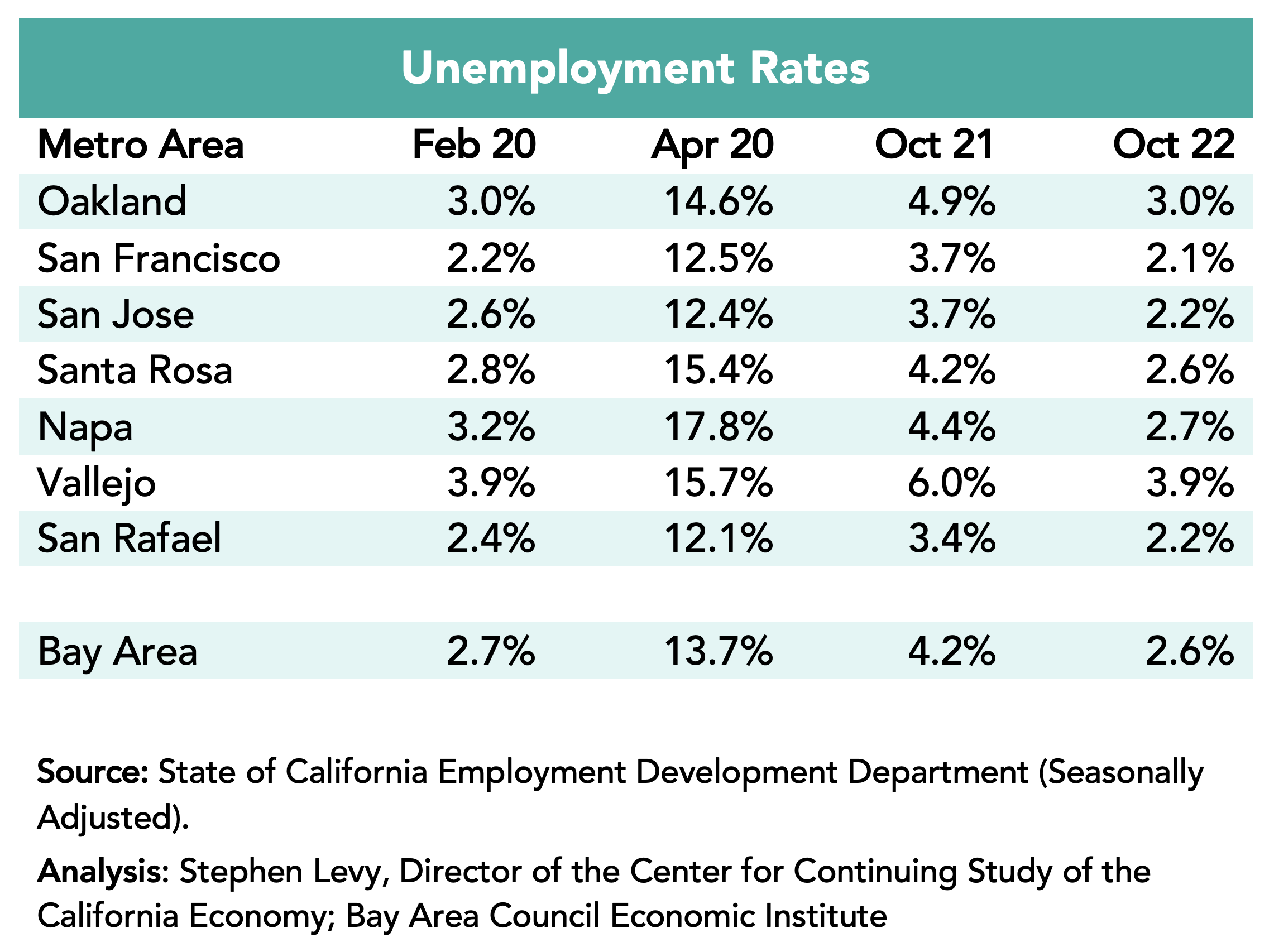

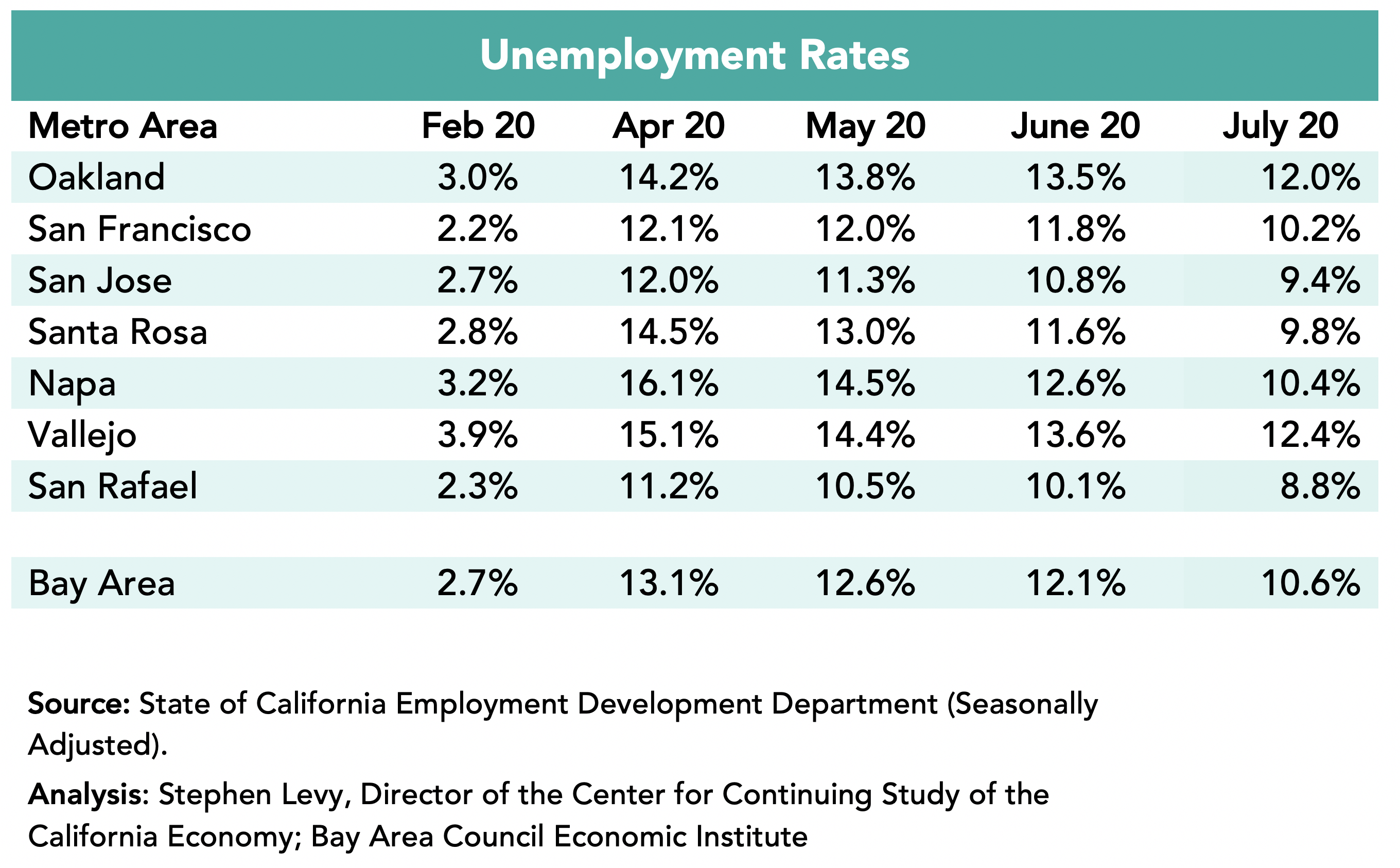

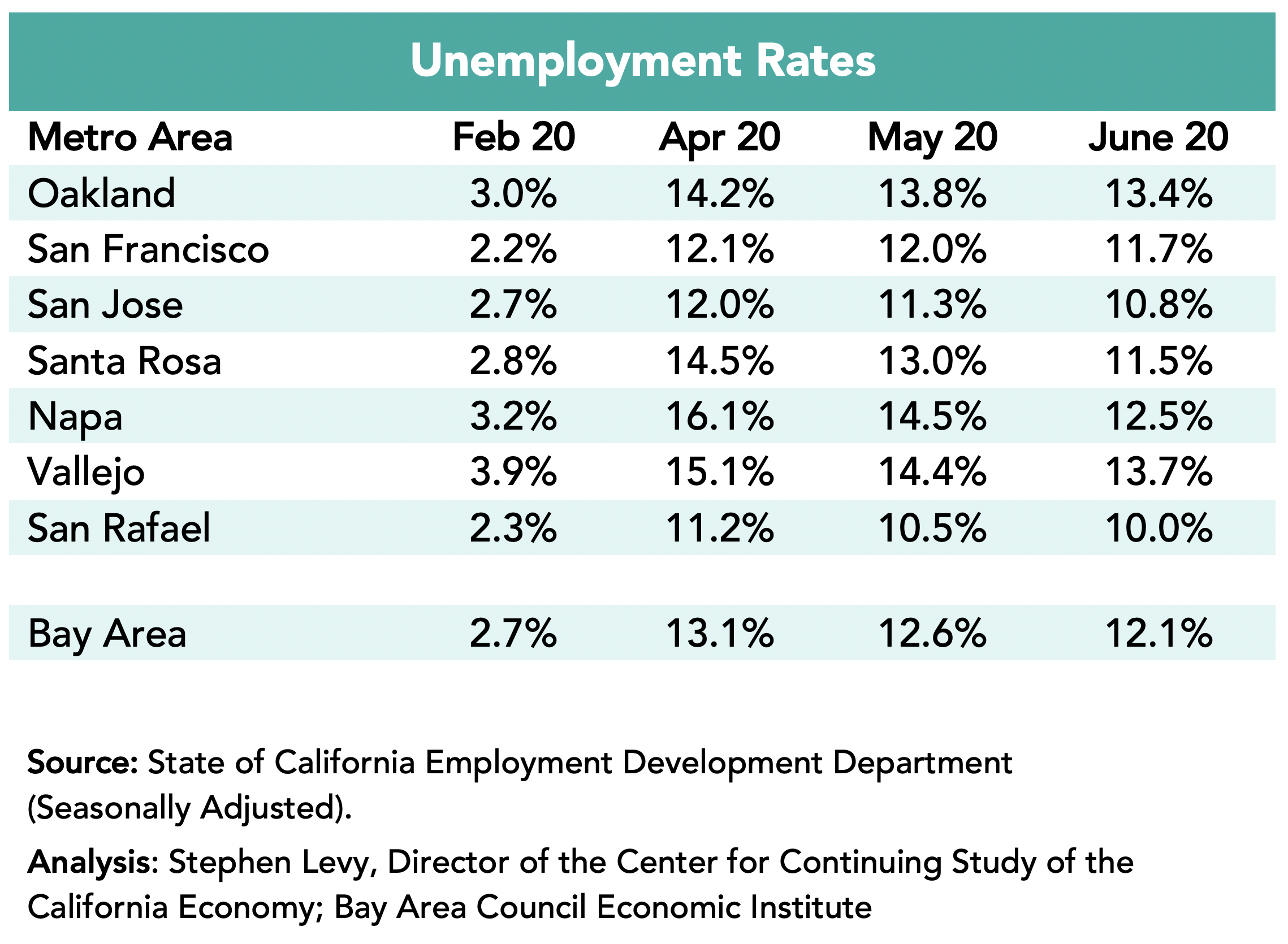

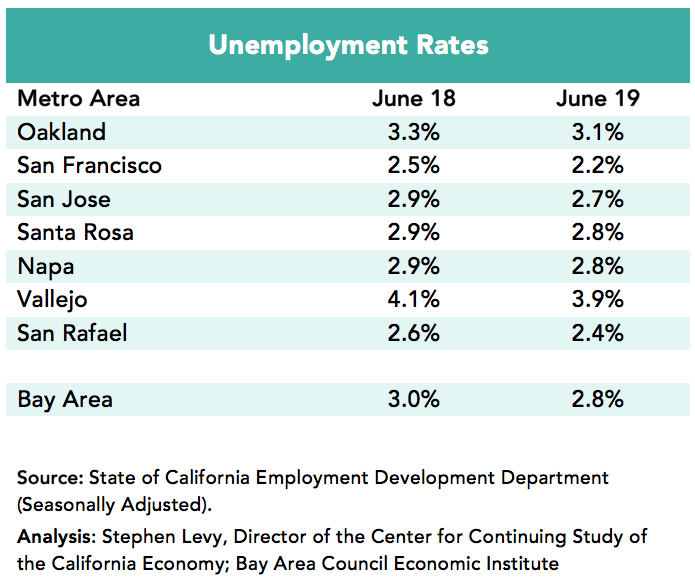

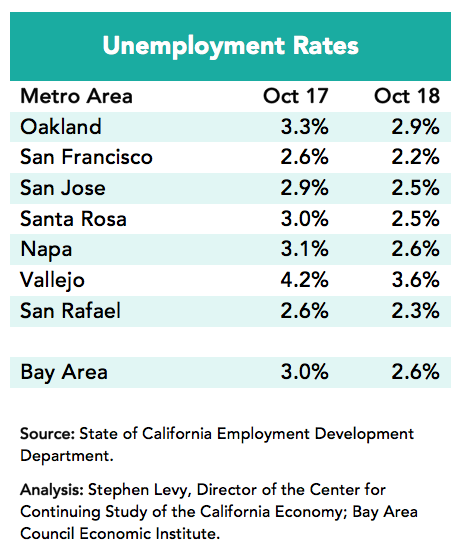

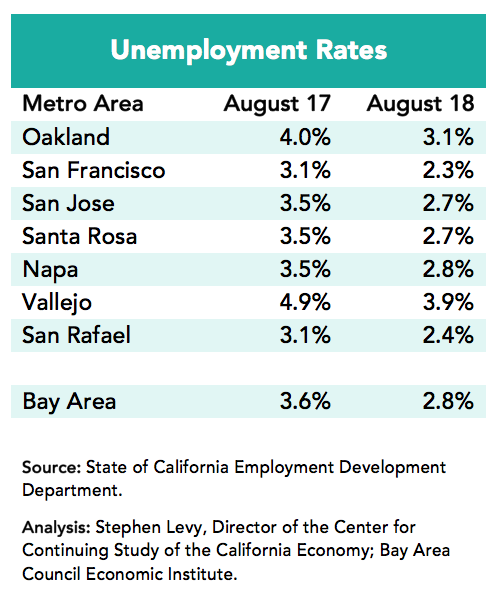

Unemployment Trends

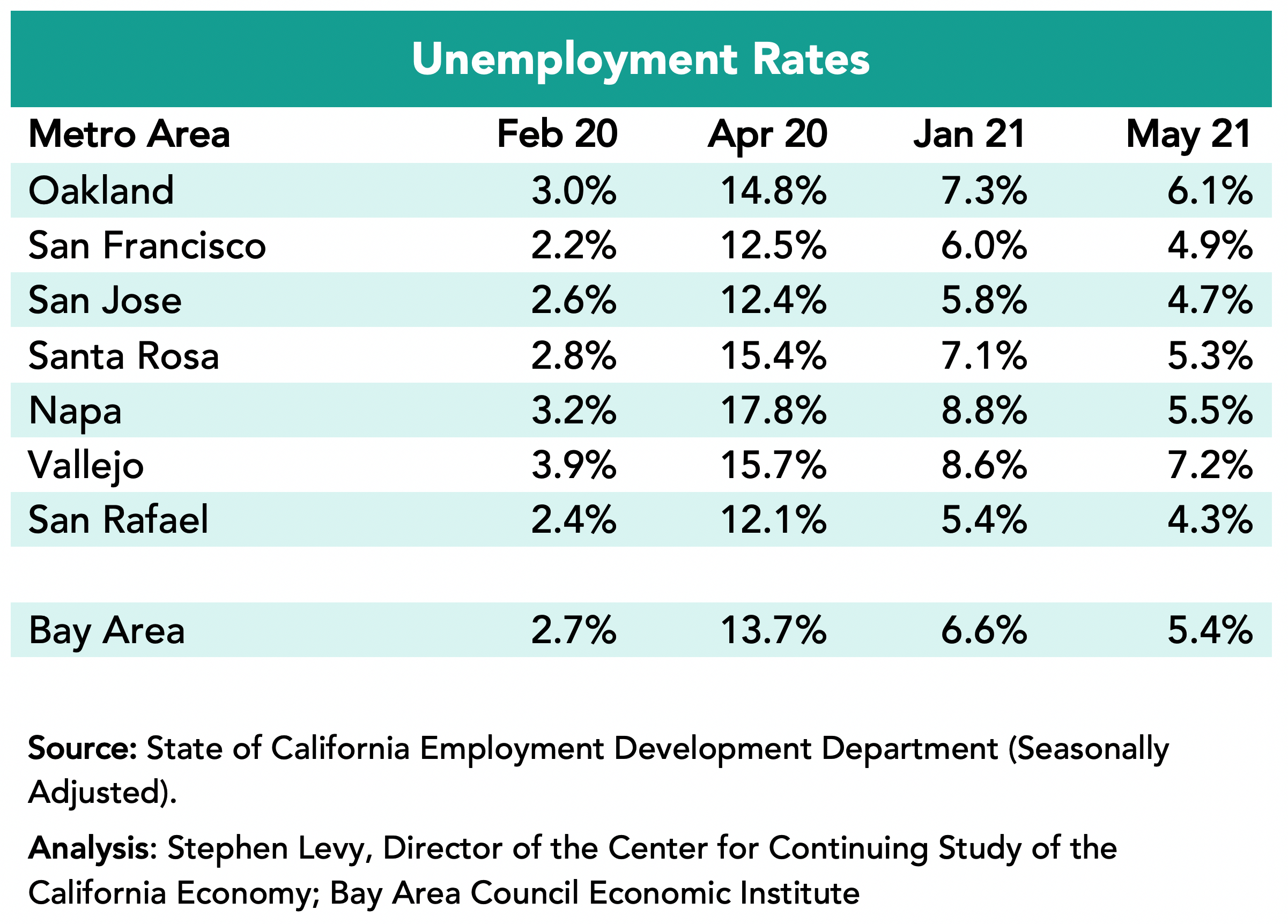

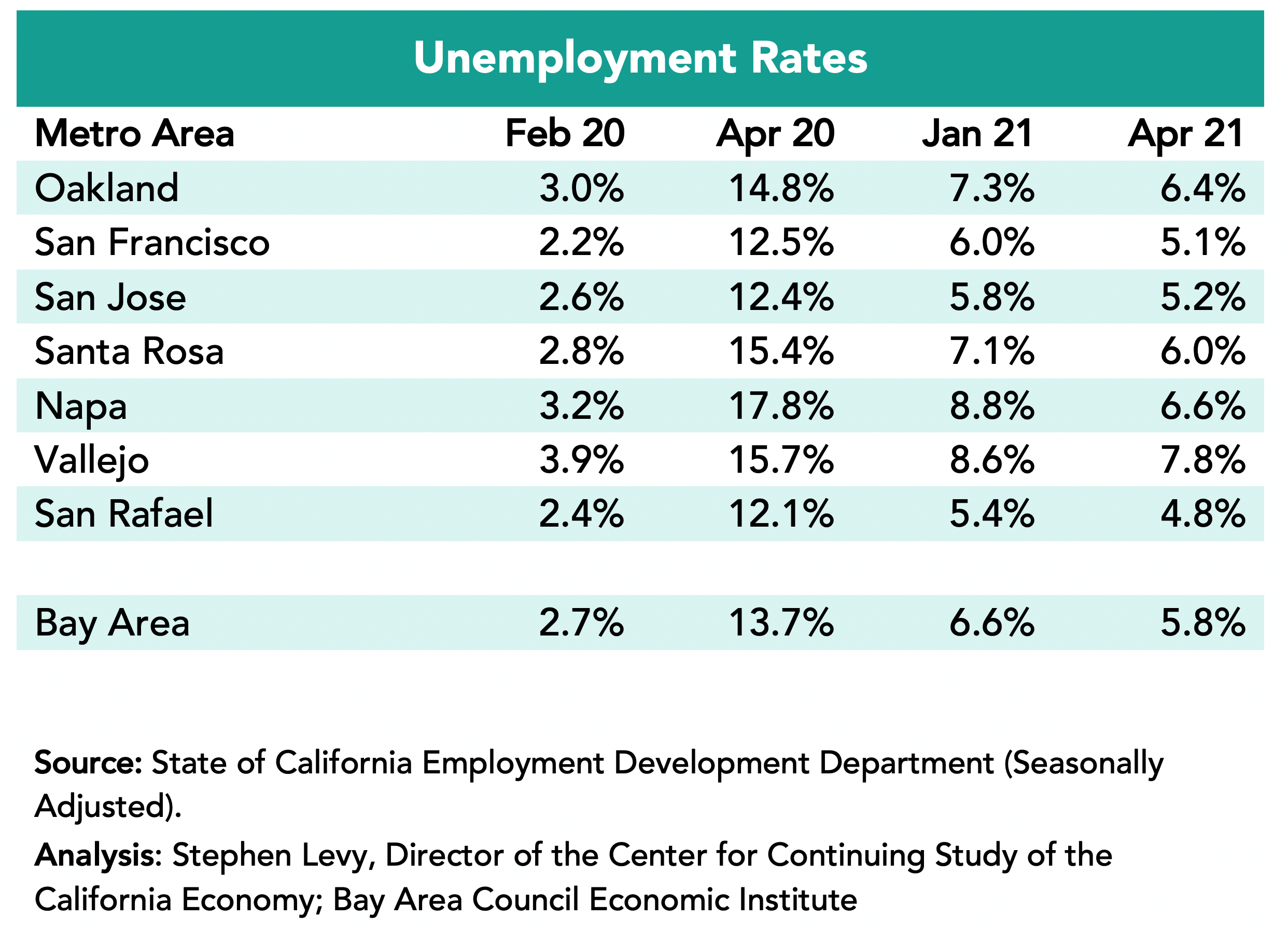

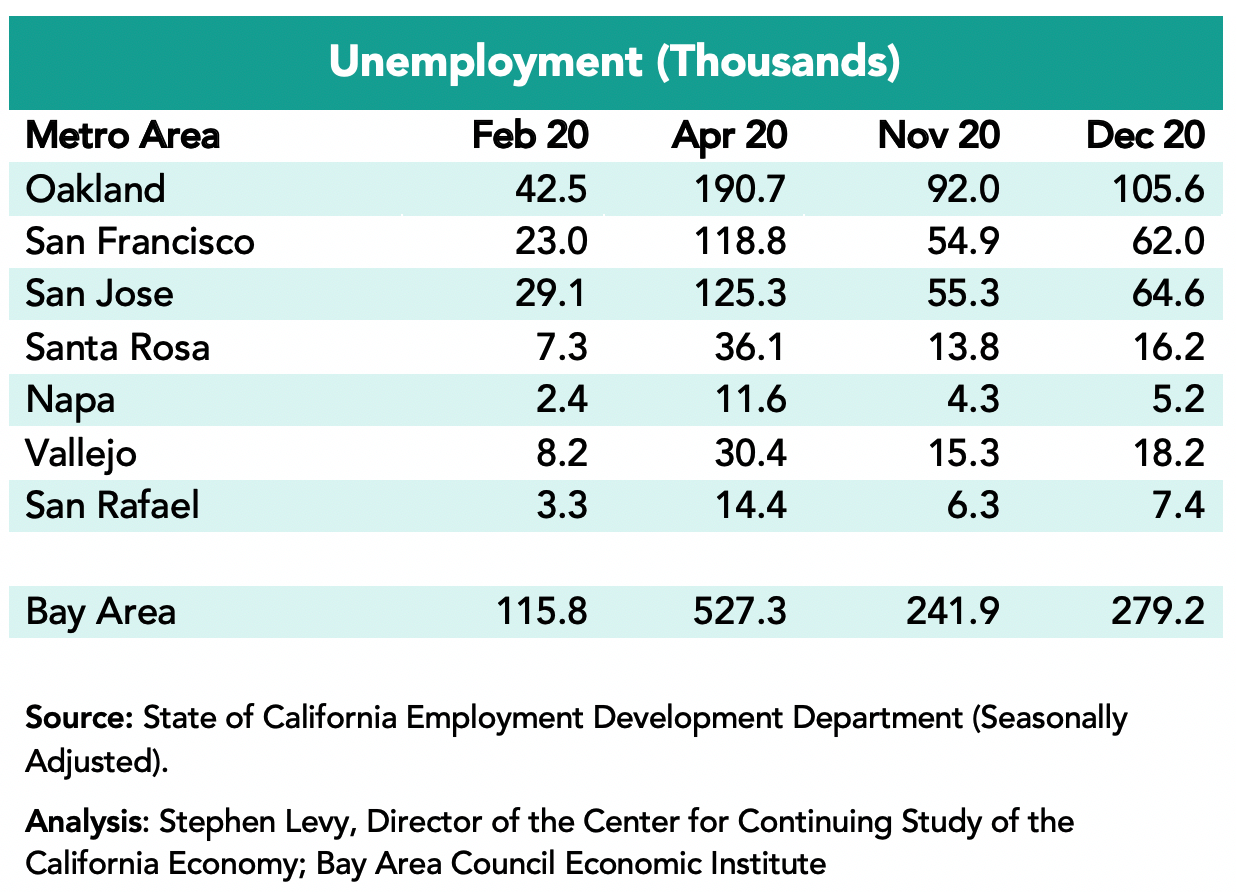

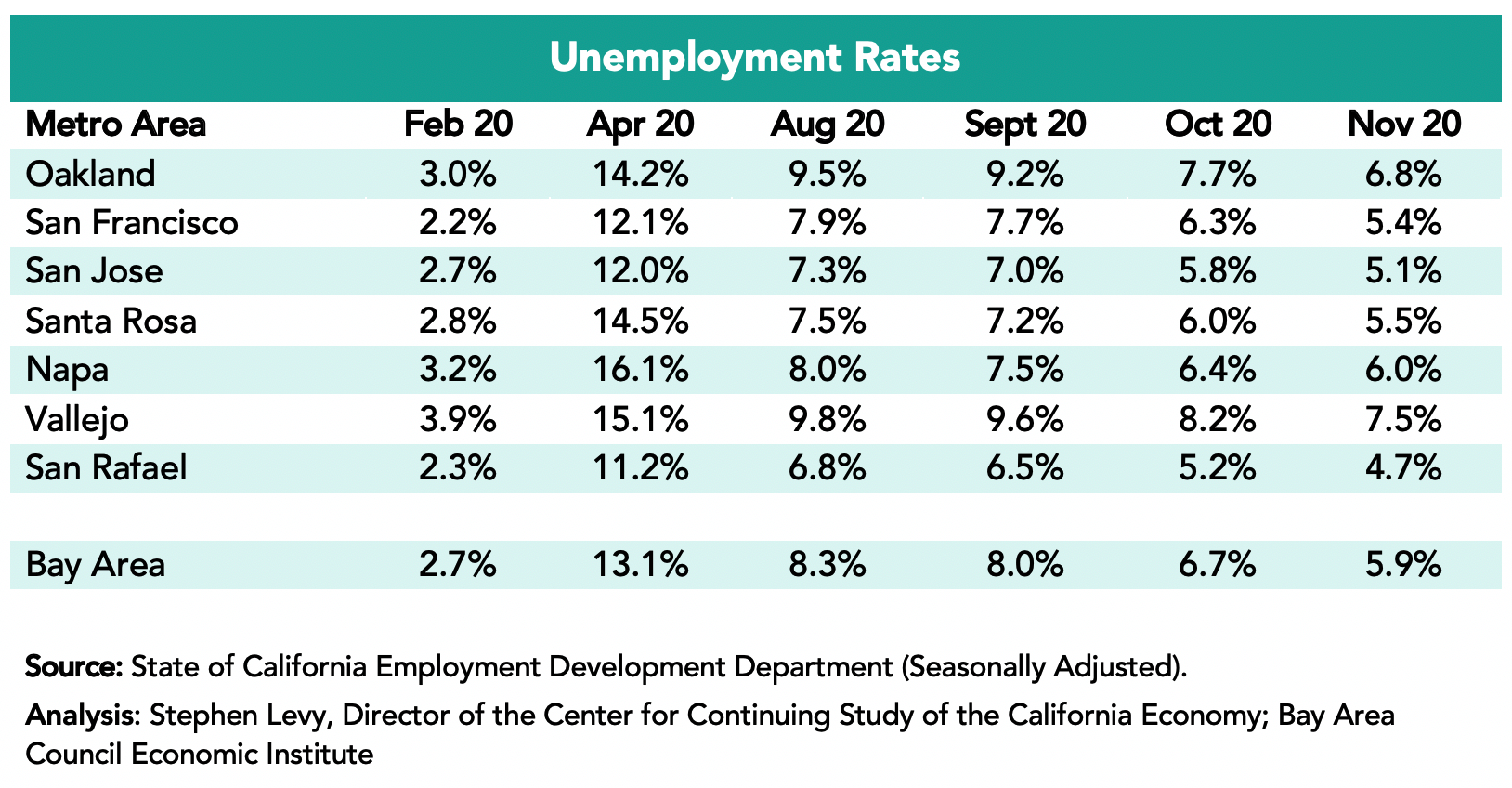

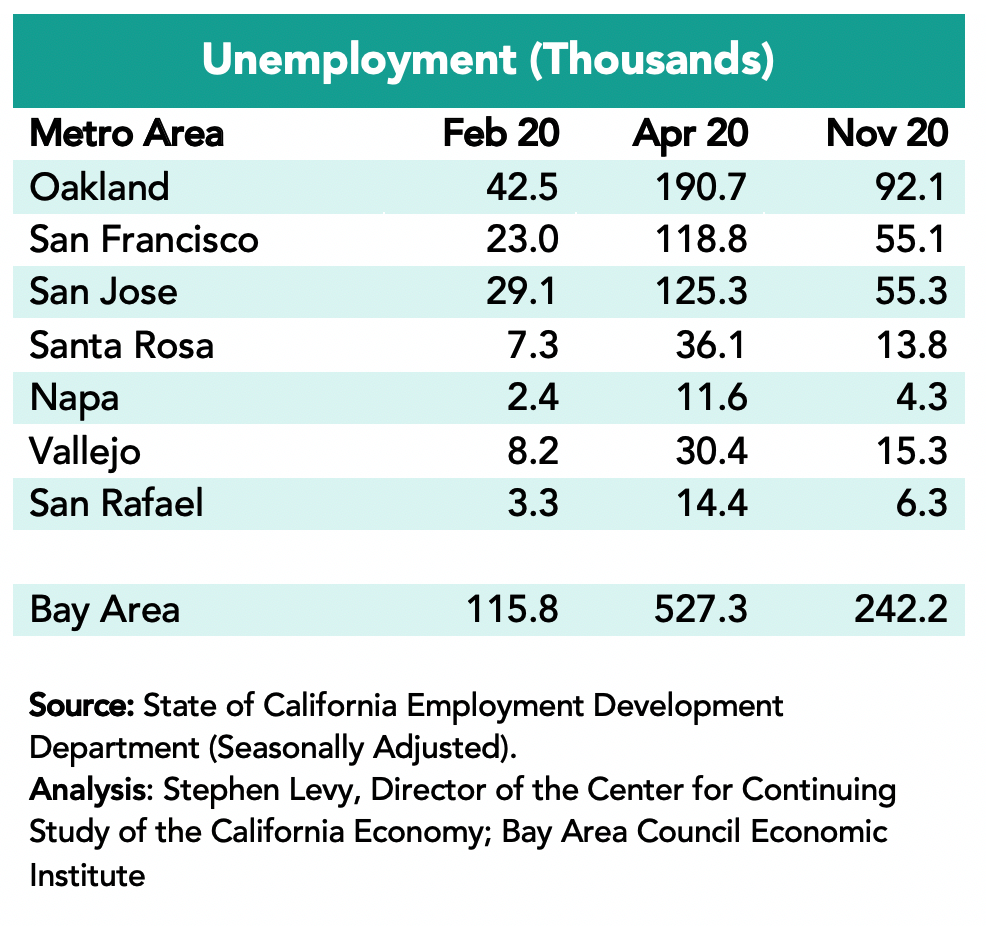

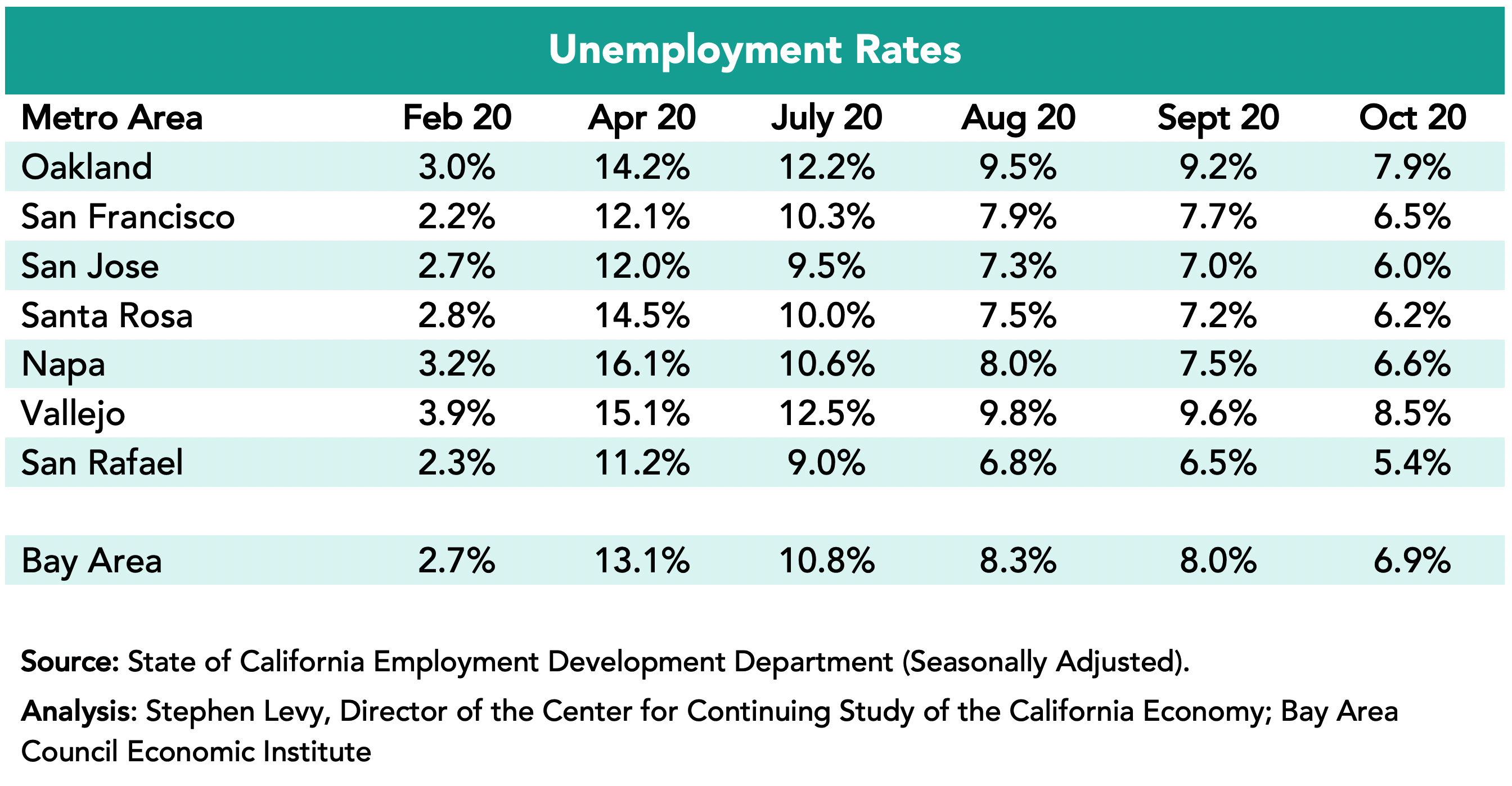

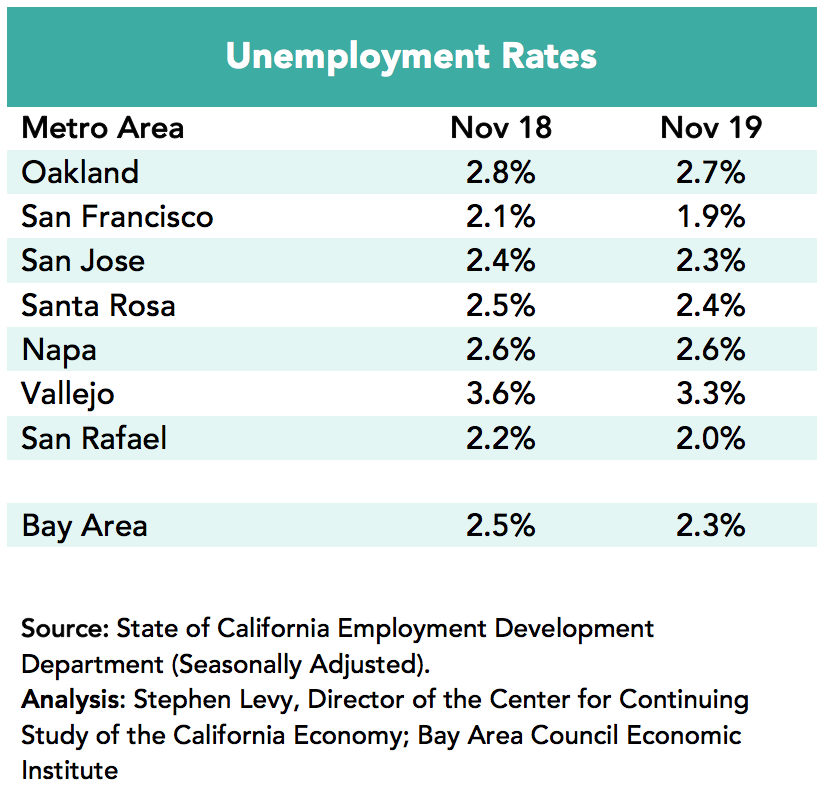

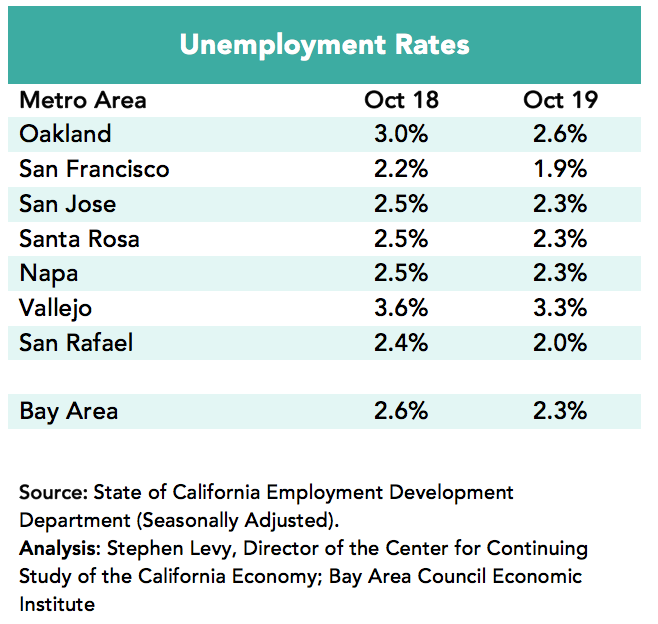

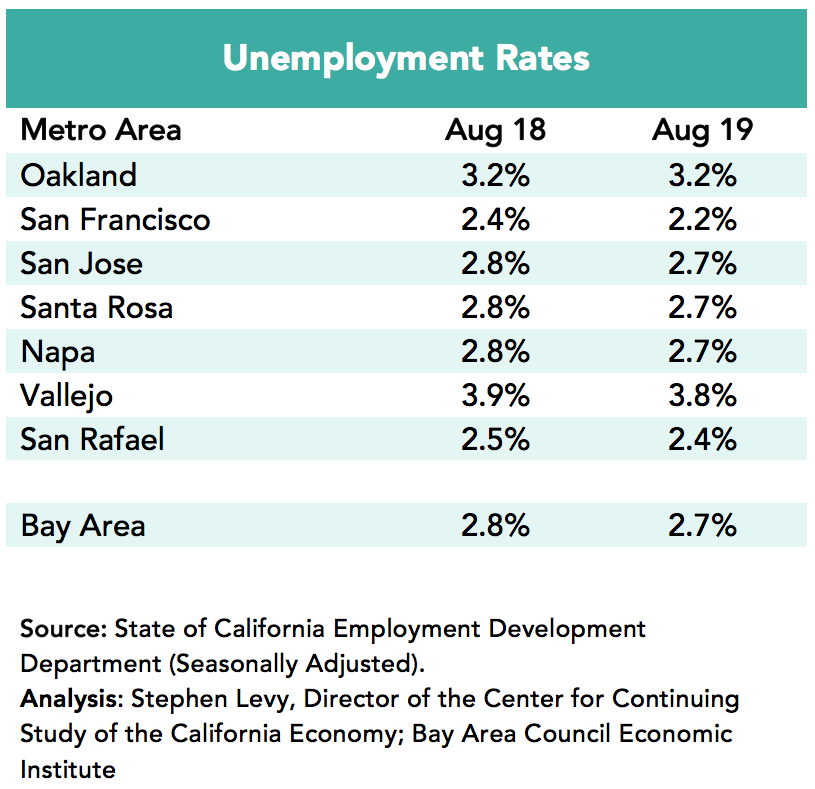

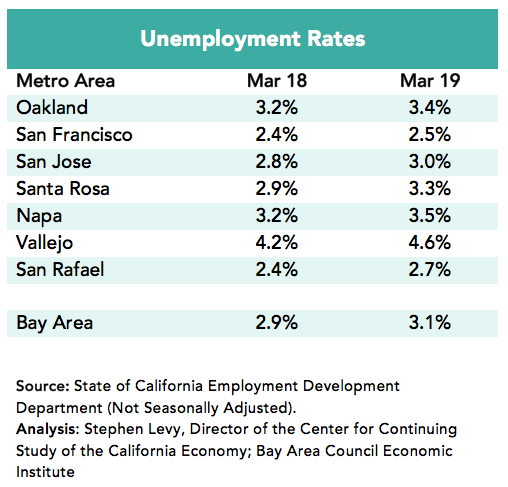

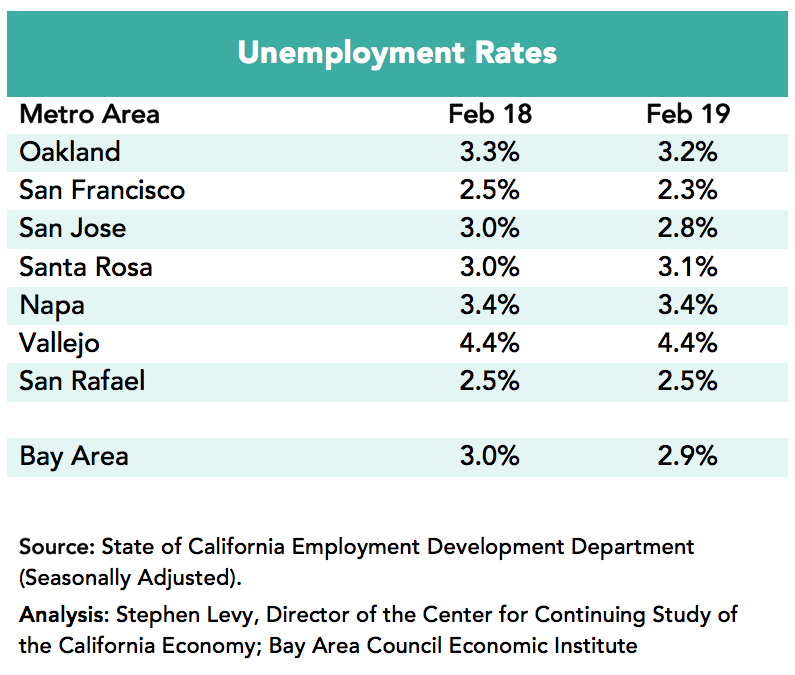

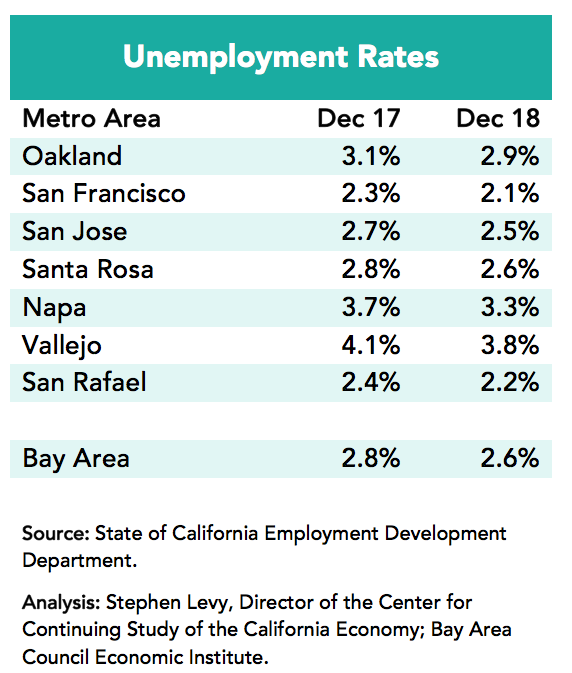

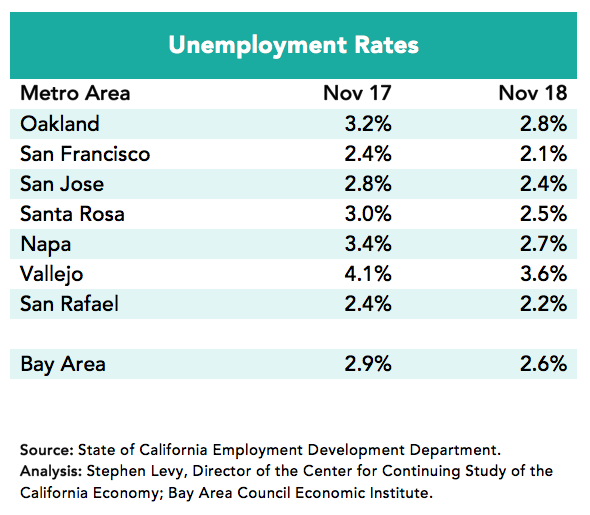

Unemployment rates ticked up in November in all metro areas but remain low by historical standards. The November 2022 rate of 2.8% for the region is just above the February 2020 pre-pandemic rate of 2.7%. And the number of unemployed residents grew in November in all metro areas reaching 115,100 up 8,000 since October.

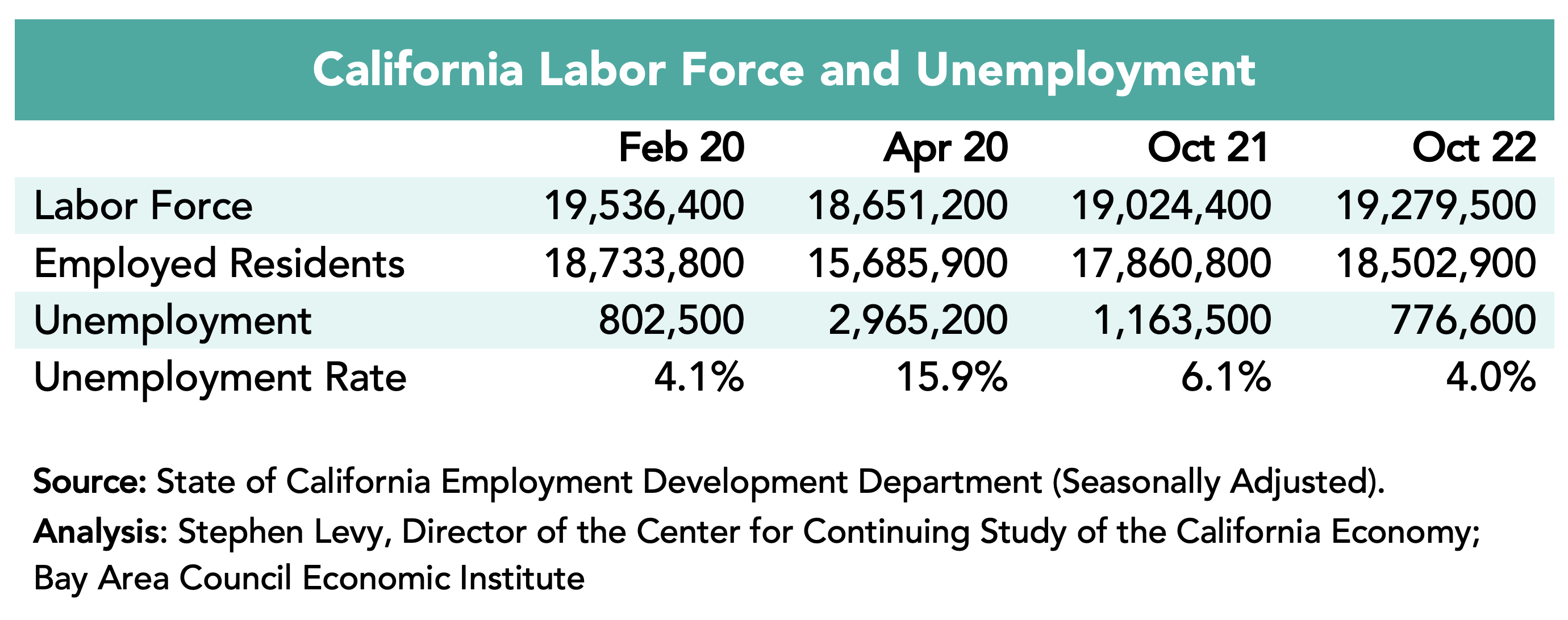

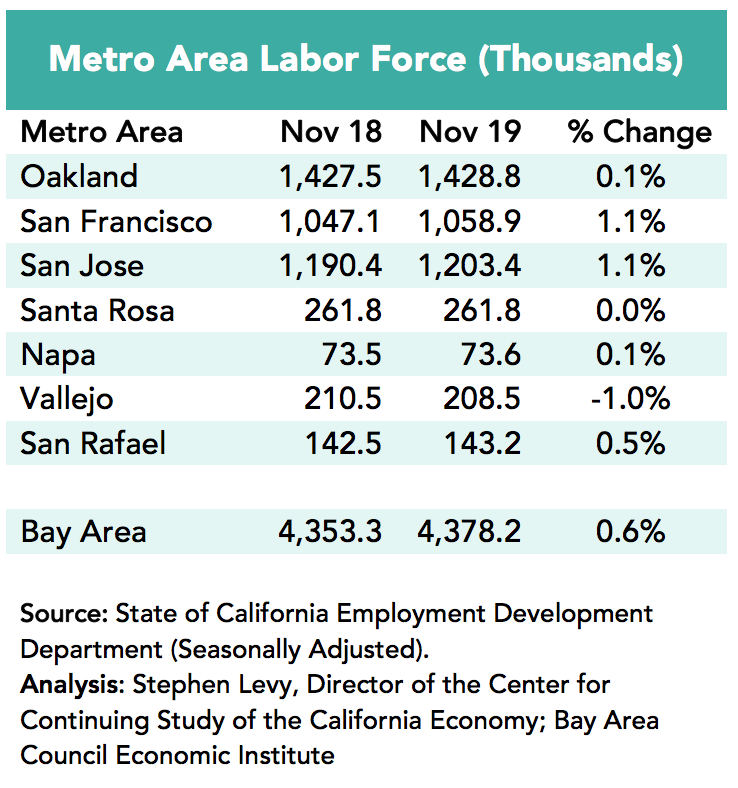

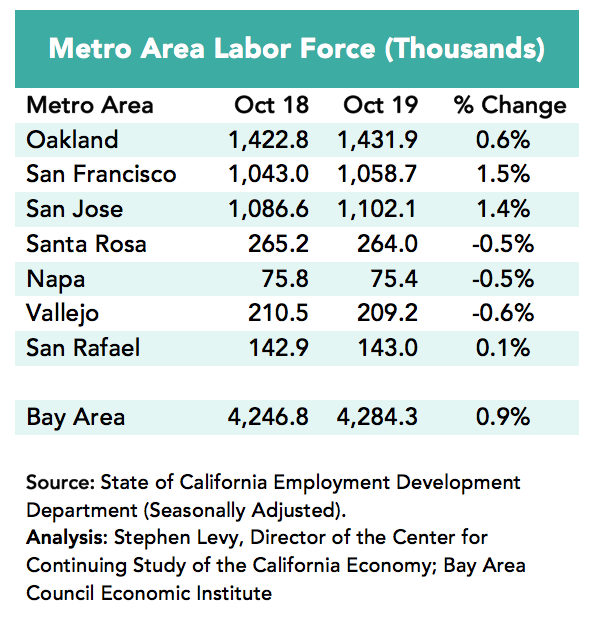

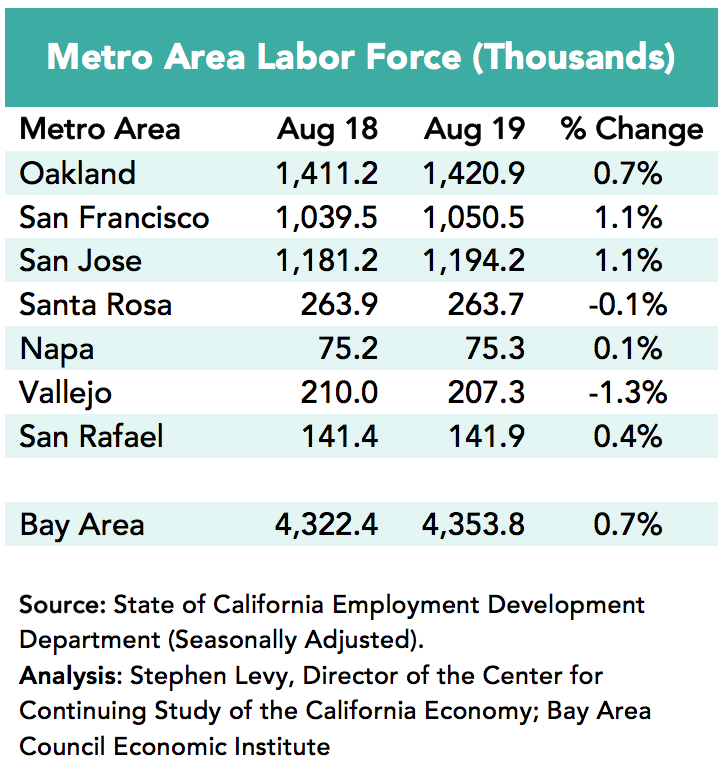

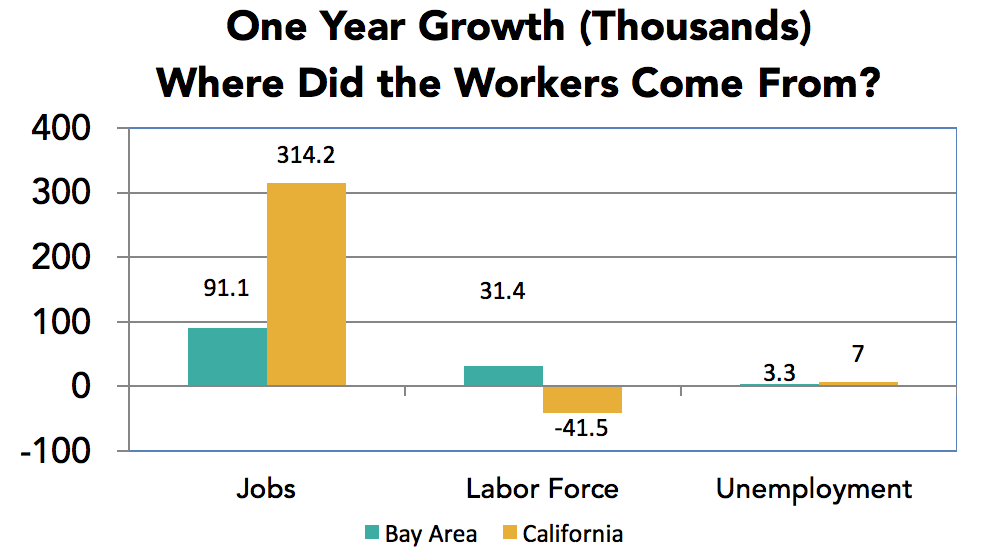

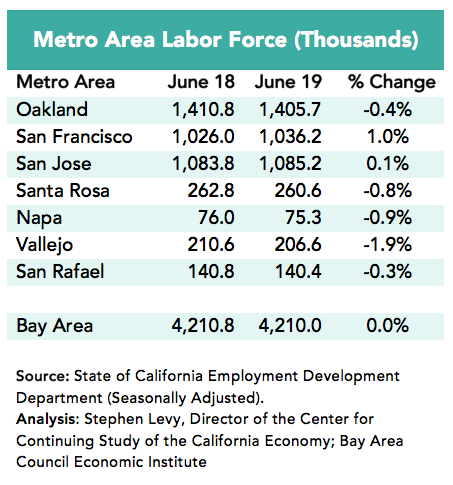

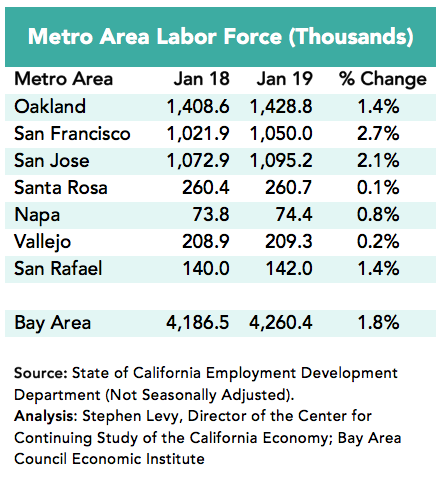

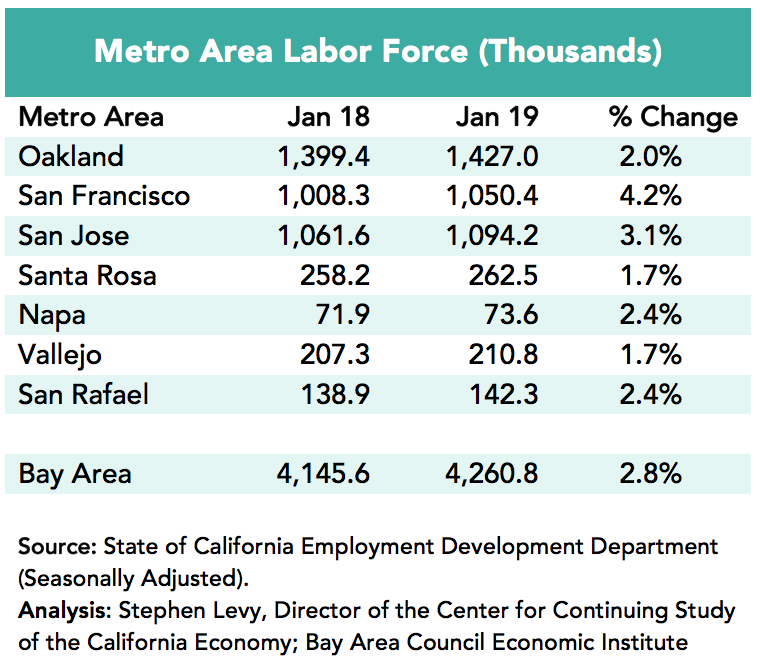

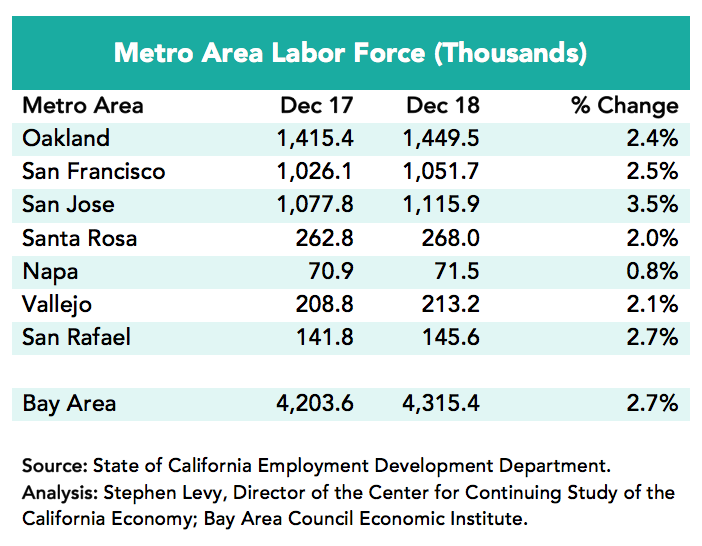

Bay Area and State Labor Force Still Below Pre-Pandemic Levels but Where Will Workforce Growth Come From.

The state has almost 300,000 fewer workers than in the month before the pandemic started and the Bay Area has almost 70,000 fewer residents in the workforce.

Though job growth has continued, it is not clear where new workers will come from with low unemployment already and low population growth It is possible that more workers can come from remote locations so the Bay Area and state can see job growth without more residents working. Job openings remain high and sectors like air travel are constrained by lack of enough workers. Increasing the level of immigration would be a large help to the region and state.

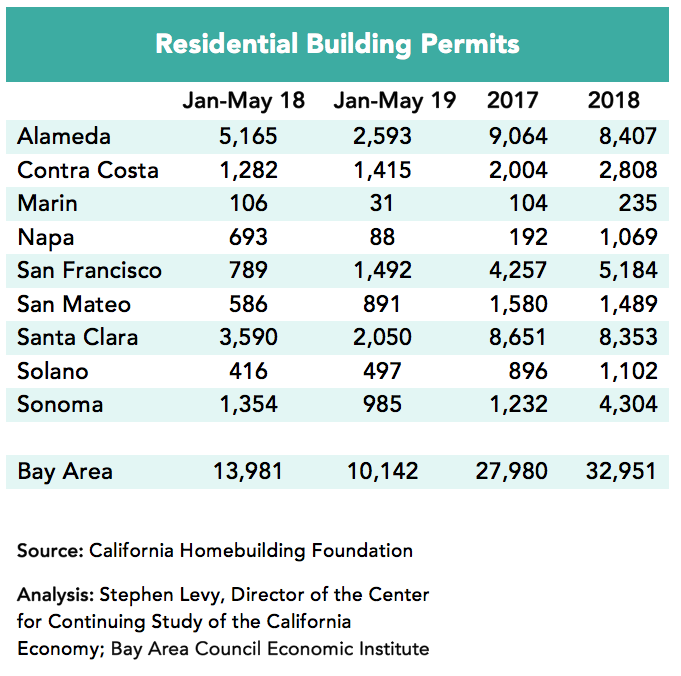

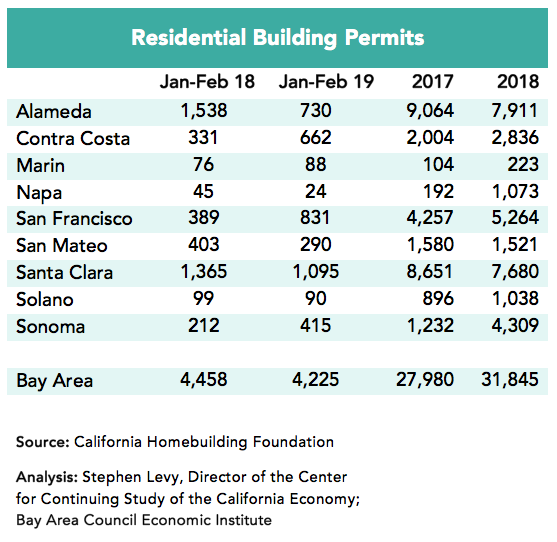

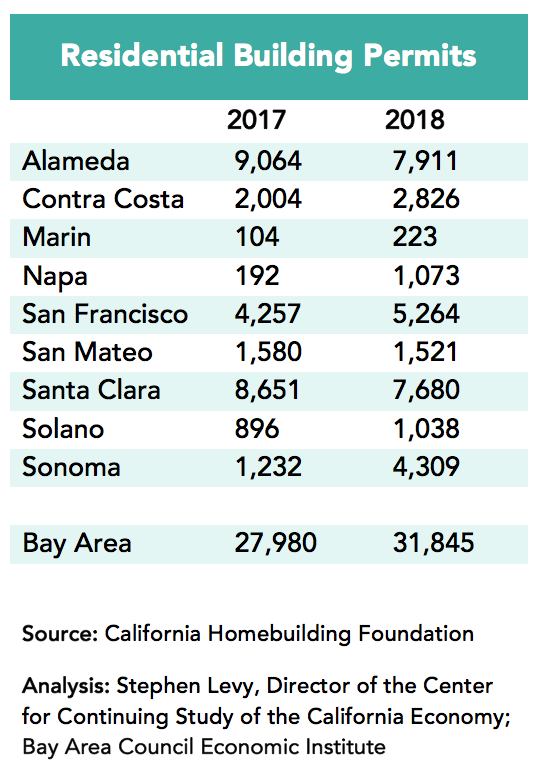

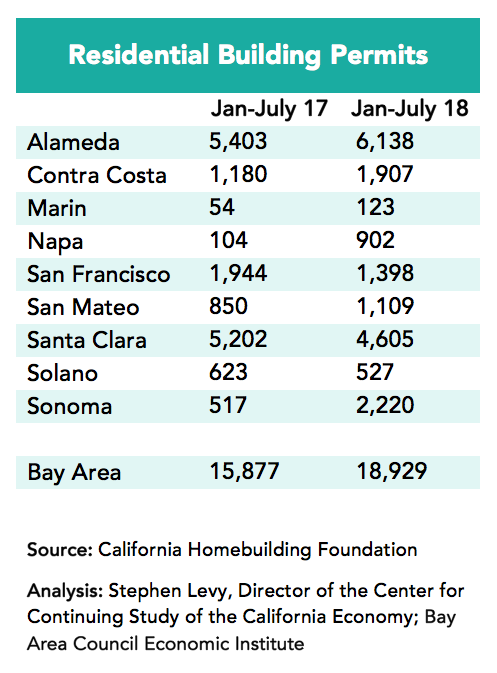

A Welcome Uptick in Housing Permits

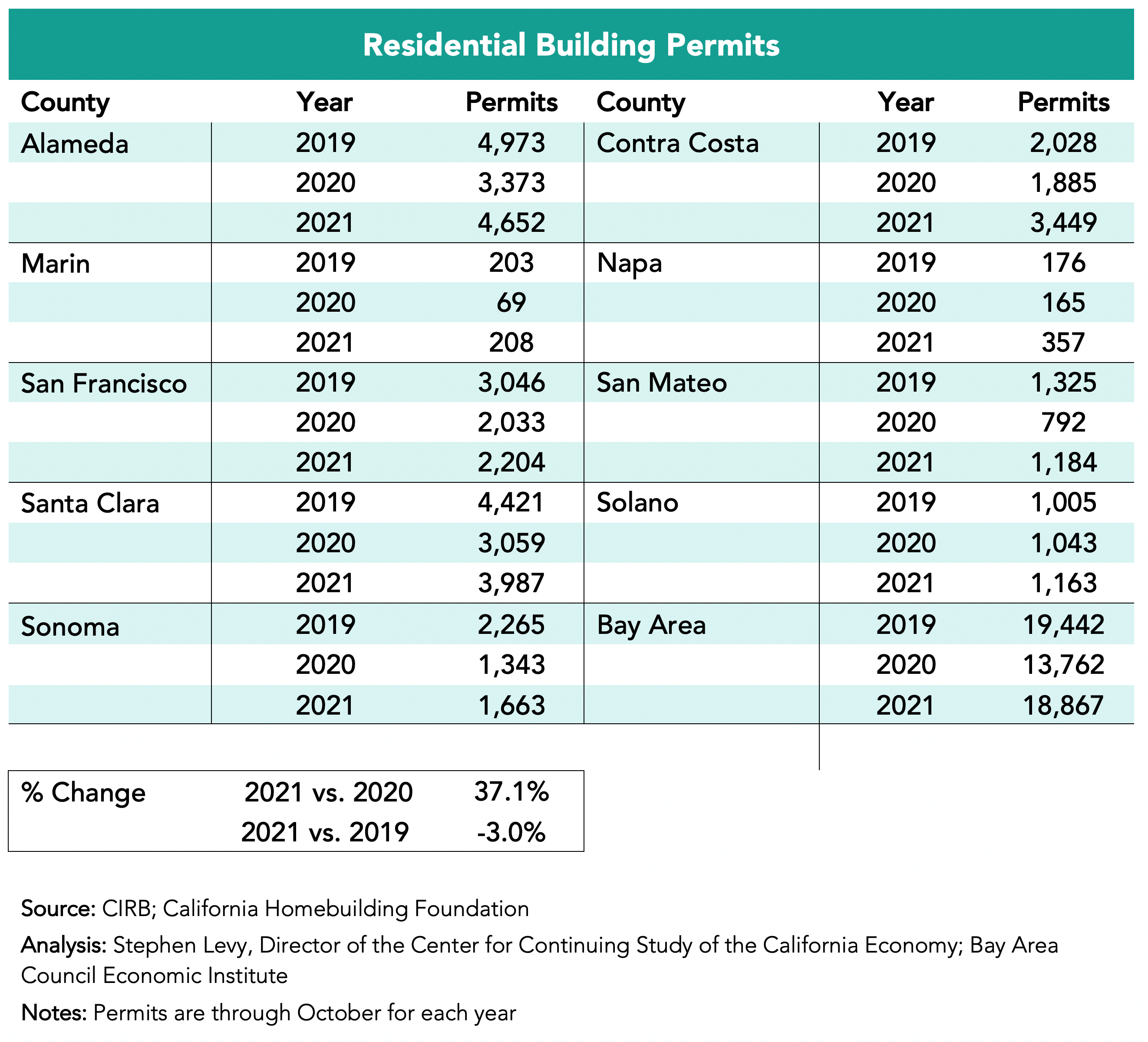

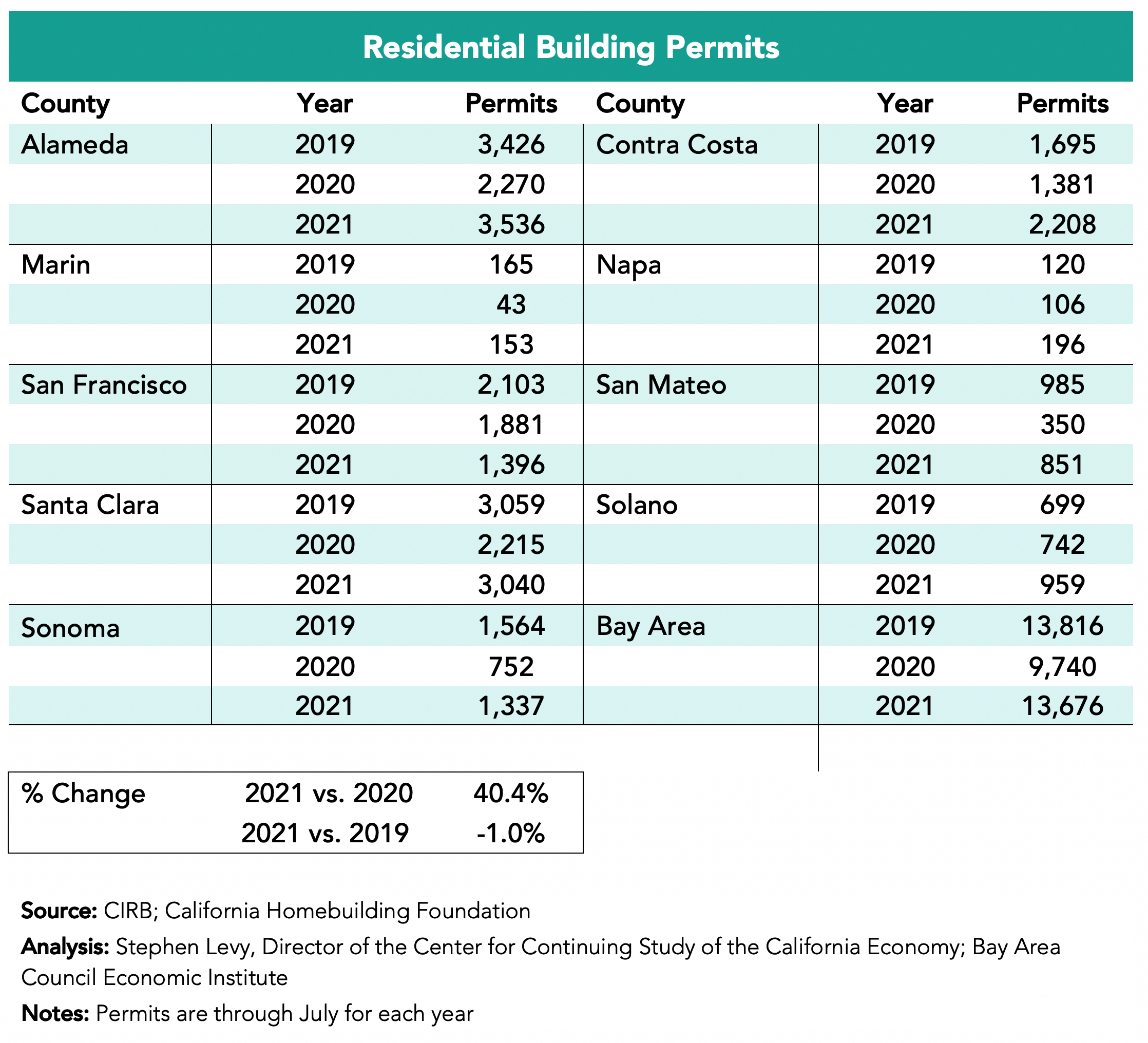

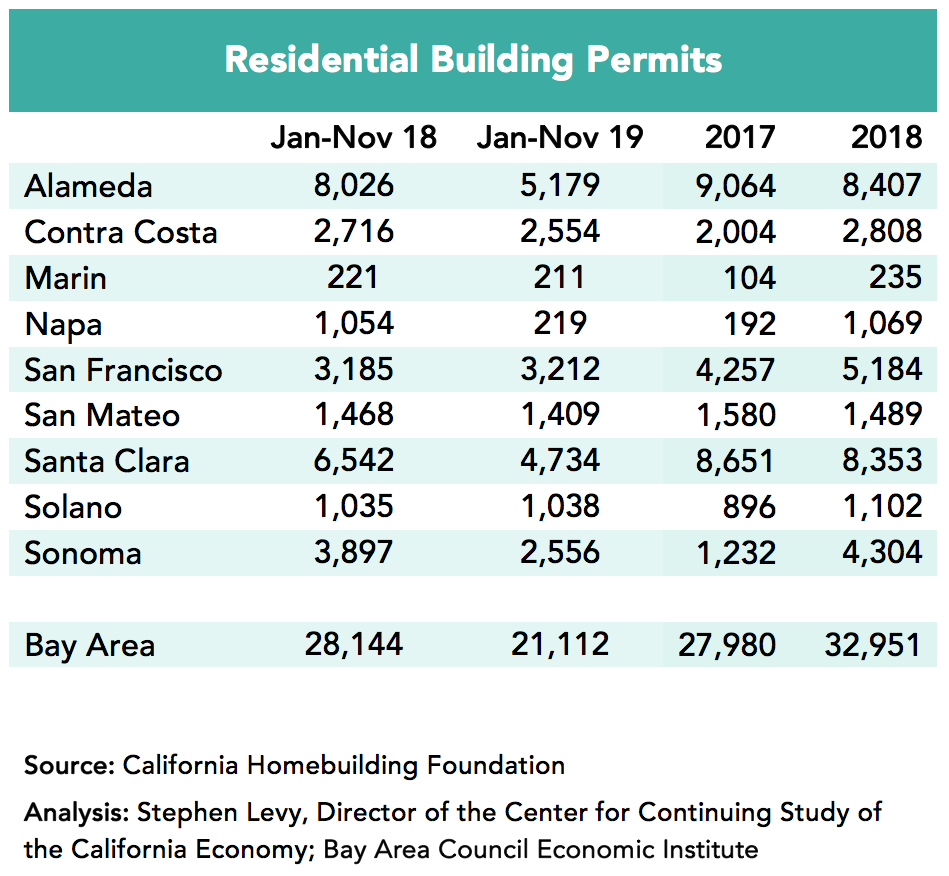

Permits levels in the first ten months of 2022 exceeded 2019 and 2021 levels though East Bay permit levels were below earlier levels. The other counties showed large year over year gains. In addition, now there are almost daily reports of new housing projects being proposed and approved though it is often a long step until these units are completed and on the market. Bay Area cities are updating their Housing Elements currently and learning about the requirements to meet their RHNA goals. It is possible that the RHNA and update process is encouraging cities to loosen development standards and to approve more projects. While the current growth in permits is a positive sign, these levels are still below the RHNA targets for the region. More needs to be done.

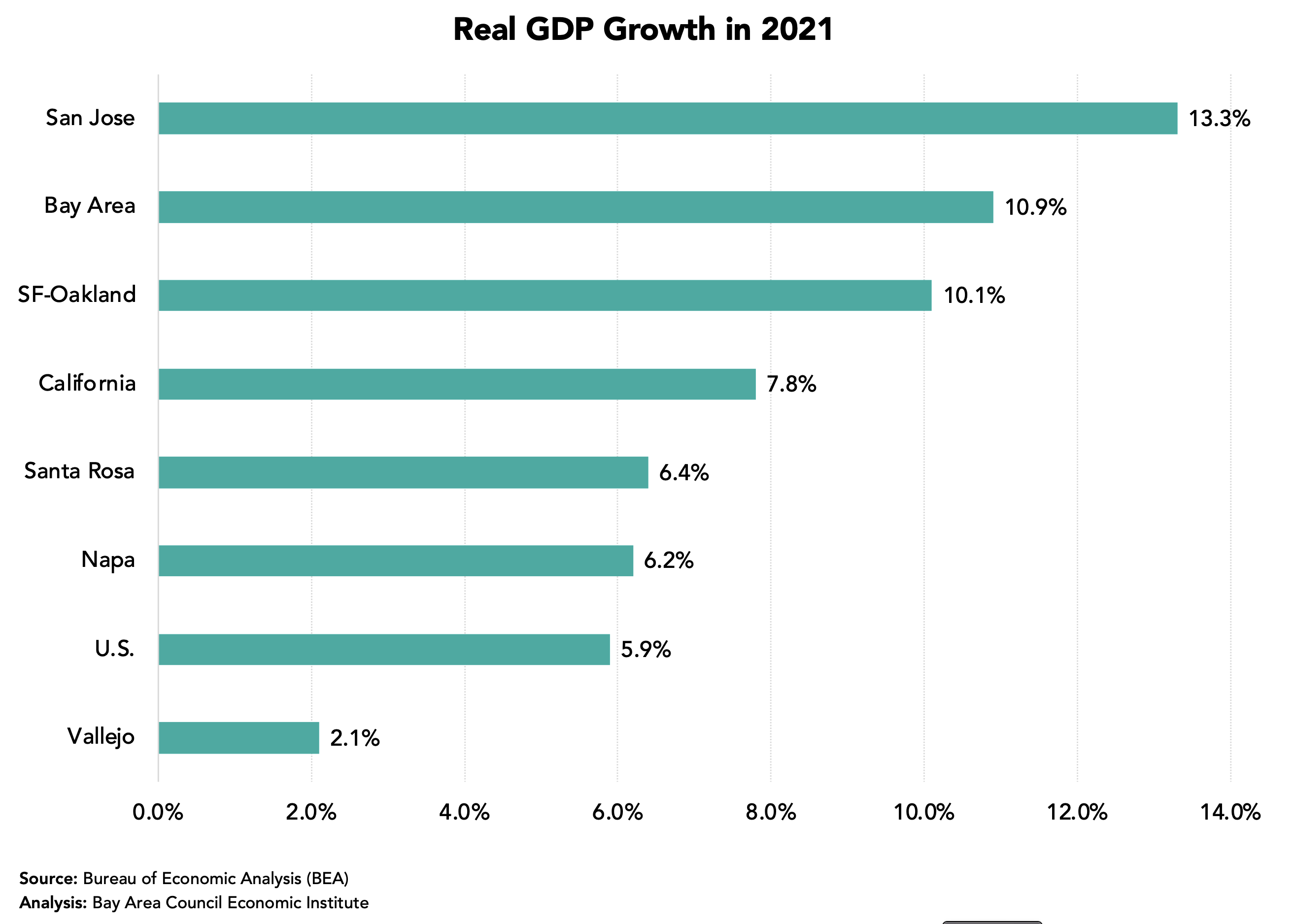

Strong GDP Gains in 2021

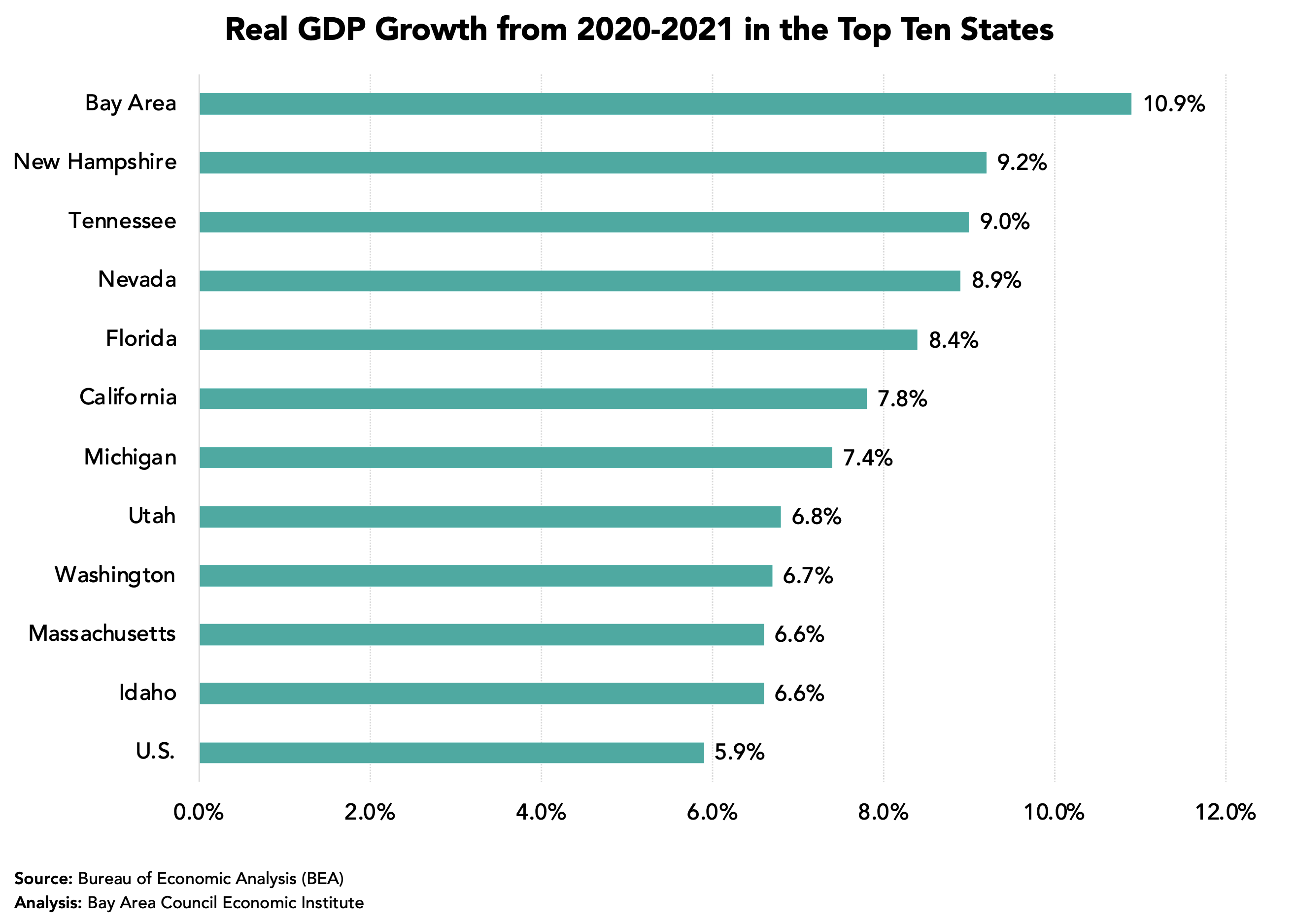

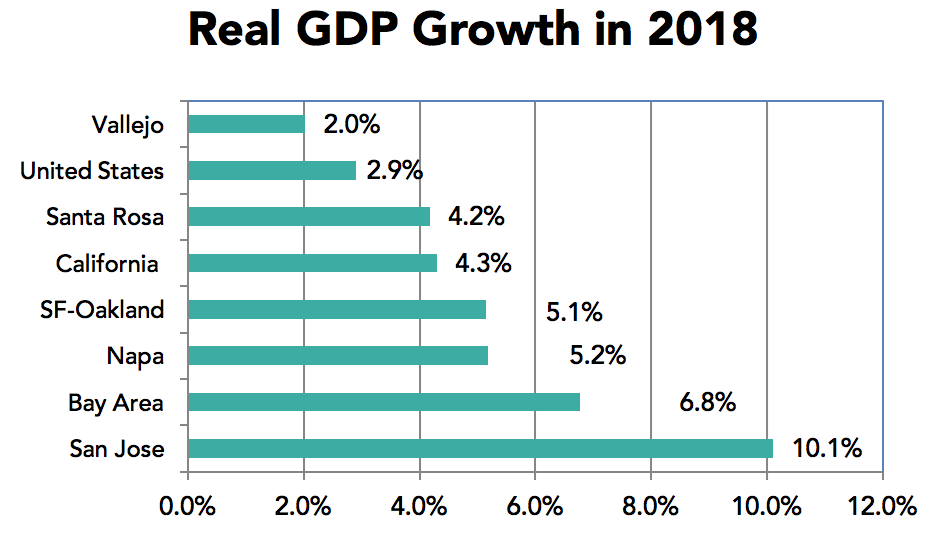

Real GDP rose by 10.9% in the region between 2020 and 2021 according to estimates released by BEA on December 8th this year.

Real GDP increased most in the San Jose metro area (+13.3%) followed by the SF-Oakland metro area that includes Marin County (+10.1%). The Napa and Santa Rose metro areas outpaced the nation while the Vallejo metro area had the region’s slowest GDP growth in 2021.

The Bay Area not only outpaced the nation in GDP growth, the region’s growth topped that of all states.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

November 21, 2022

The highlights:

• The Bay Area added 17,600 jobs in October after two months of slow growth. Unemployment rates ticked up slightly but the region’s UE rate in October was 2.6%.

• Both the region and state showed conflicting trends between the jobs survey (up) and the household survey with rising unemployment and a decline in the labor force.

• In May Bay Area unemployment levels and unemployment rates fell to record lows.

• Housing permits for the first nine months of the year surpassed both 2021 and 2019 levels though still well below the region’s new RHNA targets.

• Total and per capita income rose sharply across the region and state according to BEA estimates released this week.

• The challenges of high inflation and interest rates remain as well, as the Bay Area faces challenges of housing, transportation and supporting competitiveness.

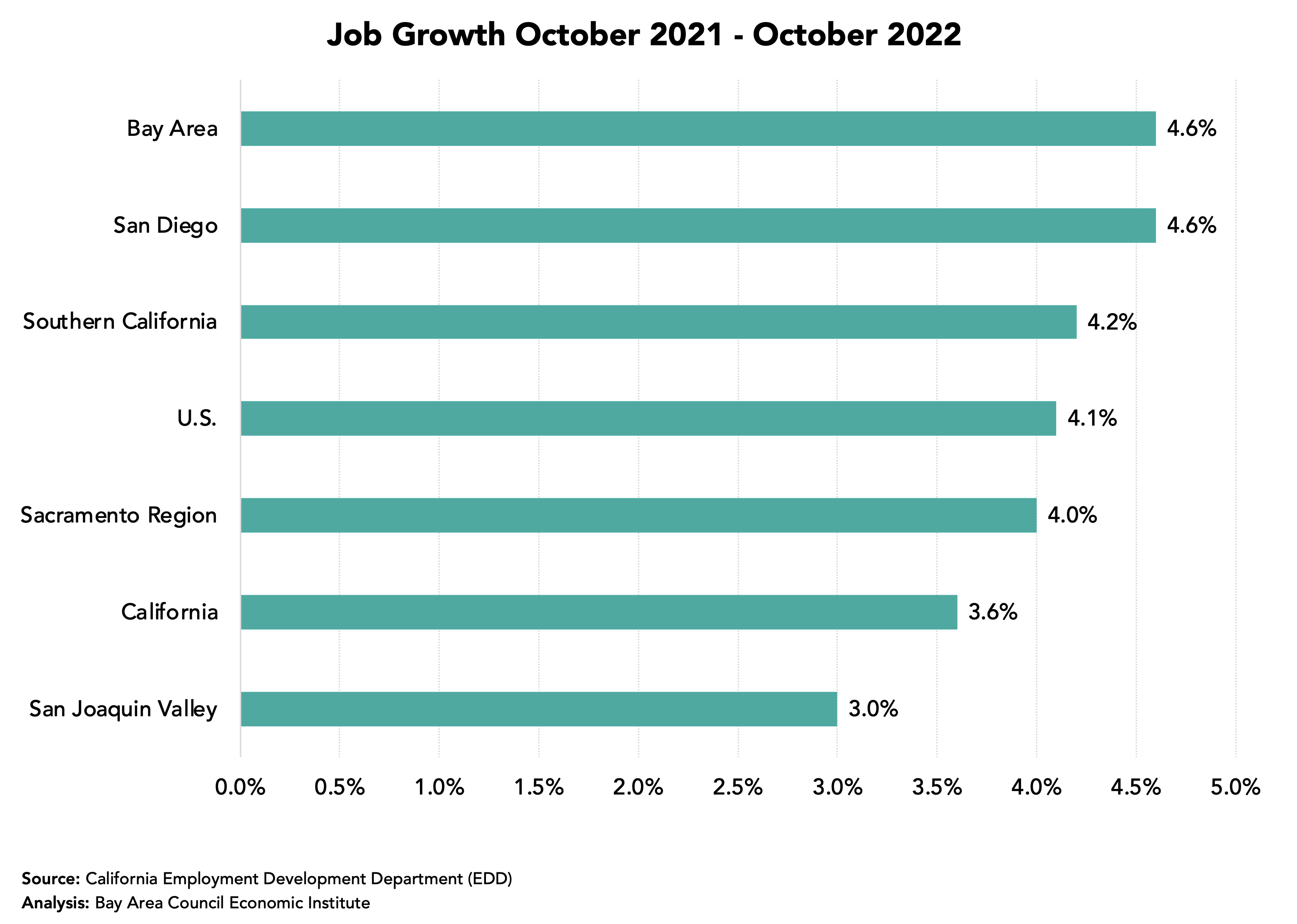

Even with the Recent Slowdown the Bay Area and State Posted Above Average Job Growth During the Past 12 Months

All regions in the state except the San Joaquin Valley outpaced the nation in job growth during the past 12 months led by the Bay Area and San Diego.

The chart below gets wide media attention and focuses on our region’s below-average job recovery rate. The chart above indicates that the Bay Area is catching up.

Payroll Job Growth Shows the San Jose Metro Area Leads the Region

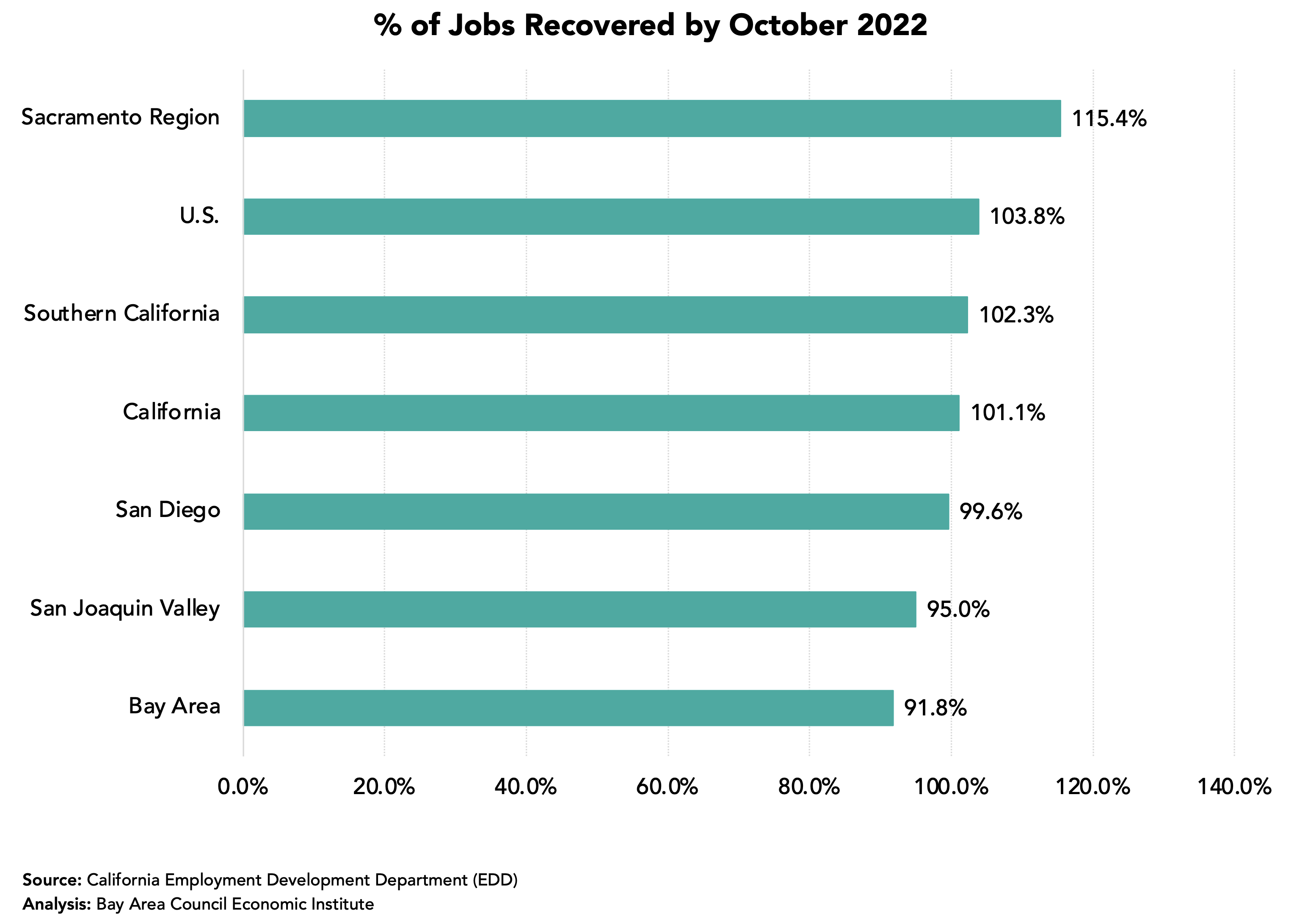

The Bay Area added 178,000 jobs in the past year (+4.6%) led by a gain of 67,300 in the San Francisco metro area though SF has recovered just 91.3% of the jobs lost between February and April 2020. The San Jose metro area added 53,700 jobs and by October 2022 had recovered 104.2% of the payroll jobs lost between February and April 2020. The Oakland metro area added 42,800 jobs during the past year. Other metro areas have been slower to recover lost jobs.

Unemployment Trends

Unemployment rates ticked up a small amount in October but remain low by historical standards. The October 2022 rate of 2.6% for the region is below the February 2020 pre-pandemic rate of 2.7%.

Bay Area and State Labor Force Still Below Pre-Pandemic Levels but Where Will Workforce Growth Come From.

The state has more than 200,000 fewer workers than in the month before the pandemic started and the Bay Area has more than 50,000 fewer residents in the workforce.

Though the recent pace of job growth has been encouraging, it is not clear where new workers will come from with low unemployment already and low population growth. Perhaps the new school year going back towards normal will allow parents who dropped out to return to the workforce. And it is possible that more workers can come from remote locations so the Bay Area and state can see job growth without more residents working. Job openings remain high and sectors like air travel are constrained by lack of enough workers. Increasing the level of immigration would be a large help to the region and state.

A Welcome Uptick in Housing Permits

Permits levels in the first nine months of 2022 exceeded 2019 and 2021 levels though East Bay permit levels were below earlier levels. The other counties showed large year over year gains. In addition, now there are almost daily reports of new housing projects being proposed and approved though it is often a long step until these units are completed and on the market. Bay Area cities are updating their Housing Elements currently and learning about the requirements to meet their RHNA goals. It is possible that the RHNA and update process is encouraging cities to loosen development standards and to approve more projects. While the current growth in permits is a positive sign, these levels are still below the RHNA targets for the region. More needs to be done.

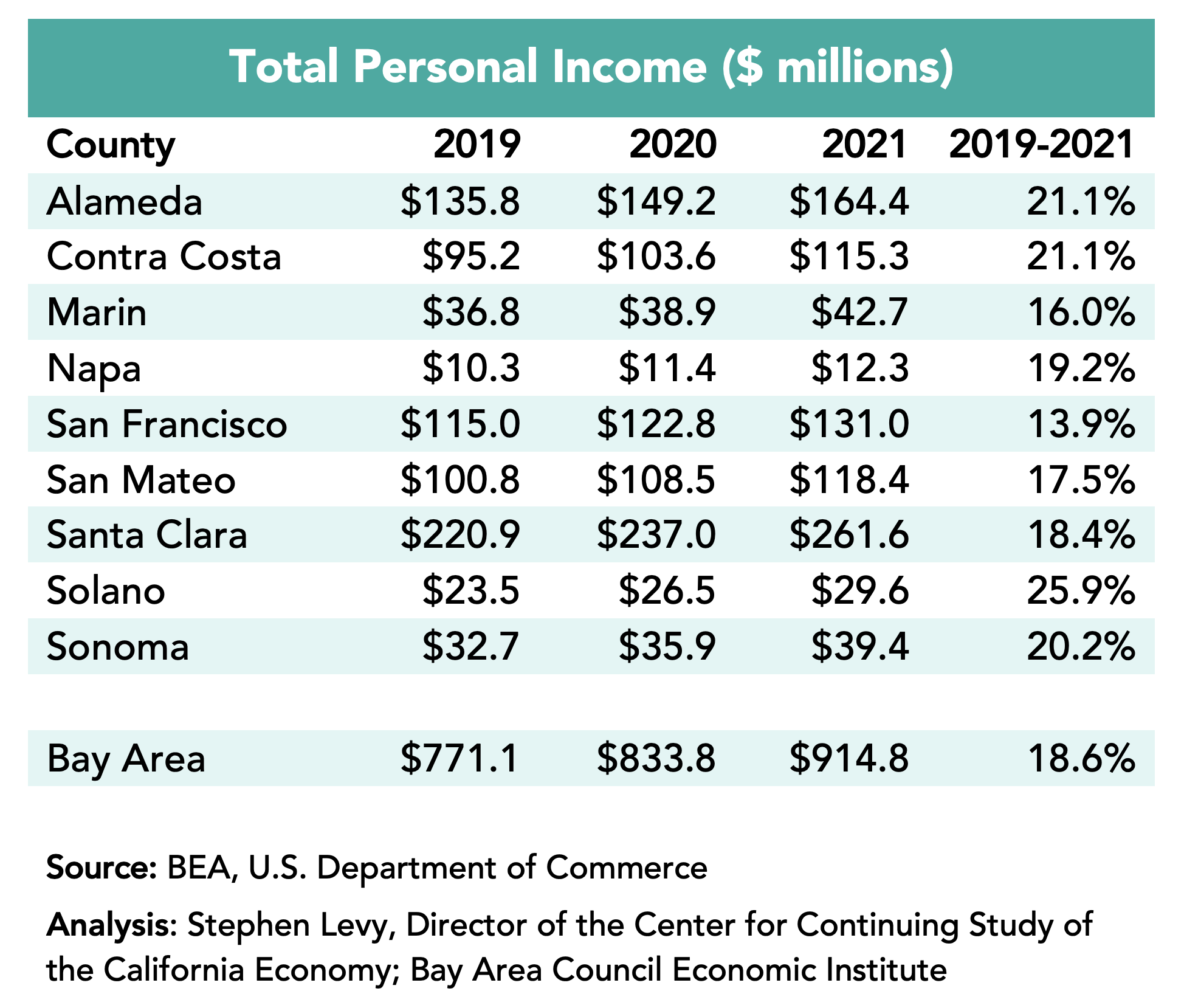

Strong Gains in Income in 2021

Total Personal Income rose by 18.6% in the region between 2019 and 2021 according to estimates released by BEA on November 16th this year. And per capita income rose by even more as most counties lost population during this period.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

We scored regions on 15 different datapoints across 5 different metrics: Jobs, People, Investment, EconomicActivity, and Costs. We use Metropolitan Statistical Areas (MSAs) as defined by the U.S. Office of Management and Budget (OMB). The San Francisco-Oakland-BerkeleyMSA includes San Francisco, Alameda, Marin, Contra Costa, and San Mateo counties. The San Jose-Sunnyvale-Santa Clara MSA includes Santa Clara and San Benito counties.

The Bay Area, which is referenced in other parts of our study, refers the the 9-county region (San Francisco, Alameda, Marin, Contra Costa, San Mateo, Santa Clara, Solano, and Sonoma counties).

The 9-county Bay Area

Each region was scored on 15 different metrics across 5 different categories. Percentile ranks were calculated for each metric (wherein 0 is the lowest rank, 100 is the highest), and then averaged across each category. Not all metrics were weighted equally, see the table below for a list of sources and weights.

Austin, Texas ranked first across the 25 regions in our study, scoring an average of 86 (out of 100) across the 15 metrics we evaluated. Within these metrics, it ranked first (100/100) on 6 metrics: job growth, “knowledge worker” growth, population growth, labor force growth, net absorption, and new housing units per capita. It also scored high (second only to Denver) on change in sales tax revenue – experiencing an increase of $33 million (or 13%) from 2019 to 2021. These figures speak to the dramatic resilience and growth Austin, and Texas as a whole, experienced during the pandemic, while coastal cities like San Francisco and New York continue to suffer losses.

Why did we pick the metro areas in our analysis?

To create a list of “peer” regions to the San Francisco metropolitan area, we gathered a list of the 25 largest regional economies, based on the latest GDP numbers available at the time:

Explore charts of every metric that went into the index:

Jobs:

People:

Investment:

Economic Activity:

Affordability:

August 29, 2022

The highlights:

• The Bay Area added 20,000+ jobs in both June and July and led all regions in California with a 5.2% 12-month job increase.

• Bay Area unemployment levels and unemployment rates remained low even with the normal summer uptick and the state unemployment rate, which is seasonally adjusted, fell to a record low of 3.9%.

• In May Bay Area unemployment levels and unemployment rates fell to record lows.

• Housing permits for the first six months of the year surpassed both 2021 and 2019 levels though still well below the region’s new RHNA targets. Air travel levels picked up though Bay Area passenger levels remain well below pre-pandemic levels.

• August 2022 brings major challenges to the global, national and regional economy with the Russian invasion of Ukraine, increases in interest rates amidst continuing high inflation, and the Bay Area challenges of housing, transportation and competitiveness. Positive signs are that inflation may be slowing, Ukrainian grain is hitting the market, COVID cases have started to decline and K-12 schools are in a more normal school year.

• Another challenge, discussed below, is where will employers find workers for continued job growth.

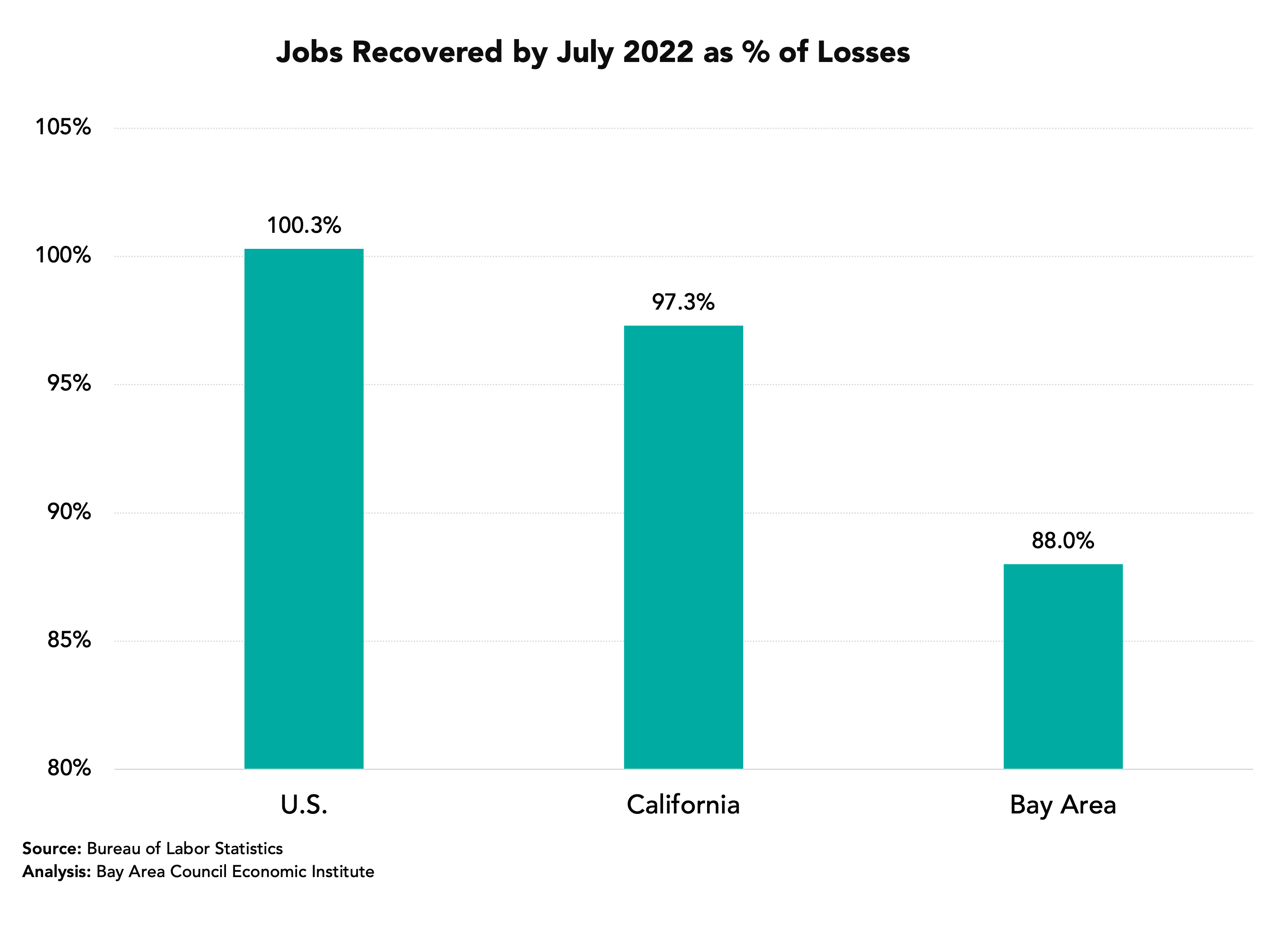

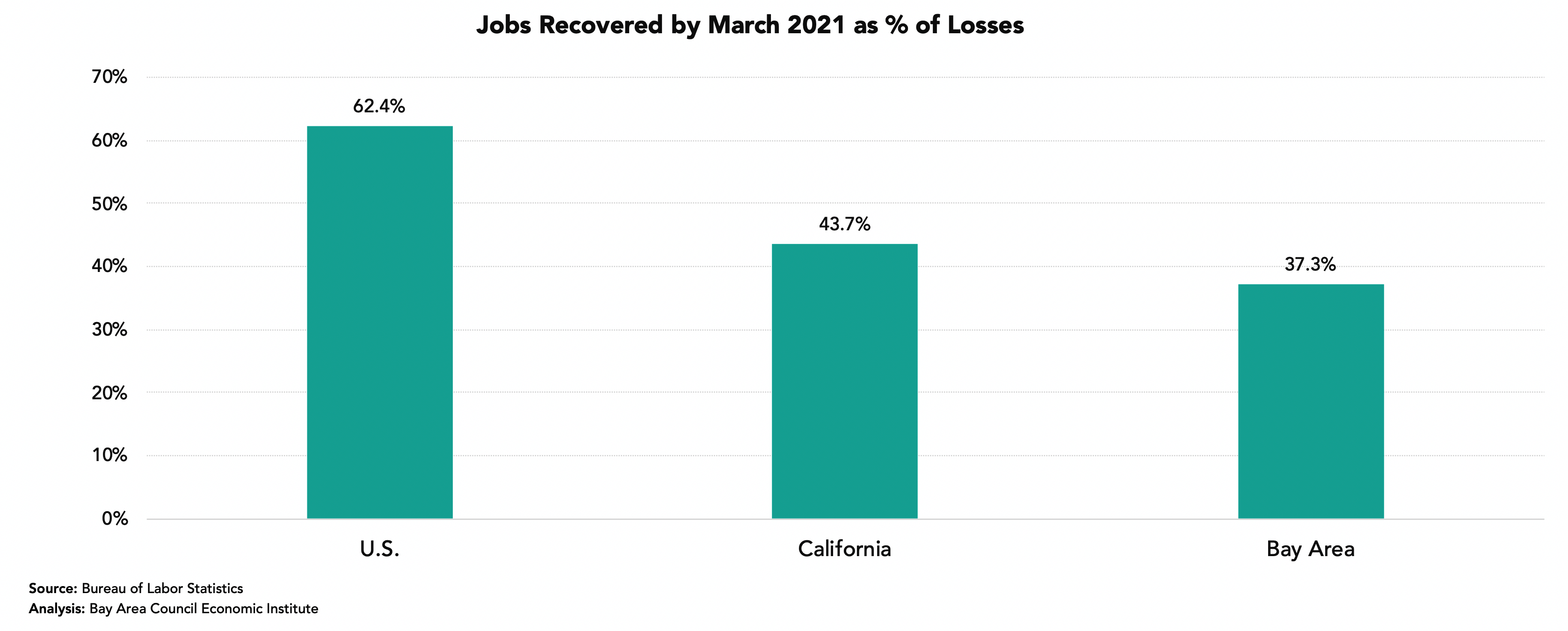

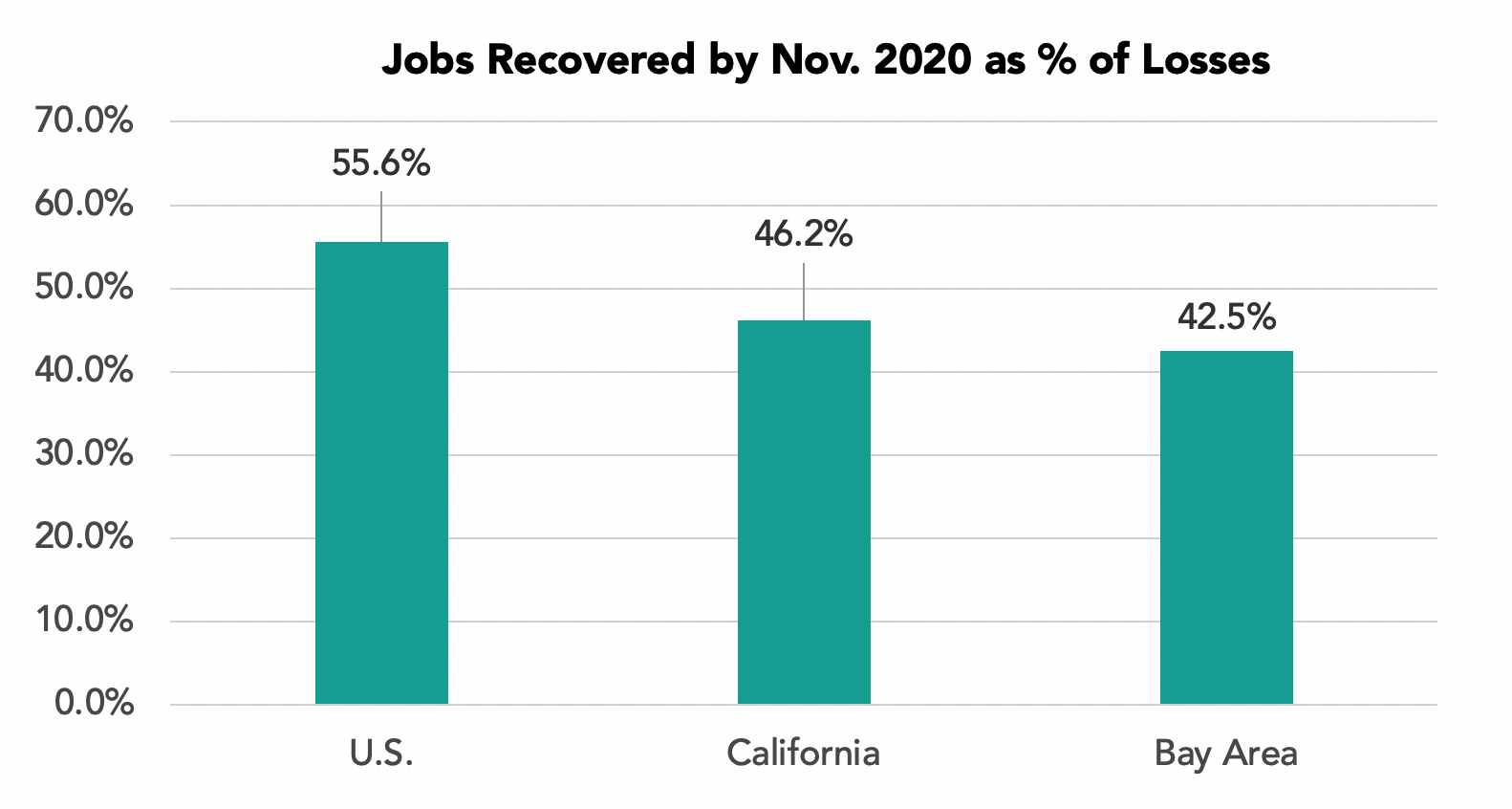

The Bay Area Trails the State and Nation in Payroll Job Recovery but the Gap is Shrinking

This is the chart that gets wide media attention and focuses on our region’s below-average job recovery rate. It is accurate and shows the better U.S. and California data. But look at the next chart to see the Bay Area catching up.

The Bay Area’s 5.2% growth rate topped all the other major economic regions in the state as well as the state and national job growth rate.

Payroll Job Growth Shows Even Recovery by Metro Area

The Bay Area added 199,200 jobs in the past year (+5.5%) led by a gain of 76,200 in the San Francisco metro area though SF has recovered just 85.8% of the jobs lost between February and April 2020. The San Jose metro area added 62,000 jobs and by July 2022 had recovered 97.0% of the payroll jobs lost between February and April 2020. The Oakland metro area added 44,800 jobs during the past year. Other metro areas have been slower to recover lost jobs.

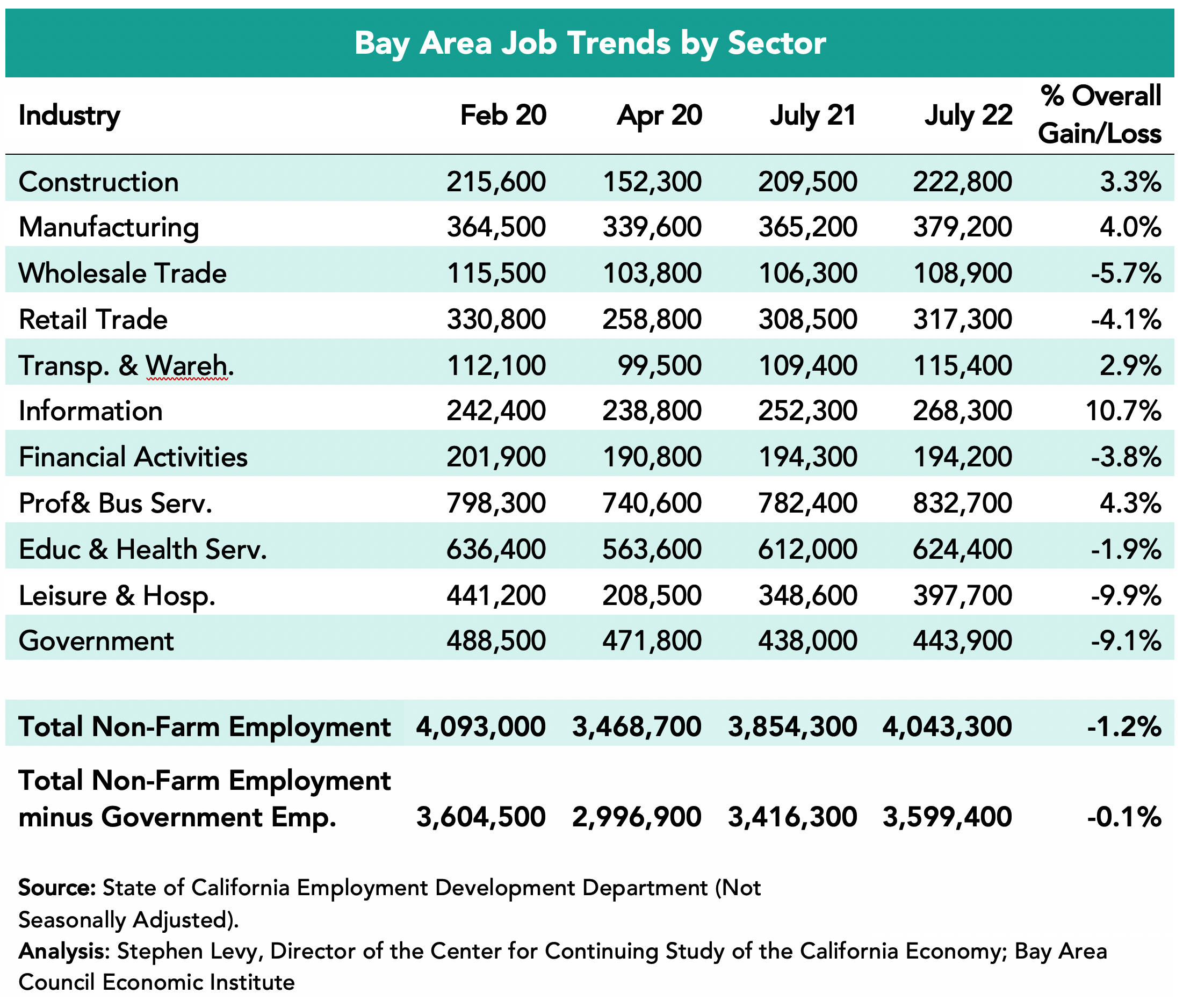

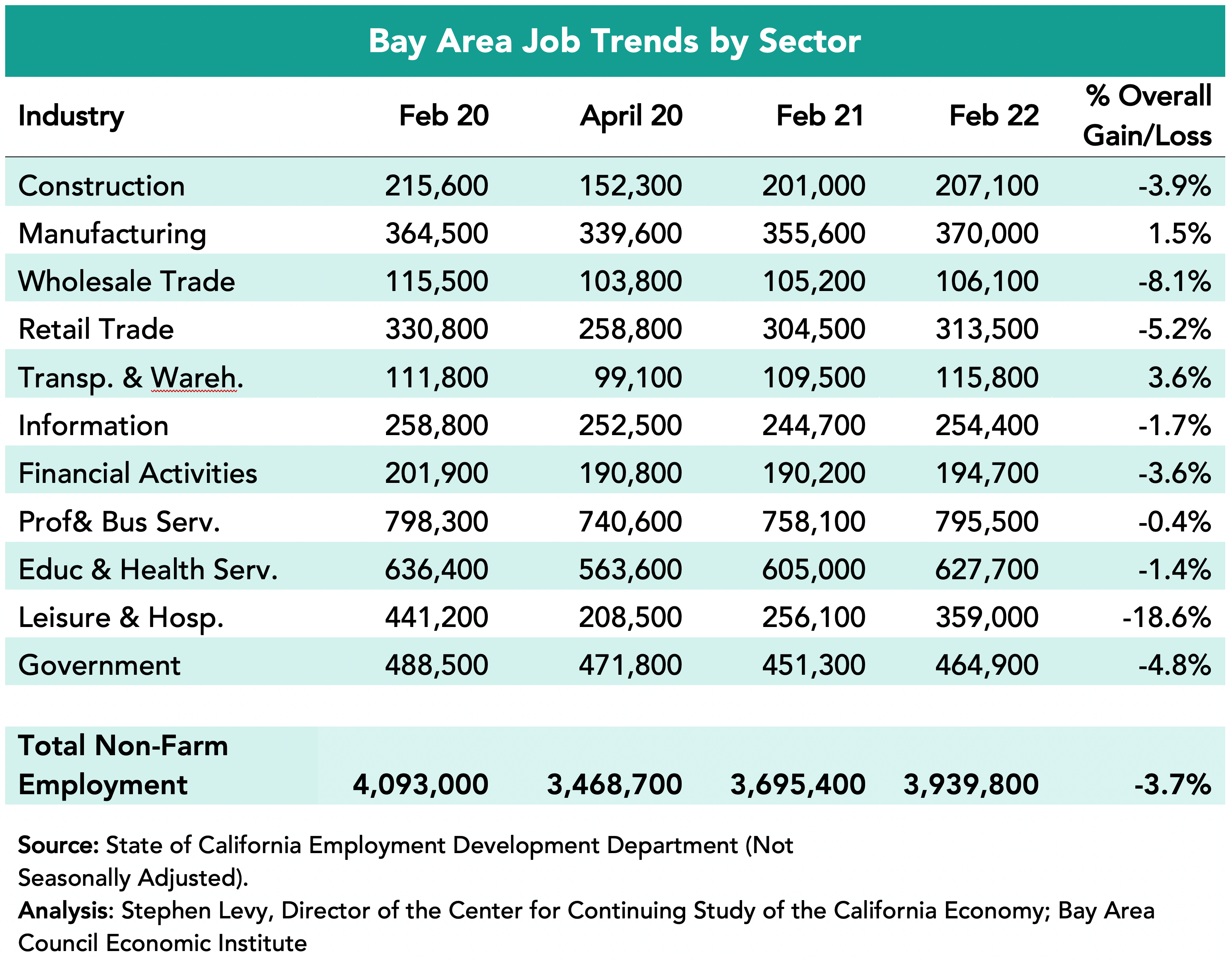

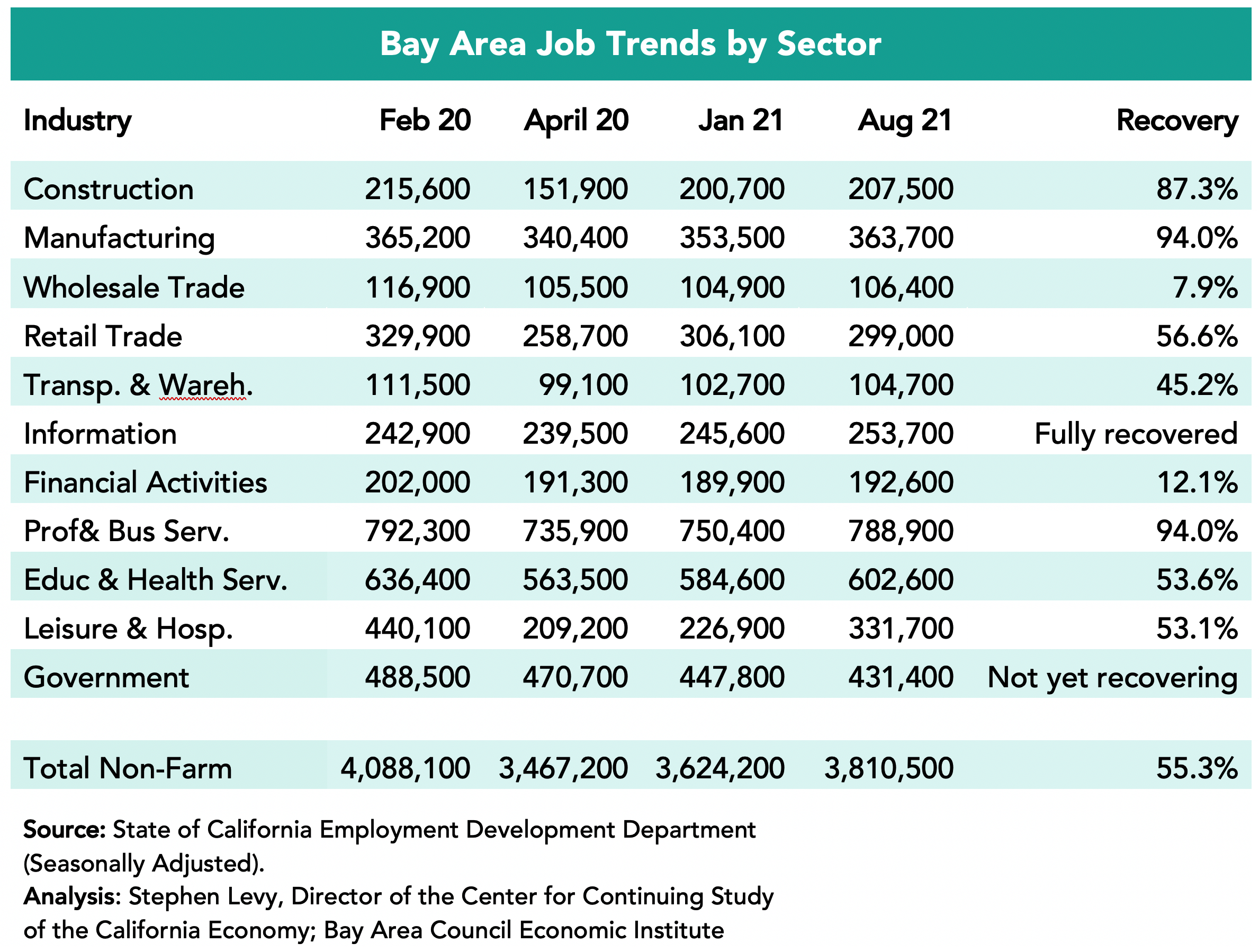

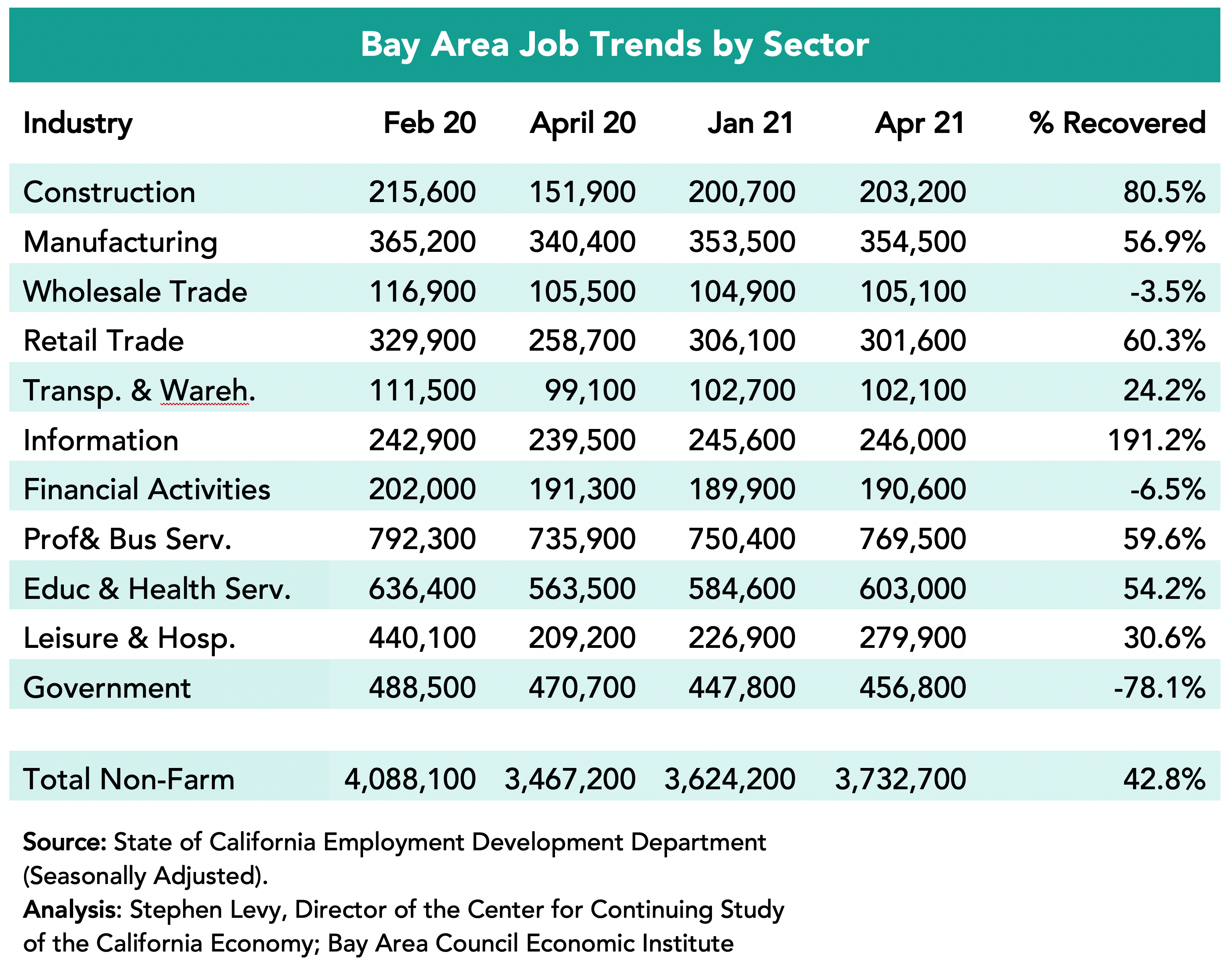

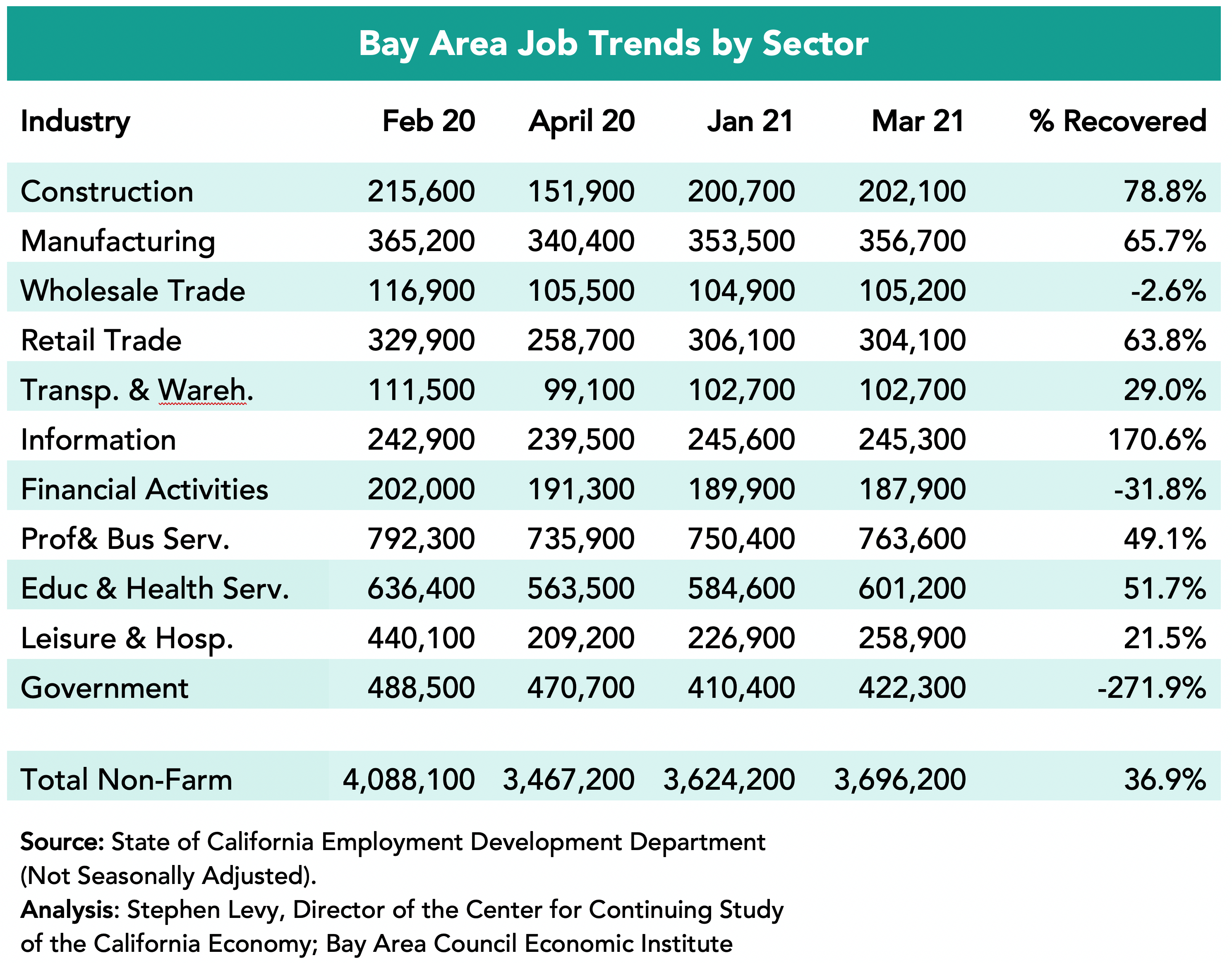

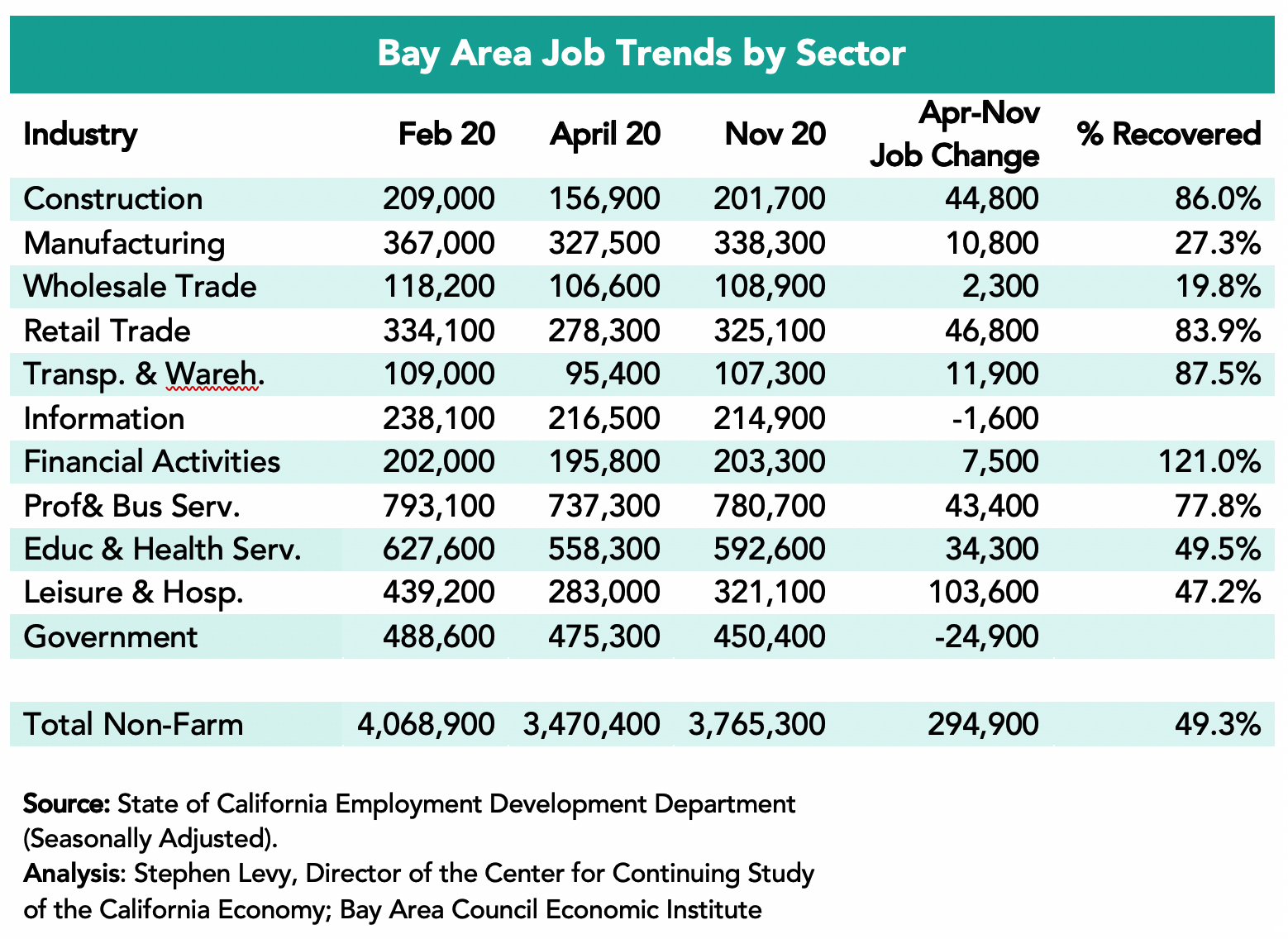

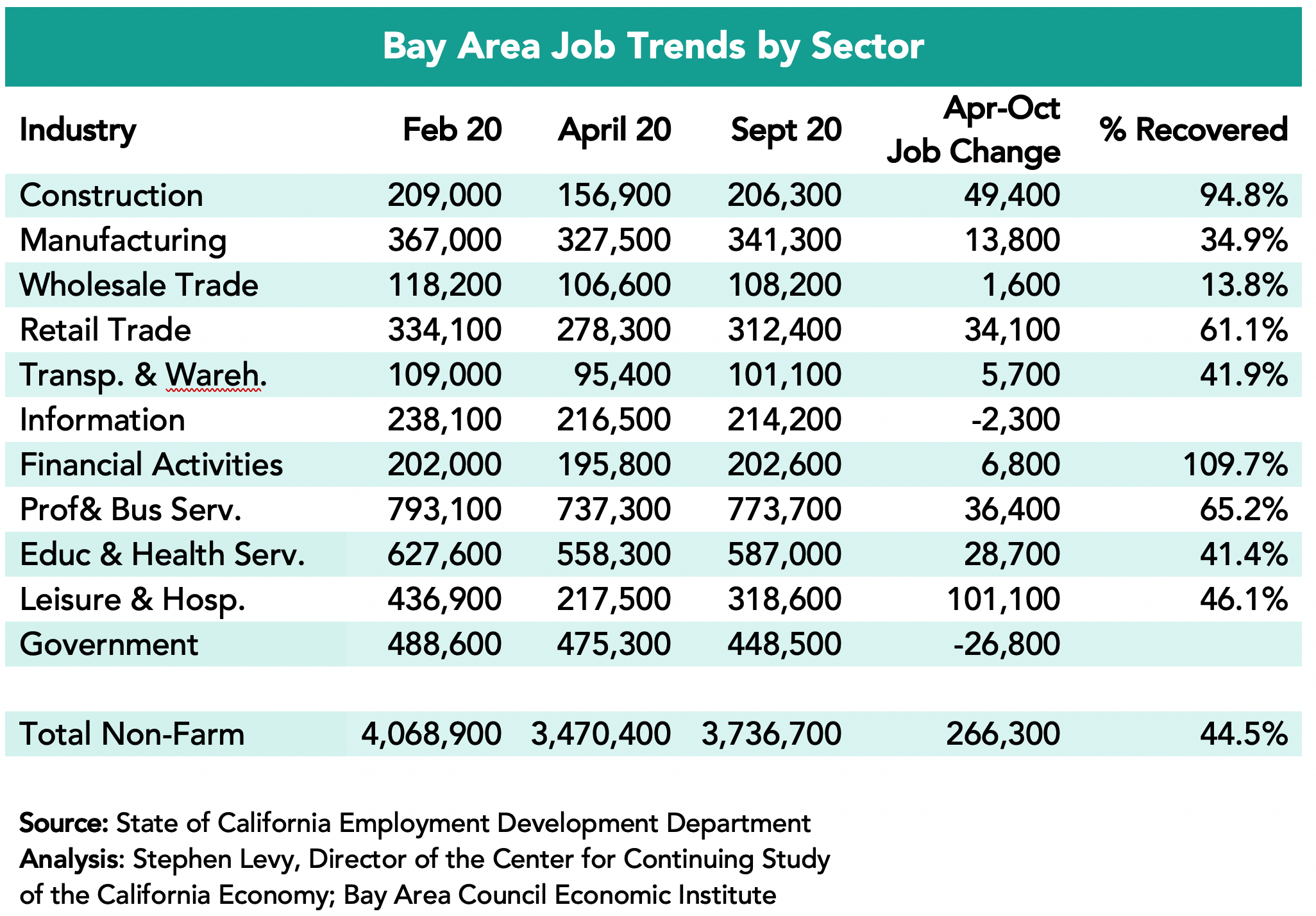

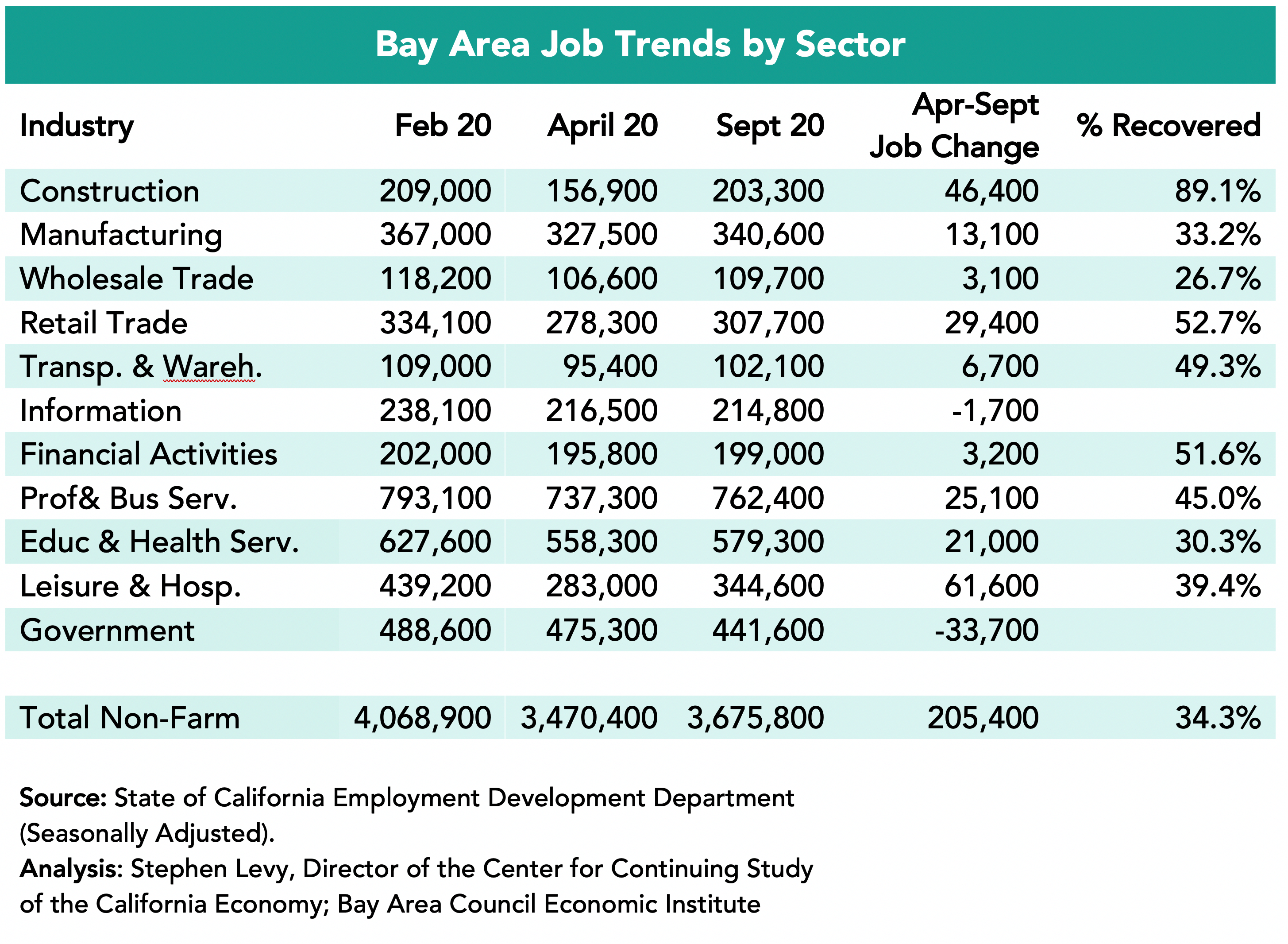

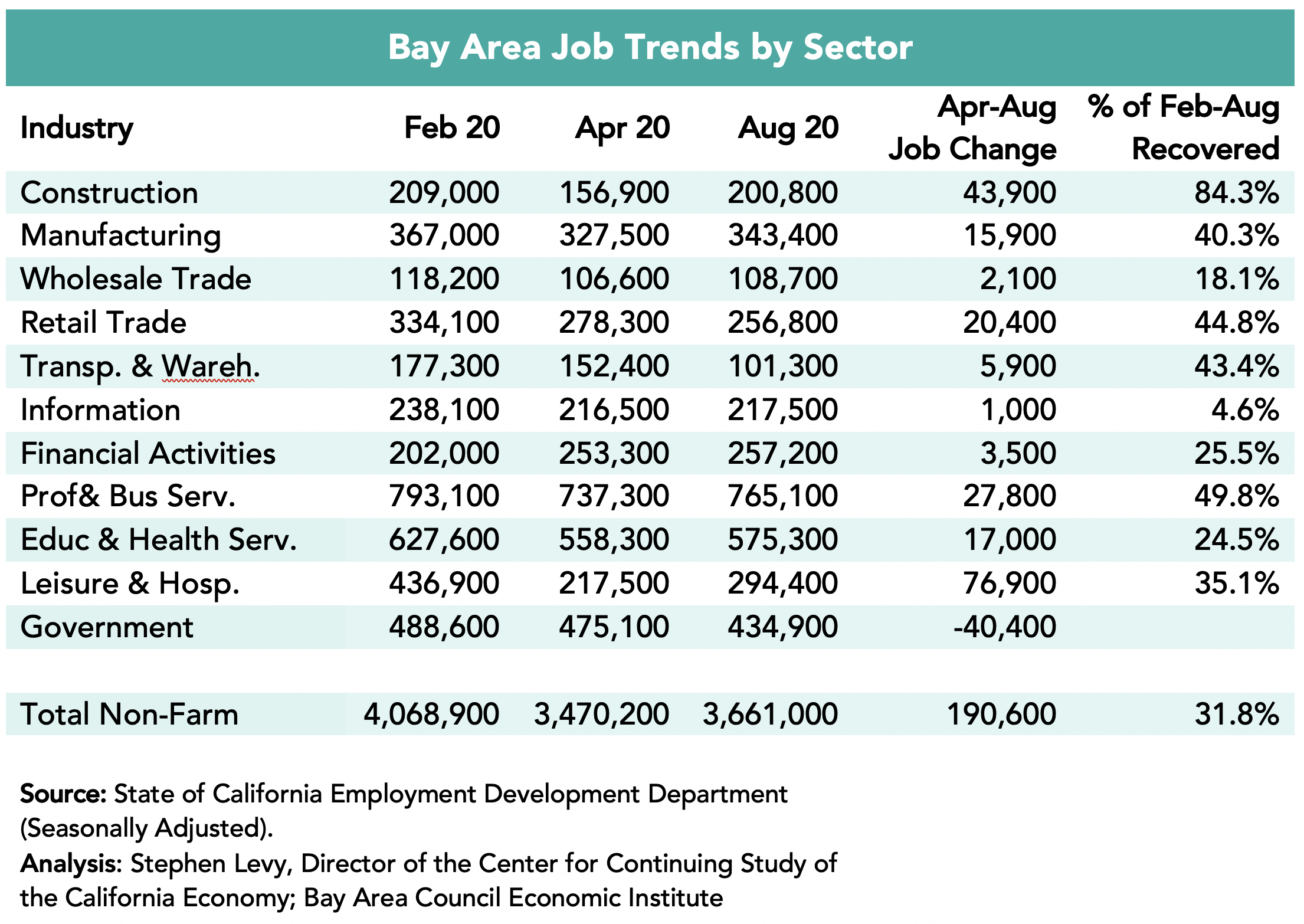

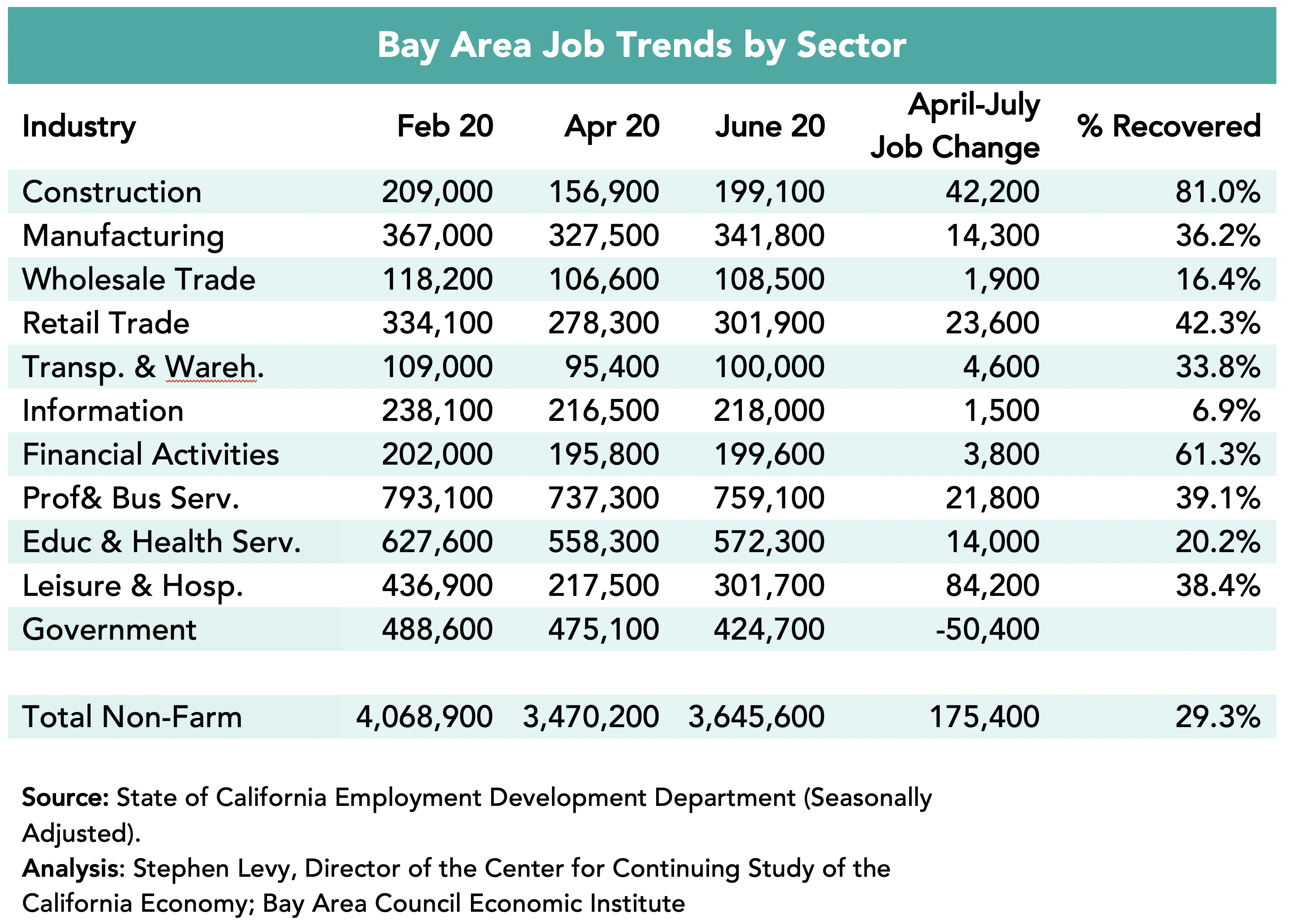

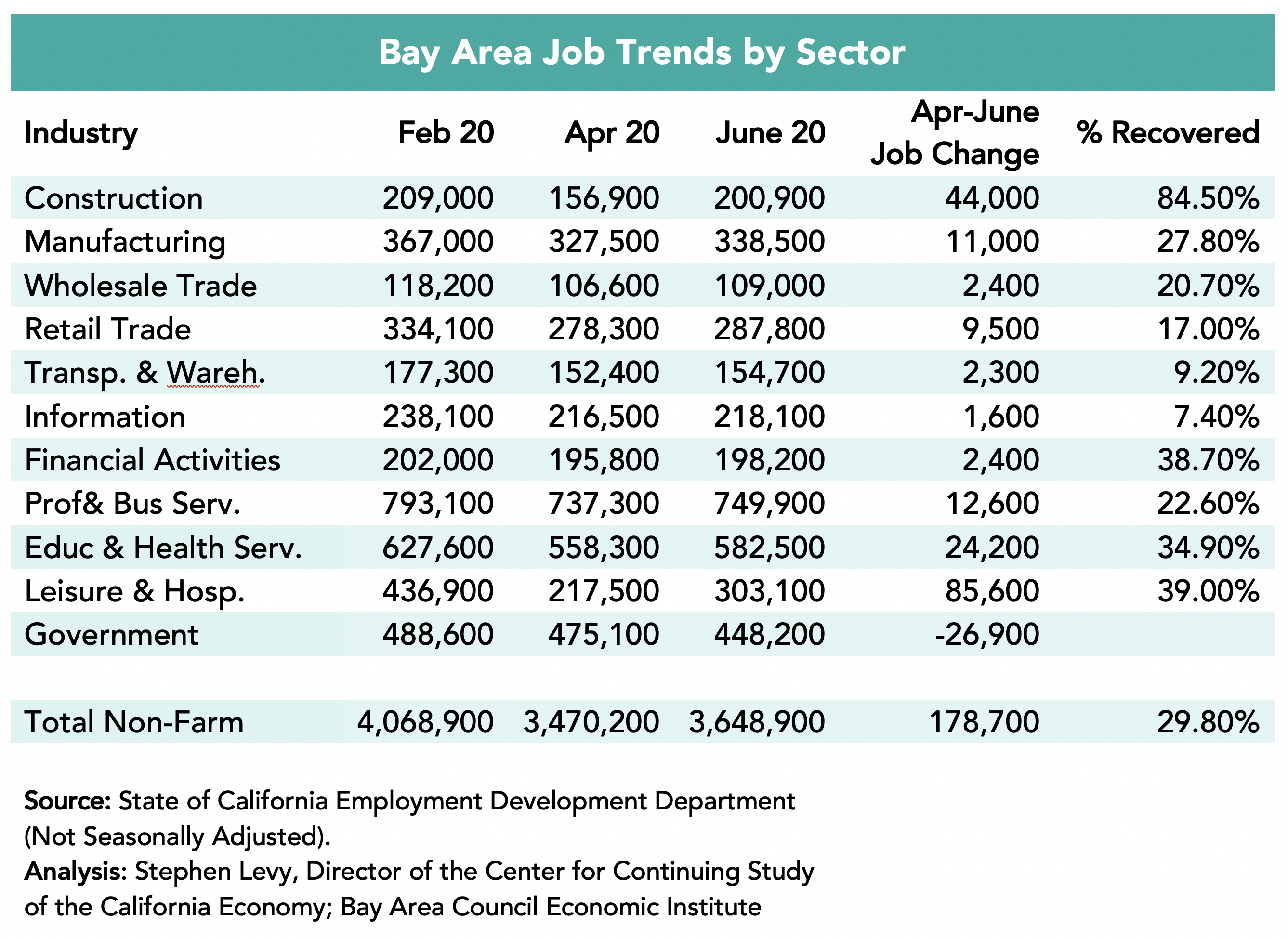

Industries Were Affected Differently

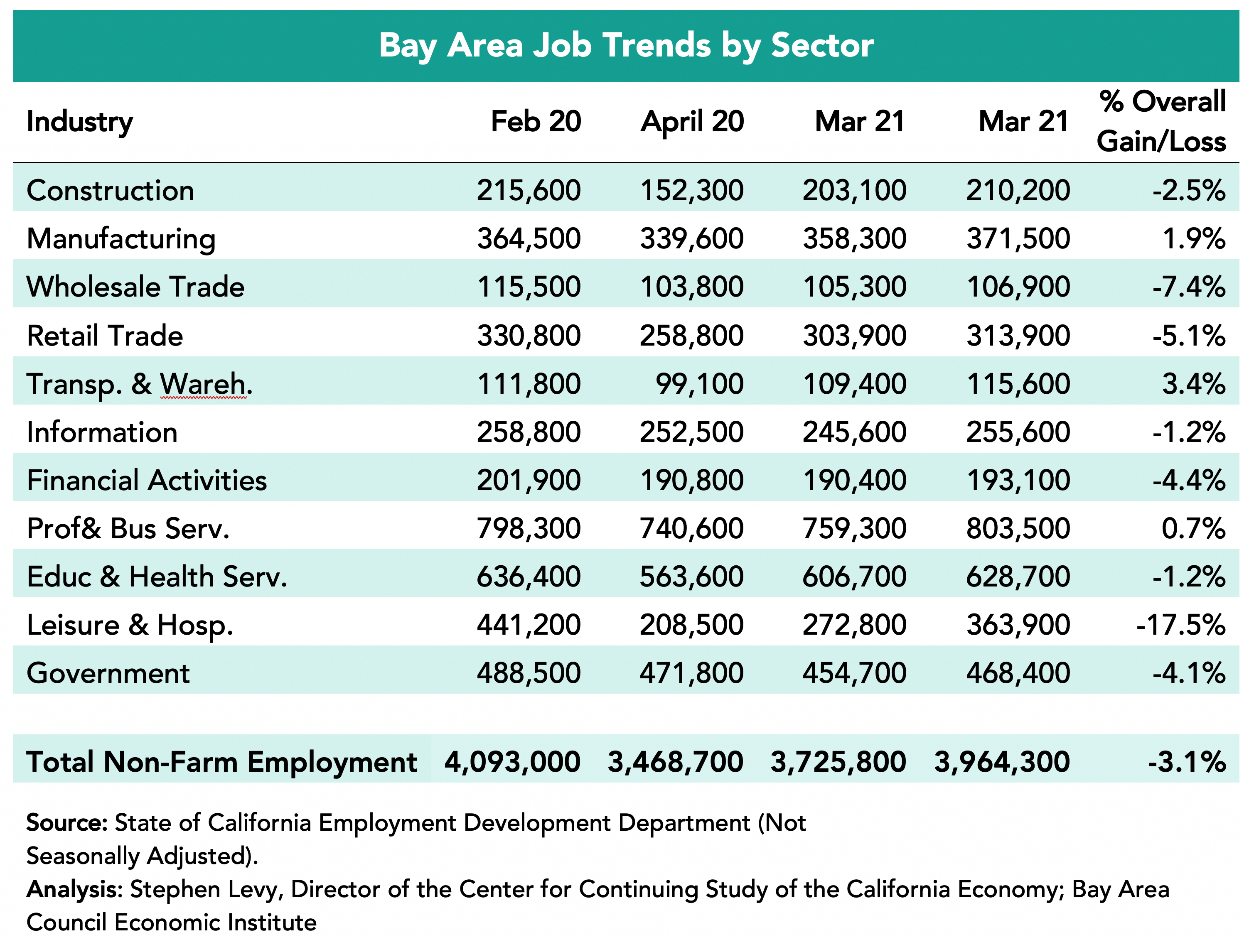

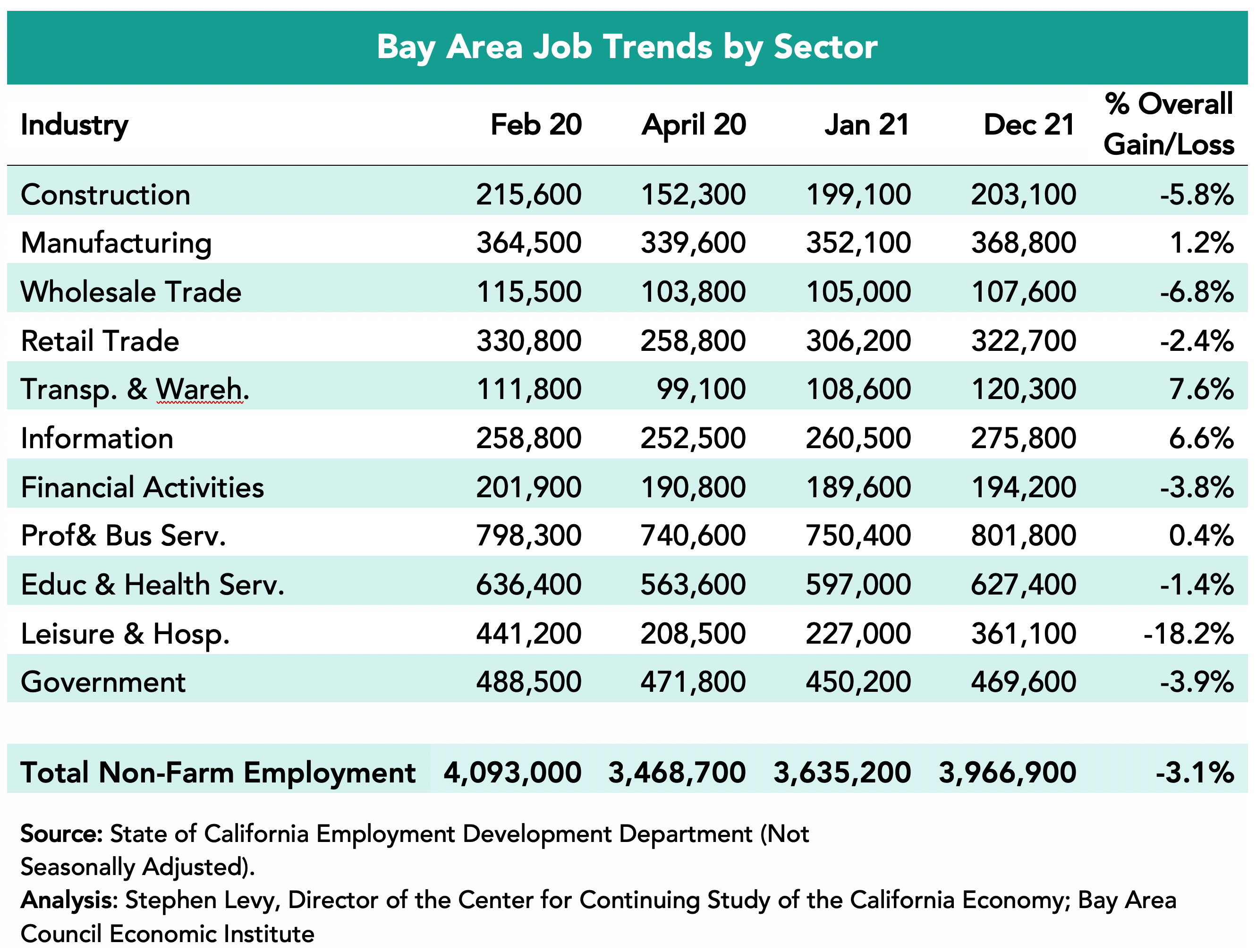

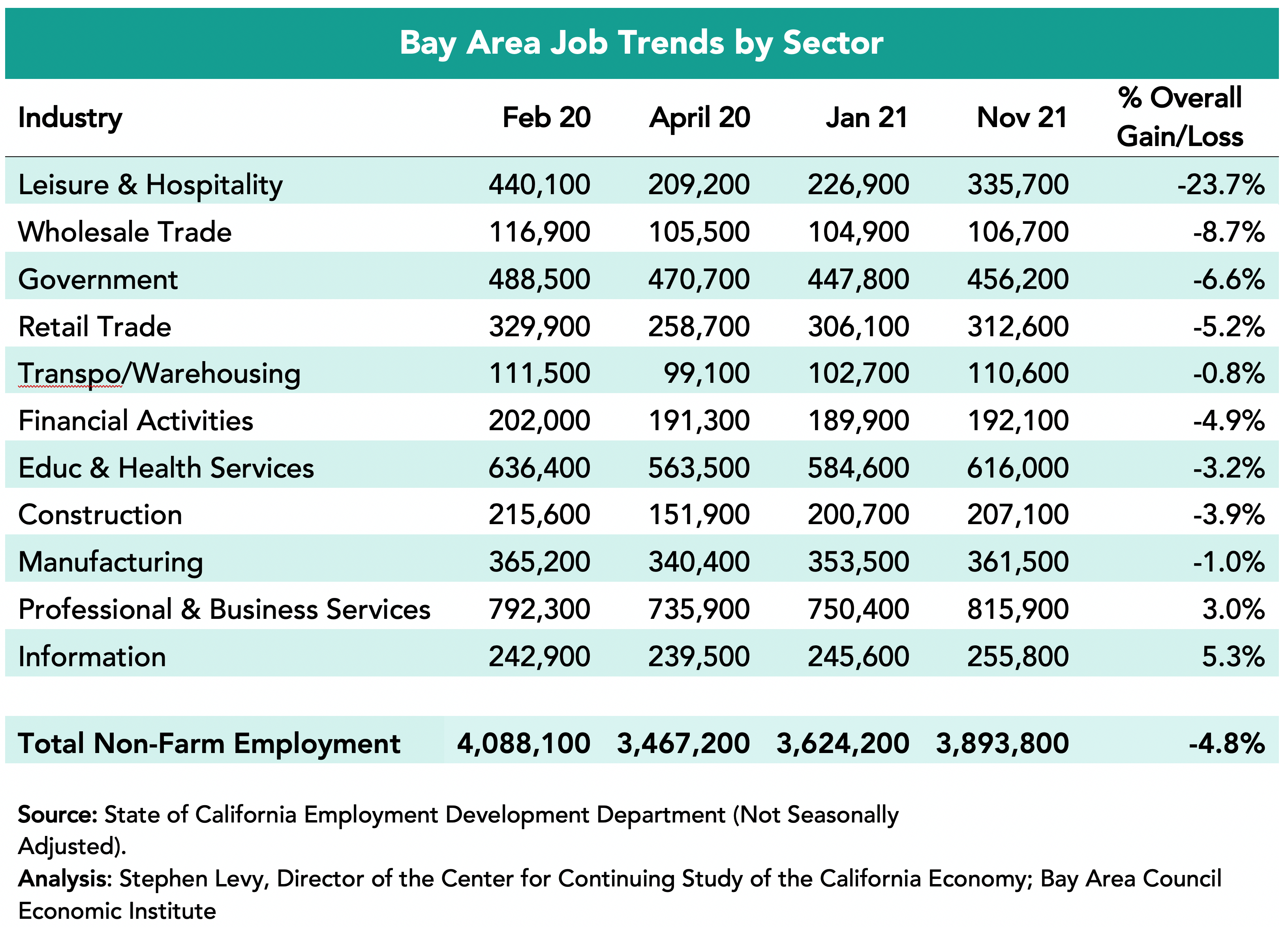

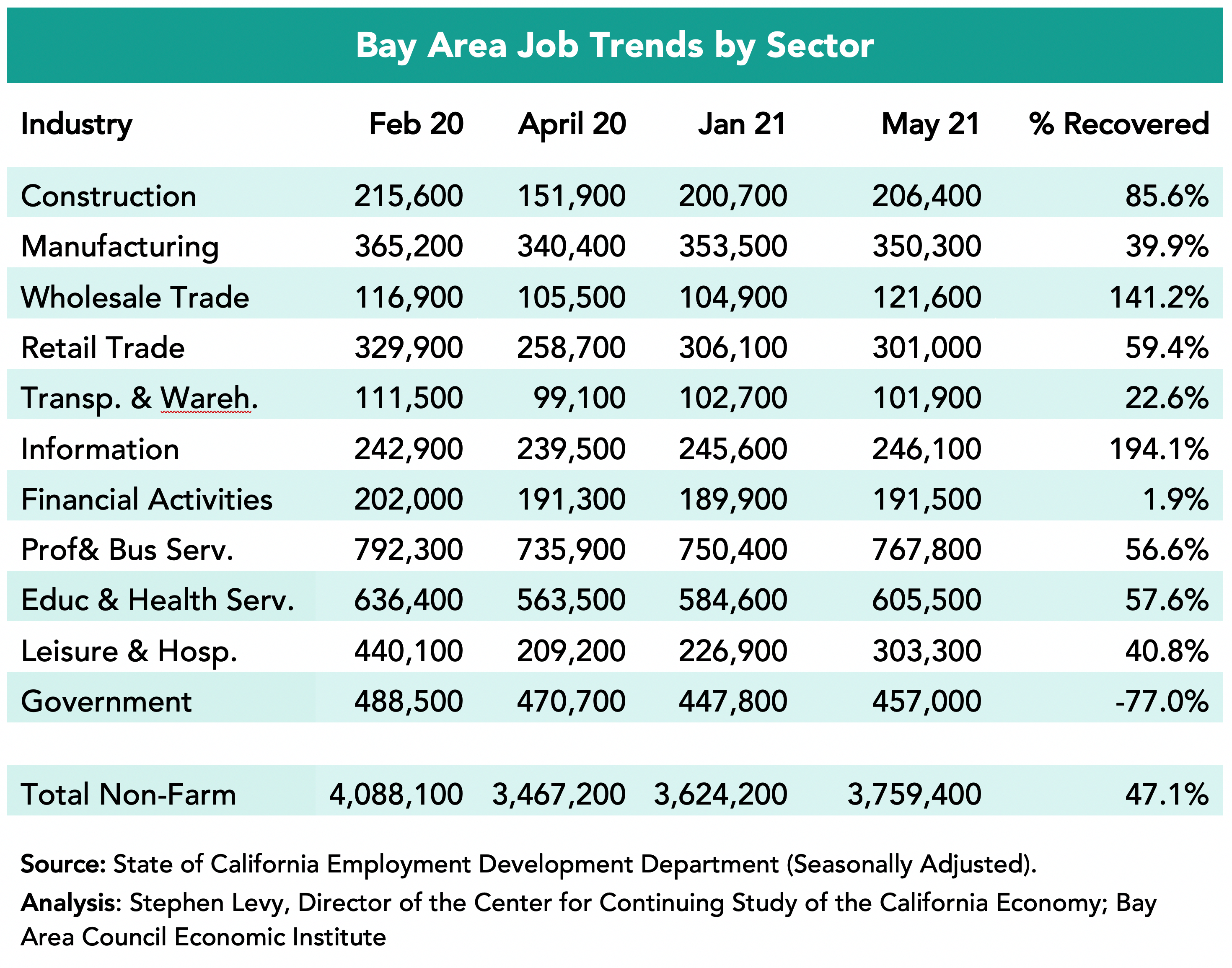

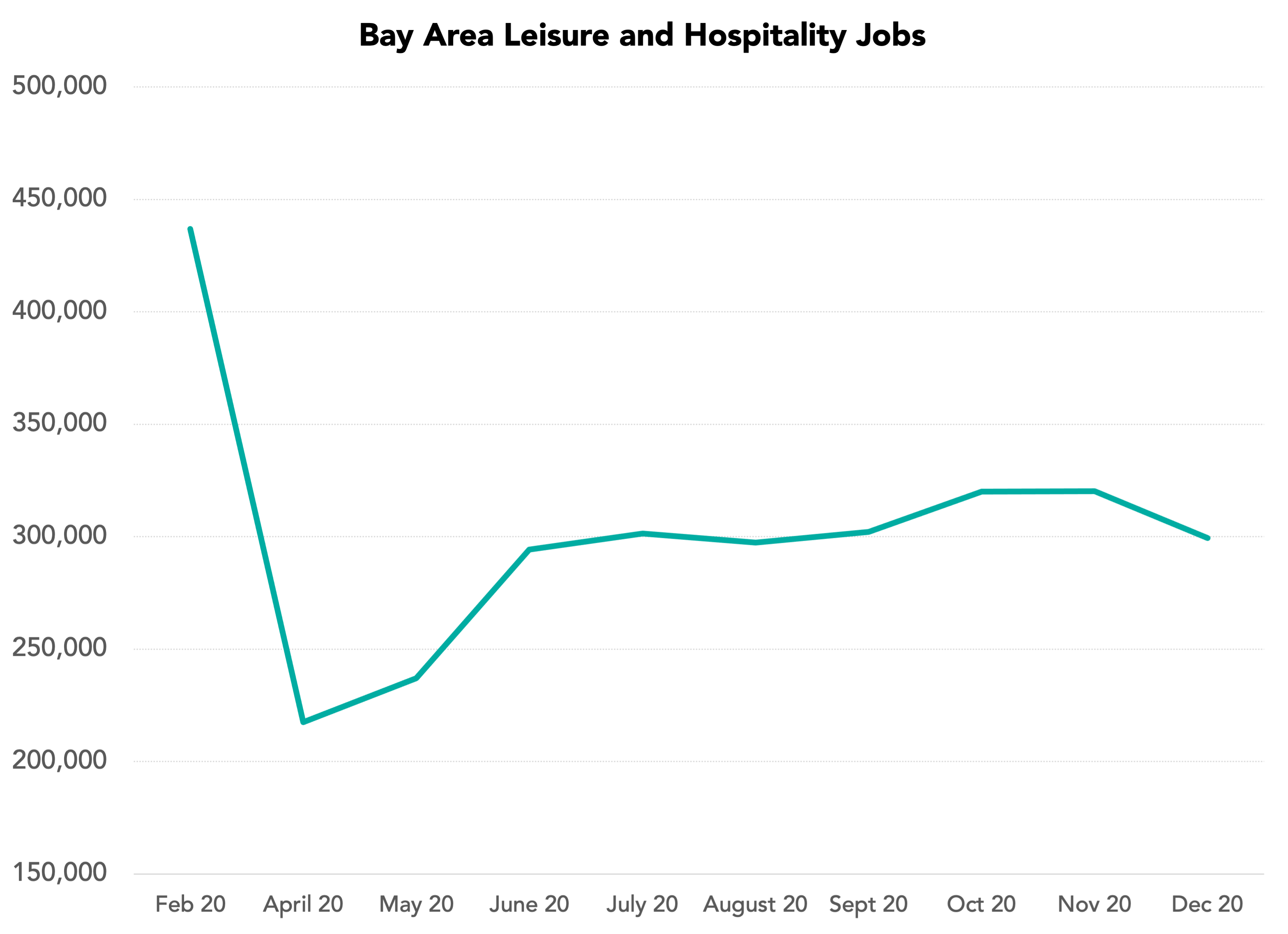

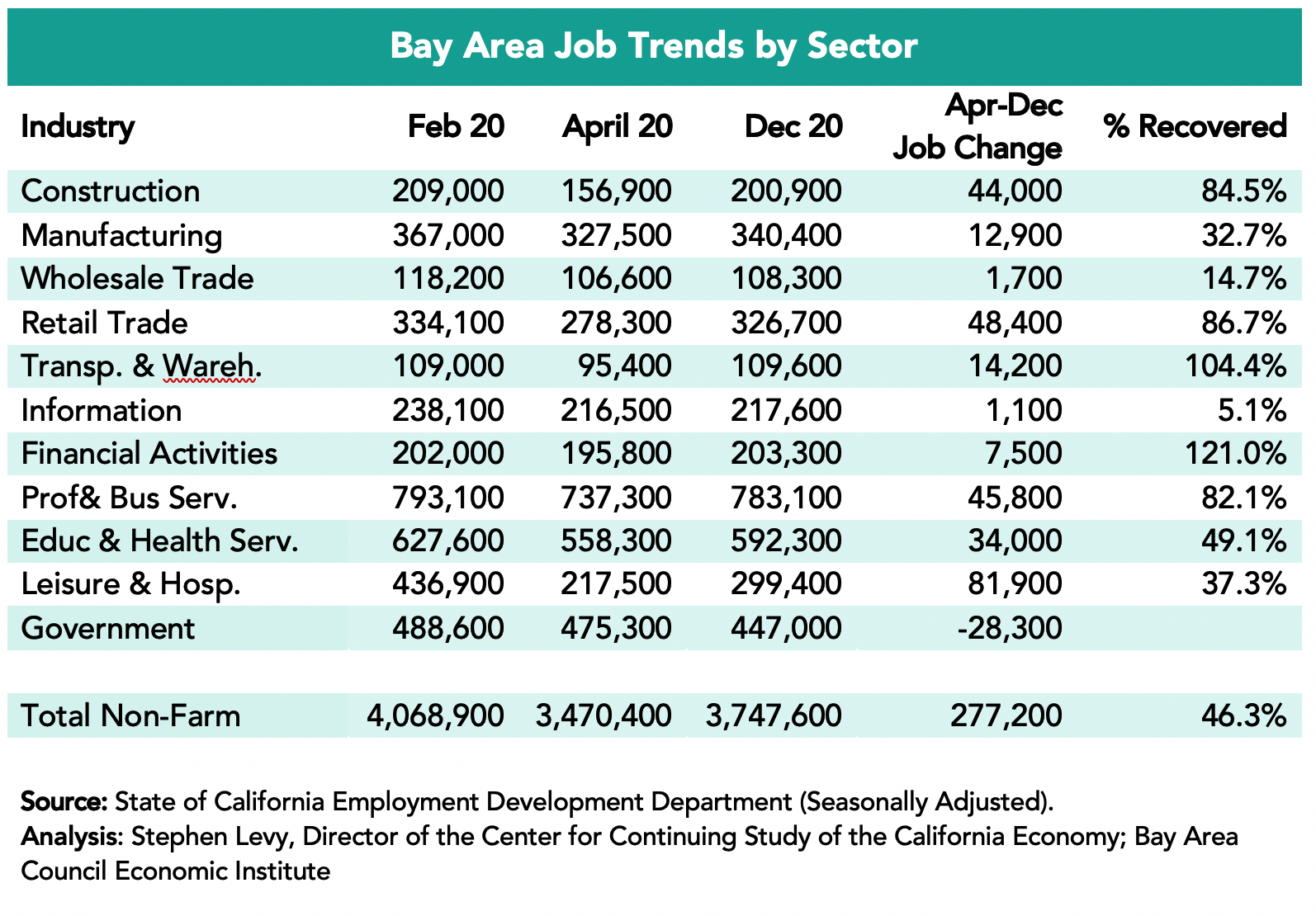

Five sectors—Construction, Manufacturing, Transportation and Warehousing, Information and Professional and Business Services—exceeded pre-pandemic job levels in July 2022. Financial Services at 30.6% had the lowest recovery rate and the Leisure and Hospitality sector has now recovered 81.3% of lost jobs by July 2022 and has the largest recent gains. The Government sector is now slowly recovering the jobs lost between February and April 2020.

Note that all sectors combined minus the government sector have now recovered nearly all the lost jobs as shown on the bottom row.

Unemployment Trends

Unemployment rates go up in the summer on the not seasonally adjusted data as education jobs decline during summer break. Still Bay Area rates in July 2022 were below pre-pandemic levels though the months are not comparable. And there were 104,700 unemployed residents in July 2022 compared to 114,500 in February 2020.

The state data that is seasonally adjusted reported a decline to 3.9%, an all-time low for the state unemployment rate in July 2022 from 4.2% in June 2022 and 4.1% in February 2020.

Bay Area and State Labor Force Still Below Pre-Pandemic Levels but Where Will Workforce Growth Come From.

The state has more than 200,000 fewer workers than in the month before the pandemic started and the Bay Area has more than 50,000 fewer residents in the workforce.

Though the recent pace of job growth has been encouraging, it is not clear where new workers will come from with low unemployment already and low population growth. Perhaps the new school year going back towards normal will allow parents who dropped out to return to the workforce. And it is possible that more workers can come from remote locations so the Bay Area and state can see job growth without more residents working. Job openings remain high and sectors like air travel are constrained by lack of enough workers

A Welcome Uptick in Housing Permits

Permits levels in the first six months of 2022 exceeded 2019 and 2021 levels though East Bay permit levels were below earlier levels. The other counties showed large year over year gains. In addition, now there are almost daily reports of new housing projects being proposed and approved though it is often a long step until these units are completed and on the market. Bay Area cities are updating their Housing Elements currently and learning about the requirements to meet their RHNA goals. It is possible that the RHNA and update process is encouraging cities to loosen development standards and to approve more projects. While the current growth in permits is a positive sign, these levels are still below the RHNA targets for the region. More needs to be done.

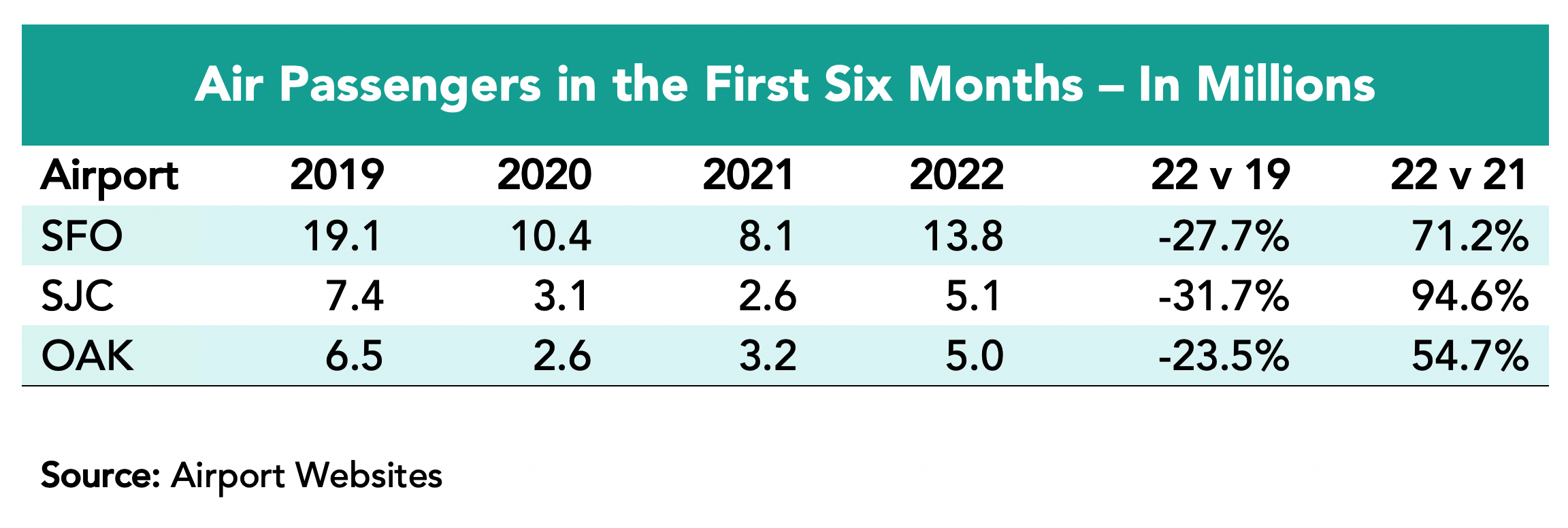

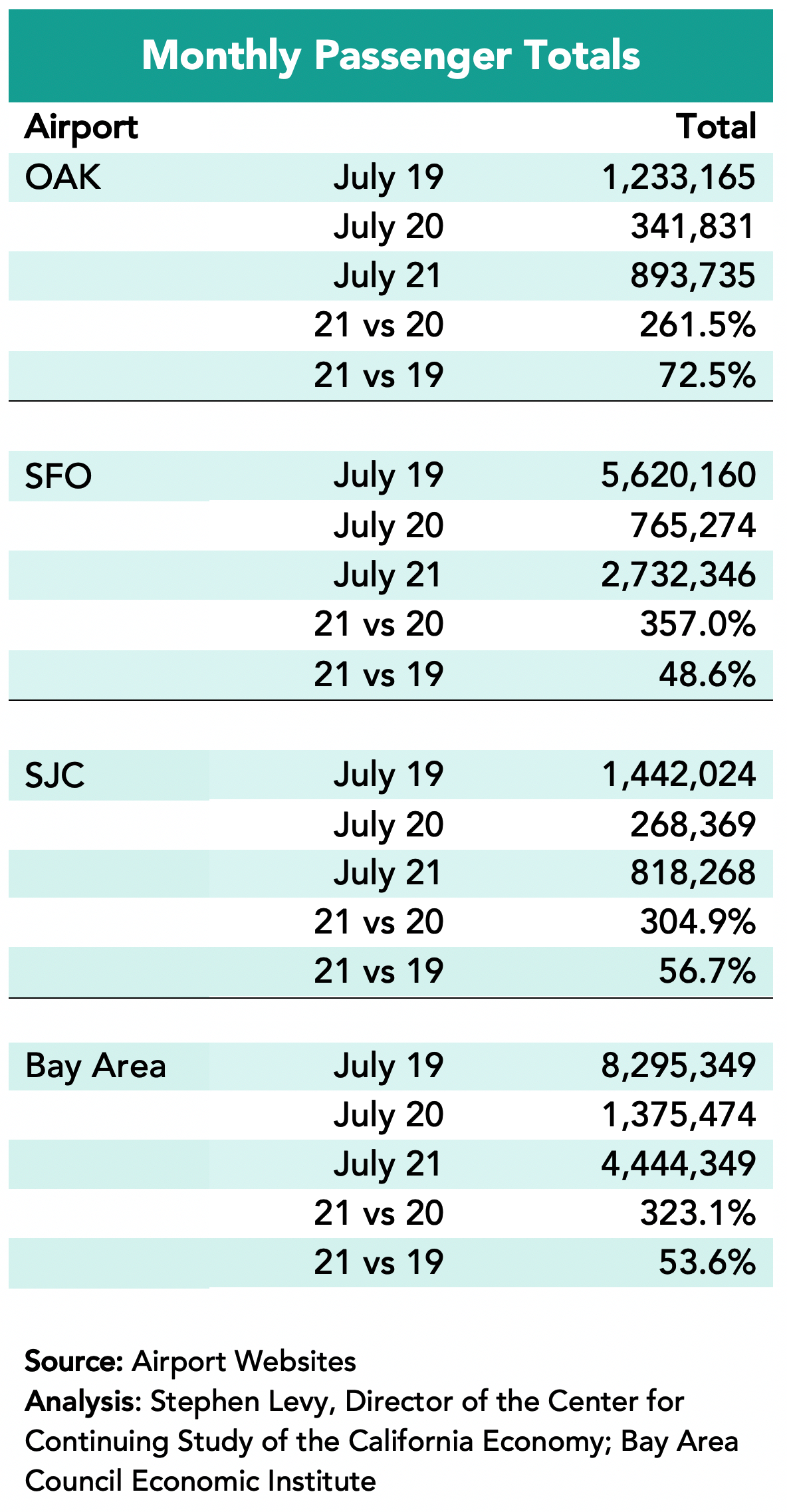

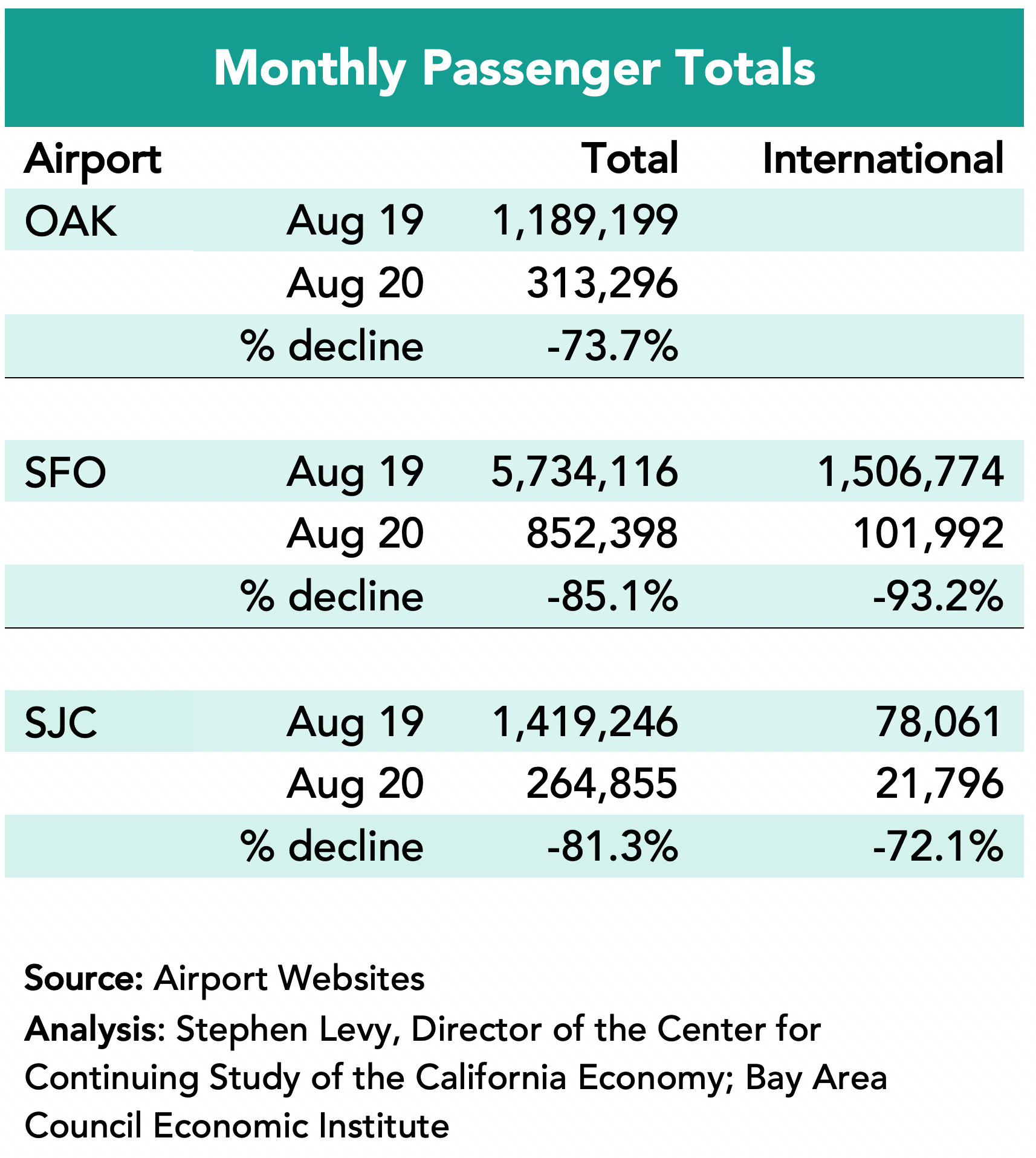

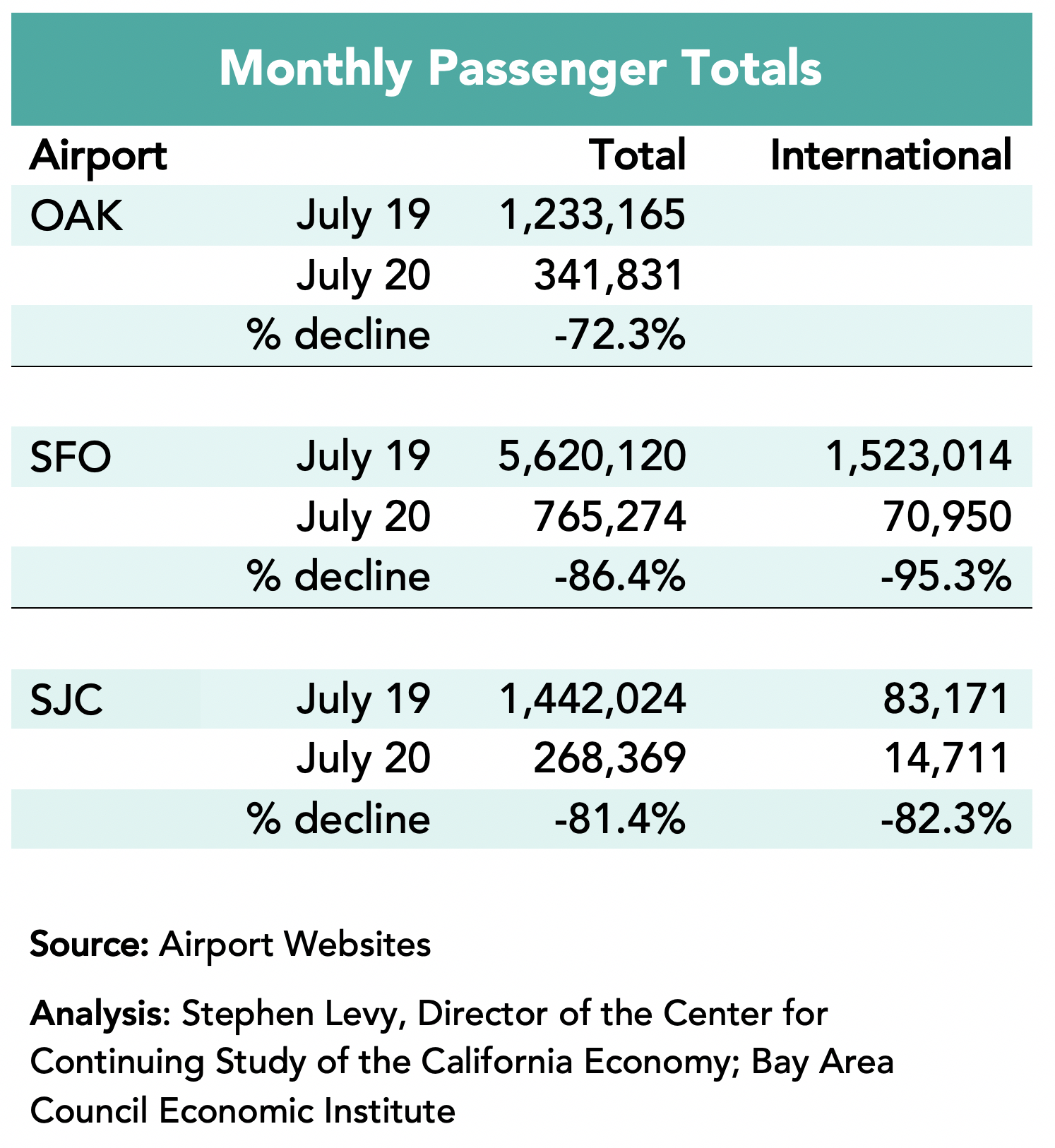

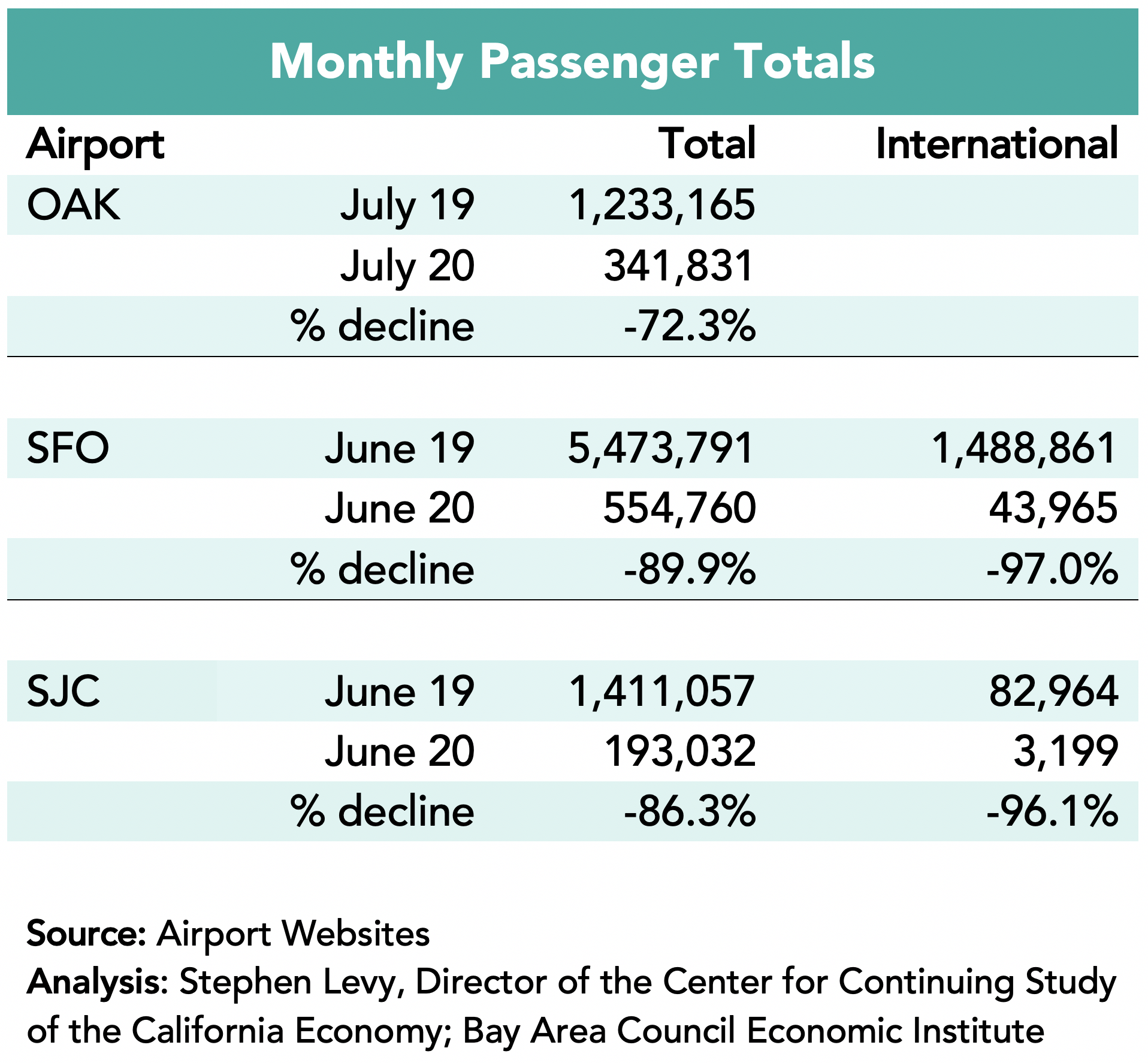

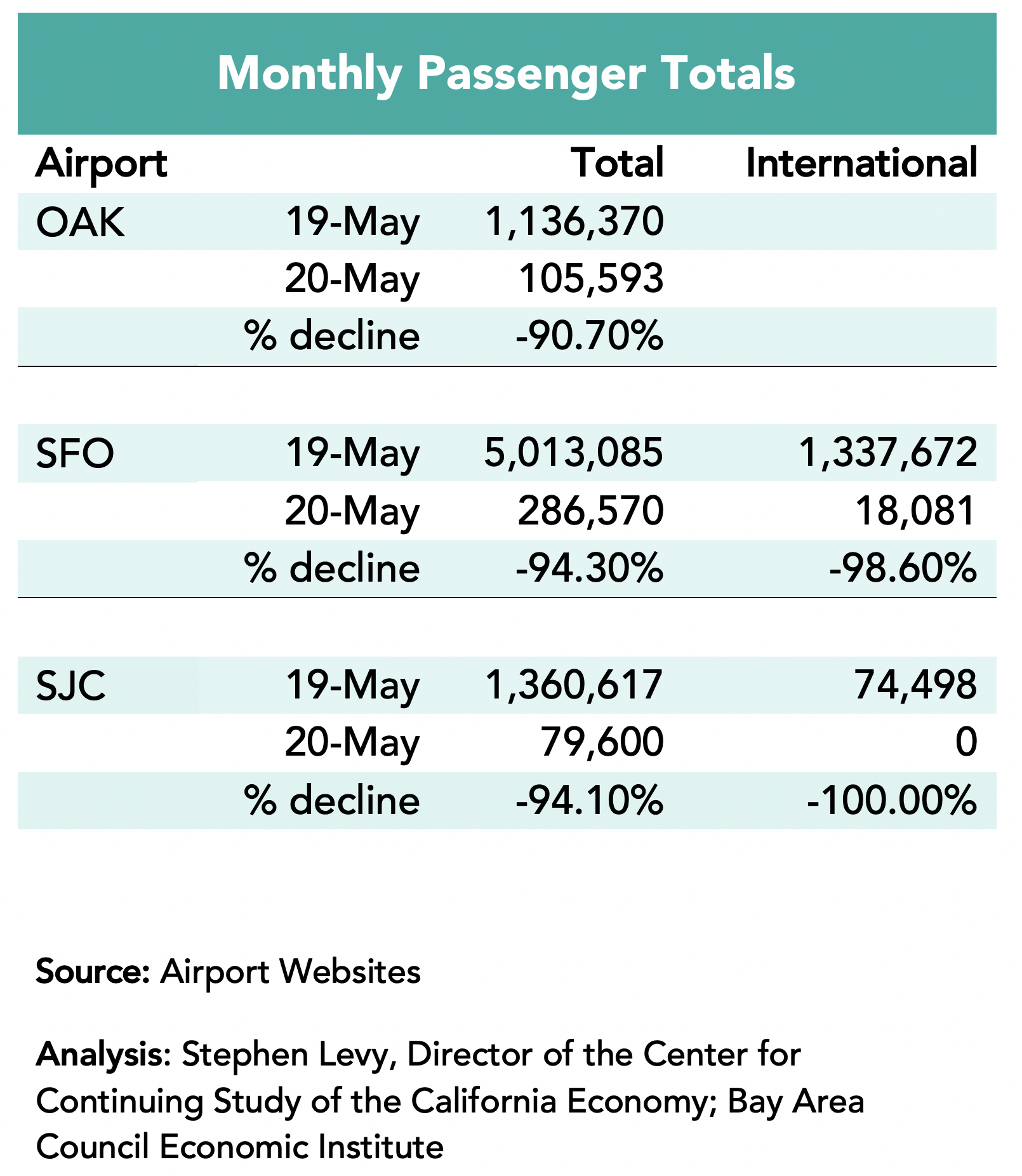

Air Travel Up but Well Below Pre-Pandemic Levels in the Region

Passenger levels are up over 2021 levels but still well below 2019 totals for the first six months of the year. Bay Area airports trail other regions in California in the recovery to pre-pandemic travel. A part of the reason is the large decline in international travel that is only recently beginning to grow again.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

August 18, 2022

With the economy in flux and the long-term effects of remote work still unknown, it’s fair to ask how the Bay Area – as the world’s leading hub for technology, entrepreneurship and innovation – is faring. In this commentary in the Times of India, Bay Area Council Economic Institute Senior Director Sean Randolph examines the hints provided from the current snapshot

The Bay Area Council and Bay Area Council Economic Institute understand well the importance of our region’s connections to the world in supporting and growing our innovation economy. In this commentary in the Silicon Valley Business Journal, Bay Area Council Economic Institute Senior Director Sean Randolph examines these connections and why they remain strong even during these turbulent economic times.

Payroll Job Growth Slumps but That is Not the Whole Story

June 27, 2022

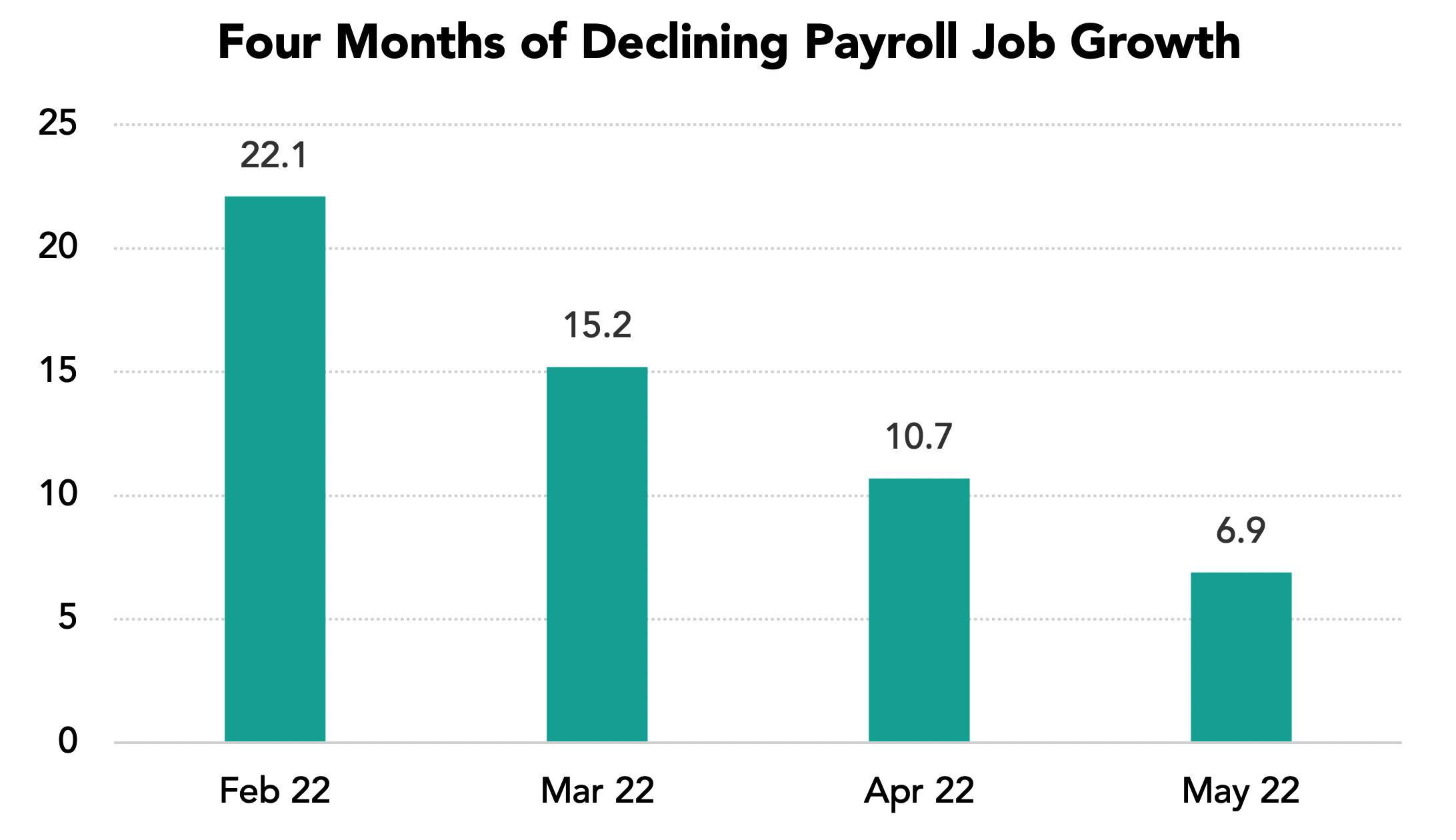

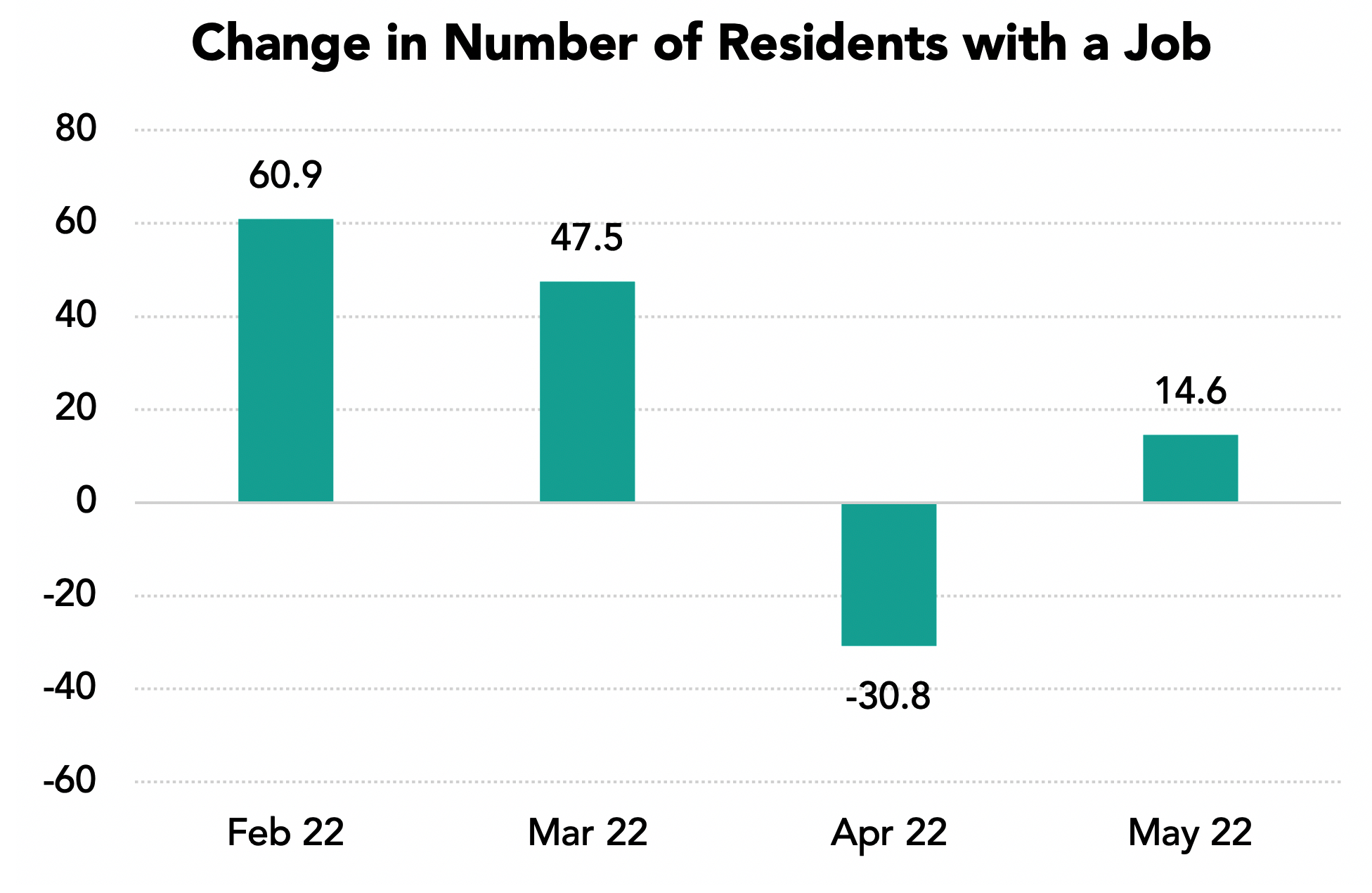

The Bay Area added 6,900 payroll jobs in May with substantial payroll declines in added jobs for each of the past four months. But this is not the full story of what happened in the Bay Area economy in recent months.

The highlights:

• Payroll job growth declined from 22,100 in February to 6,900 in May for a four month gain of 59,900 payroll jobs.

• During this period the number of residents with jobs of all kinds increased by 92,200.

• In May Bay Area unemployment levels and unemployment rates fell to record lows.

• April 2022 brings major crosscurrents to the global, national and regional economy with the Russian invasion of Ukraine, rising interest rates amidst continuing high inflation and the ongoing Bay Area challenges of housing, transportation and competitiveness.

• June 2022 brings major challenges to the global, national and regional economy with the Russian invasion of Ukraine, large increases in interest rates amidst continuing high inflation, the recent spike in Bay Area COVID cases and the ongoing Bay Area challenges of housing, transportation and competitiveness.

Four Months of Declining Payroll Job Growth

This is the chart shown in media around the region last weekend and it is accurate. Payroll job growth has declined substantially.

But the Number of Residents with a Job Grew More

These data come from the household survey, which is smaller than the payroll survey and more volatile month to month. But it is accurate over time. The inference is that workers are finding jobs in traditional self-employment and gig work. The discrepancy between payroll job and employed worker growth (59,200 versus 92,200 for the past four months) could be for many reasons. One is the difficulty in hiring in some industries from our high cost of housing. One could be a decline is jobs at tech startups. Workers unable to find jobs in declining sectors may be switching to self-employment.

But these data offer a counterpoint to the disappointing payroll job trends.

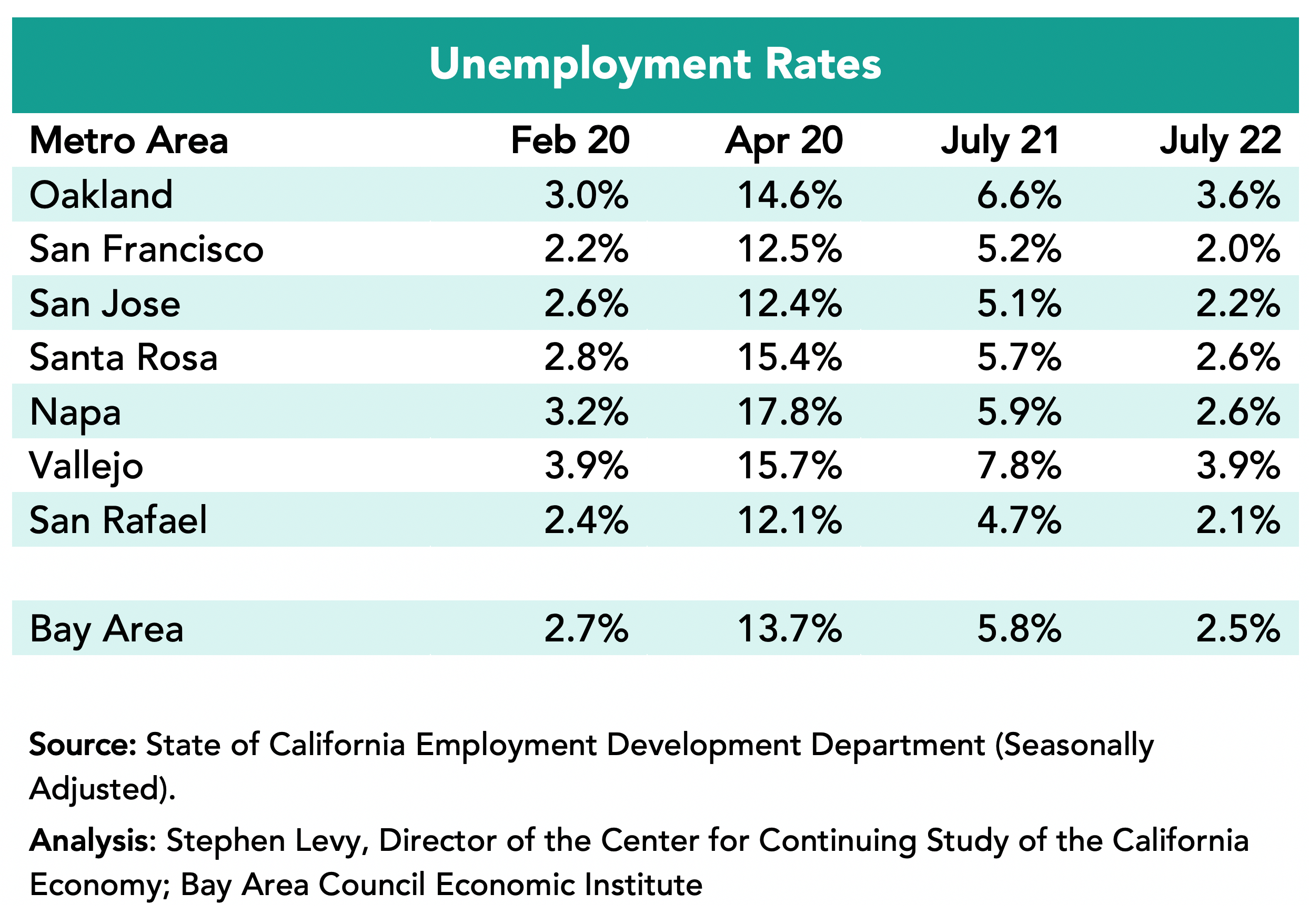

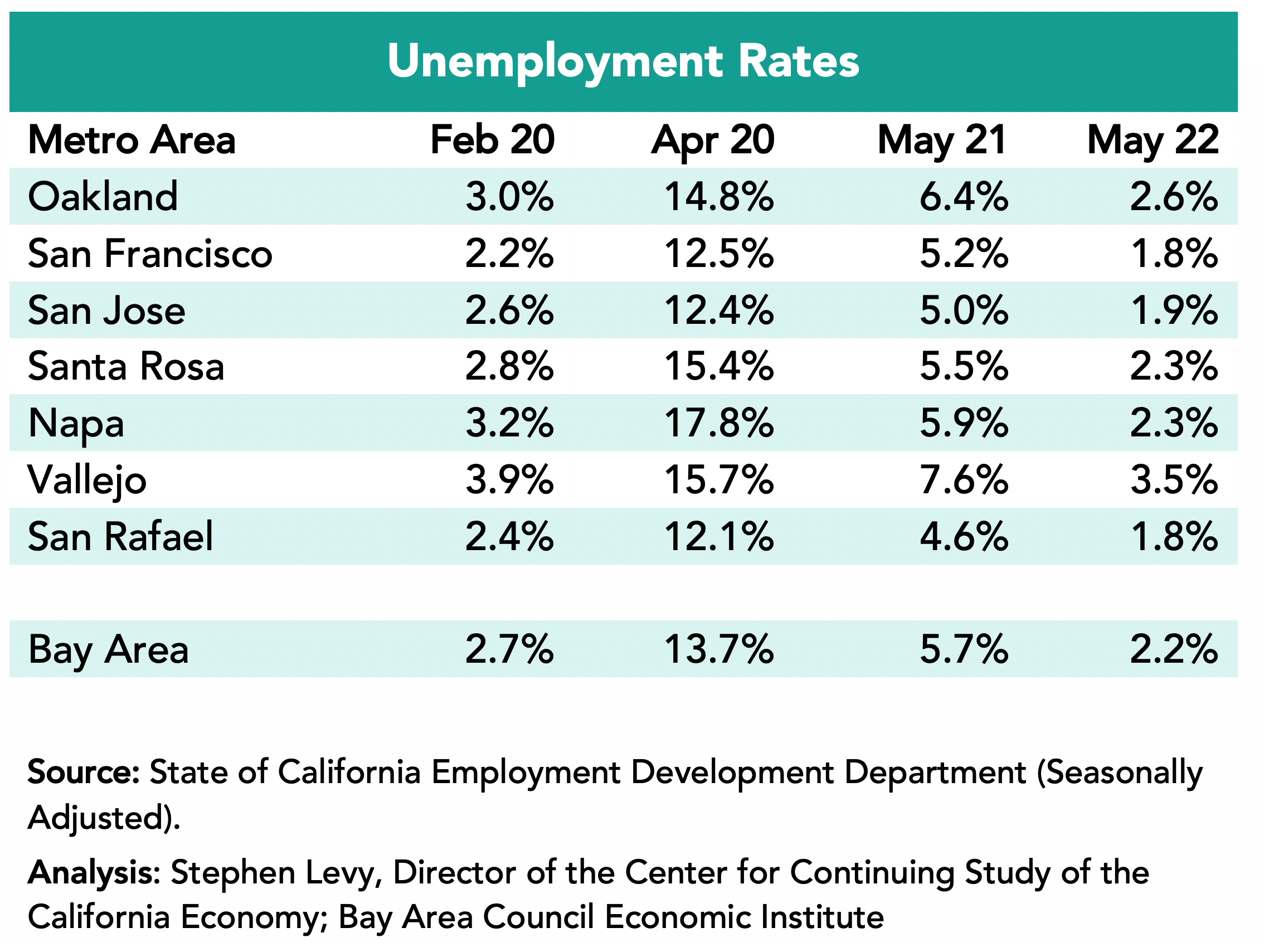

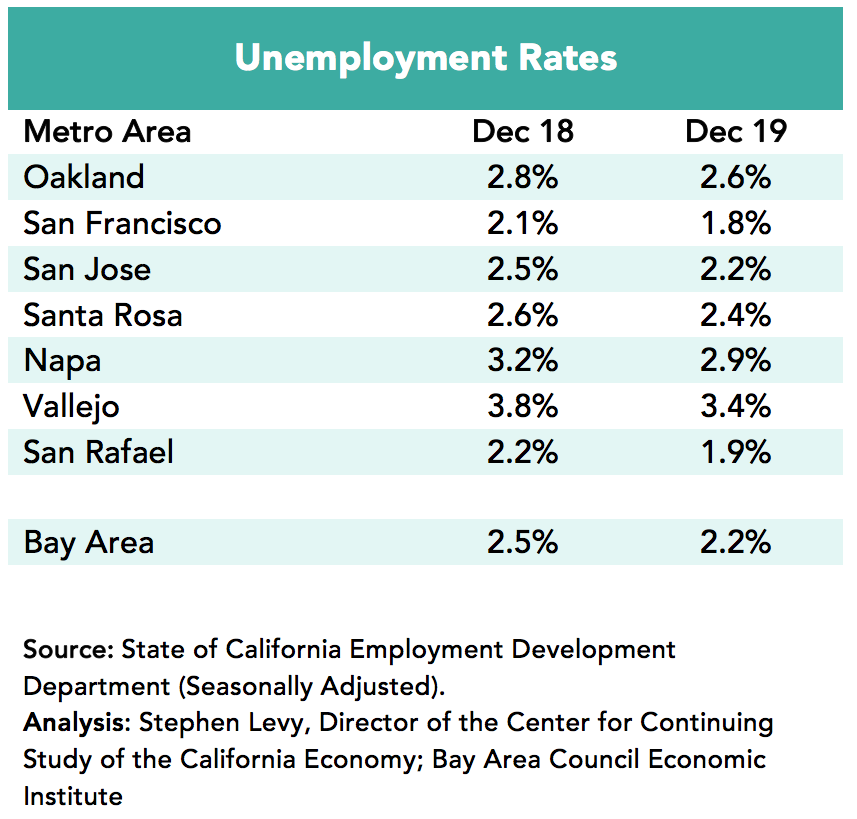

Unemployment Rates Fell to 2.2 in the Region in May 2022 from 5.7% in May 2021 and is now below the pre-pandemic level in February 2020

The lowest rates were in the San Rafael and San Francisco metro areas (1.8%) followed by the San Jose metro areas (1.9%) in May 2022.

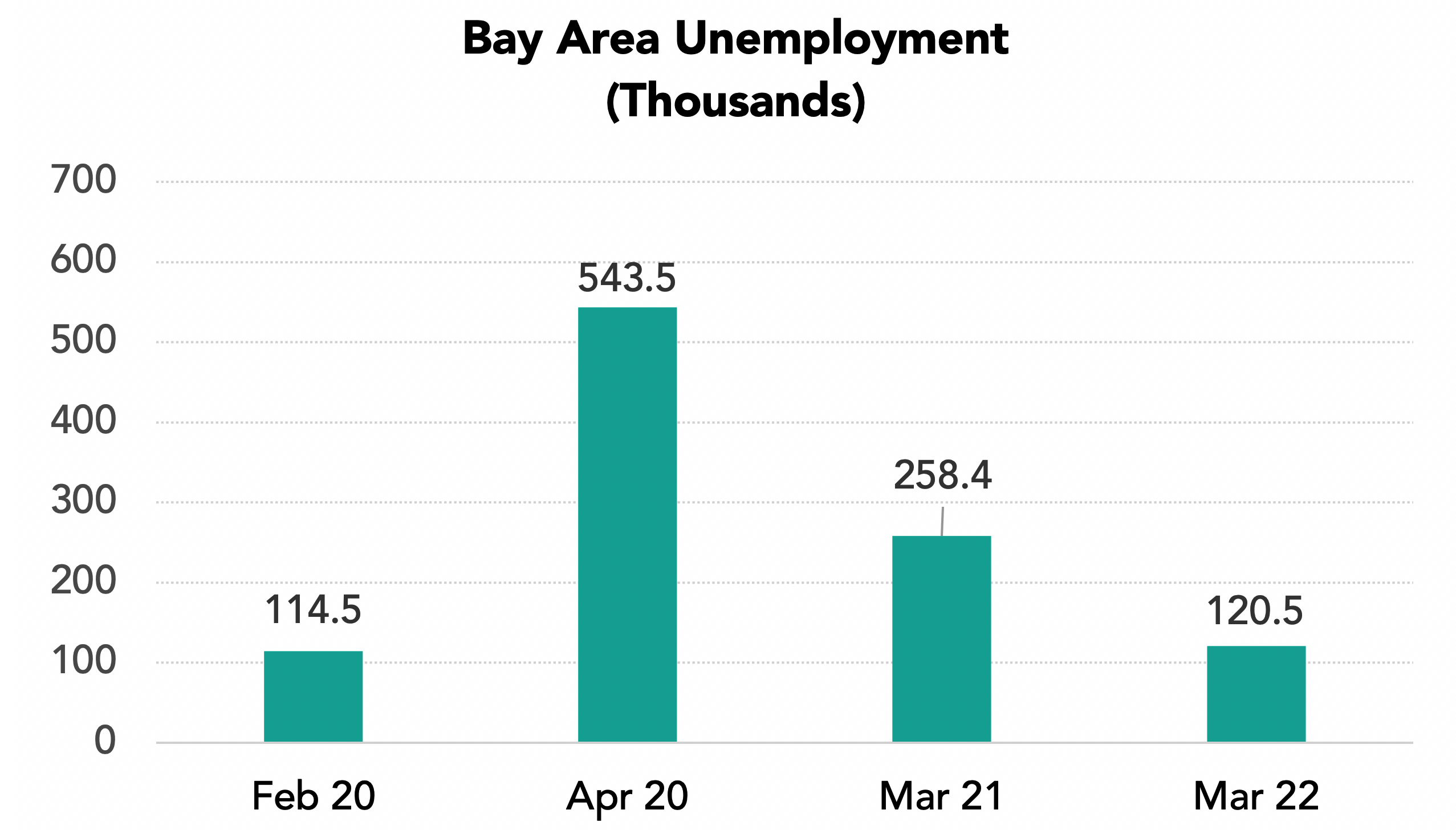

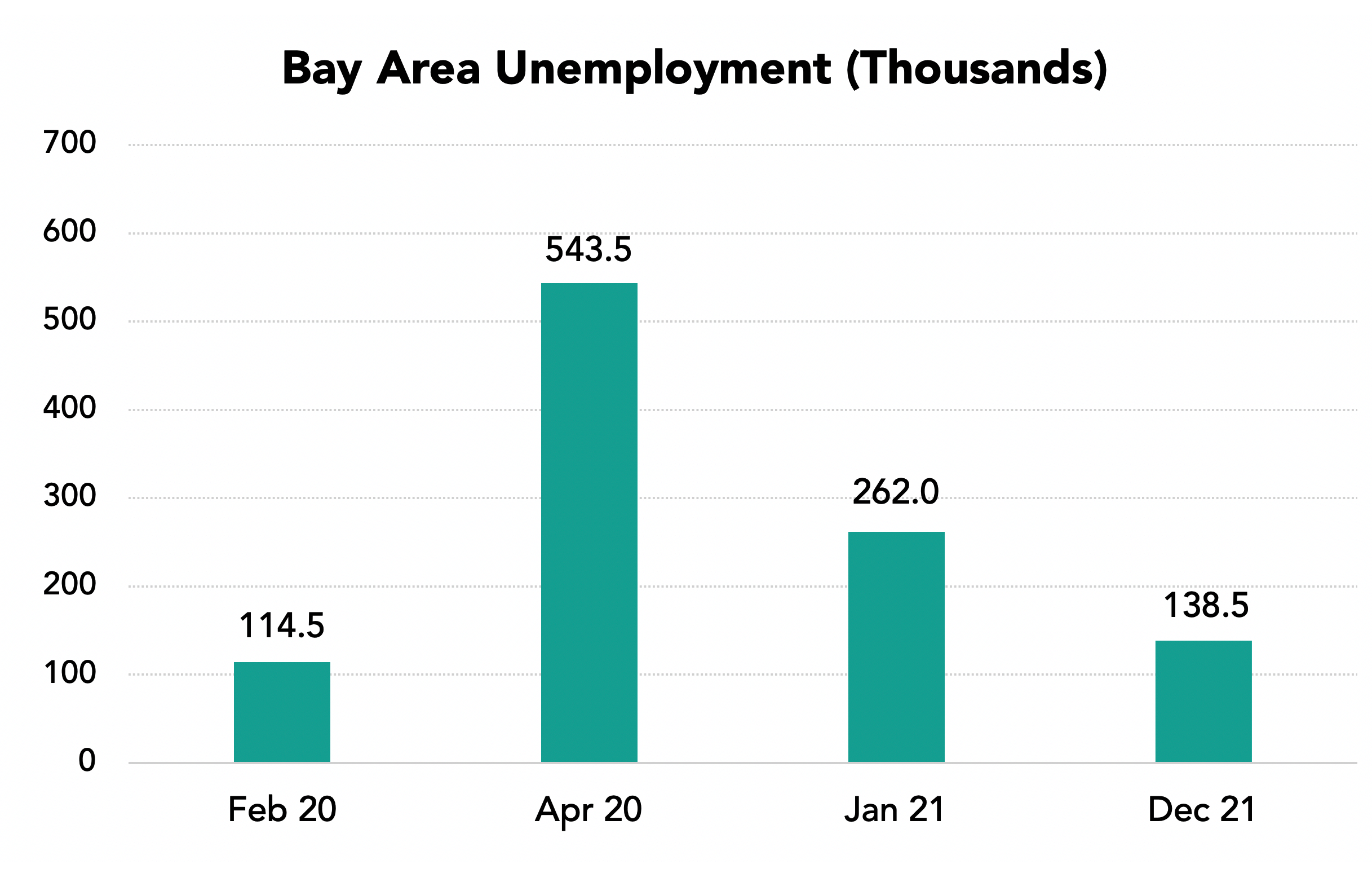

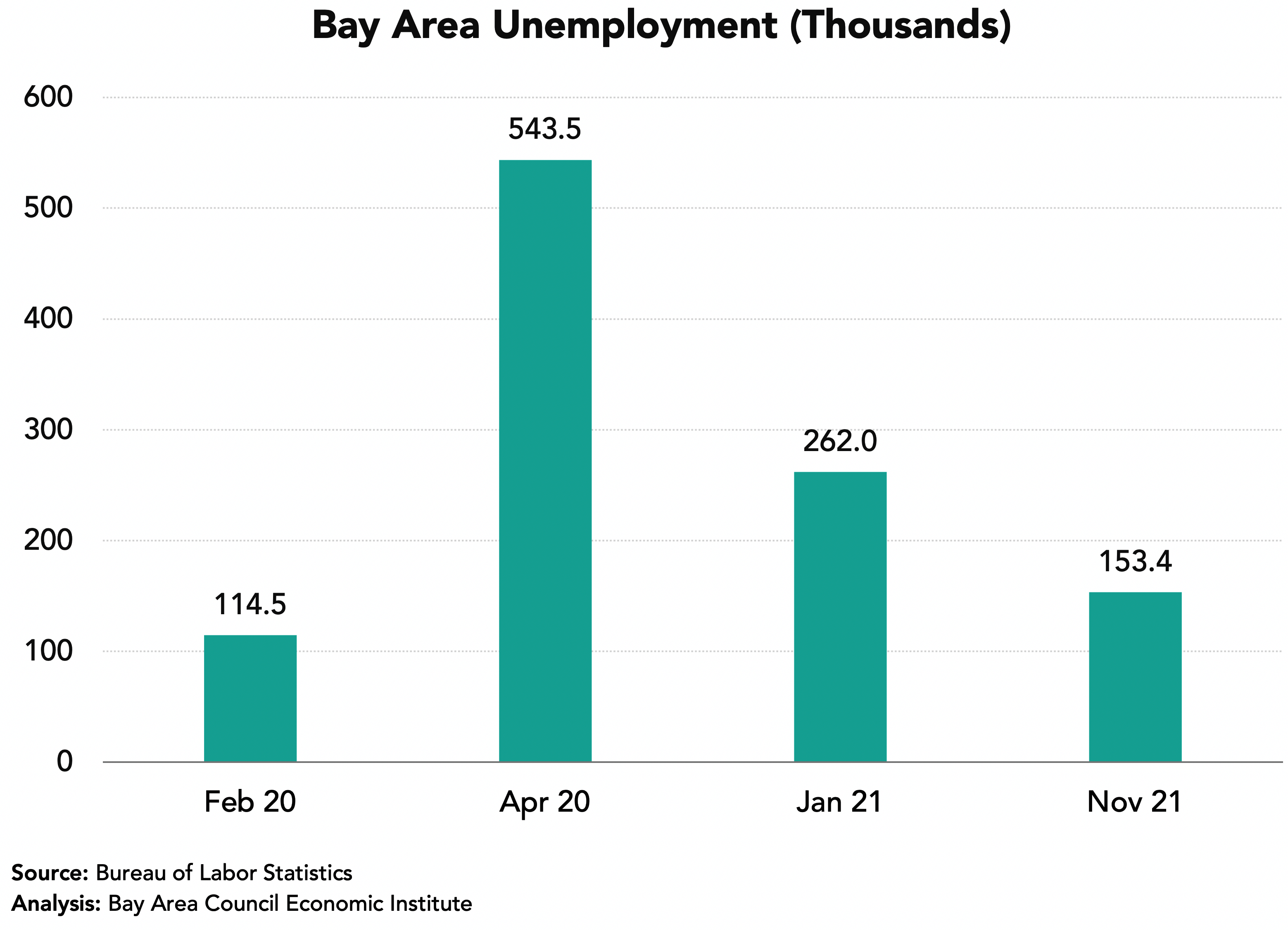

The number of unemployed residents has fallen sharply from the April 2020 high of 543,500 to 90,500 in May 2022 well below the pre-pandemic level in February 2020.

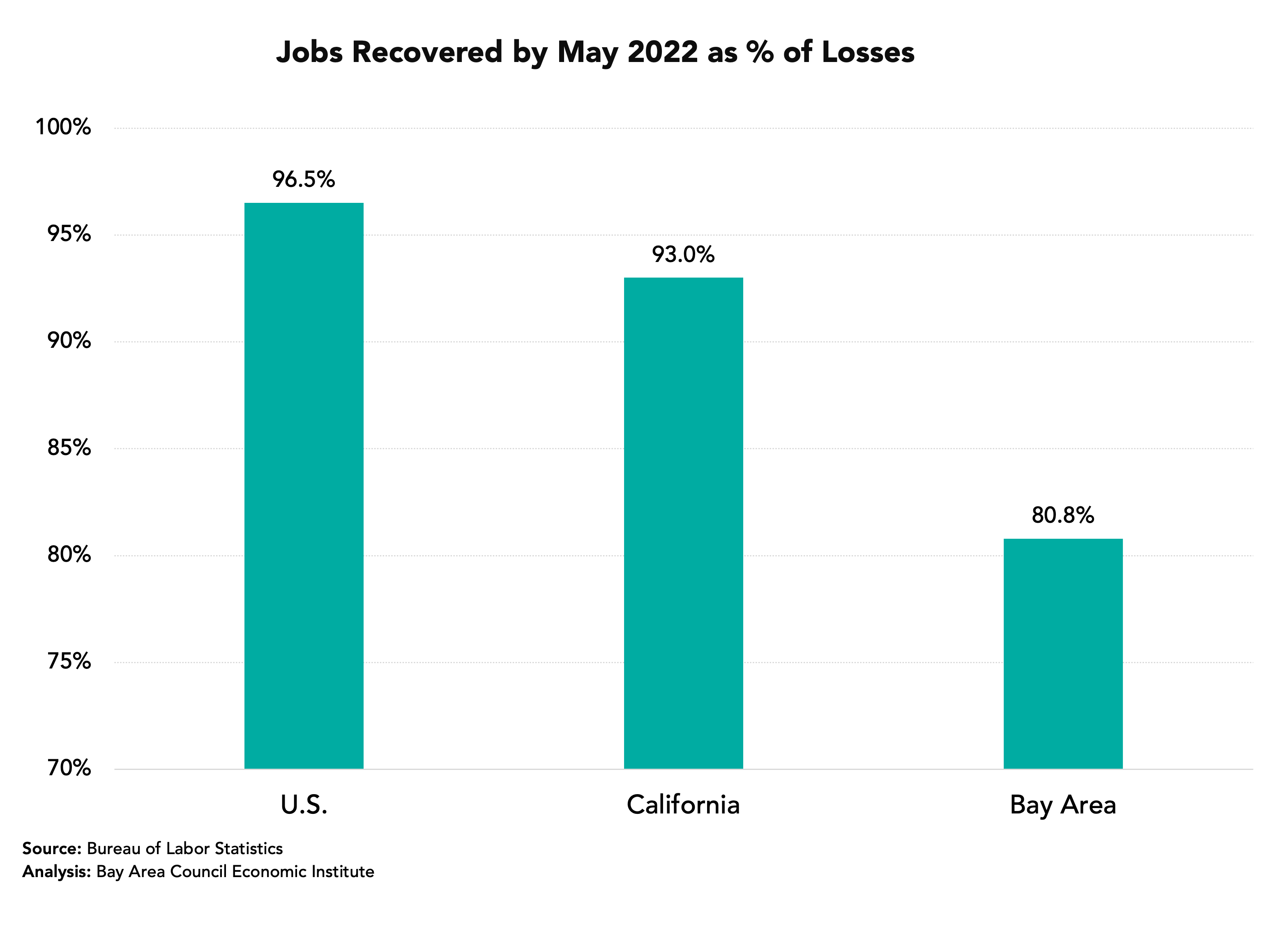

The Bay Area Trails the State and Nation in Payroll Job Recovery

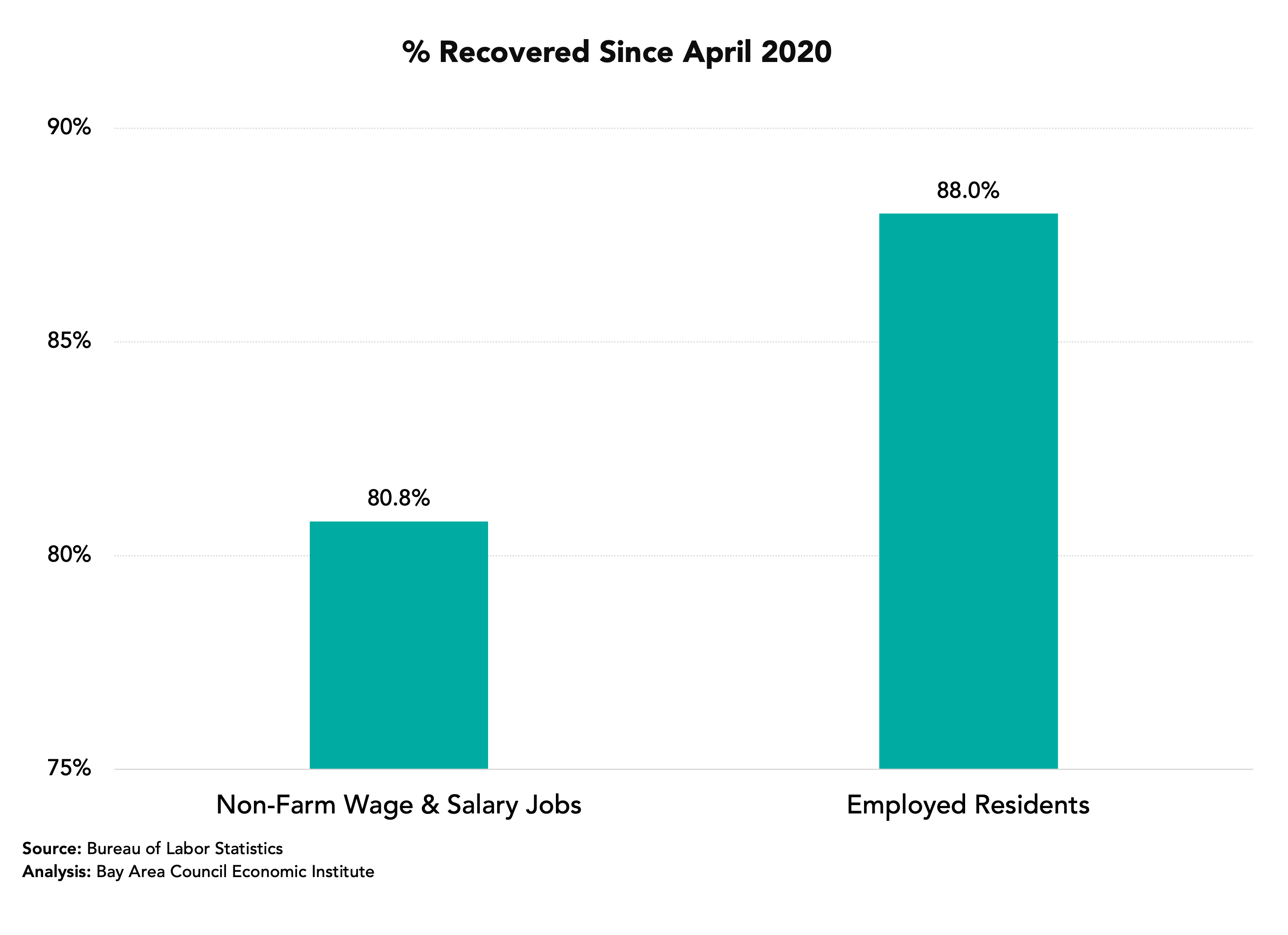

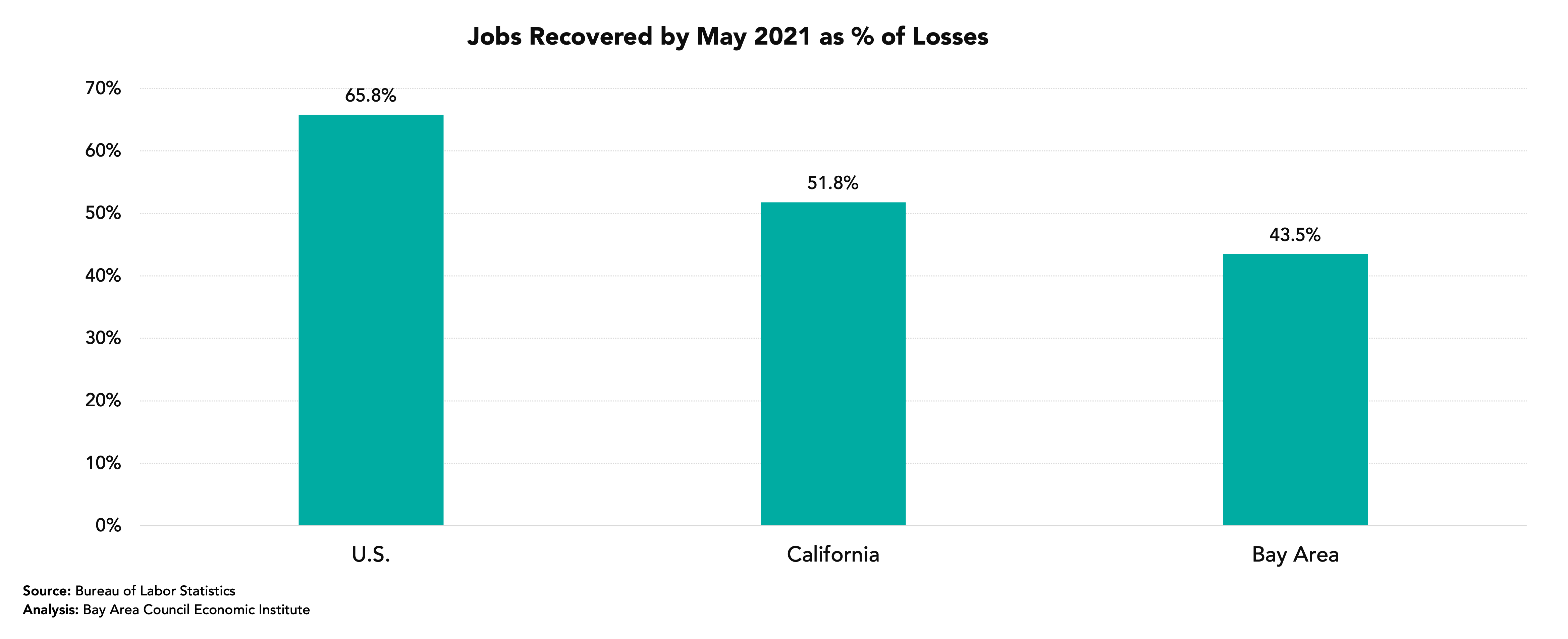

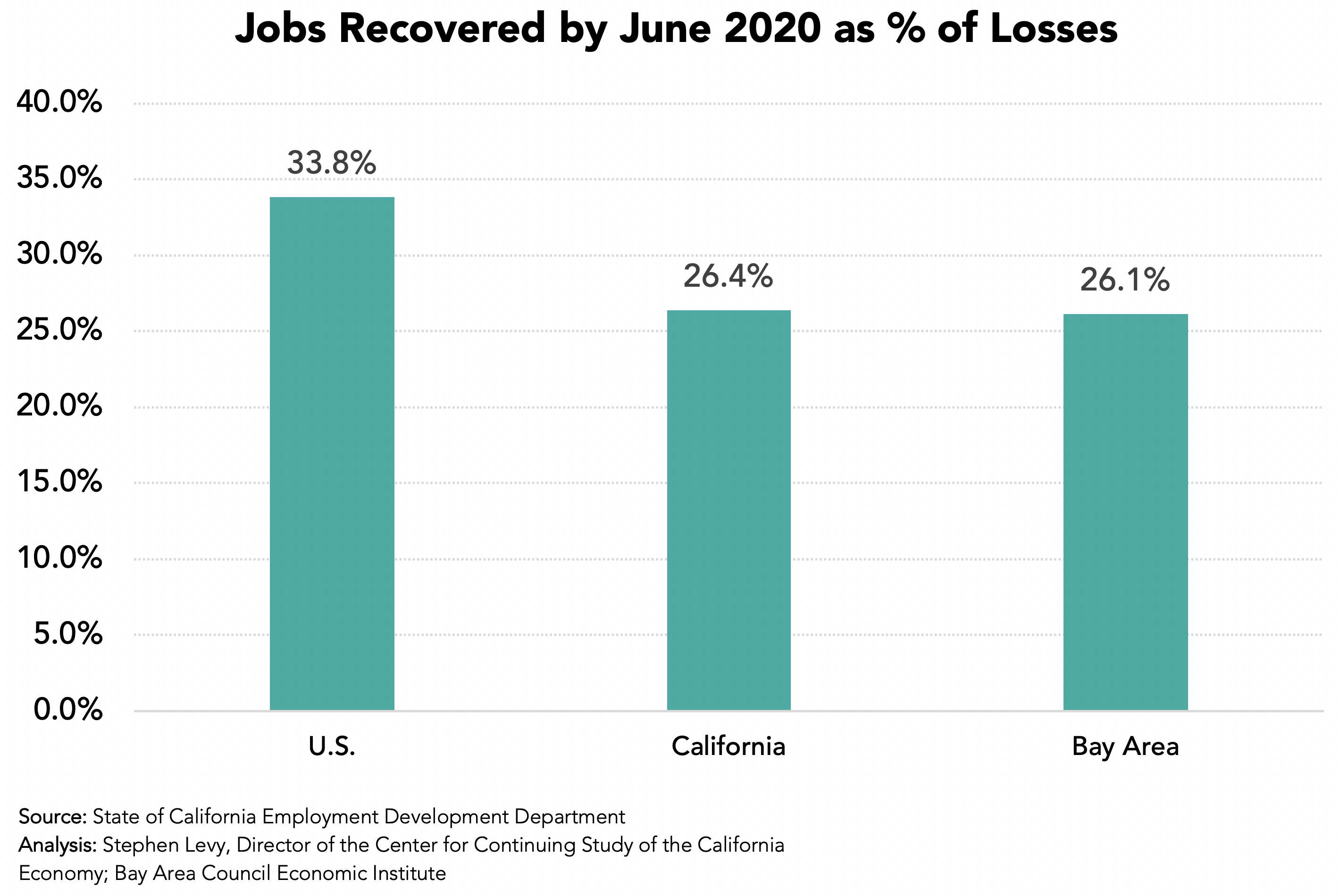

By May 2022 the region had recovered 80.8% of the payroll jobs lost between February and April 2020. This is a lower recovery rate than the state and nation, though the region has closed the gap in recent months.

While the region has recovered just 80.8% of the non-farm payroll jobs lost between February and April 2020, it has recovered 88.0% of the decline in the number of residents with jobs. The explanation for the gap between the two measures is an increase in self-employment jobs, most likely gig work jobs.

Payroll Job Growth Strong for the Year Though Lagging Recently

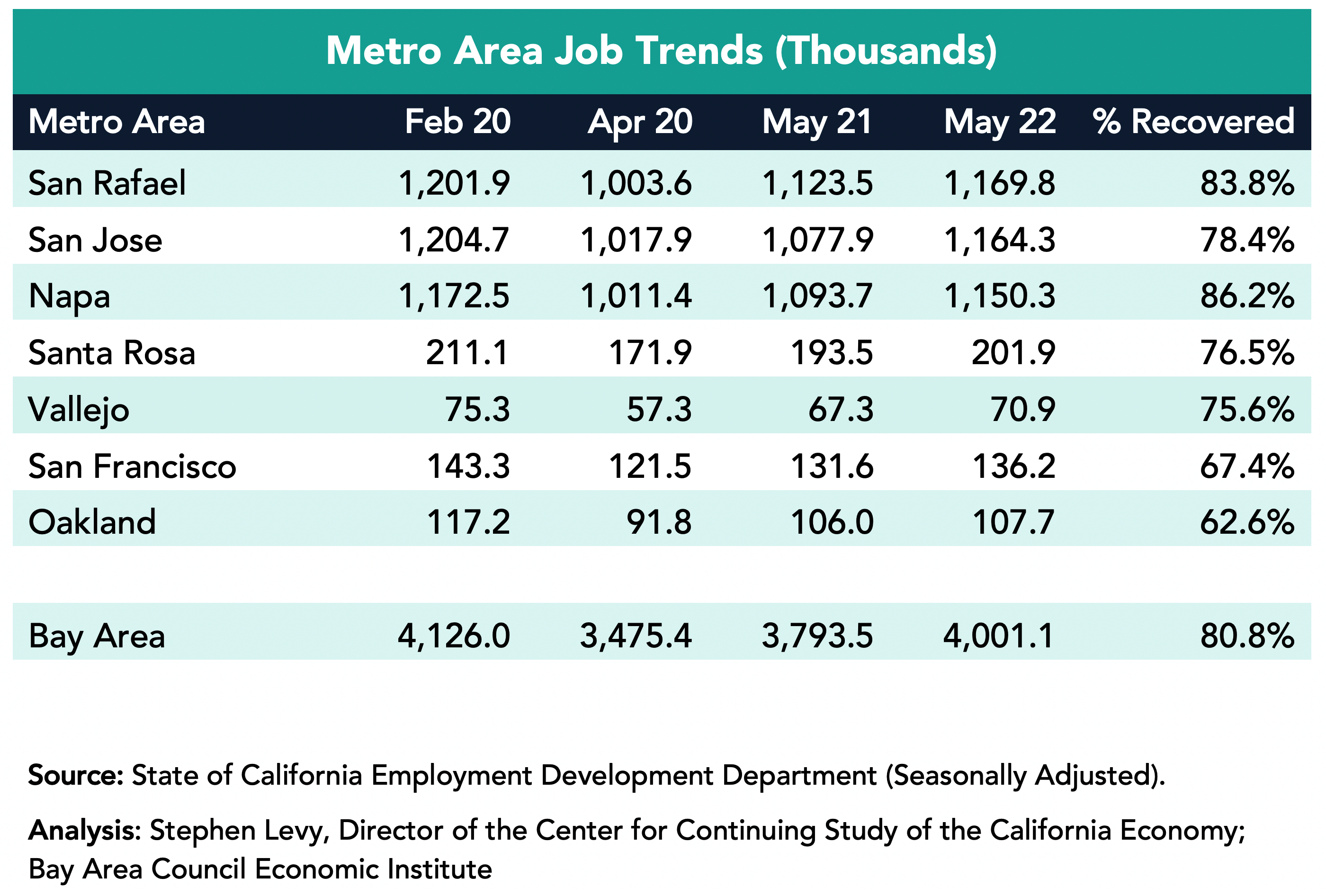

The Bay Area added 207,600 jobs in the past year (+5.5%) led by a gain of 86,400 in the San Francisco metro area though SF has recovered just 78.4% of the jobs lost between February and April 2020. The San Jose metro area added 56,600 jobs and by May 2022 had recovered 86.2% of the payroll jobs lost between February and April 2020. The Oakland metro area added 46,300 jobs during the past year.

But 102,900 Workers Have Not Rejoined the Workforce Since February 2020

Residents who are not in the labor force are not counted as unemployed. As a result, the number of unemployed residents can decline while some are still prevented by choice or lack of child care or work in industries that have not fully recovered. The number of residents not in the labor force has increased recently, perhaps in response to the rise of COVID cases in the region.

Industries Were Affected Differently

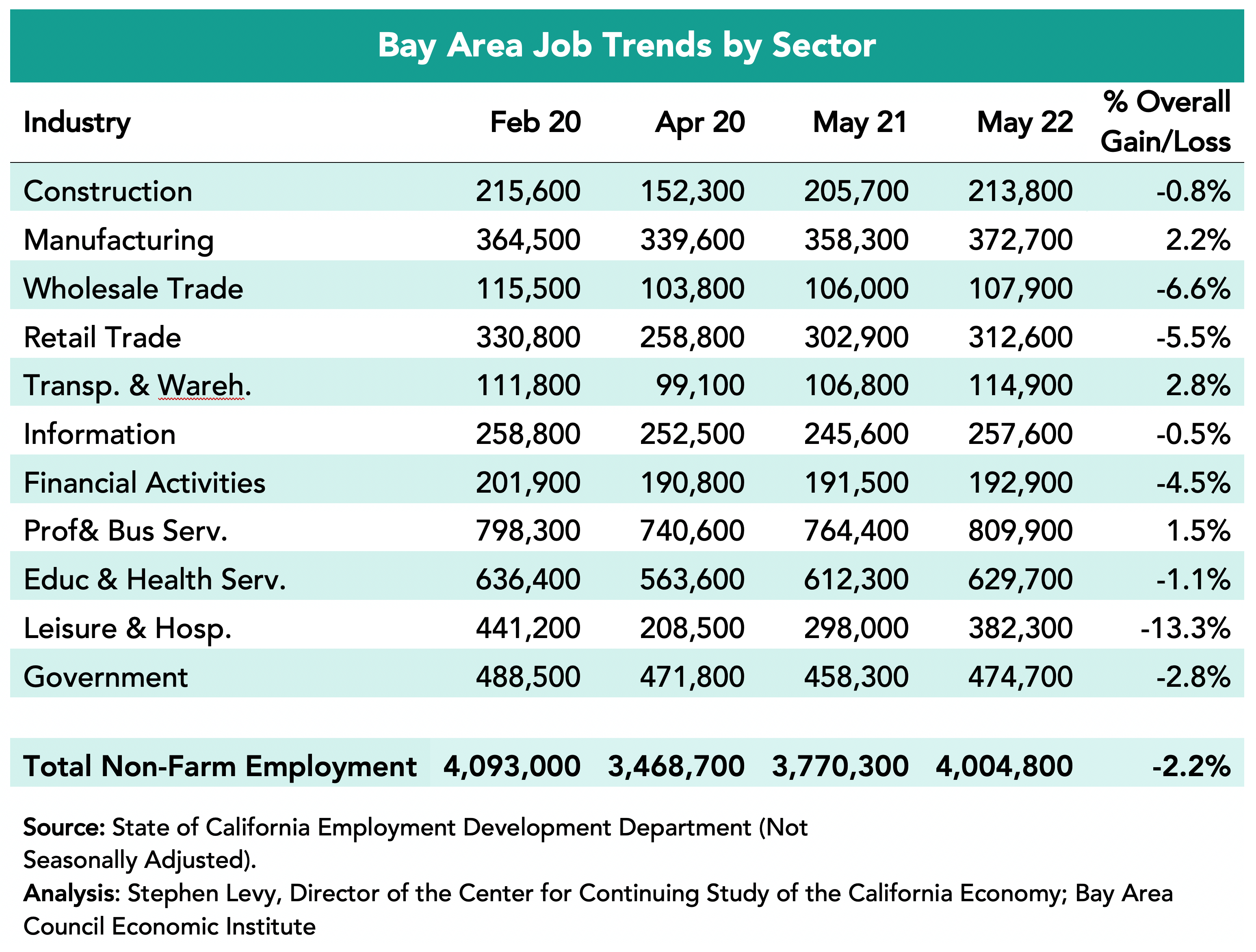

Four sectors—Manufacturing, Transportation and Warehousing, Information and Professional and Business Services—exceeded pre-pandemic job levels in May 2022 and Construction and Education and Health Care Services were close to full recovery. On the other hand, the Leisure and Hospitality sector recovered only 74.7% of lost jobs by May 2022, though travel and tourism jobs are now in a strong recovery. The Government sector is now slowly recovering the jobs lost between February and April 2020.

In the past two months Leisure and Hospitality and Government have shown the largest job growth.

Note that these data are not seasonally adjusted.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

June 24, 2022

In May 2022, the United States and 13 nations launched the Indo-Pacific Economic Framework (IPEF), a next-generation economic initiative designed to bring together economies in the Indian Ocean and Asia-Pacific regions around shared economic objectives. In this article on Medium.com, by Sean Randolph, Senior Director of the Institute, details the potential for the agreement in the future.

For years technology entrepreneurship was almost exclusive domain of Silicon Valley. In this article on Medium.com, by Sean Randolph, Senior Director of the Institute, details how new opportunities for growth and innovation are occurring in different nations across the globe.

Slower Job Growth in April and Some Good News in the Report

May 23, 2022

TThe Bay Area added 11,500 payroll jobs in April down from 15,500 in March and 24,100 in February. Job growth slowed in the state and nation as well and the region is still outpacing the nation in job growth over the past 12 months after the sharp job losses in 2020.

The highlights:

• Bay Area jobs increased by 5.8% between April 2021 and 2022 compared to a 4.6% increase in the nation and 5.6% gain in California.

• The Bay Area unemployment rate in March 2022 was 2.5% compared to 2.7% in the pre-pandemic month of February 2020.

• May 2022 brings major crosscurrents to the global, national and regional economy with the Russian invasion of Ukraine, rising interest rates amidst continuing high inflation, the recent spike in Bay Area COVID cases and the ongoing Bay Area challenges of housing, transportation and competitiveness.

• April 2022 brings major crosscurrents to the global, national and regional economy with the Russian invasion of Ukraine, rising interest rates amidst continuing high inflation and the ongoing Bay Area challenges of housing, transportation and competitiveness.

• Bay Area jurisdictions have been given large increases in their housing goals for the next eight years as a result of state legislation and policy to reduce overcrowding and increase affordability. Each jurisdiction is in the process of updating their Housing Elements in 2022 to meet state and regional policy goals and requirements.

The Bay Area Outpaced the Nation in Recent Job Growth

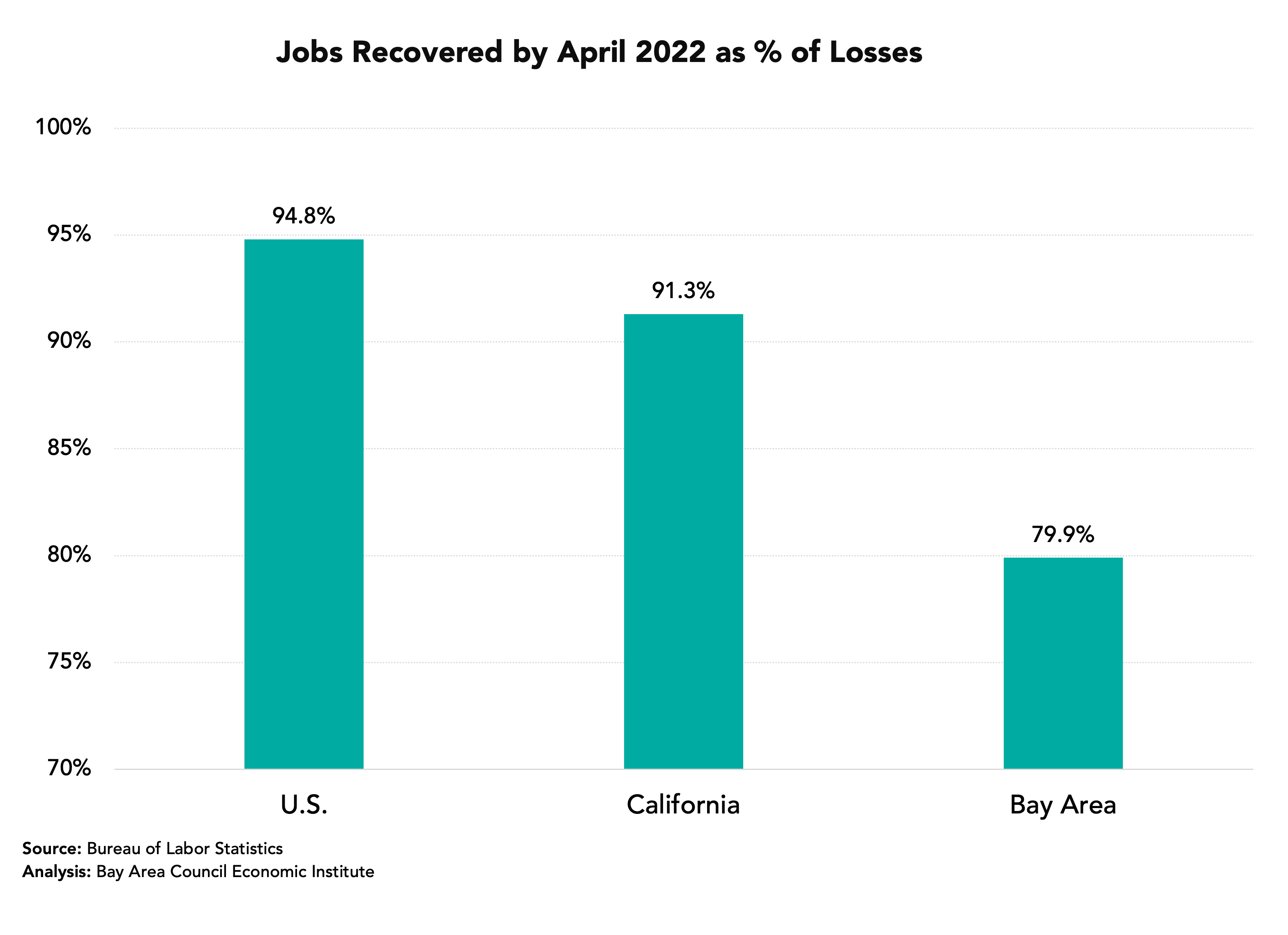

Job growth slowed in the nation, state and region in April. Still, Bay Area payroll jobs increased by 5.8% between April 2021 and April 2022 outpacing the U.S. 4.6% growth rate. The region still lags the nation and state in the % of jobs recovered since April 2020 as a result of the large job losses in 2020.

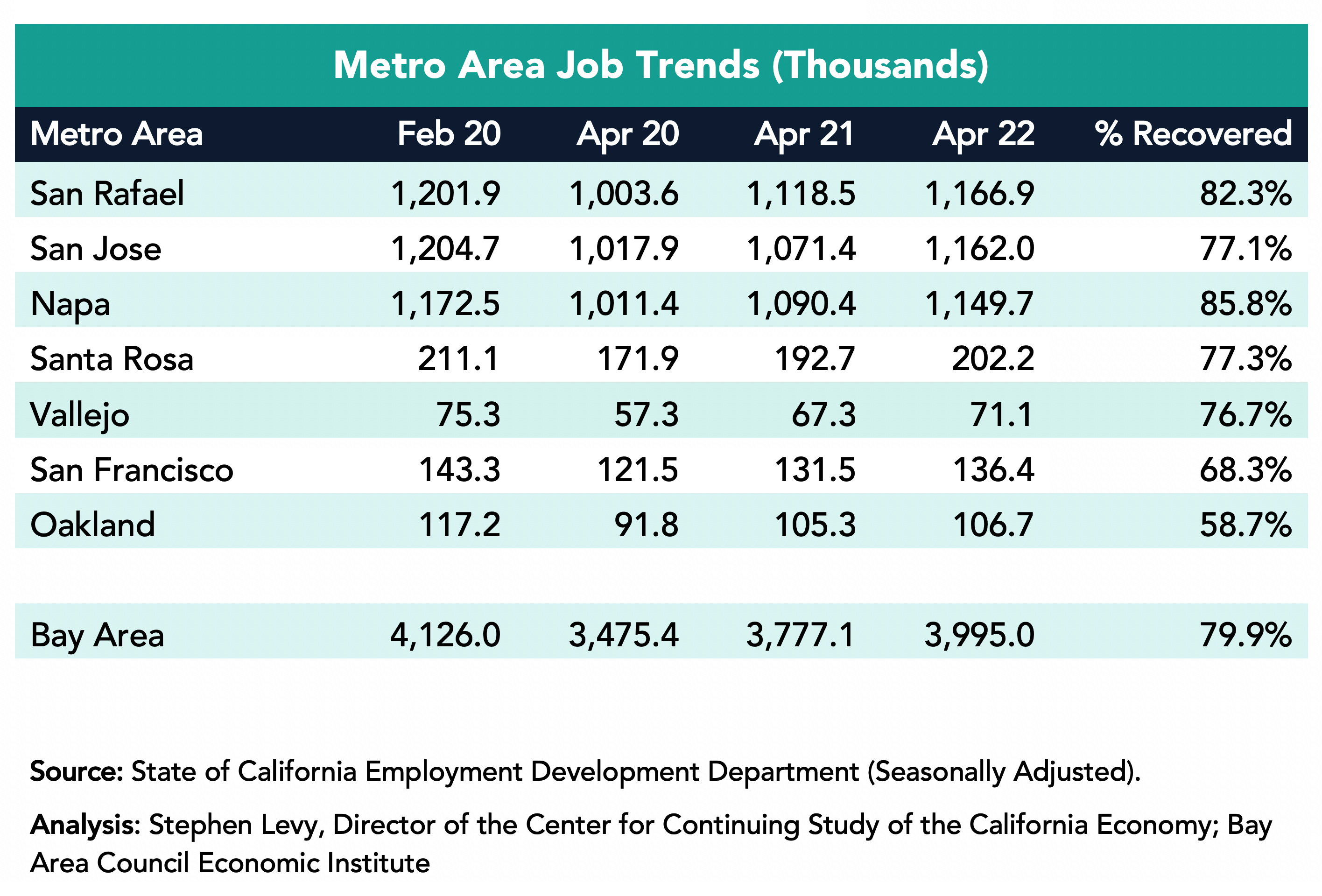

By April 2022 the region had recovered 79.9% of the jobs lost between February and April 2020. This is a lower recovery rate than the state and nation, though the region has closed the gap in recent months.

The Bay Area added 217,900 jobs in the past year led by a gain of 90,600 in the San Francisco metro area though SF has recovered just 77.1% of the jobs lost between February and April 2020. The San Jose metro area added 59,300 jobs and by April 2022 had recovered 85.8% of the jobs lost between February and April 2020. The Oakland metro area added 47,400 jobs during the past year.

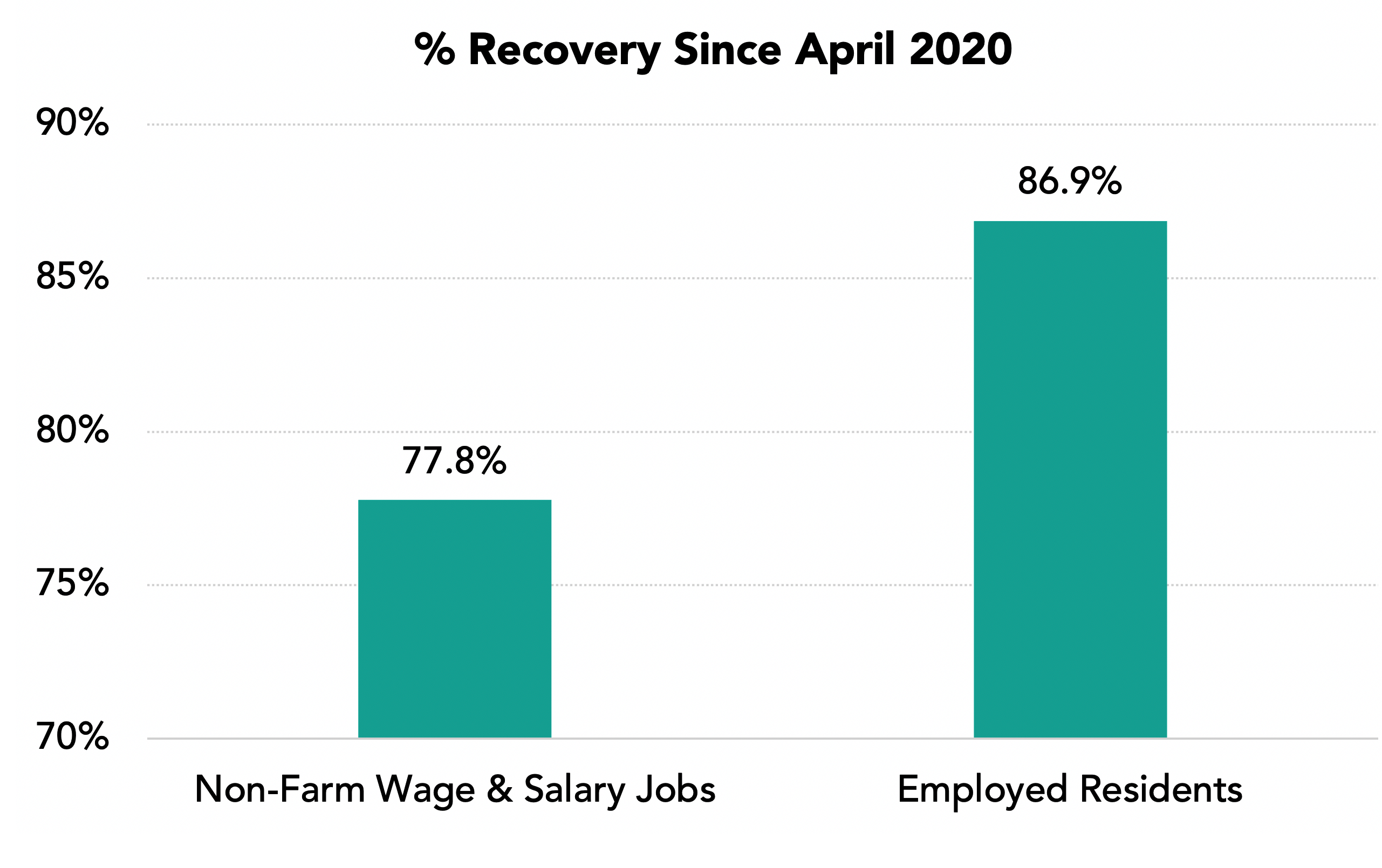

While the region has recovered just 79.9% of the non-farm wage & salary jobs lost between February and April 2020, it has recovered 85.6% of the decline in the number of residents with jobs. The explanation for the gap between the two measures is an increase in self-employment jobs, most likely gig work jobs.

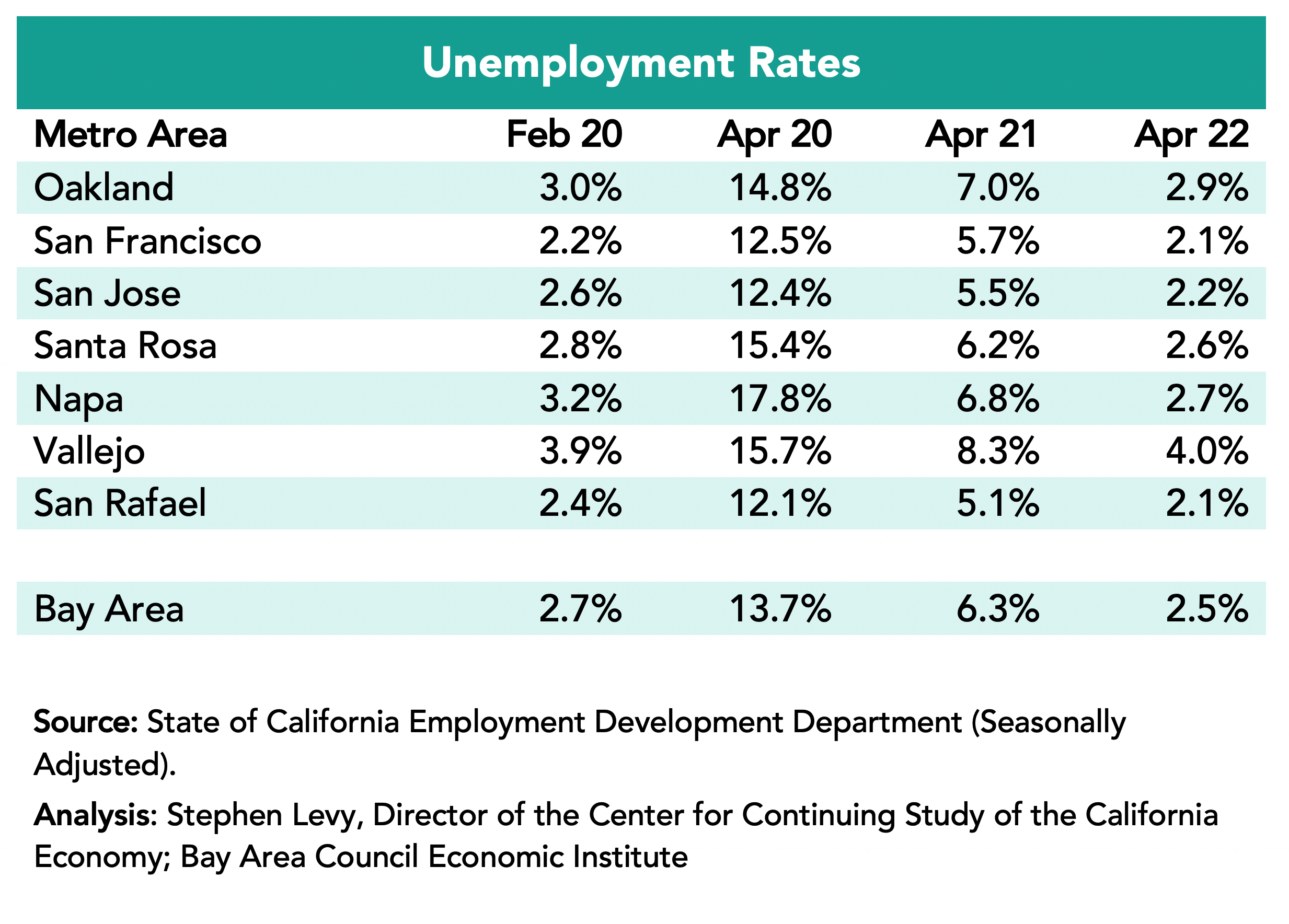

Unemployment Rates Fell to 2.5% in the Region in April 2022 from 6.3% in April 2021 and is now below the pre-pandemic level in February 2020

The lowest rates were in the San Rafael and San Francisco metro areas (2.1%) followed by the San Jose metro areas (2.2%) in April 2022.

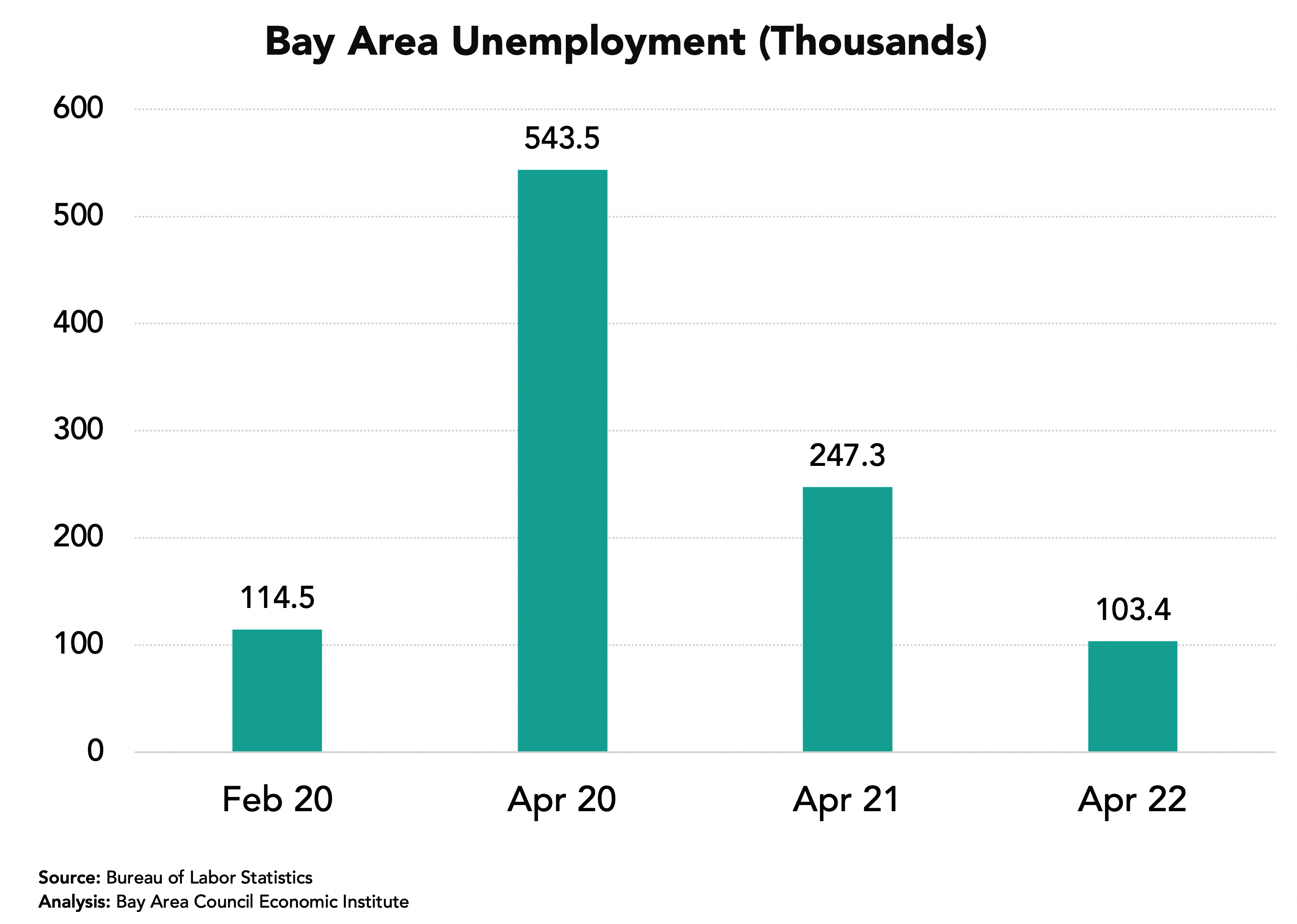

The number of unemployed residents has fallen sharply from the April 2020 high 103,400 in April 2022 below the pre-pandemic level in February 2020.

But 105,600 Workers Have Not Rejoined the Workforce Since February 2020

Residents who are not in the labor force are not counted as unemployed. As a result, the number of unemployed residents can decline while some are still prevented by choice or lack of child care or work in industries that have not fully recovered. The number of residents not in the labor force has increased recently, perhaps in response to the rise of COVID cases in the region.

Industries Were Affected Differently

Four sectors—Manufacturing, Transportation and Warehousing, Information and Professional and Business Services—exceeded pre-pandemic job levels in April 2022 and Construction and Education and Health Care Services were close to full recovery. On the other hand, the Leisure and Hospitality sector recovered only 72% of lost jobs by April 2022, though travel and tourism jobs are now picking up again. The Government sector is now slowly recovering the jobs lost between February and April 2020.

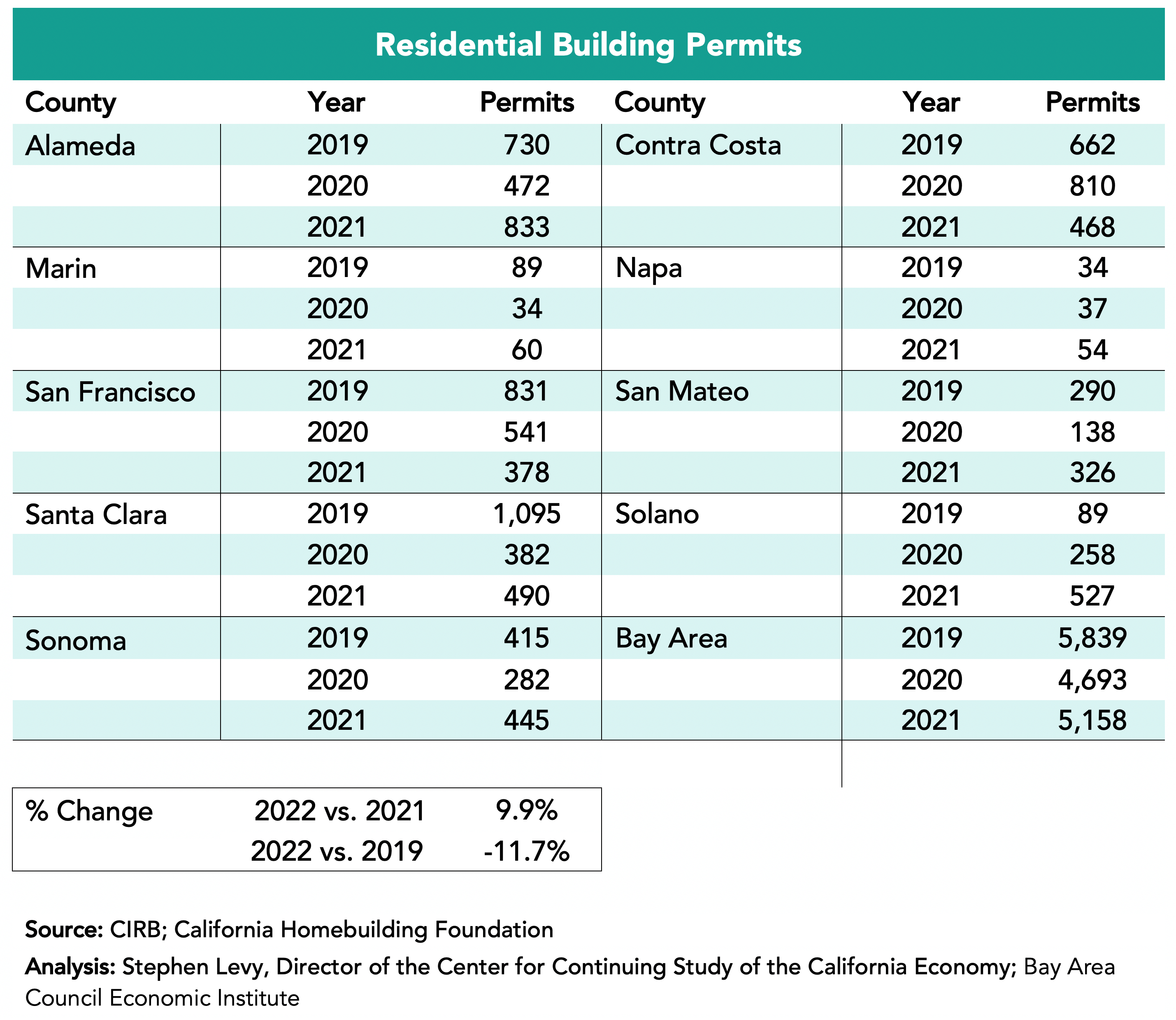

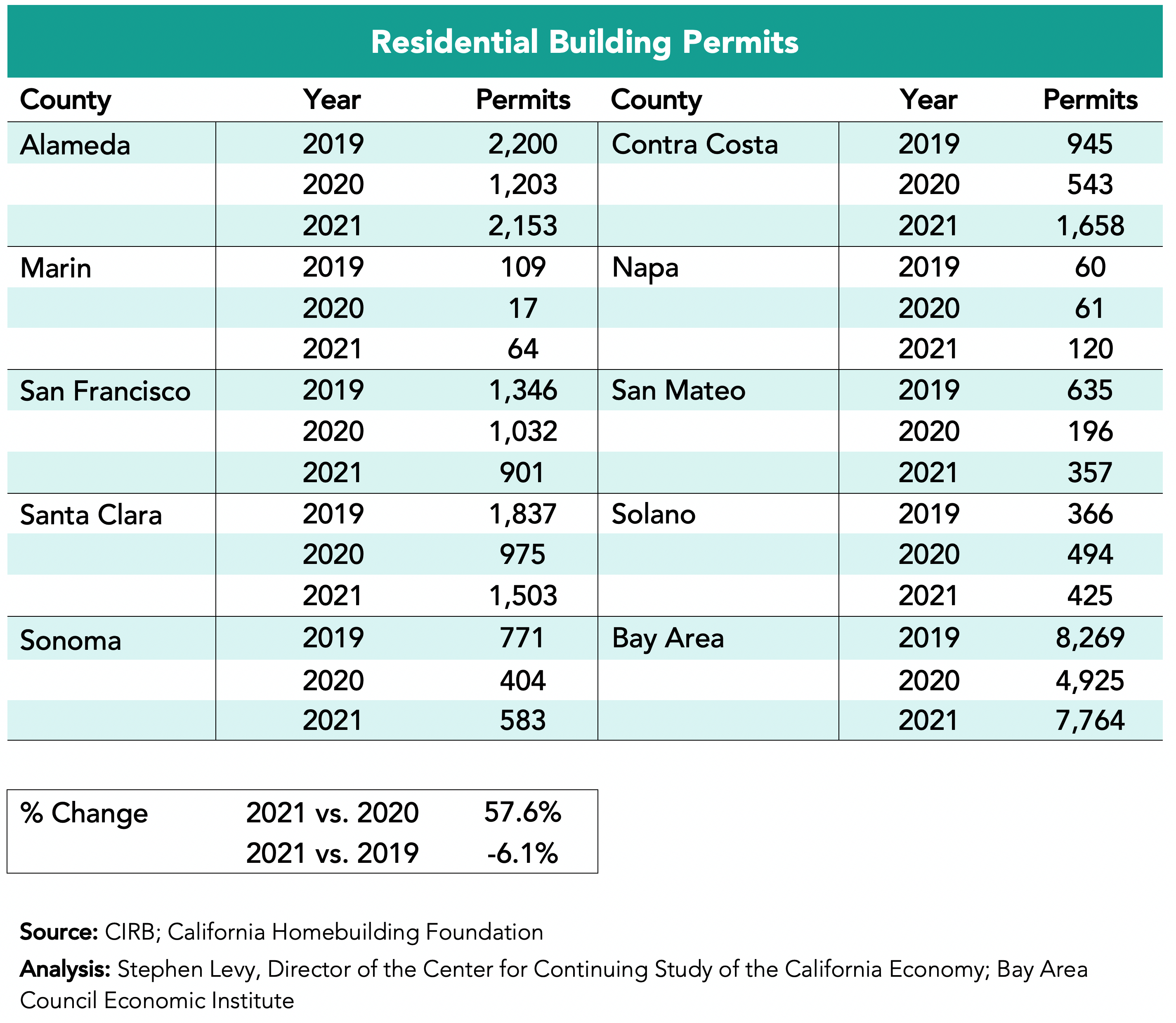

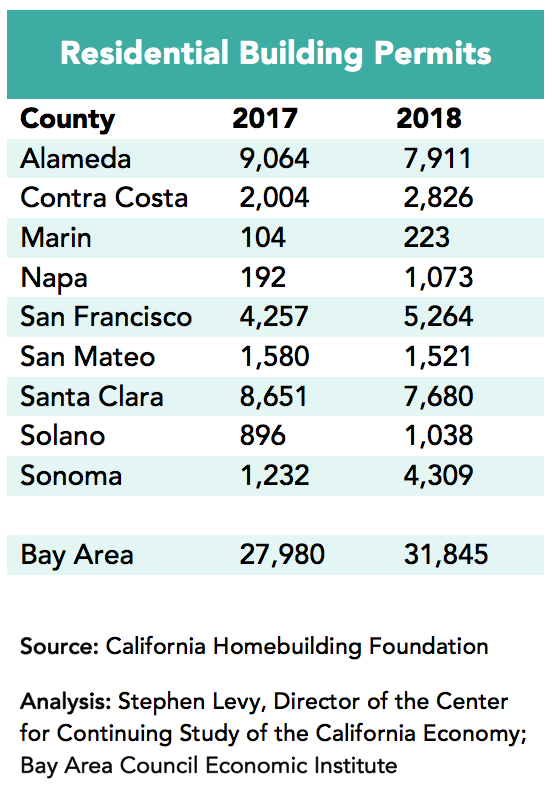

Housing Permits Rebound to 2019 Levels in 2021

Housing permit levels were up 35.5% in 2021 over 2020 levels and equaled permit levels in 2019. In the first two months of 2022, permit levels were slightly above comparable 2021 months. There are positive and negative trends going forward. On the one hand, each week brings new large housing proposals and approvals. At the same time mortgage rates and prices and rents are surging.

This year all Bay Area cities are required to update their Housing Elements to meet greatly increased regional and local jurisdiction housing goals. Below is a link to a report released on March 18th that I prepared at the request of the Silicon Valley Community Foundation to help residents understand and engage in their city’s Housing Element update process. Although the report focuses on five Midpeninsula cities—Cupertino, Menlo Park, Mountain View, Palo Alto and Sunnyvale—it has broad applicability for other communities. The report is part of an engagement effort led by SV@Home with local partners.

The report is part of an engagement effort led by SV@Home with local partners.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

Slower Job Growth in March and Some Good News in the Report

February 19, 2022

The Bay Area added 13,100 payroll jobs in March down from 22,100 in February but is still outpacing the nation in job growth over the past 12 months after the sharp job losses in 2020.

The highlights:

• Bay Area jobs increased by 6.2% between March 2021 and 2022 compared to a 4.5% increase in the nation and 6.4% gain in California.

• The Bay Area unemployment rate in March 2022 was 2.9% compared to 2.7% in the pre-pandemic low.

• More workers returned to the workforce in March and non-traditional job growth continues to outpace payroll job growth drawing workers back to the labor force and pushing unemployment levels down.

• April 2022 brings major crosscurrents to the global, national and regional economy with the Russian invasion of Ukraine, rising interest rates amidst continuing high inflation and the ongoing Bay Area challenges of housing, transportation and competitiveness.

• Bay Area jurisdictions have been given large increases in their housing goals for the next eight years as a result of state legislation and policy to reduce overcrowding and increase affordability. Each jurisdiction is in the process of updating their Housing Elements in 2022 to meet state and regional policy goals and requirements.

The Bay Area Outpaced the Nation in Recent Job Growth

Bay Area payroll jobs increased by 6.2% between March 2021 and March 2022 outpacing the U.S. 4.5% growth rate. The region still lags the nation and state in the % of jobs recovered since April 2020 as a result of the large job losses in 2020.

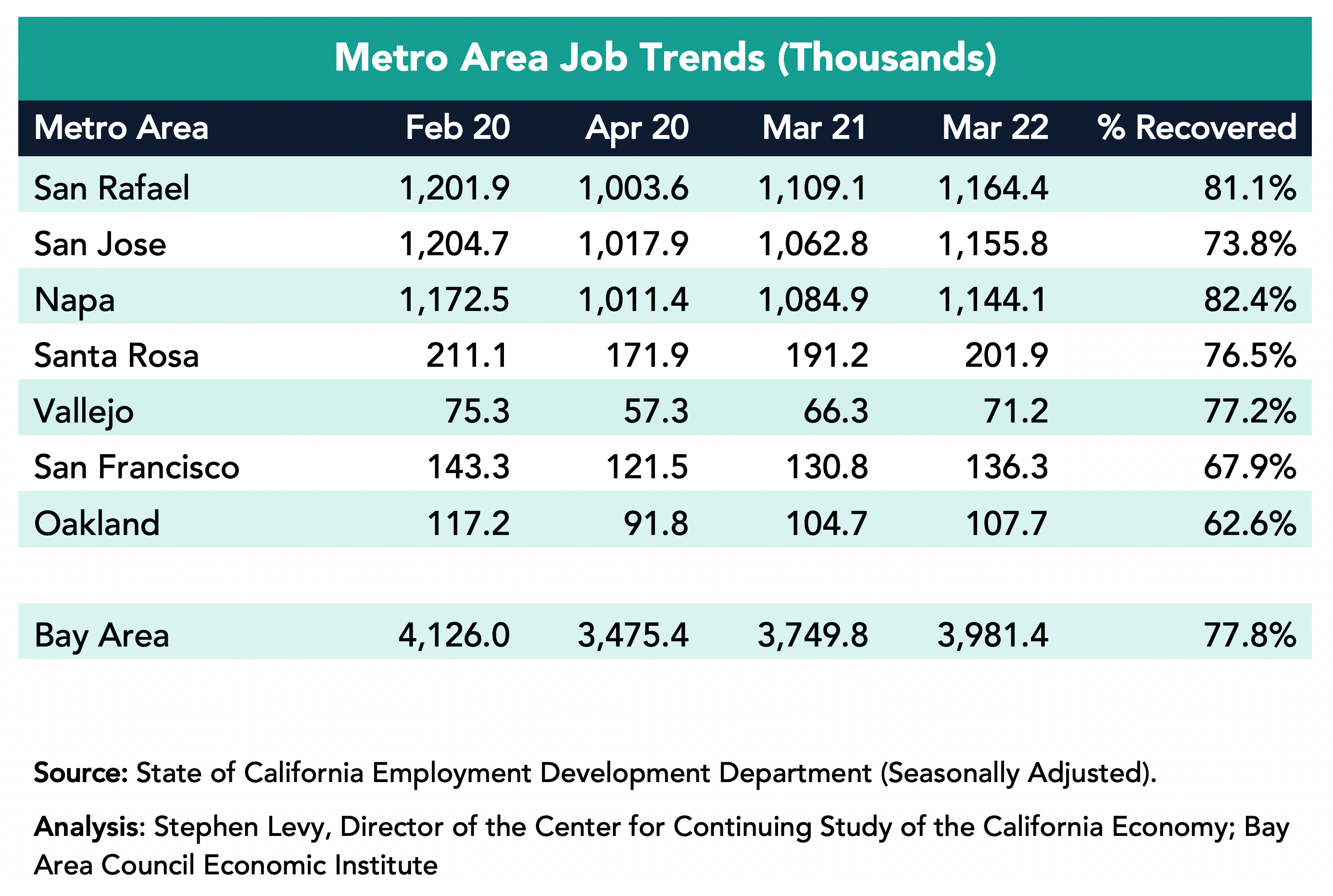

By March 2022 the region had recovered 77.8% of the jobs lost between February and April 2020. This is a lower recovery rate than the state and nation, though the region has closed the gap in recent months.

The Bay Area added 231,600 jobs in the past year led by a gain of 93,000 in the San Francisco metro area though SF has recovered just 73.8% of the jobs lost between February and April 2020. The San Jose metro area added 59,200 jobs and by March 2022 had recovered 82.4% of the jobs lost between February and April 2020. The Oakland metro area added 55,300 jobs.

By March 2022 the region had recovered 77.8% of the jobs lost between February and April 2020. This is a lower recovery rate than the state and nation, though the region has closed the gap in recent months.

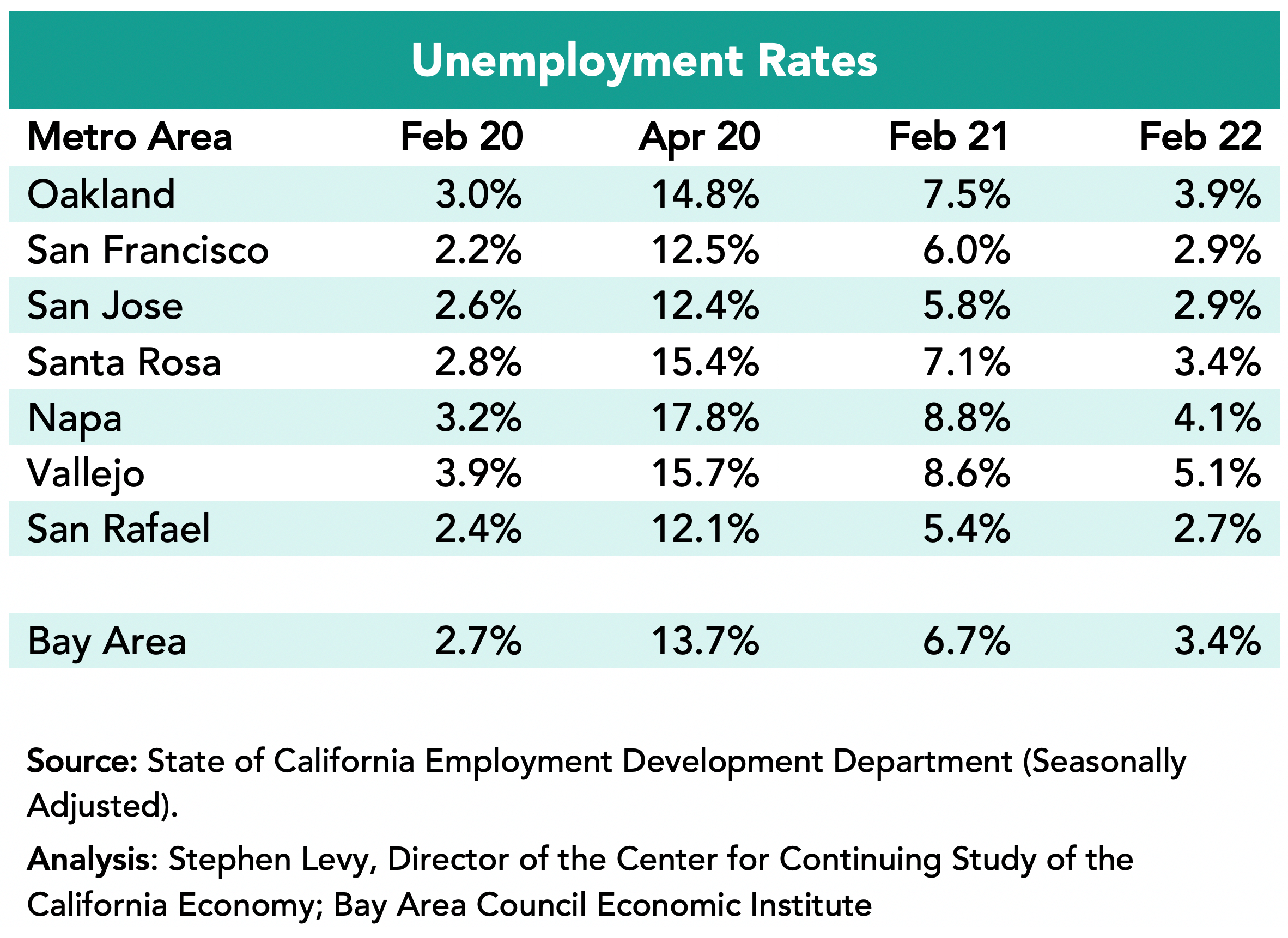

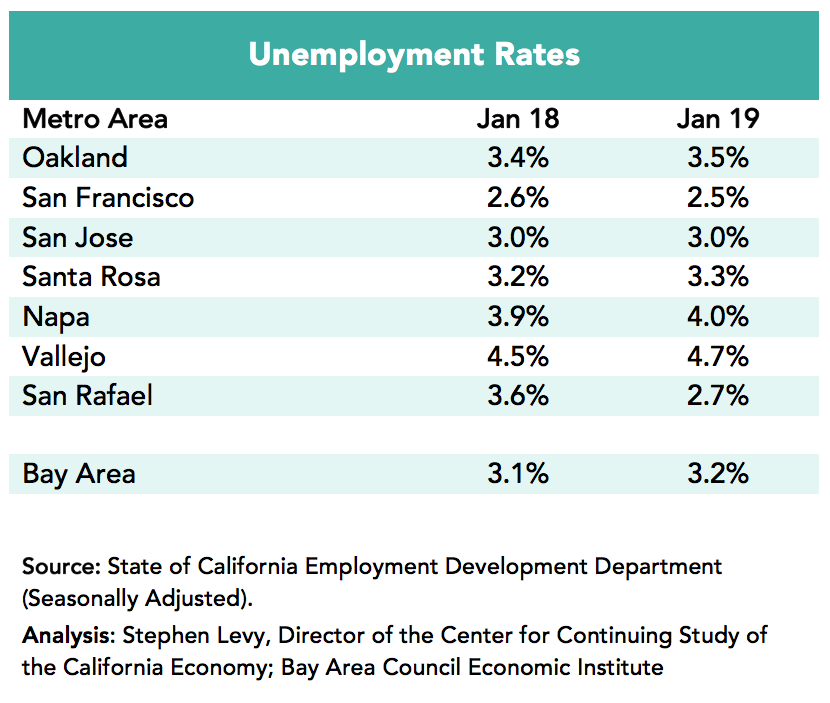

Unemployment Rates Fell to 2.9% in the Region in March 2022 from 6.5% in March 2021.

The lowest rates were in the San Rafael and San Francisco metro areas (2.4%) followed by the San Jose metro areas (2.5%) in March 2022.

The number of unemployed residents has fallen sharply from the April 2020 high and from March 2021 to 120,500 in February 2022 close to the pre-pandemic low in February.

But 58,700 Workers Have Not Rejoined the Workforce Since February 2020

Residents who are not in the labor force are not counted as unemployed. As a result, the number of unemployed residents can decline while some are still prevented by choice or lack of child care or work in industries that have not fully recovered. However, more workers are now returning to the workforce with an addition of 24,800 in March and 170,800 over the past 12 months.

Industries Were Affected Differently

Four sectors—Manufacturing, Transportation and Warehousing, Information and Professional and Business Services—exceeded pre-pandemic job levels in March 2022 and Construction and Education and Health Care Services were close to full recovery. On the other hand, the Leisure and Hospitality sector recovered only 66.8% of lost jobs by March 2022 though travel and tourism are now picking up again. The Government sector still has fewer jobs now than in April 2020.

Housing Permits Rebound to 2019 Levels in 2021

Housing permit levels were up 35.5% in 2021 over 2020 levels and equaled permit levels in 2019. In the first two months of 2022, permit levels were slightly above comparable 2021 months. There are positive and negative trends going forward. On the one hand, each week brings new large housing proposals and approvals. At the same time mortgage rates and prices and rents are surging.

This year all Bay Area cities are required to update their Housing Elements to meet greatly increased regional and local jurisdiction housing goals. Below is a link to a report released on March 18th that I prepared at the request of the Silicon Valley Community Foundation to help residents understand and engage in their city’s Housing Element update process. Although the report focuses on five Midpeninsula cities—Cupertino, Menlo Park, Mountain View, Palo Alto and Sunnyvale—it has broad applicability for other communities. The report is part of an engagement effort led by SV@Home with local partners.

The report is part of an engagement effort led by SV@Home with local partners.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

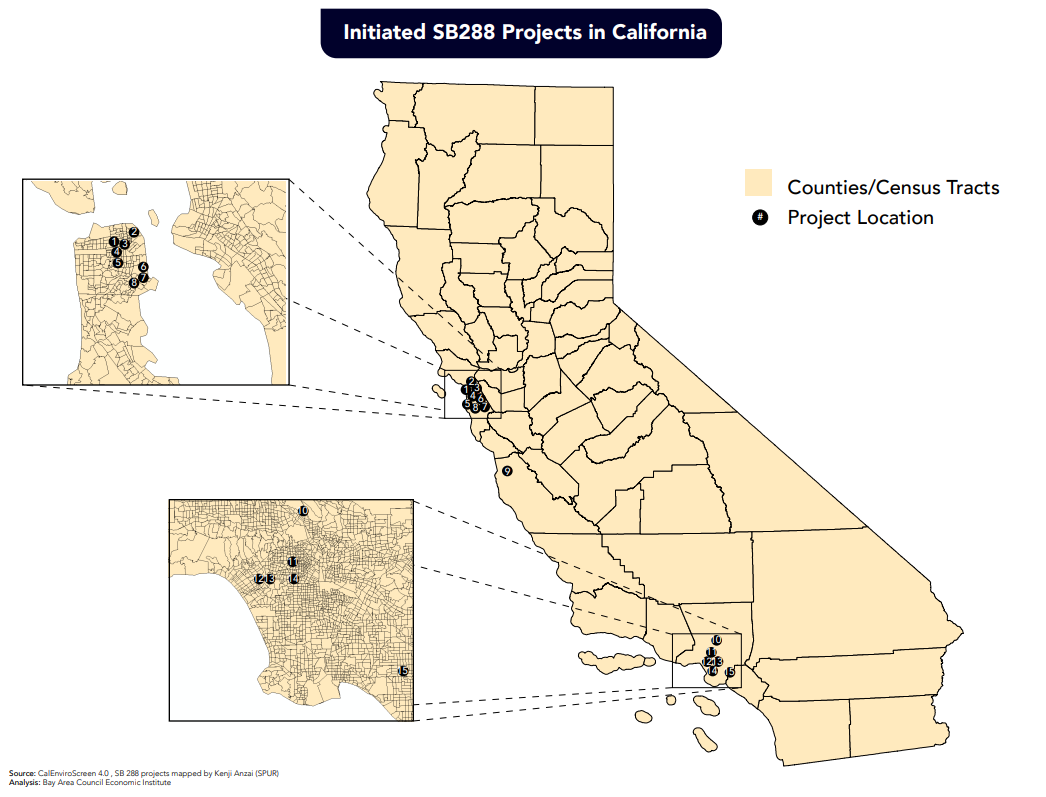

What is SB288?

The purpose of SB288 (Wiener) is to reduce the time and cost of delivering sustainable transportation projects across California by exempting certain projects from CEQA that are in the public right of way and are in an environmentally cleared long-term plan. SB288 is a safer route than taking advantage of existing categorical exemptions, which can require extensive analyses to prove the project is exempt and can still be challenged in court. The law sunsets on December 31, 2022.

SB288 provides statutory exemptions from CEQA for:

Potential benefits include:

Bill’s Impacts to-date:

The SB288 project team mapped the CEQA projects that have been initiated to date, and those under consideration to understand where agencies have been using the exemption and for what project types the exemption is most frequently used.

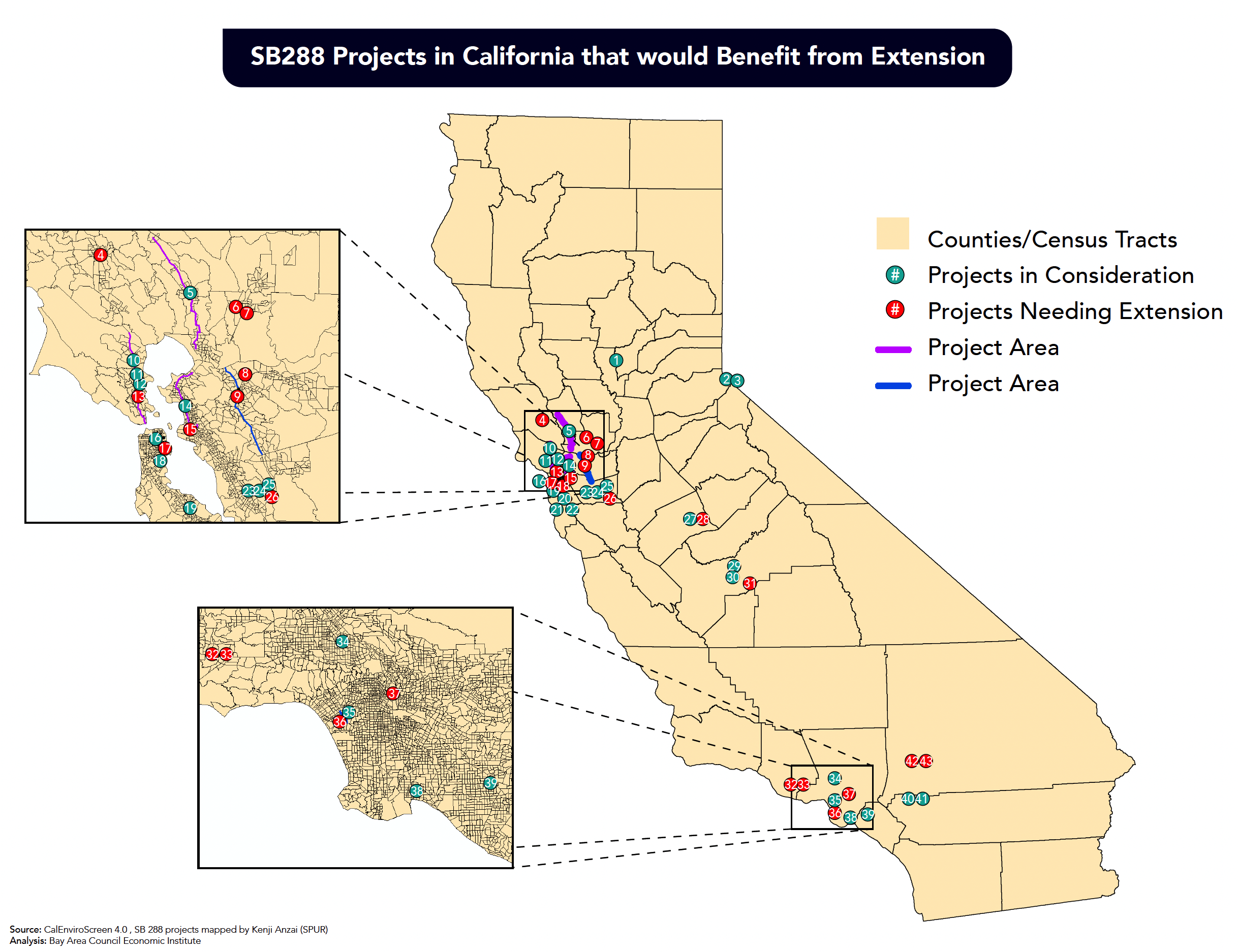

SB922 was introduced in February 2022 by Senator Wiener; the bill extends the existing exemption, fine-tunes the law for ease of implementation, has targeted expansions for electric fleet conversion, and adds an anti-displacement analysis requirement.

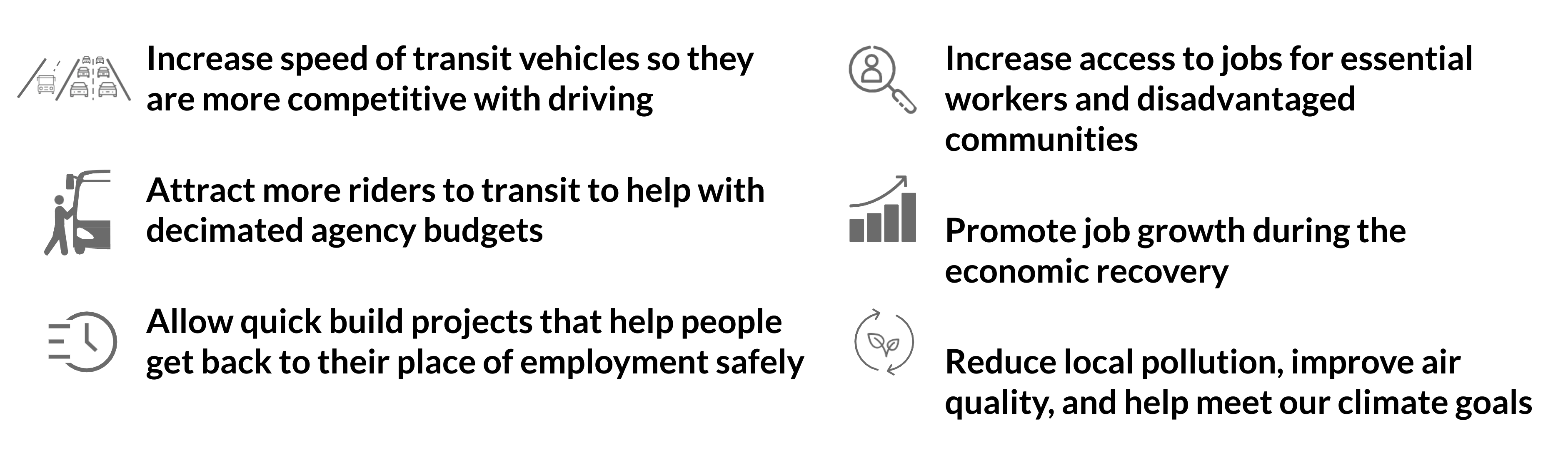

The goals of the bill are to:

• create safe, accessible and healthy communities for all;

• ensure reliable, high-quality transit for all;

• attract people back to transit;

• reduce climate pollution and congestion;

• reduce cumulative pollution burden in disadvantaged communities; and

• ensure meaningful involvement from communities impacted by the project.

With strict qualifying criteria, projects must be in an existing public right-of-way, be located in an urbanized area or urban cluster (50,000+ people), not add new auto capacity, not demolish affordable housing, and use a skilled and trained workforce. Projects that are over $100 million have additional criteria which include holding at least three public meetings, completion of a project business case to help the public engage in the project early, completion of a racial equity analysis and suggest mitigations for disproportionate impacts, and completion of a residential anti-displacement analysis on high-frequency projects in areas at risk of displacement.

The following organizations are co-sponsors of SB922:

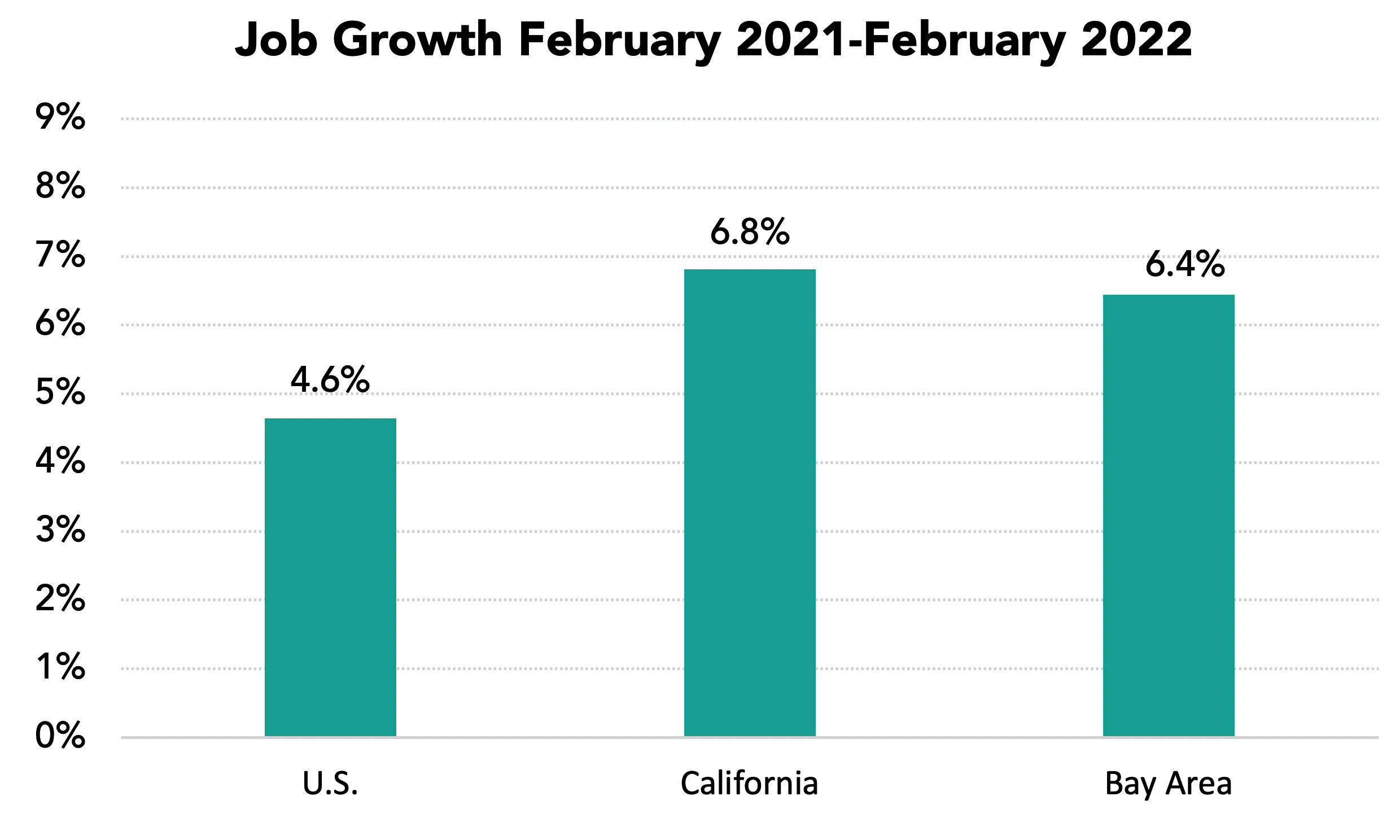

Bay Area Economy Continues Recovery but Still Lags the Nation

March 31, 2022

The Bay Area added 24,500 jobs in February and outpaced the nation in job growth over the past 12 months but still lags the state and nation in job recovery since April 2020

The highlights:

• Bay Area jobs increased by 6.4% between February 2021 and 2022 compared to a 4.6% increase in the nation and 6.8% gain in California.

• The Bay Area unemployment rate in February 2022 was 3.4% compared to 2.7% in the pre-pandemic low.

• Venture capital funding reached a record $105.4 billion in 2021 up from $49.8 billion in 2020.

• March 2022 brings major crosscurrents to the global, national and regional economy with the Russian invasion of Ukraine, rising interest rates amidst continuing high inflation, the easing of COVID cases and related activity restrictions and the ongoing Bay Area challenges of housing, transportation and competitiveness.

• Bay Area jurisdictions have been given large increases in their housing goals for the next eight years as a result of state legislation and policy to reduce overcrowding and increase affordability. Each jurisdiction is in the process of updating their Housing Elements in 2022 to meet state and regional policy goals and requirements.

The Bay Area Outpaced the Nation in Recent Job Growth

Bay Area jobs increased by 6.4% between February 2021 and February 2022 outpacing the national 4.6% growth rate. The region still lags the nation and state in the percentage of jobs recovered since April 2020 as a result of the large job losses in 2020.

By February 2022 the region had recovered 75.8% of the jobs lost between February and April 2020. This is a lower recovery rate than the state and nation, though the region has closed the gap in recent months.

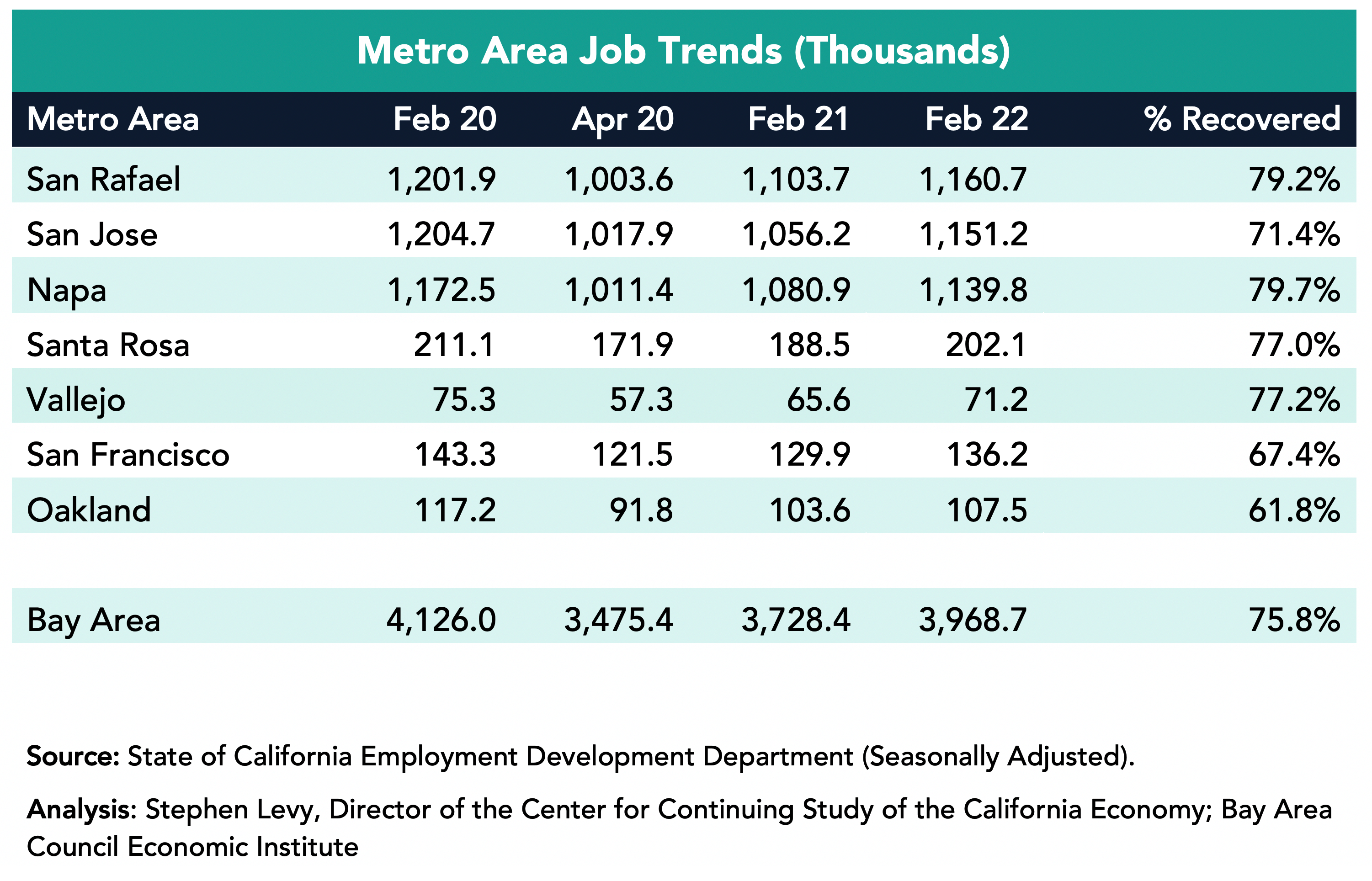

The Bay Area added 240,300 jobs in the past year led by a gain of 95,000 in the San Francisco metro area though SF has recovered just 71.4% of the jobs lost between February and April 2020. The San Jose metro area added 58,900 jobs and by February 2022 had recovered 79.7% of the jobs lost between February and April 2020. The Oakland metro area added 57,000 jobs.

Unemployment Rates Fell to 3.4% in the Region in February 2022 from 6.7% in February 2021.

The lowest rates were in the San Rafael metro area (2.7%) followed by the San Francisco and San Jose metro areas (2.9%) in February 2022.

The number of unemployed residents has fallen sharply from the April 2020 high and from February 2021 to 138,800 in February 2022.

But 90,000 Workers Have Not Rejoined the Workforce Since February 2020

Residents who are not in the labor force are not counted as unemployed. As a result, the number of unemployed residents can decline while some are still prevented by choice or lack of child care or work in industries that have not fully recovered.

Industries Were Affected Differently

Three sectors—Manufacturing, Transportation and Warehousing, and Information—exceeded pre-pandemic job levels in February 2022 and Professional and Business Services was close to full recovery. On the other hand, the Leisure and Hospitality sector recovered only 64.7% of lost jobs by February 2022 though travel and tourism are now picking up again. The Government sector still has fewer jobs now than in April 2020. The Construction and Education and Health Services sectors have also recovered most of the jobs between February and April 2020.

Housing Permits Rebound to 2019 Levels in 2021

Housing permit levels are up 35.5% in 2021 over 2020 levels and equaled permit levels in 2019. This year all Bay Area cities are required to update their Housing Elements to meet greatly increased regional and local jurisdiction housing goals. Below is a link to a report released on March 18th that I prepared at the request of the Silicon Valley Community Foundation to help residents understand and engage in their city’s Housing Element update process. Although the report focuses on five Midpeninsula cities—Cupertino, Menlo Park, Mountain View, Palo Alto and Sunnyvale—it has broad applicability for other communities. The report is part of an engagement effort led by SV@Home with local partners.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

Bay Area Economic Growth Estimates for 2021 Revised Upwards

March 21, 2022

Bay Area job growth in 2021 was revised upward in annual revisions released in March 2022 by EDD. At the same time, unemployment rates for December 2022 were slightly reduced. The Bay Area posted record VC funding in 2021. Housing permits rebounded to 2019 levels but remain far below region’s housing goals for the next 8 years. All Bay Area jurisdictions must update their Housing Elements in 2022 to meet state and regional housing goals and requirements.

The highlights:

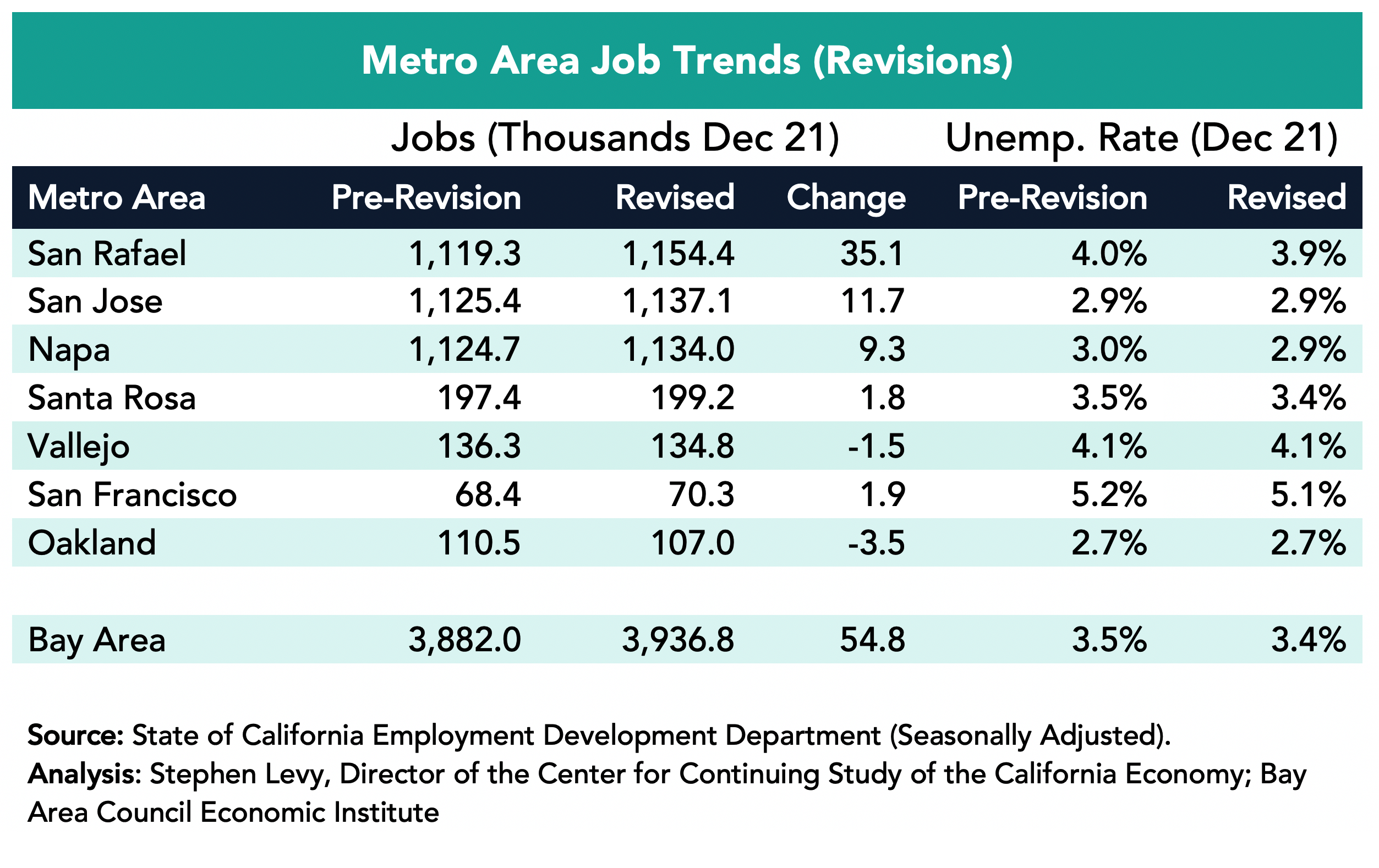

• Bay Area job estimates for December 2021 rose by 54,800 compared to the pre-revision estimates.

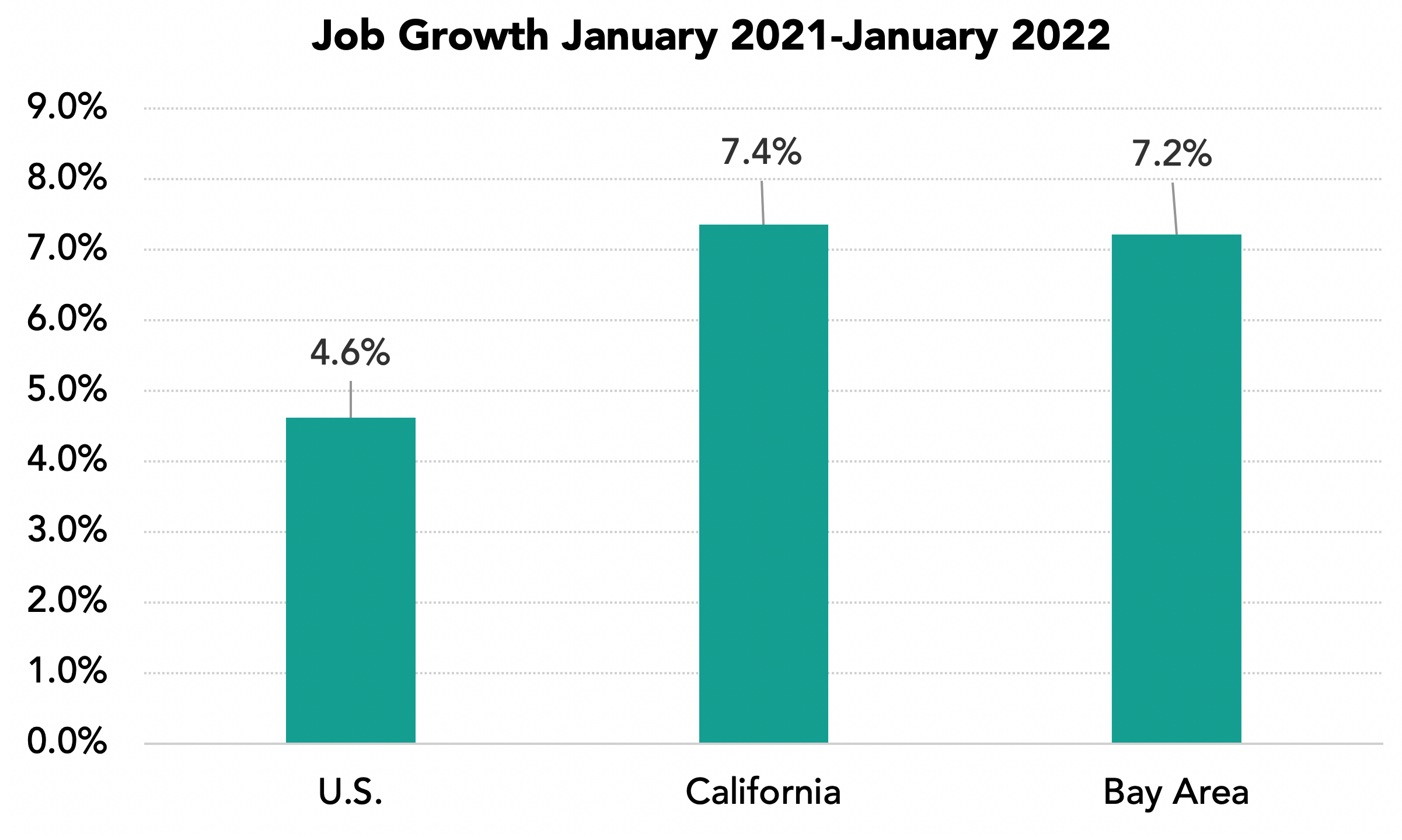

• Bay Area jobs increased by 7.2% between January 2021 and 2022 compared to a 4.6% increase in the nation and 7.4% gain in California.

• The Bay Area unemployment rate in December 2021 was 3.4% compared to 3.5% in the pre-revision estimate.

• March 2022 brings major crosscurrents to the global, national and regional economy with the Russian invasion of Ukraine, rising interest rates amidst continuing high inflation, the easing of COVID cases and related activity restrictions and the ongoing Bay Area challenges of housing, transportation and competitiveness.

• Bay Area jurisdictions have been given large increases in their housing goals for the next eight years as a result of state legislation and policy to reduce overcrowding and increase affordability. Each jurisdiction is in the process of updating their Housing Elements in 2022 to meet state and regional policy goals and requirements.

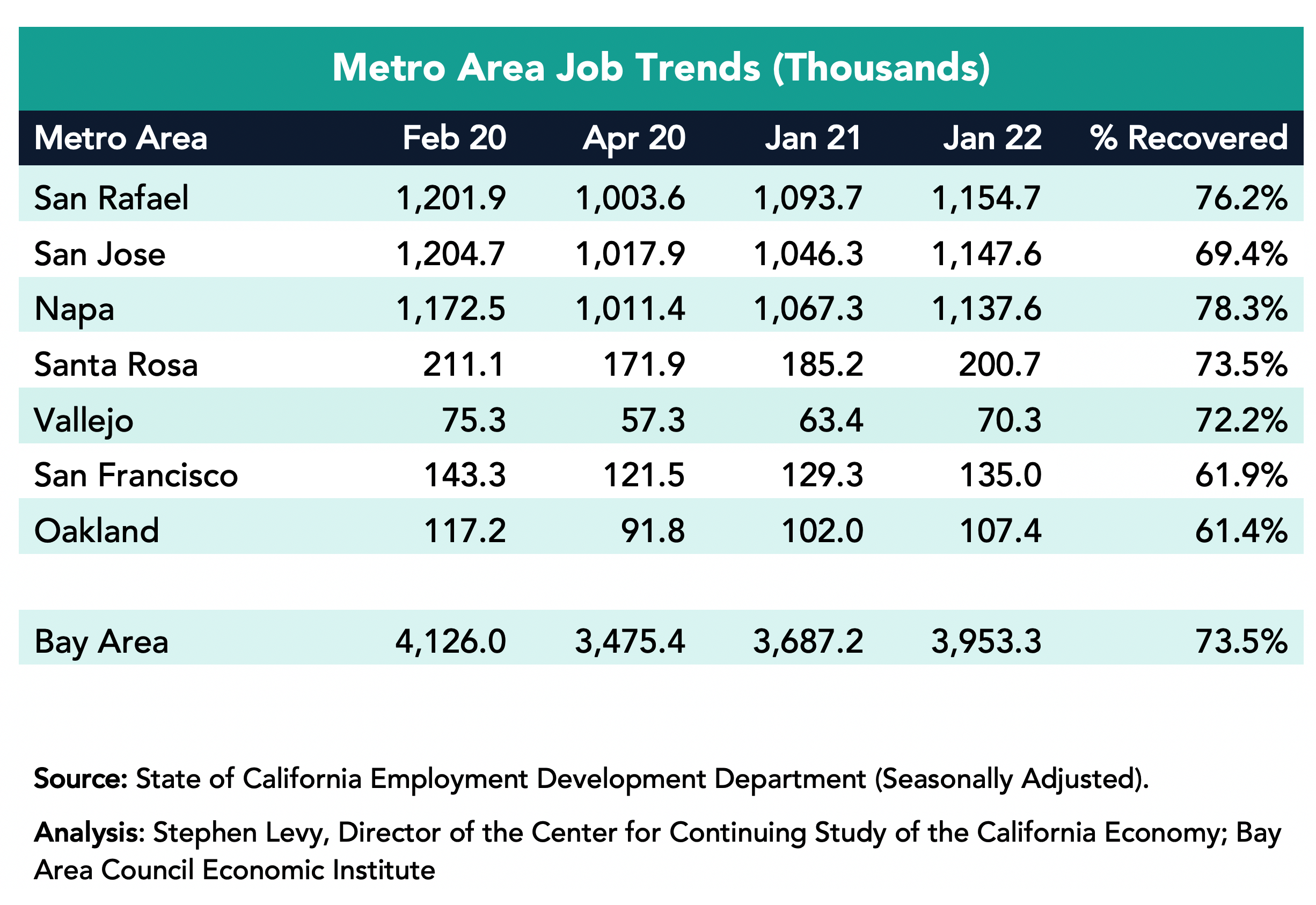

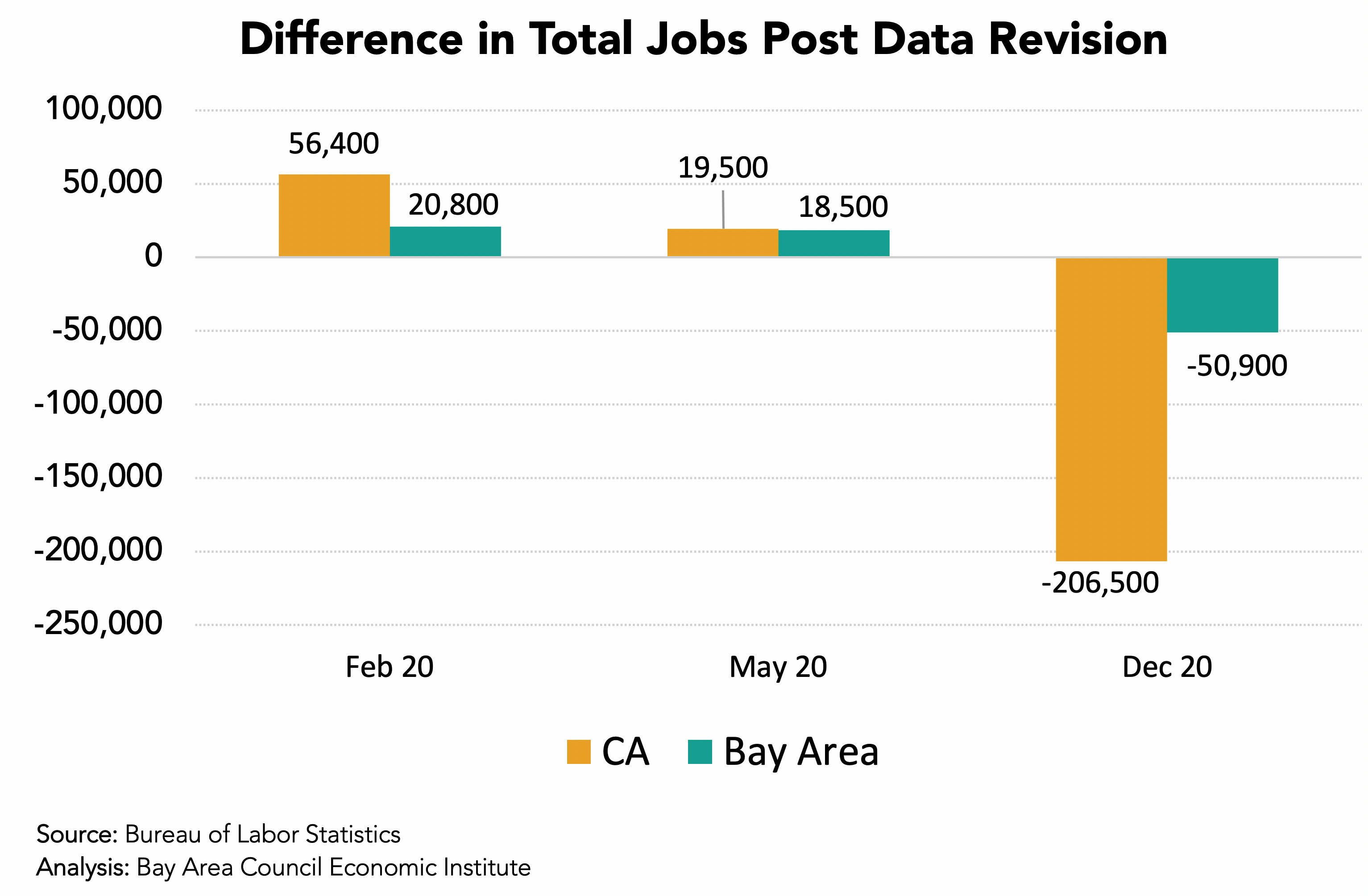

The Oakland Metro Area Had the Largest Upward Job Revision

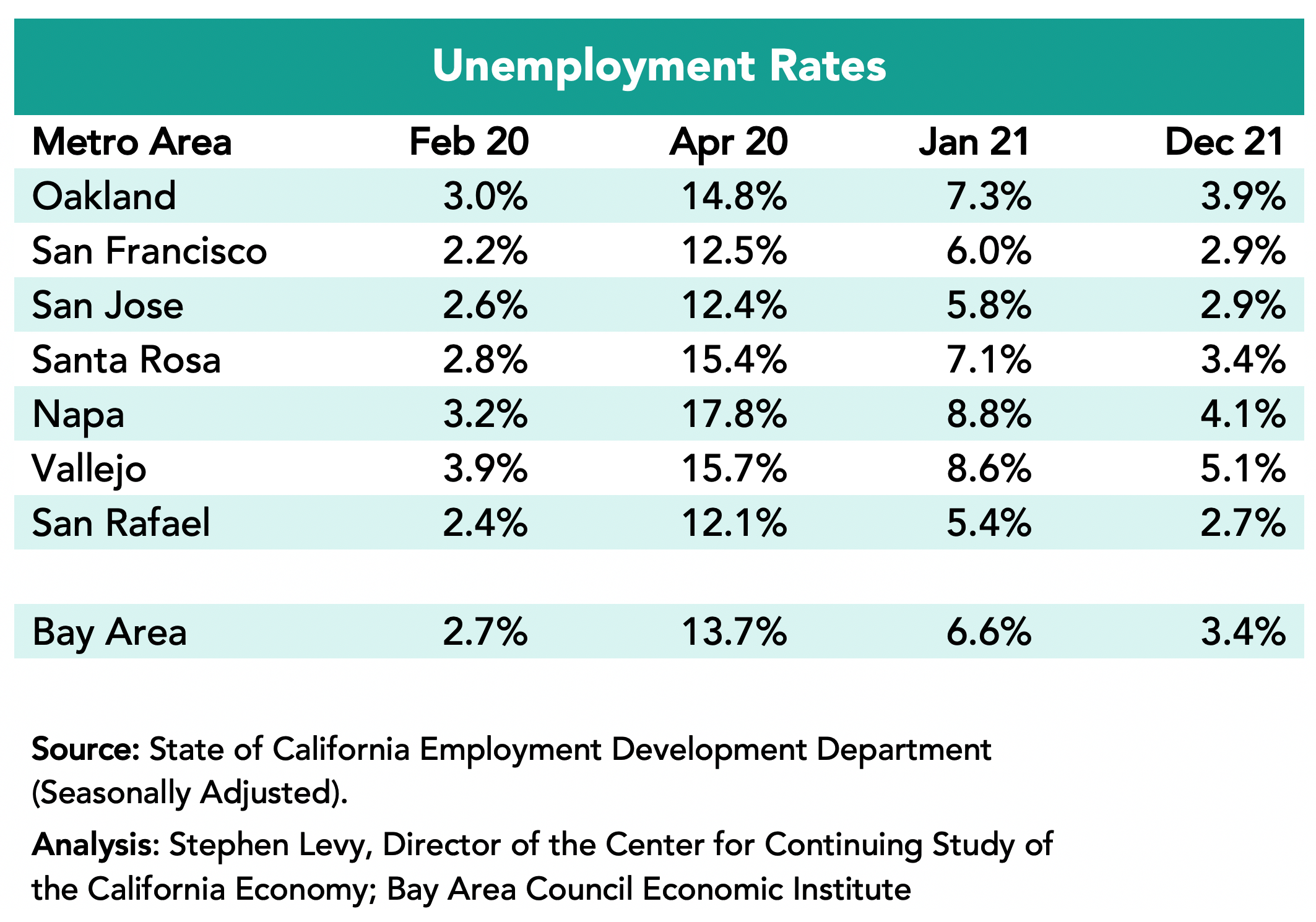

December job levels in the Oakland metro area were revised up by 35,100 or nearly 2/3 of the regional revision. Other gains were posted in the San Francisco and San Jose metro areas. Unemployment rate estimates were revised slightly downward in most metro areas. The regional unemployment rate for December 2021 was revised down to 3.4% from the pre-revision estimate of 3.5%.

The Bay Area Outpaced the Nation in 2021 Job Growth

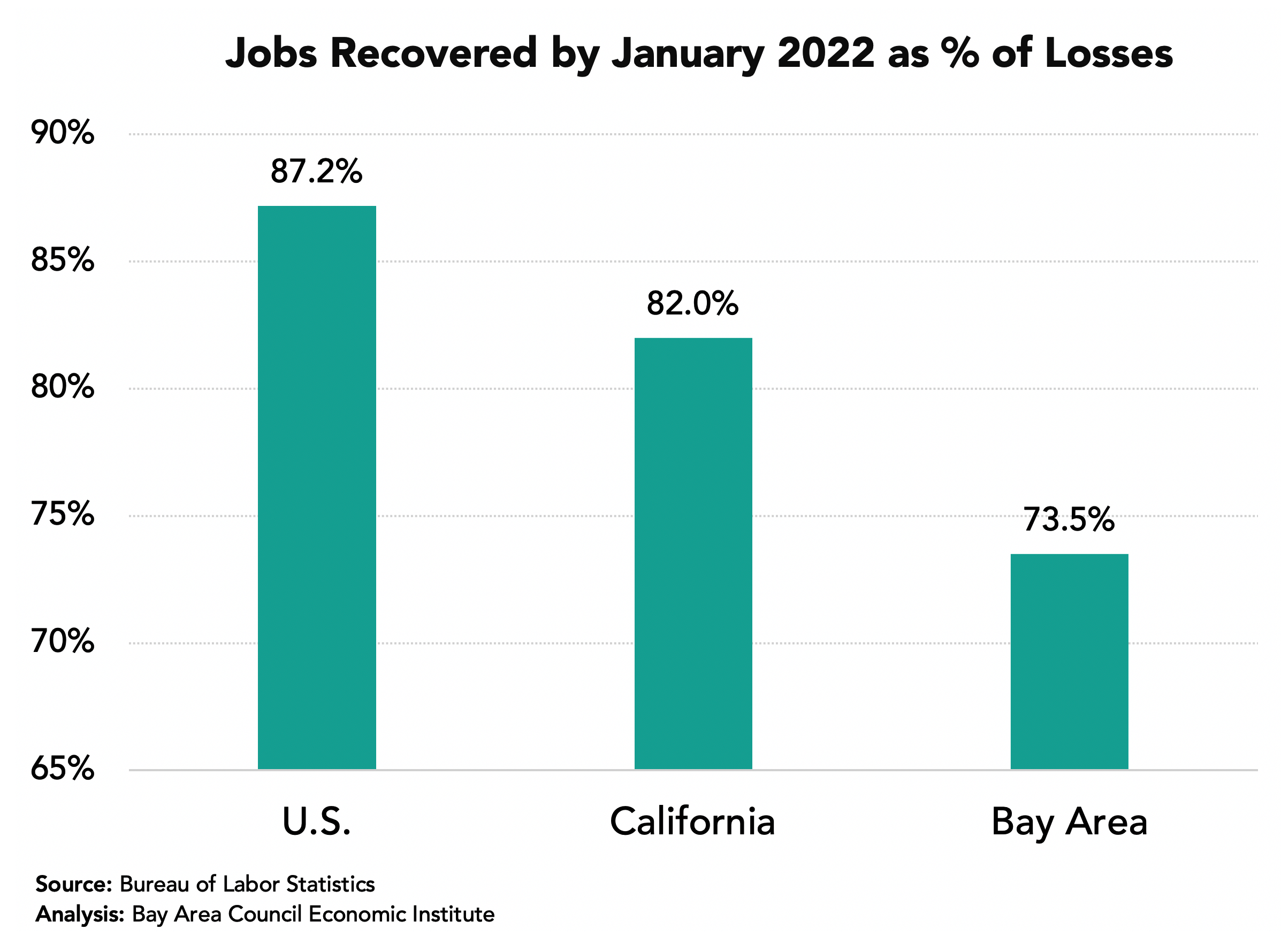

Bay Area jobs increased by 7.2% between January 2021 and January 2022 outpacing the national 4.6% growth rate. The region still lags the nation and state in the percentage of jobs recovered since April 2020 as a result of the large job losses in 2020.

By January 2022 the region had recovered 73.5% of the jobs lost between February and April 2020. This is a lower recovery rate than the state and nation, though the region has closed the gap in recent months.

The Bay Area added 266,100 jobs in the past year led by a gain of 101,300 in the San Francisco metro area though SF has recovered just 69.4% of the jobs lost between February and April 2020. The San Jose metro area added 70,300 jobs and by January 2022 had recovered 78.3% of the jobs lost between February and April 2020. The Oakland metro area added 61,000 jobs.

Unemployment Rates Fell to 3.4% in the Region in December 2021 from 6.6% in January 2021.

The lowest rates were in the San Rafael metro area (2.7%) followed by the San Francisco and San Jose metro areas (2.9%) in December 2021.

The number of unemployed residents has fallen sharply from the April 2020 high and from January 2021 to 138,500 in December 2021.

Industries Were Affected Differently

Four sectors—Manufacturing, Transportation and Warehousing, Information and Professional and Business Services—exceeded pre-pandemic job levels in December 2021. On the other hand, the Leisure and Hospitality sector recovered only 65.6% of lost jobs by December 2021 though travel and tourism are now picking up again. The Government sector still has fewer jobs now than in April 2020. The Construction and Education and Health Services sectors have recovered most of the jobs between February and April 2020.

Housing Permits Rebound to 2019 Levels in 2021

Housing permit levels are up 35.5% in 2021 over 2020 levels and equaled permit levels in 2019. This year all Bay Area cities are required to update their Housing Elements to meet greatly increased regional and local jurisdiction housing goals. Below is a link to a report released on March 18th that I prepared at the request of the Silicon Valley Community Foundation to help residents understand and engage in their city’s Housing Element update process. Although the report focuses on five Midpeninsula cities—Cupertino, Menlo Park, Mountain View, Palo Alto and Sunnyvale—it has broad applicability for other communities. The report is part of an engagement effort led by SV@Home with local partners.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

March 21, 2022

In 2020, China began to crackdown on technology companies through regulations and politics. Now in 2022, China’s massive tech sector collectively and publicly fell in line with China’s government and the Communist Party’s leadership. In this article on Medium.com, by Sean Randolph, Senior Director of the Institute, details China’s regulatory focus and politics, along with the implications for overseas businesses and governments.

China is rapidly connecting Hong Kong, Macao and nine cities in Guangdong Province into a regional finance, technology, manufacturing and tourism hub of 86 million people. Over the next decade, this Greater Bay Area (GBA) will mature into a global showcase for China’s economic model, “One Country-Two Systems” integration, and Belt and Road development strategy.

GBA hopes to partner with comparable regions worldwide, including the San Francisco Bay Area, in areas such as clean energy, health care, mobility and fintech. On December 9. 2021, Bay Area Council Economic Institute Senior Director Sean Randolph participated in a webinar to discuss in-depth findings from a new Institute report in collaboration with the Hong Kong Trade Development Council which assesses the commercial opportunities and political obstacles amid U.S.-China tensions.

Bay Area job losses in 2020 were a larger percent than in the state and nation. But in 2021 Bay Area and state job growth has outpaced the nation accompanied by large declines in unemployment. At the same time VC funding has reached record levels, housing permits have begun to rebound, the Governor signed several housing bills and the region is a leader in vaccinations and lowering COVID cases. Congress passed an infrastructure bill and international travel restrictions have been eased. The Bay Area still faces challenges in housing, transportation and other areas that affect our economic competitiveness and, in doing so, reduce our ability to meet equity and environmental goals.

The highlights:

• The Bay Area added 188,900 jobs between January and November 2021 (+5.2%) outpacing U.S. gains (4.1%) for this period. The regional unemployment rate fell from 6.6% to 3.8%. Job gains were led by the San Francisco and San Jose metro areas

• The U.S. economy is recovering even as inflation and supply chain challenges remain and COVID cases are rising again. At the same time immigration and tourism are on pace to increase and some infrastructure spending could start next year.

• The region is a state and national leader in vaccinations and reducing COVID cases that is allowing a return to more normal living here.

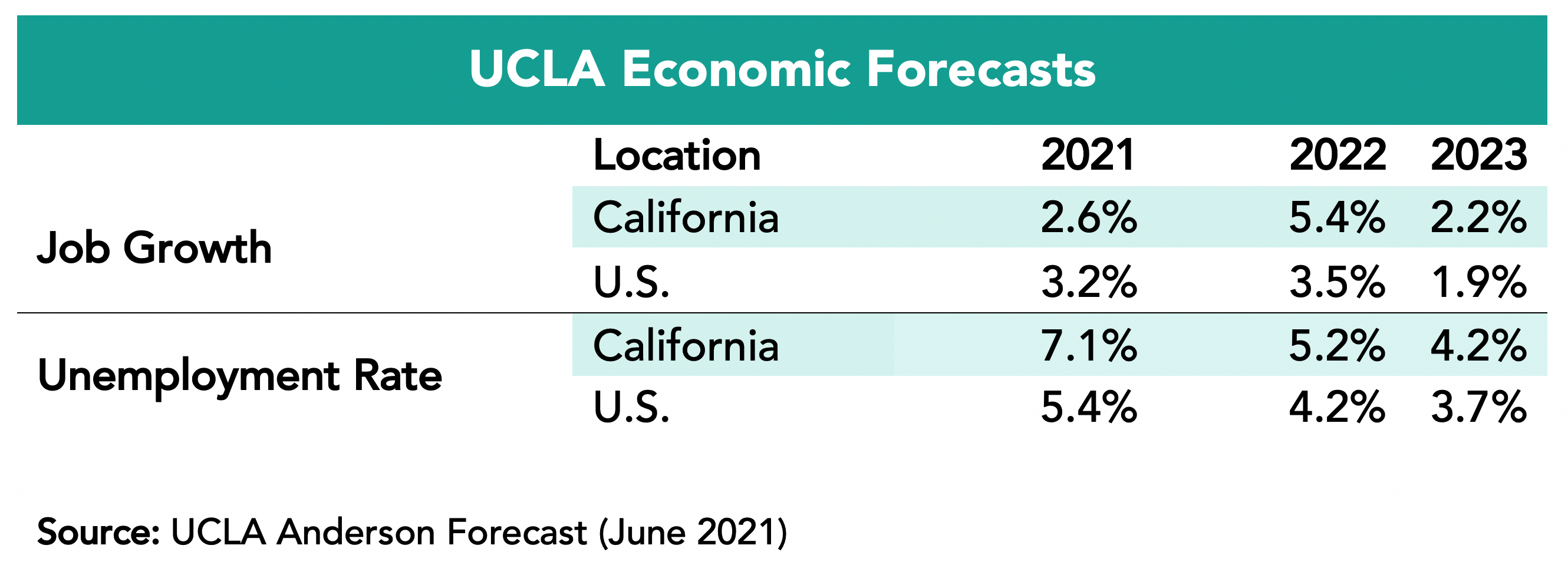

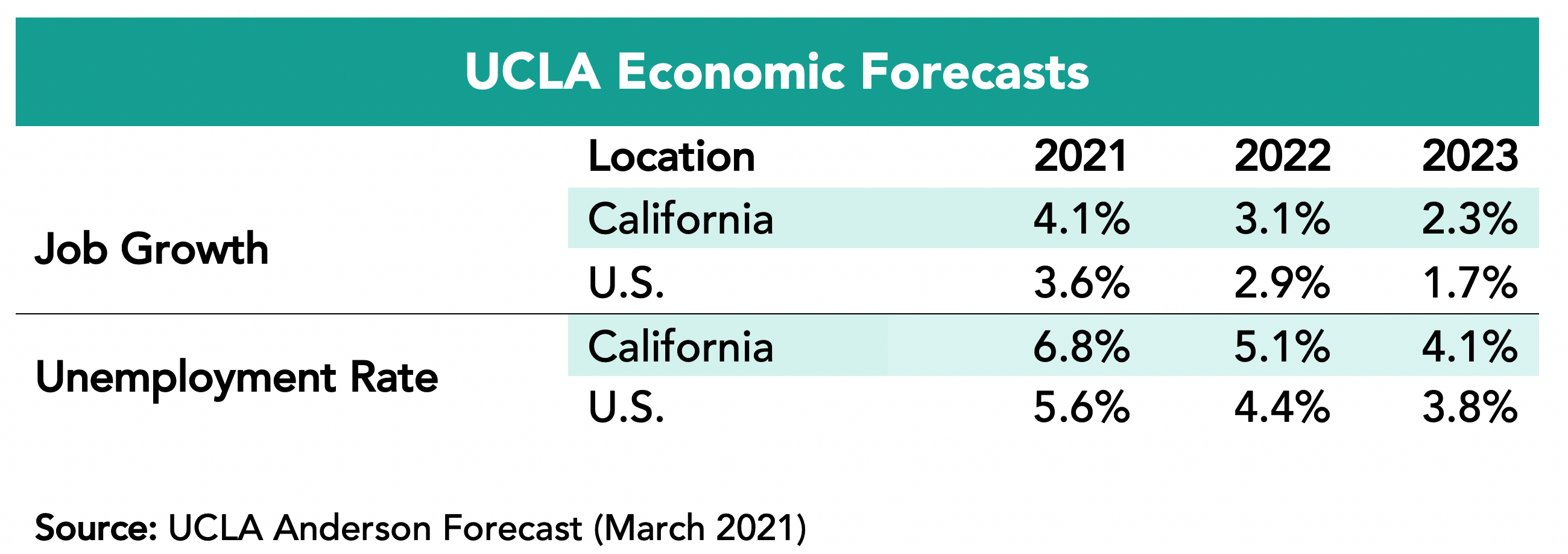

• The UCLA December 2021 forecast has the Bay Area and state outpacing the nation in job growth in 2022 and 2023.

Job Growth Continues But 2020 Losses Constrain the Rate of Recovery

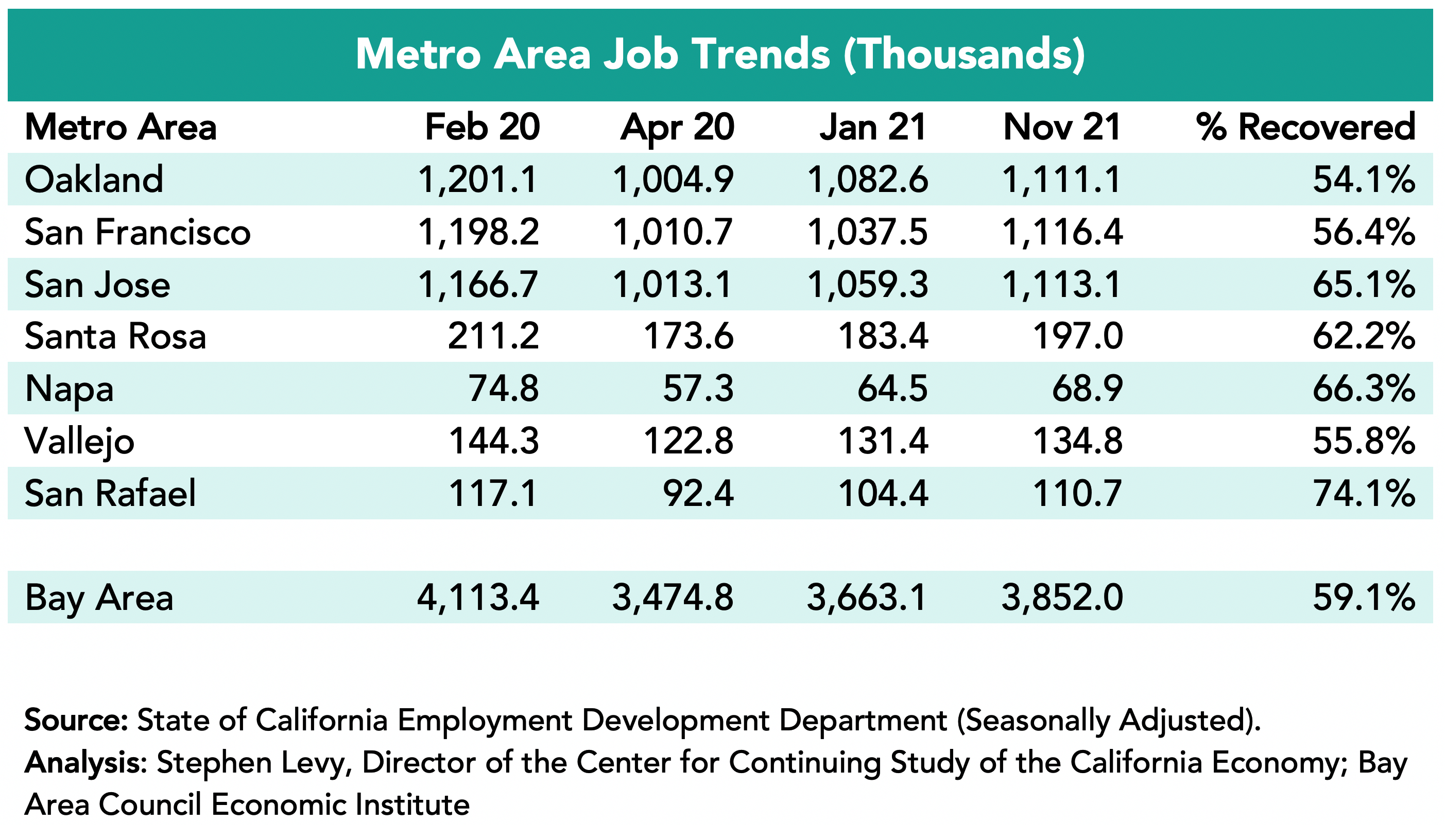

The Bay Area added 188,900 jobs since January 2021 led by a gain of 78,900 in the San Francisco metro area though SF has recovered just 56.4% of the jobs lost between February and April 2020. The San Jose metro area added 53,800 jobs but by November had recovered 65.1% of the jobs lost between February and April 2020. The San Jose, Napa, and San Rafael metro areas had the largest % job recovery by November 2021.

The Bay Area Had Recovered Just 59.1% of Lost Jobs by November 2021 Yet VC Funding is Surging and Tech Jobs Are Above Pre-Pandemic Levels

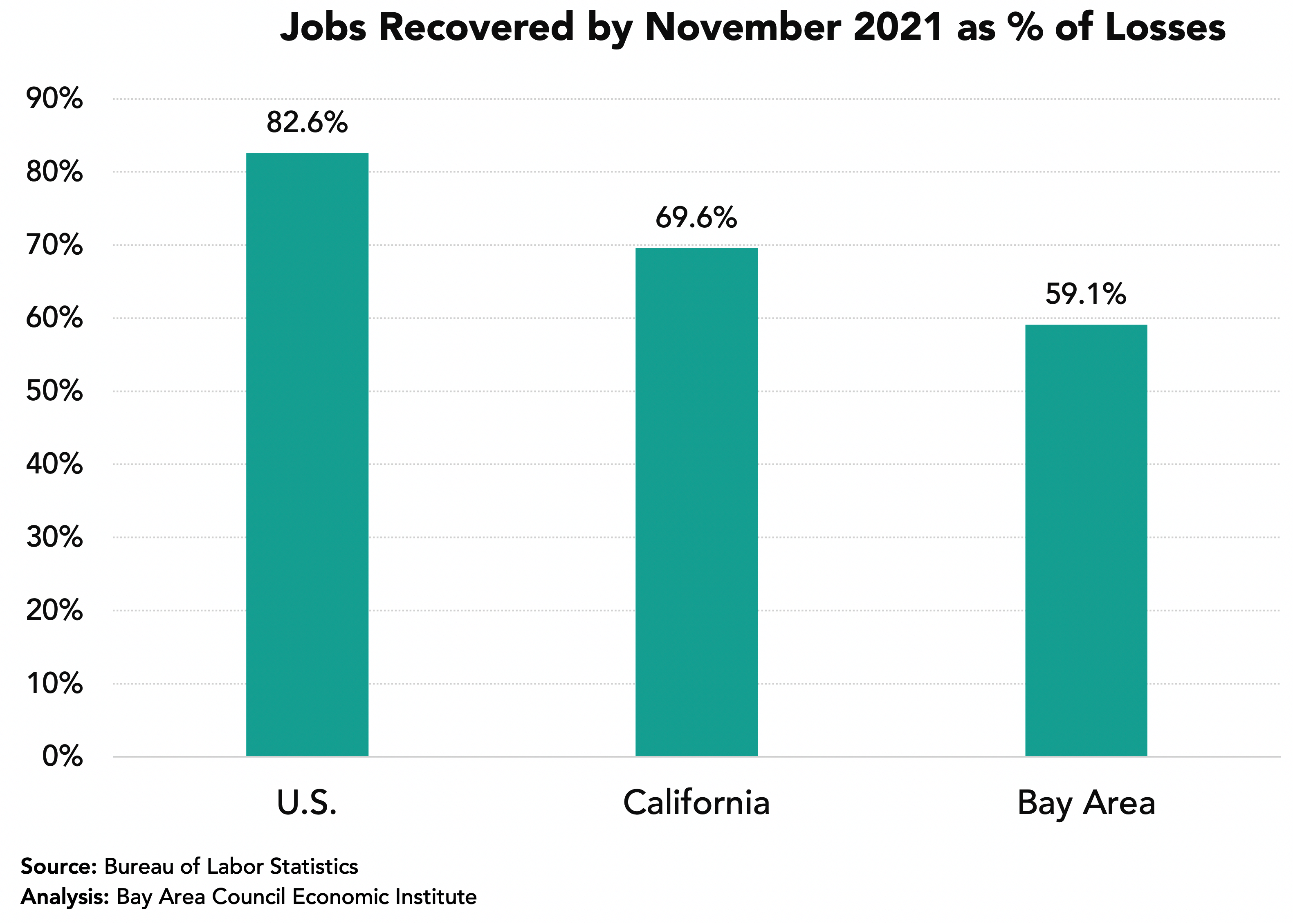

In November 2021 the Bay Area had recovered 59.1% of the jobs lost between February and April 2020 up from 29.4% in January. The state had recovered 69.6% up from 34.0% while the nation had recovered 82.2% of lost jobs up from 55.4%. At the same time VC funding in the first three quarters of 2021 was the highest on record. The Bay Area lagged the nation in 2020 job performance but has outpaced the nation in job growth so far in 2021 (5.2% versus 4.1%).

Unemployment Rates Fell to 3.8% in the Region in November 2021 from 6.6% in January 2021

The lowest rates were in the San Rafael metro area (2.9%) followed by the San Francisco and San Jose metro areas (3.2%) in November 2021.

The number of unemployed residents has fallen sharply from the April 2020 high and from January 2021.

Industries Were Affected Differently

The Information sector added jobs in comparison to before the pandemic hit. And the Professional & Business Services sector is also above pre-pandemic job levels. On the other hand, the Leisure and Hospitality sector recovered only 54.8% of lost jobs by November 2021 though travel and tourism are now picking up again. The Government sector has fewer jobs now than in April 2020 though many jobs are returning as schools and colleges reopen. The Construction and Manufacturing sectors have recovered most of the jobs between February and April 2020.

Housing Permits Up Over 2020 Levels, Trail 2019 Slightly

Housing permit levels are up over 2020 in the first ten months of 2021 but still slightly trail 2019 comparable months. But recently many new developments have been approved or proposed in places like Oakland and San Jose and in other cities as well as new developments being proposed.

Bay Area COVID Stats

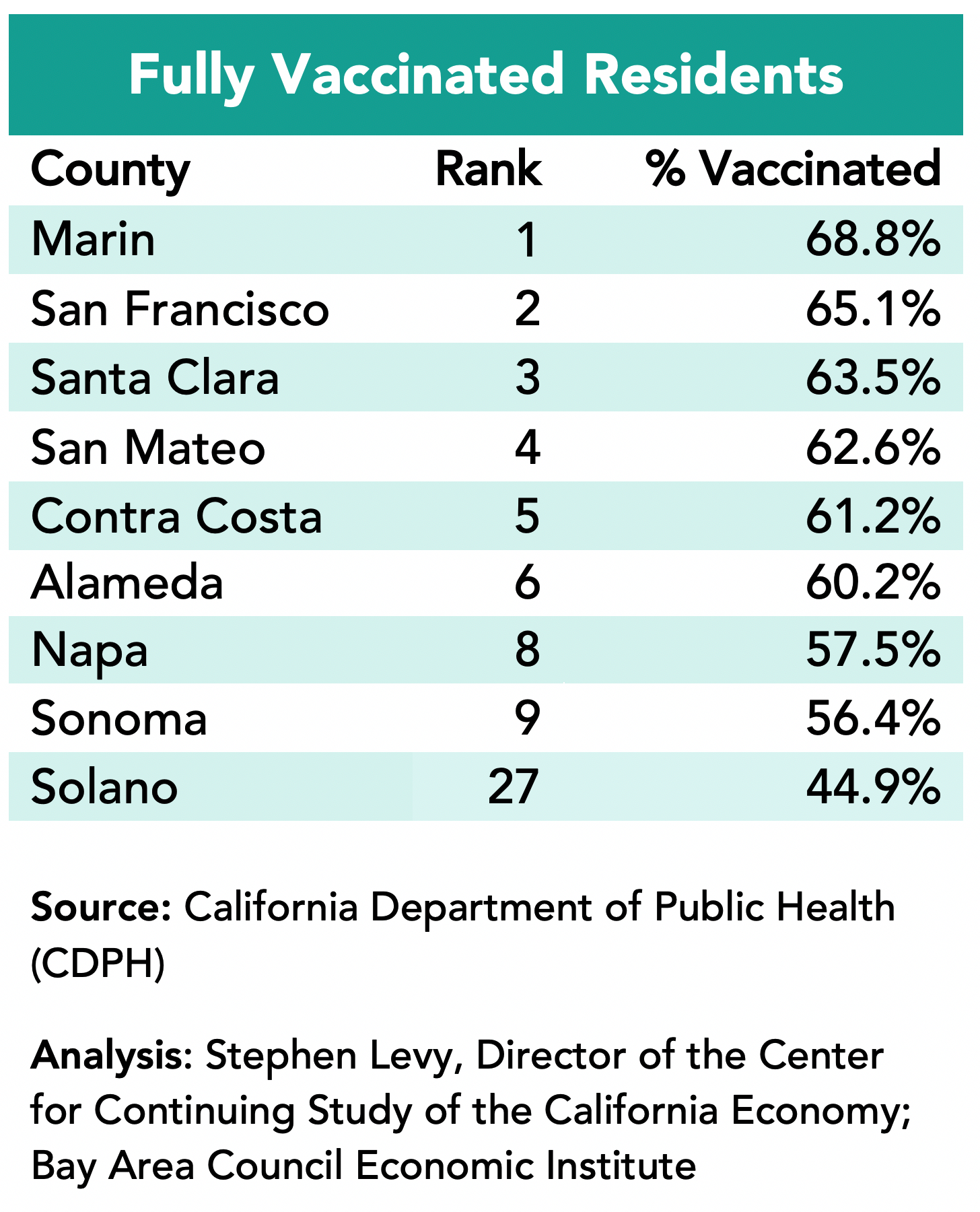

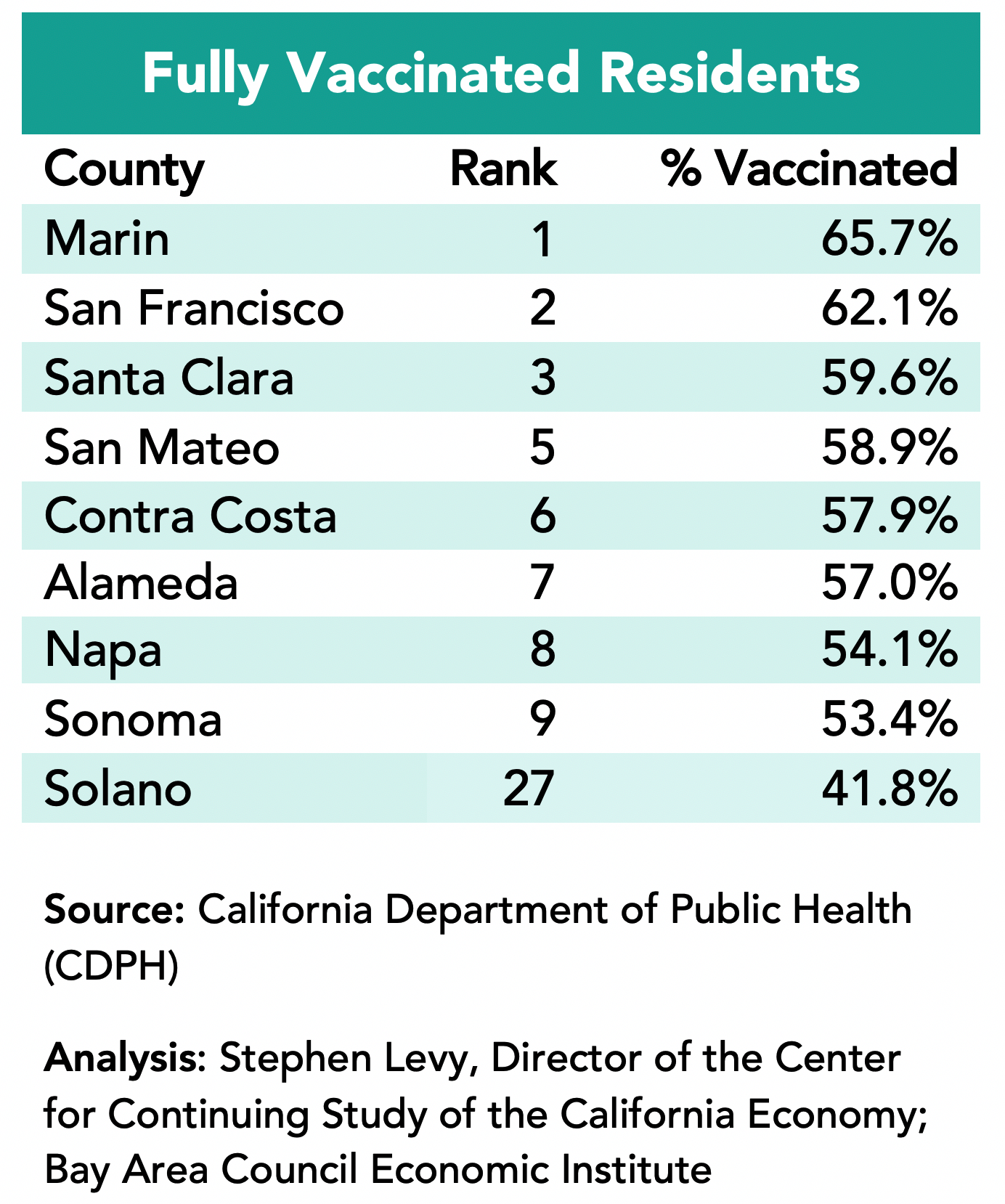

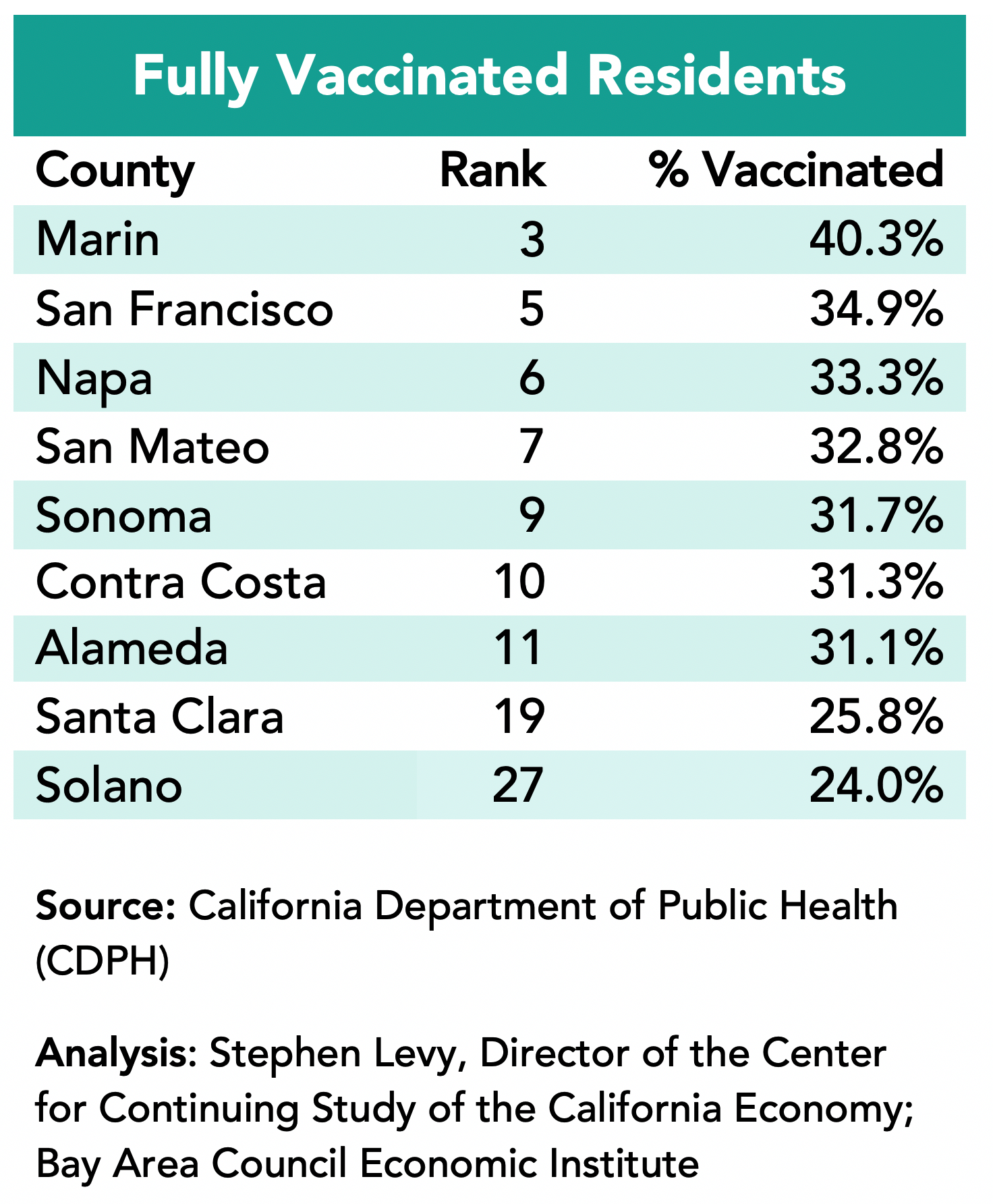

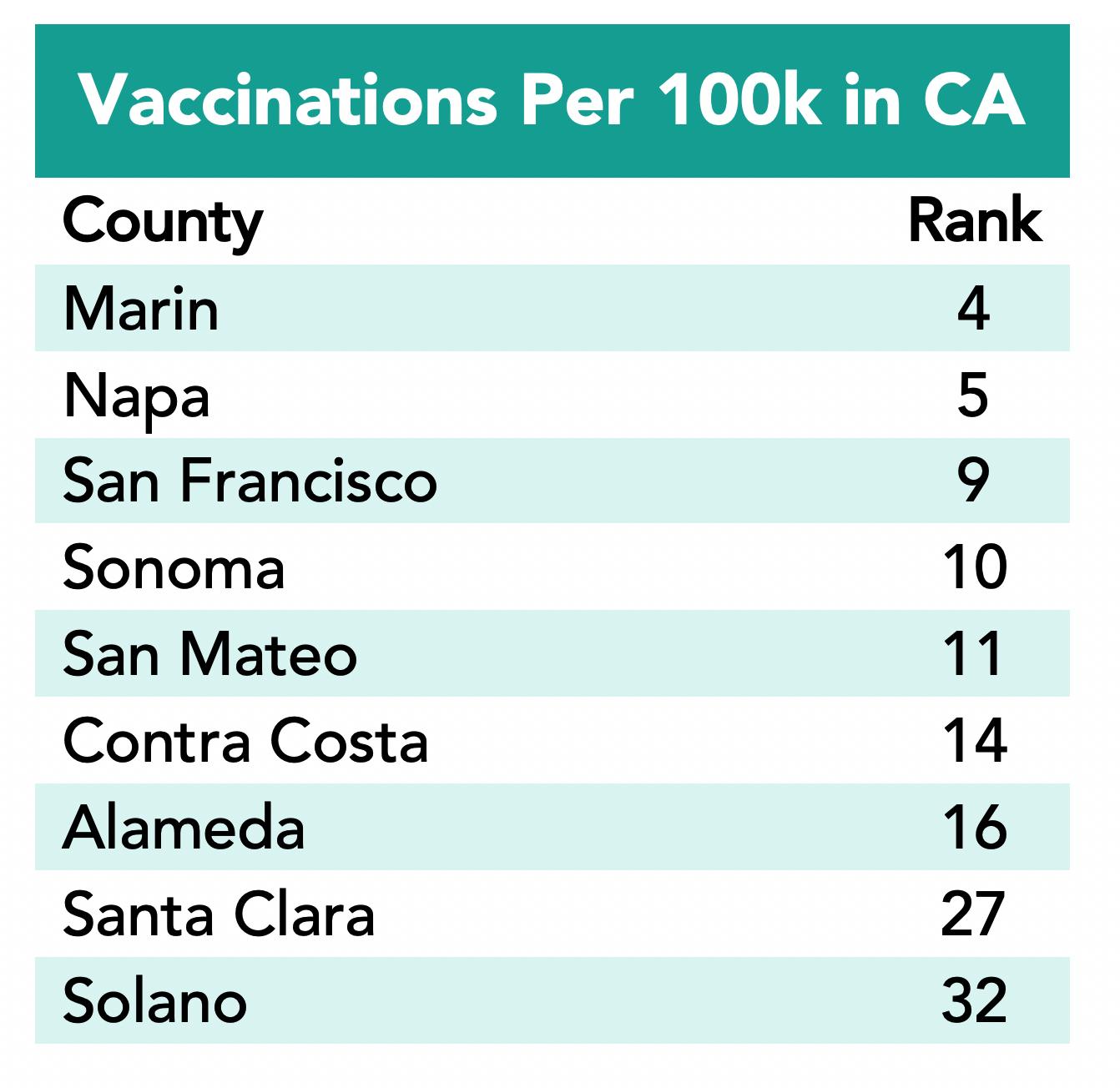

The top eight counties in terms of vaccination percentages (all but Solano) are from the Bay Area with all having more than 80% first doses and six having more than 75% fully vaccinated.

Large Challenges Remain:

We have the paradox of continuing reports of headquarters’ relocations outside of the region at the same the region is capturing record VC funding levels and tech jobs are slightly above pre-pandemic levels. Yet, the Bay Area Council warnings about losing our competitiveness remain as housing and mobility challenges are far from solved—the major causes of recent movements of companies and residents.

The rebound from pandemic related economic losses will continue but new policies are needed to maintain and improve the long-term competitiveness of the Bay Area economy. There is now increased movement to integrate our many transportation systems and agencies and pursue fare integration in an effort both to improve but to maintain the solvency of our main public transit options.

2022 is the year all Bay Area communities must update their Housing Elements to 1) identify sites attract and approve their allocation of new housing units affordable to major income groups, 2) develop programs and policies to overcome constraints and make the sites attractive to non-profit and market-rate developers and 3) comply with the state’s fair housing guidelines.

This is both a great opportunity and a challenge to combine meeting our equity, environmental and economic goals.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

December 9, 2021

Unique economic ties link the Bay Area and California with Israel. For a nation of only 9.3 million people, Israel has an extraordinary record of generating technology and startups. Its role as a major startup hub and source of innovation in fields such as water technology and management, agtech, fintech, mobility, and cybersecurity connect it deeply with Silicon Valley. Built also on shared values and aligned interests, that relationship is reflected in growing venture investment, large-scale acquisitions of Israeli companies, successful Israeli-founded unicorns and public companies in Silicon Valley, and extensive corporate and binational R&D. This article by Sean Randolph, Senior Director of the Institute, in the San Francisco Business Times, further details the connection between the Bay Area and Israel..

Bay Area job growth accelerated in September and October. At the same time VC funding has reached record levels, housing permits have begun to rebound, the Governor signed several housing bills and the region is a leader in vaccinations and lowering COVID cases. Congress passed an infrastructure bill and international travel restrictions have been eased. The Bay Area still faces challenges in housing, transportation and other areas that affect our economic competitiveness and, in doing so, reduce our ability to meet equity and environmental goals.

The highlights:

• The Bay Area added 178,600 jobs between January and October 2021 (+4.9%) outpacing U.S. gains (3.9%) for this period. The regional unemployment rate fell from 6.6% to 4.4%. Job gains were led by the San Francisco and San Jose metro areas

• The U.S. economy is recovering even as inflation and supply chain challenges remain and COVID cases are rising again. At the same time immigration and tourism are on pace to increase and some infrastructure spending could start next year.

• The region is a state and national leader in vaccinations and reducing COVID cases that is allowing a return to more normal living here.

• The long-term Bay Area economic challenges remain with only slow progress on housing, transportation and economic competitiveness, challenges at the front of the Bay Area Council policy agenda.

Job Growth is Steady but Disappointing Compared to the Nation

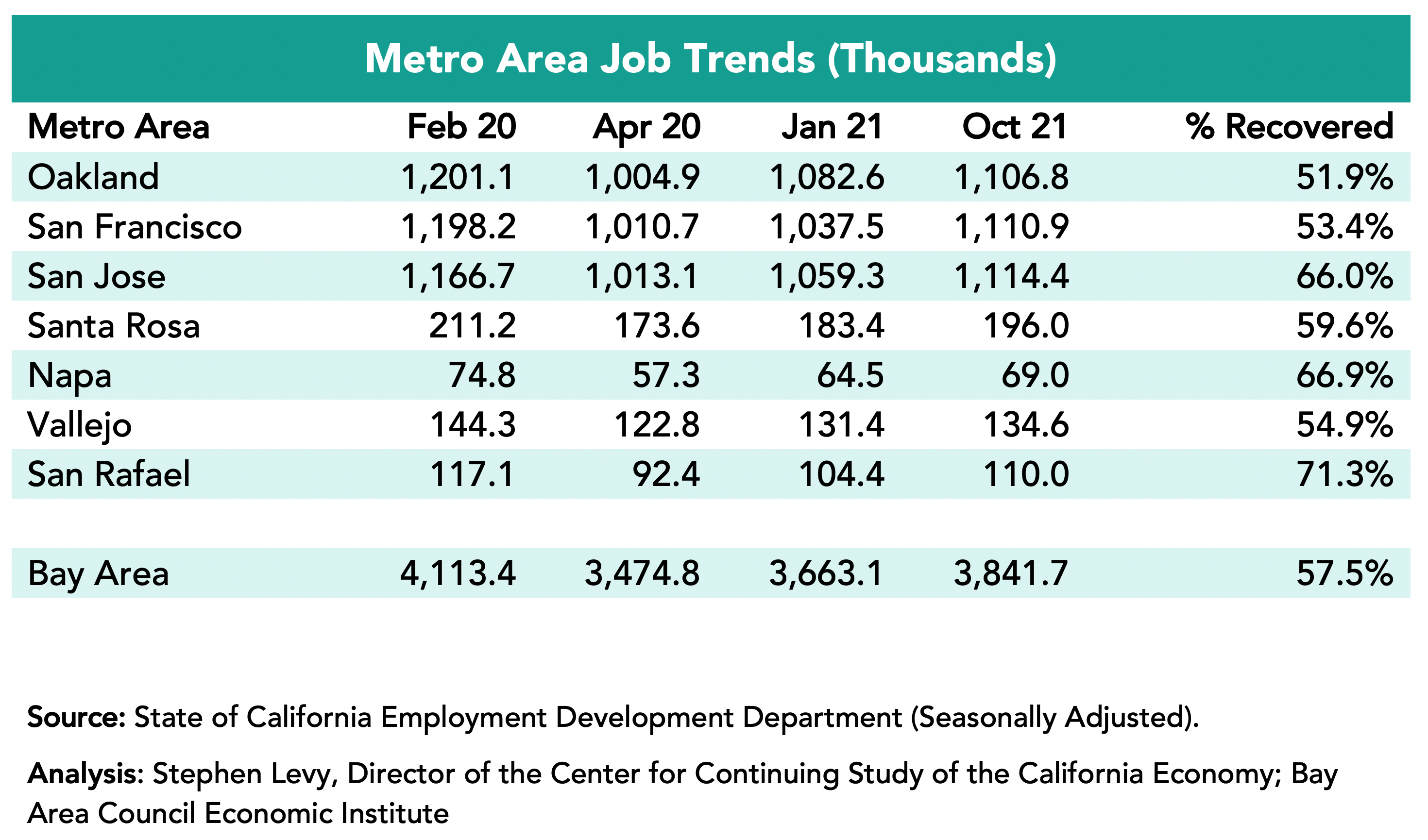

The Bay Area added 178,600 jobs since January 2021 led by a gain of 73,400 in the San Francisco metro area though SF has recovered just 53.4% of the jobs lost between February and April 2020 as job gains are offset by companies moving jobs out of SF. The San Jose metro area added 55,100 jobs but by October had recovered 66.0% of the jobs lost between February and April 2020. The San Jose, Napa, and San Rafael metro areas had the largest % job recovery by October August 2021.

Job growth accelerated in the past two months with gains of 21,100 jobs in October and an upward revised 18,200 jobs in September. There were strong gains in Professional and Business Services as well as a continuing recovery in Leisure and Hospitality.

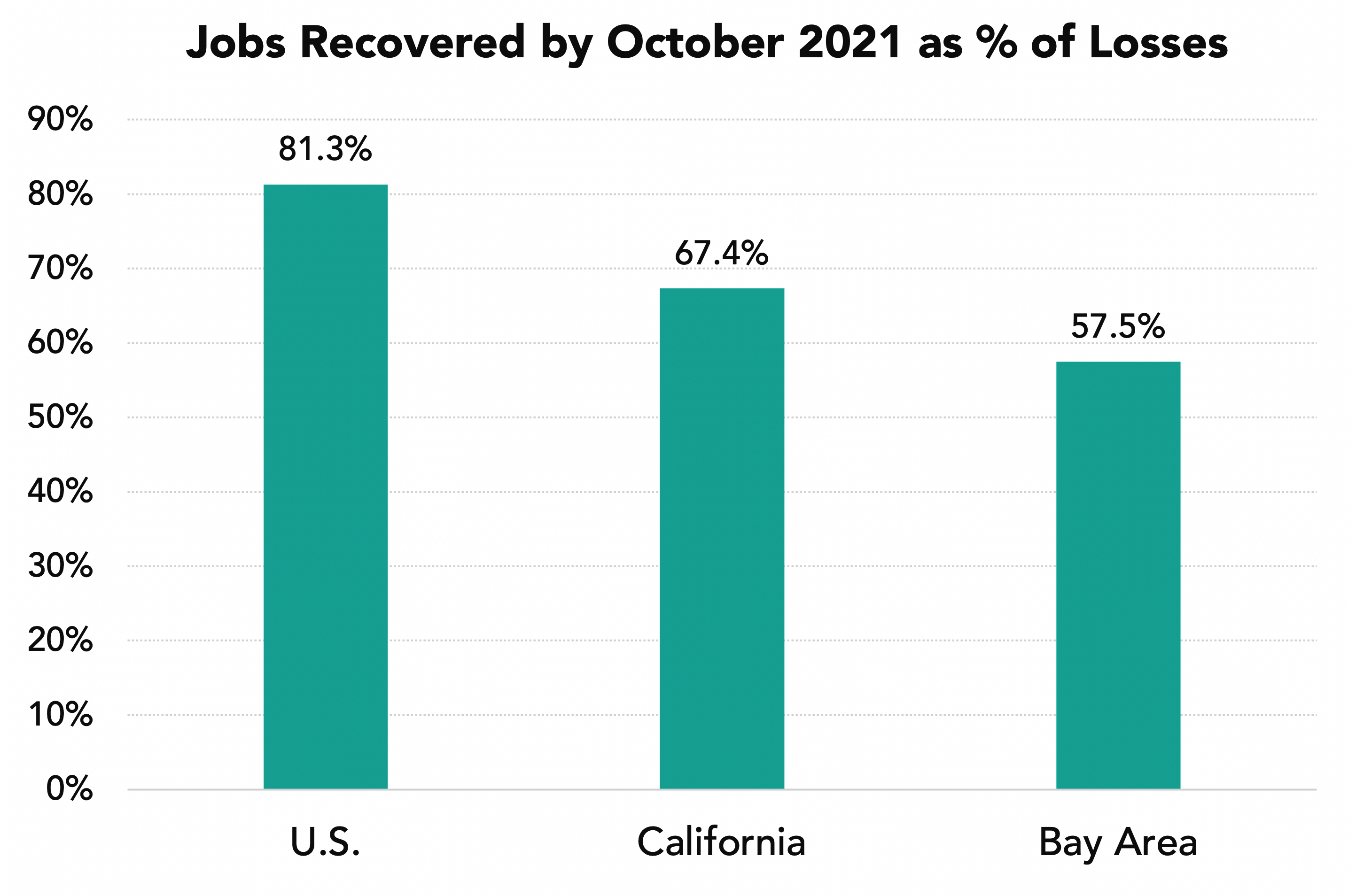

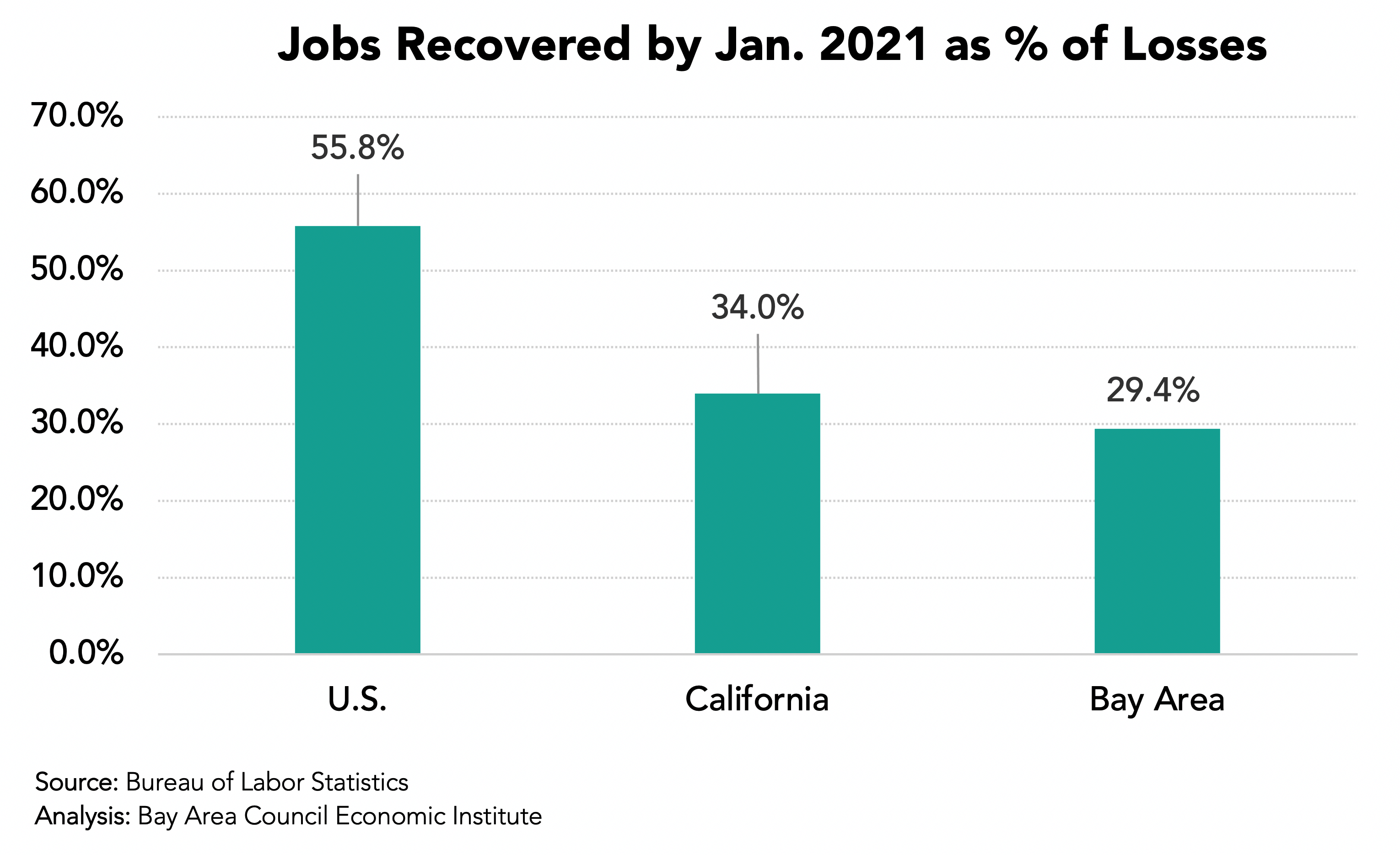

The Bay Area Had Recovered Just 57.5% of Lost Jobs by October 2021 Yet VC Funding is Surging and Tech Jobs Are Above Pre-Pandemic Levels

In October 2021 the Bay Area had recovered 57.5% of the jobs lost between February and April 2020 up from 29.4% in January. The state had recovered 67.4% up from 34.0% while the nation had recovered 81.3% of lost jobs up from 55.4%. At the same time VC funding in the first three quarters of 2021 was the highest on record. The Bay Area lagged the nation in 2020 job performance but has outpaced the nation in job growth so far in 2021 (4.9% versus 3.9%).

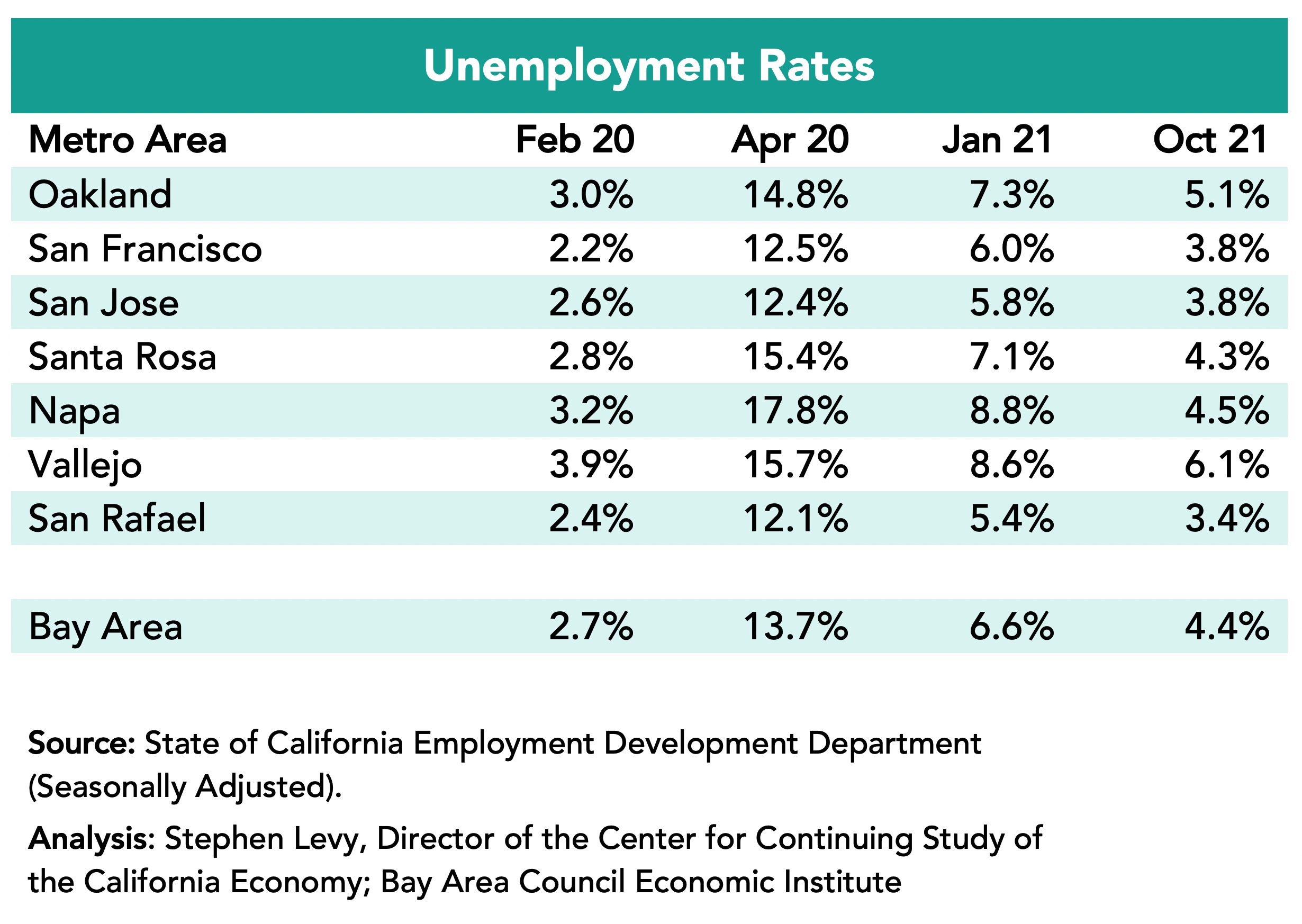

Unemployment Rates Fell to 4.4% in the Region in October 2021 from 6.6% in January 2021.

The lowest rates were in the San Rafael metro area (3.4%) followed by the San Francisco and San Jose metro areas (3.8%) in October 2021.

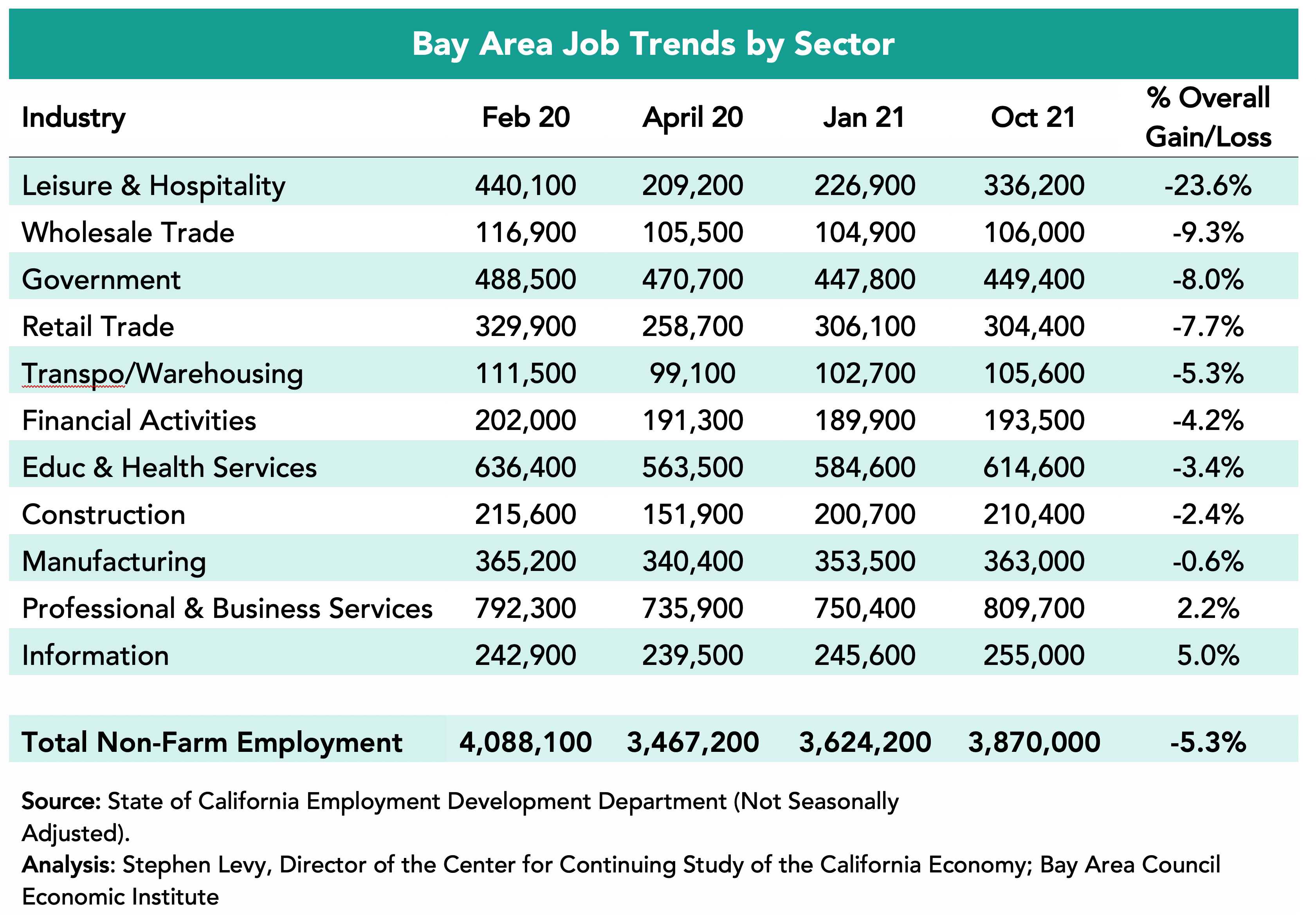

Industries Were Affected Differently

The Information sector actually added jobs compared to before the pandemic hit. And the Professional & Business Services sector is also above pre-pandemic job levels. On the other hand, the Leisure and Hospitality sector recovered only 55.0% of lost jobs by October 2021 though travel and tourism are now picking up again. The Government sector has fewer jobs now than in April 2020 though many jobs may be returning as schools and colleges reopen. The Construction and Manufacturing sectors have recovered most of the jobs between February and April 2020.

Housing Permits Up Over 2020 Levels, Trail 2019 Slightly

Housing permit levels are up over 2020 in the first nine months of 2021 but still slightly trail 2019 comparable months. But recently many new developments have been approved or proposed in places like Oakland and San Jose and in other cities as well as new developments being proposed.

Bay Area COVID Stats

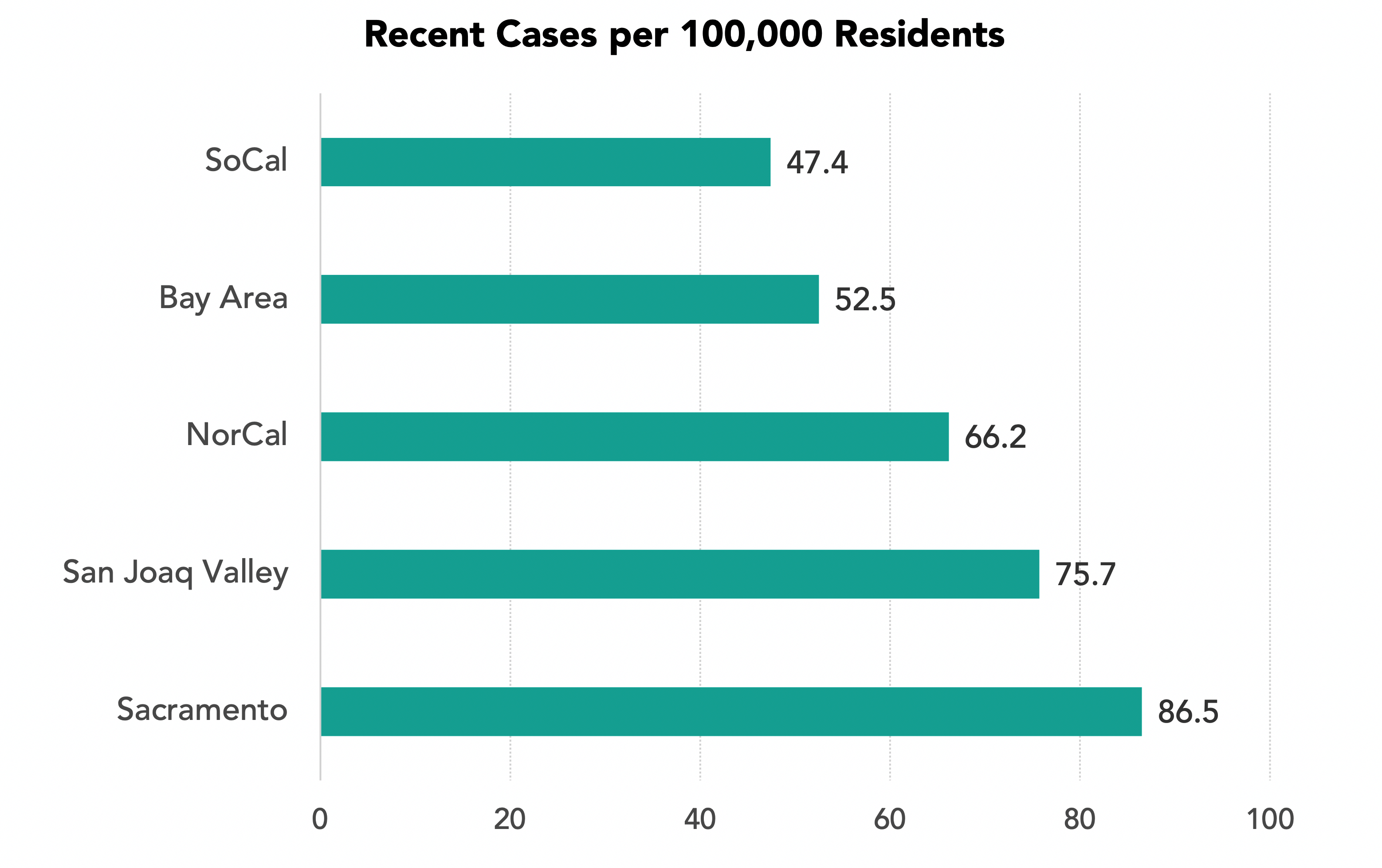

The top eight counties in terms of vaccination %s (all but Solano) are from the Bay Area with all having more than 75% first doses and six having more than 70% fully vaccinated. The Bay Area has by far the lowest number of new cases per capita and all 9 Bay Area counties are in the 15 counties with the lowest recent per capita cases are in the Bay Area.

Large Challenges Remain:

We have the paradox of continuing reports of headquarters’ relocations outside of the region at the same the region is capturing record VC funding levels and tech jobs are slightly above pre-pandemic levels. Yet, the Bay Area Council warnings about losing our competitiveness remain as housing and mobility challenges are far from solved—the major causes of recent movements of companies and residents.

The rebound from pandemic related economic losses will continue but new policies are needed to maintain and improve the long-term competitiveness of the Bay Area economy. There is now increased movement to integrate our many transportation systems and agencies and pursue fare integration in an effort both to improve but to maintain the solvency of our main public transit options.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

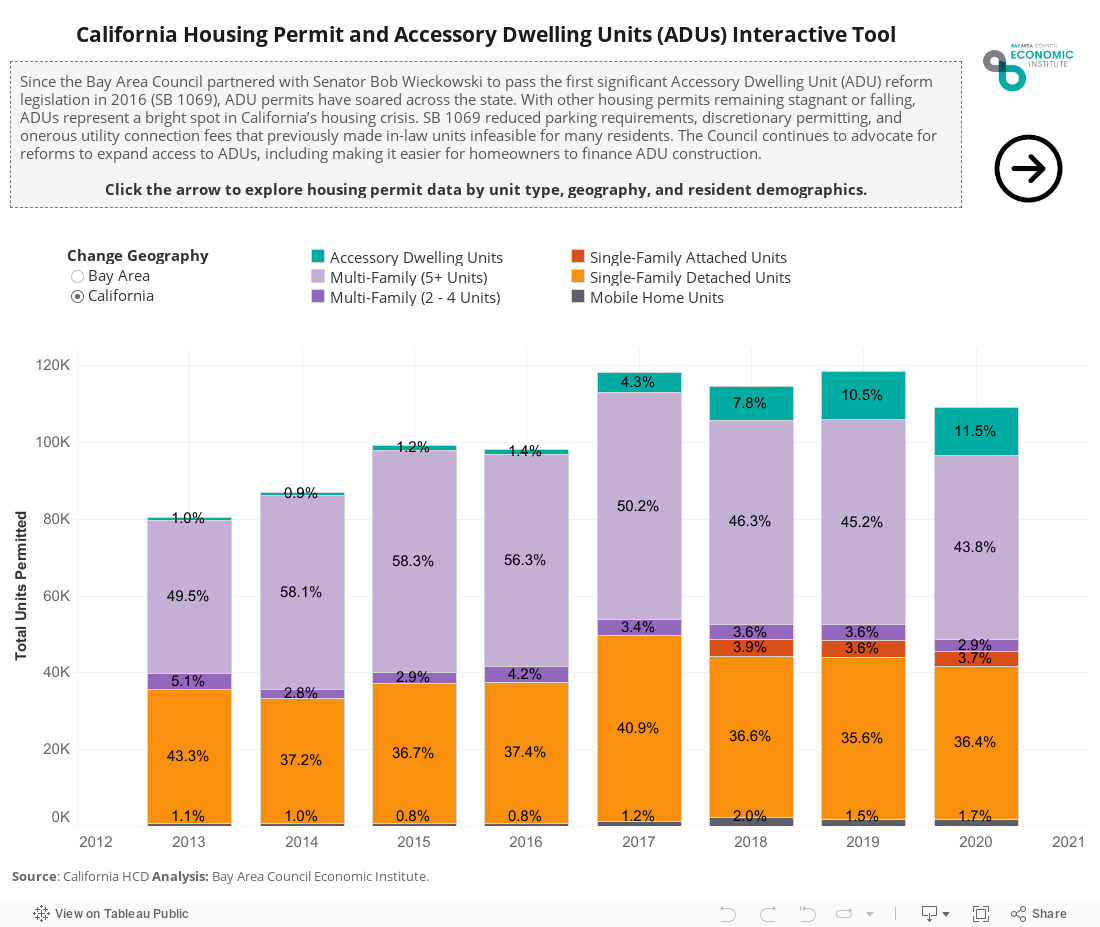

An analysis by the Bay Area Council Economic Institute using data from the California Department of Housing and Community Development (HCD) shows Accessory Dwelling Units (ADUs) accounted for 13.4 percent of all housing permit types in the Bay Area in 2020, a significant jump from 3.2 percent in 2016. In Marin and Napa, the Bay Area counties permitting the lowest amount of housing, ADUs are the majority of permits, making up 49.4 percent of all housing permits in Marin County and 40.3 percent in Napa County.

Since the Bay Area Council partnered with Senator Bob Wieckowski to pass the first significant Accessory Dwelling Unit (ADU) reform legislation in 2016 (SB 1069), ADU permits have soared across the state. With other housing permits remaining stagnant or falling, ADUs represent a bright spot in California’s housing crisis. The Council continues to advocate for reforms to expand access to ADUs, including most recently sponsoring legislation by Assemblymember Phil Ting (AB 561) making it easier for homeowners to finance ADU construction. For questions or to engage in the Council’s housing policy work,please contact Senior Policy Manager, Kelli Fallon. For questions on this data visualization,please contact Research Manager, Abby Raisz.

Image Source: Housable

Modest Job Growth, Good News on Housing and COVID

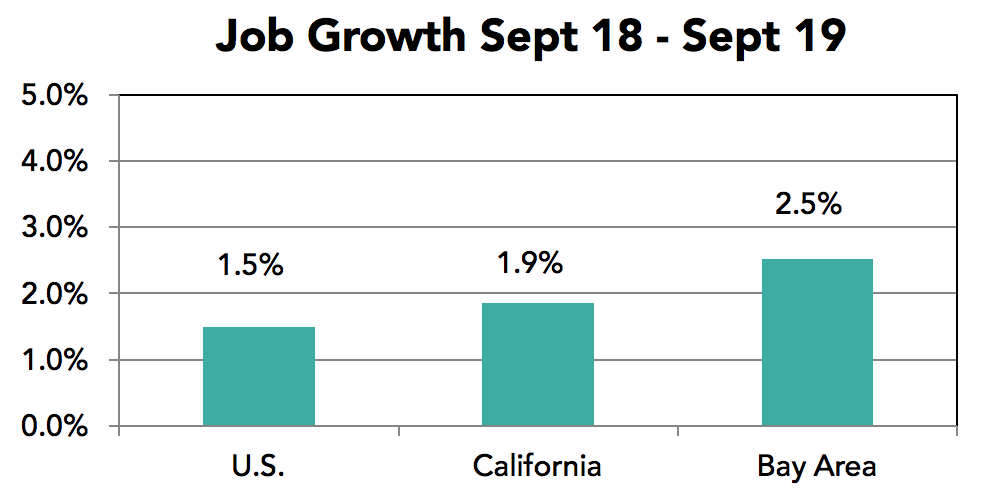

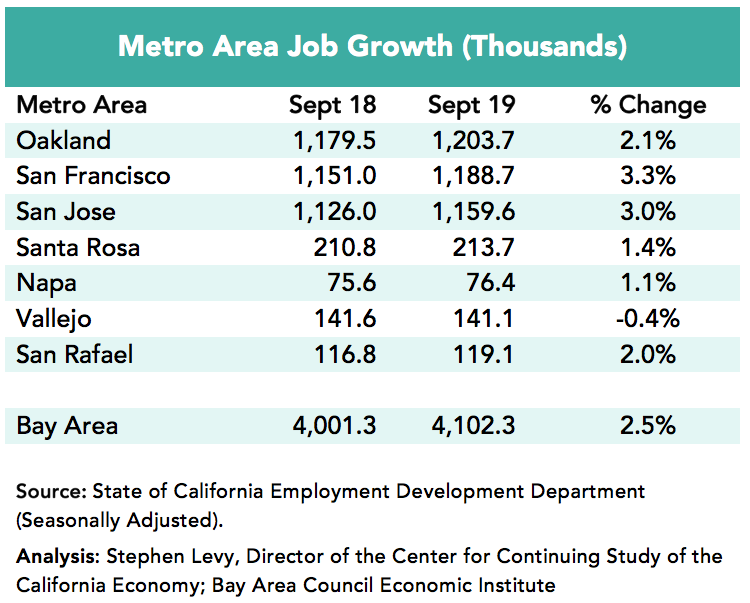

Sept 22, 2021

The Bay Area has posted modest but disappointing job gains since March. At the same time VC funding is strong, housing permits have begun to rebound, the Governor signed several housing bills and the region is a leader in vaccinations and lowering COVID cases. The U.S. economic outlook and federal policies have improved with positive implications for our region. The Bay Area still faces challenges in housing, transportation and other areas that affect our economic competitiveness and, in doing so, reduce our ability to meet equity and environmental goals.

The highlights:

• The Bay Area added 141,500 jobs between January and August 2021 and the regional unemployment rate fell from 6.6% to 5.5%. Job gains were led by the San Francisco and San Jose metro areas and a rebound in the restaurant and tourist sectors.

• The U.S, and Bay Area economic outlook has been upgraded by the $1.9 billion COVID relief package, the likely passage of a major infrastructure package, and positive movement on the safety net and environmental investments and the possibility of more favorable immigration policies that all play to Bay Area strengths.

• The region is a state and national leader in vaccinations and reducing COVID cases that is allowing a return to more normal living here

• The long-term Bay Area economic challenges remain with only slow progress on housing, transportation and economic competitiveness, challenges at the front of the Bay Area Council policy agenda.

Job Growth is Steady but Disappointing Compared to the Nation

The Bay Area added 141,500 jobs since January 2021 led by a gain of 57,600 in the San Francisco metro area though SF has recovered just 45.0% of the jobs lost between February and April 2020 as job gains are offset by companies moving jobs out of SF. The San Jose metro area added 39,200 jobs but by August had recovered only 55.6% of the jobs lost between February and April 2020. The Napa, Vallejo and San Rafael metro areas had the largest % job recovery by August 2021.

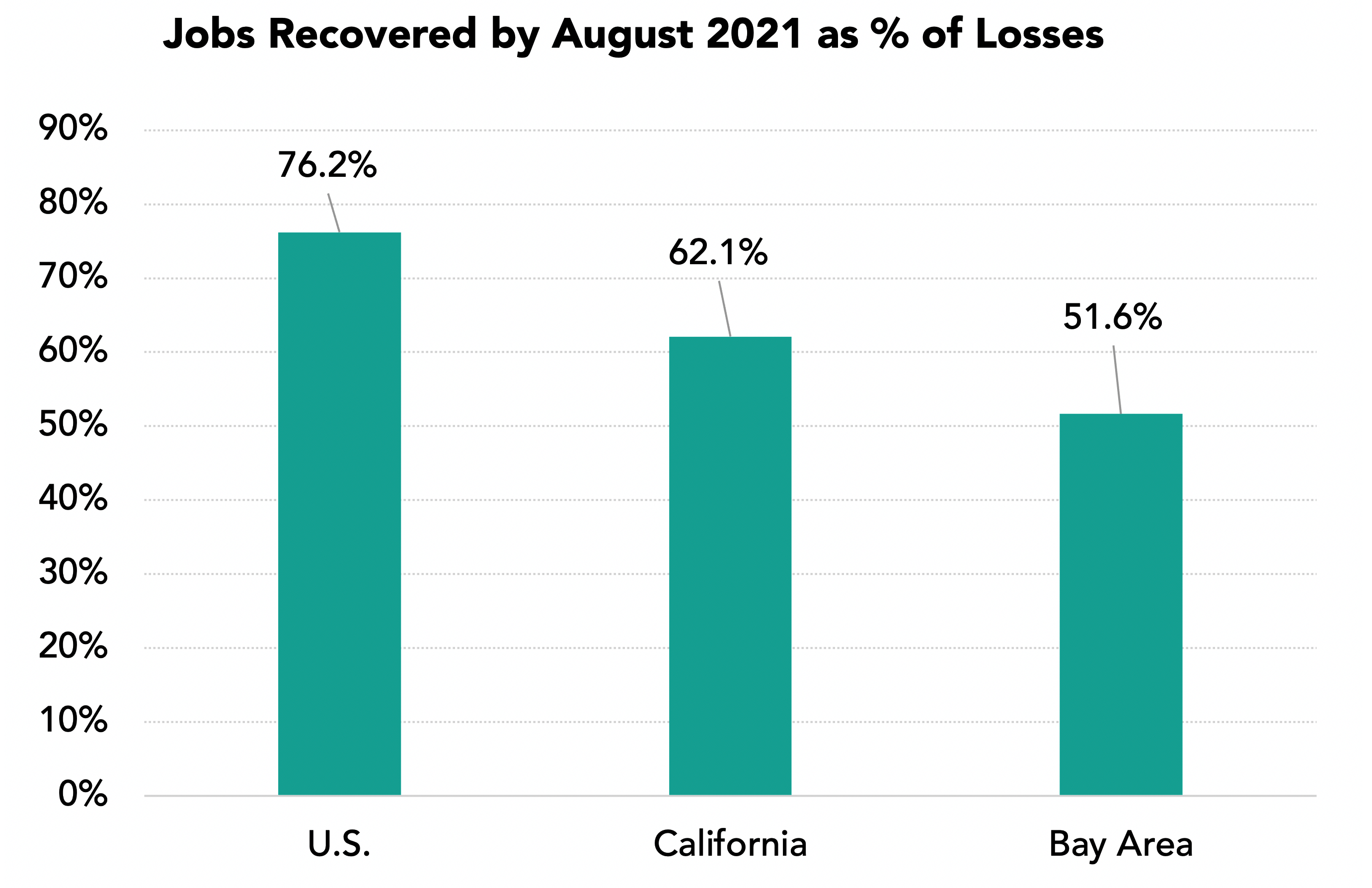

The Bay Area Had Recovered Just 51.6% of Lost Jobs by August 2021 Yet VC Funding is Surging and Tech Jobs Are Above Pre-Pandemic Levels

In August 2021 the Bay Area had recovered 51.6% of the jobs lost between February and April 2020 up from 29.4% in January. The state had recovered 62.1% up from 34.0% while the nation had recovered 76.2% of lost jobs up from 55.4%. At the same time VC funding in the first half of 2021 was $48.1 billion, the highest first half on record and 35% of a record $139 billion nationally.

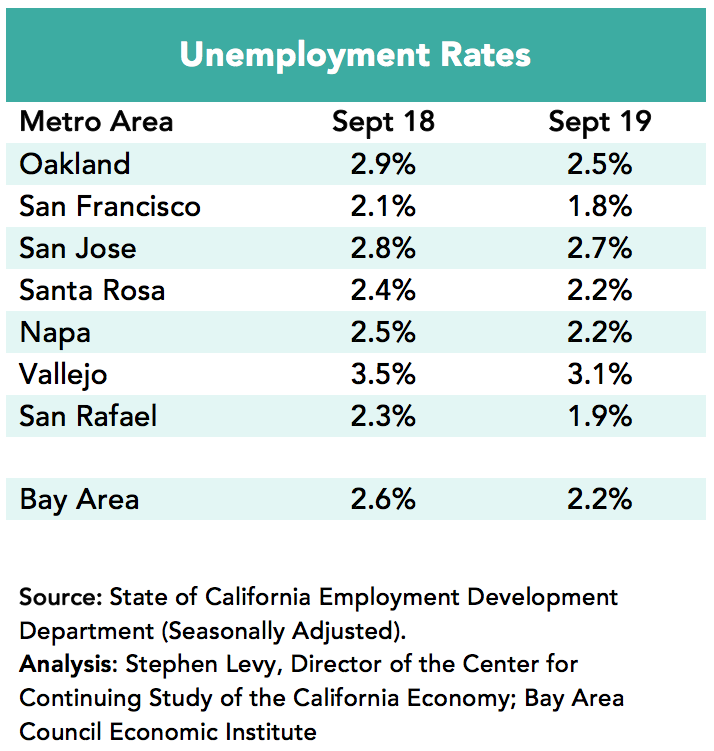

Unemployment Rates Fell to 5.5% in the Region in August 2021 from 6.6% in January 2021.

The lowest rates were in the San Rafael metro area (4.4%) followed by the San Francisco and San Jose metro areas (4.8%) in August 2021. Unemployment rates jump in the summer months and then fall in September normally. Bay area rates are well below the state 7.5% unemployment rate.

Industries Were Affected Differently

The Information sector actually added a small number of jobs compared to before the pandemic hit. And the Professional & Business Services sector has regained 94% of the lost jobs. On the other hand, the Leisure and Hospitality sector recovered only 53.1% of lost jobs by August 2021 though strong gains were posted these in the past six months. The Government sector has fewer jobs now than in April 2020 though many jobs may be returning as schools and colleges reopen. The Construction and Manufacturing sectors have recovered most of the jobs between February and April 2020.

Airline Passenger Count Up, But Still Far Behind 2019 Levels

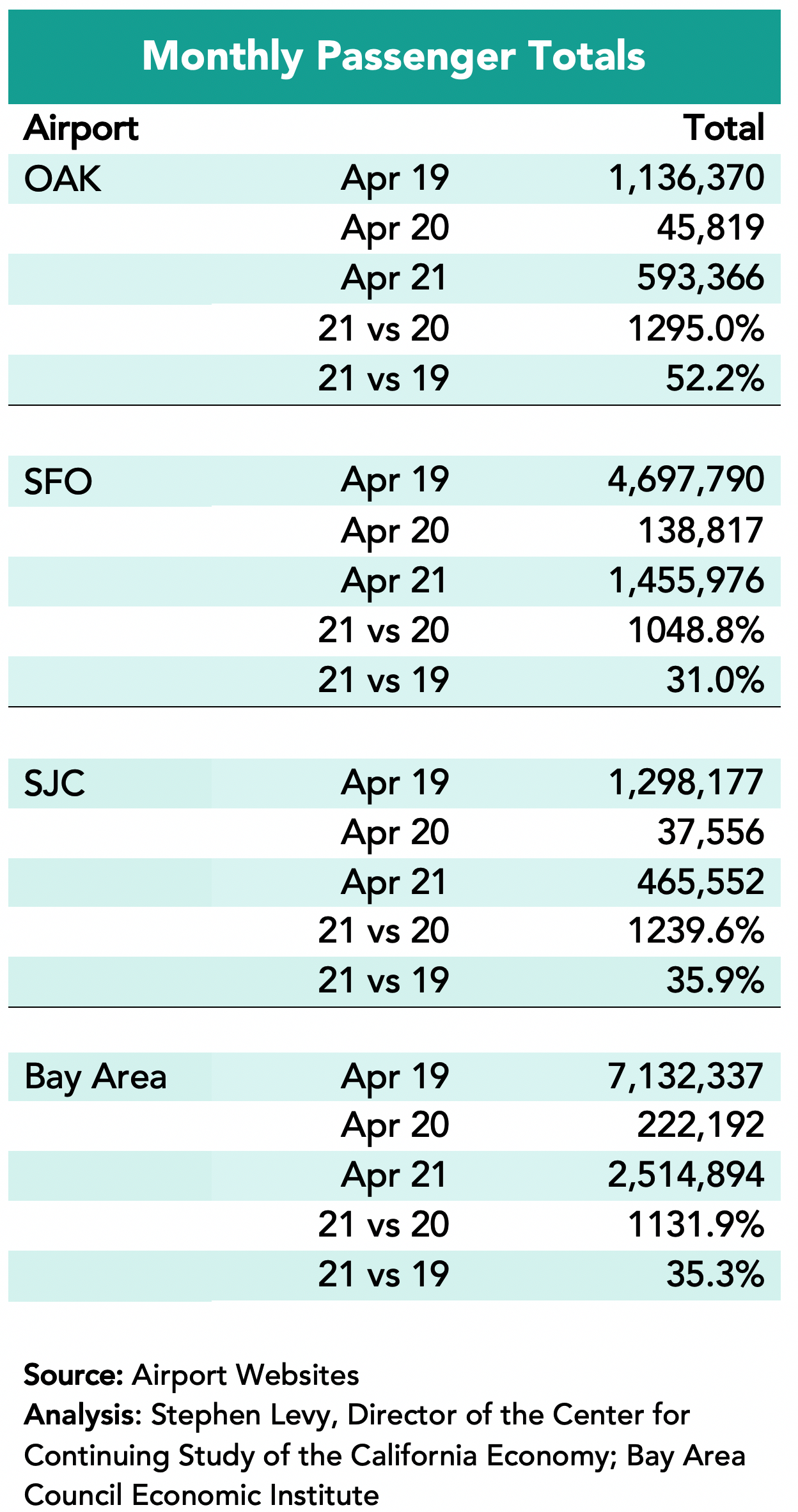

Airline passenger counts picked up in July at all Bay Area airports. However, Bay Area passenger counts in July 2021 were just over 1/2 of comparable month 2019 totals.

Housing Permits Up Over 2020 Levels, Trail 2019 Slightly

Housing permit levels are up over 2020 in the first seven months of 2021 but still slightly trail 2019 comparable months. But this month many new developments have been approved or proposed in places like Oakland and San Jose and in my neighborhood Menlo Park approved an 800-unit project and a developer proposed 500 units in Palo Alto this week.

Bay Area COVID Stats

The top eight counties in terms of vaccination percentages (all but Solano) are from the Bay Area with all having more than 70% first doses and six having more than 70% fully vaccinated. The Bay Area has by far the lowest number of new cases per capita and 8 of the 12 counties with the lowest recent per capita cases are in the Bay Area.

Large Challenges Remain:

We have the paradox of continuing reports of headquarters’ relocations outside of the region at the same the region is capturing record VC funding levels and tech jobs are slightly above pre-pandemic levels. Yet, the Bay Area Council warnings about losing our competitiveness remain as housing and mobility challenges are far from solved—the major causes of recent movements of companies and residents.

The rebound from pandemic related economic losses will continue but new policies are needed to maintain and improve the long-term competitiveness of the Bay Area economy. There is now increased movement to integrate our many transportation systems and agencies and pursue fare integration in an effort both to improve but to maintain the solvency of our main public transit options.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

On September 8, Bay Area Council Economic Institute Senior Director Sean Randolph presented the findings of the Institute’s new study on the China Greater Bay Area to an audience in the U.S. and China organized by the US-China Business Council. The forum was the first in a new series of USCBC programs that will focus on perspectives on China from U.S. states.

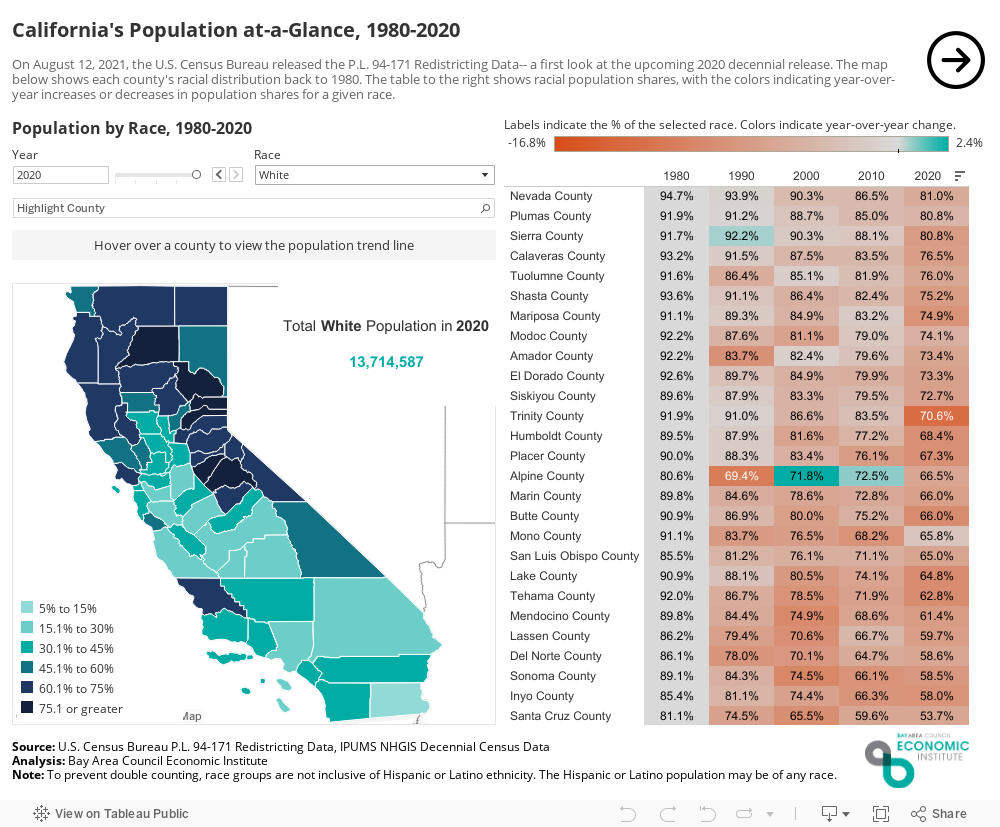

California’s population growth has been slowing, most recently leading to the loss of a congressional seat for the first time in the state’s history. This shift is nothing new, but rather part of a decades-long trend in decreasing birth rates, increasing death rates, and domestic out-migration. The state’s white population, which shrank by 8 percent from 2010 to 2020, lost 1 million people every decade since 1990. The Black population also declined slightly, largely due to decreases within the top six counties in terms of their Black population share.

Still, the state overall added 2.3 million people since 2010, mainly driven by an increase in the Hispanic or Latino population, which accounted for 69% of the state’s total population growth. In the Bay Area, only Solano and Contra Costa counties grew at a faster rate than the state (using 1980 as a baseline), due to a rise in both their Hispanic or Latino and Asian populations, and only a modest decrease in their white populations.