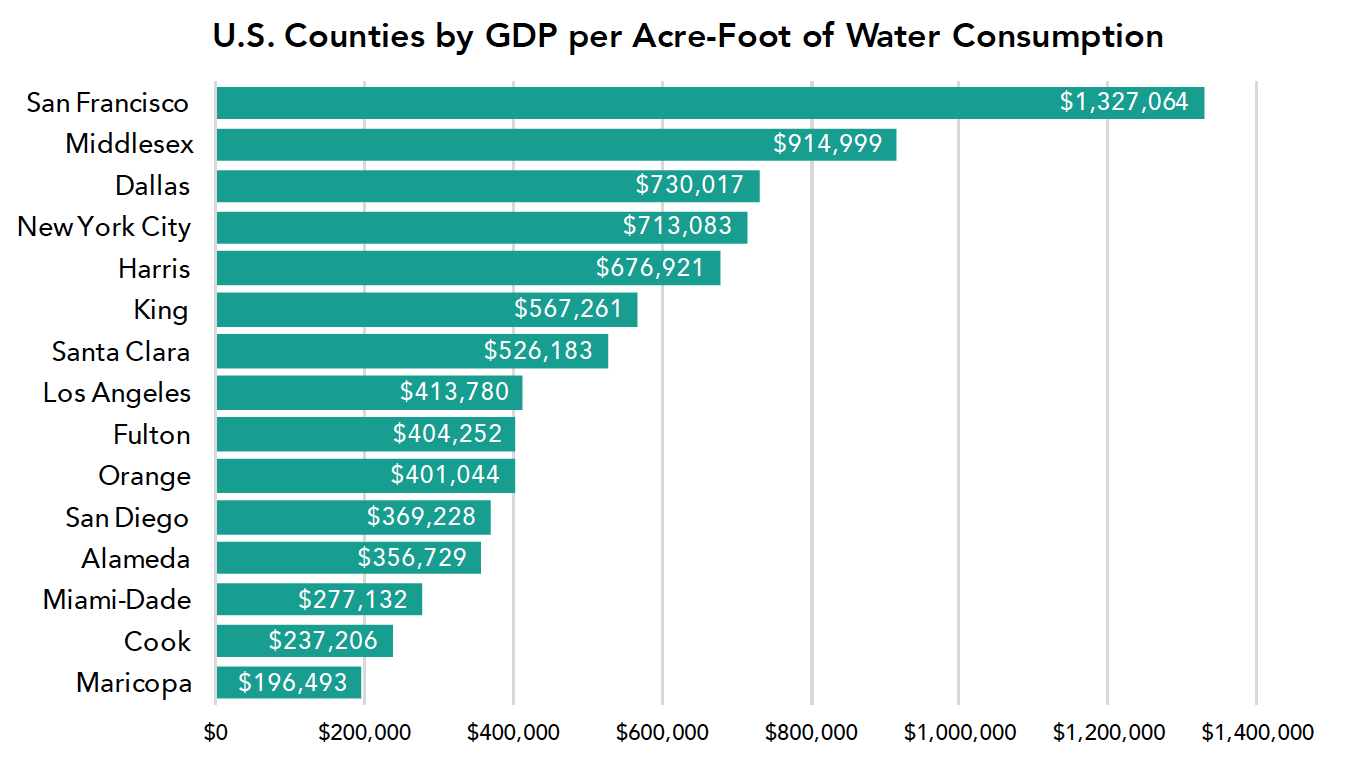

San Francisco tops U.S. counties in economic value created per unit of water consumed.

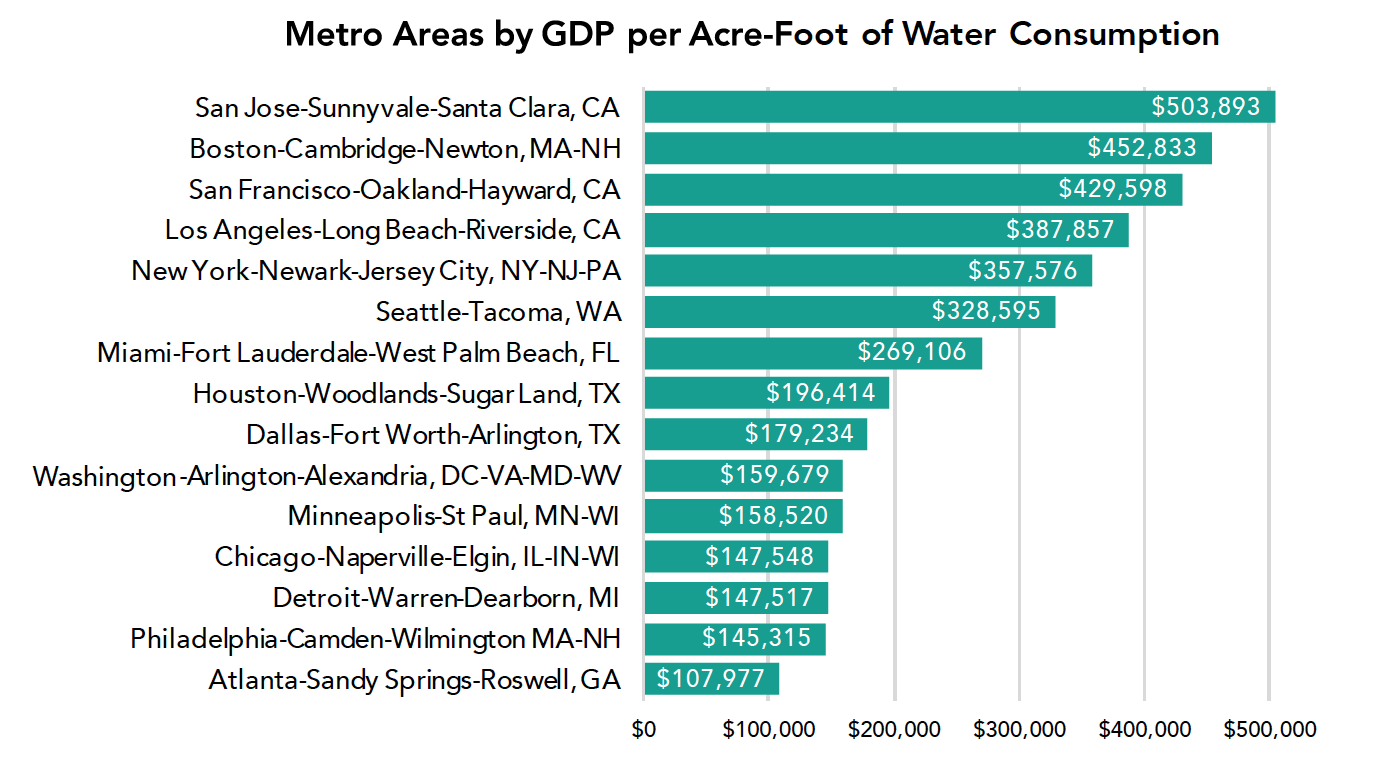

San-Jose-Sunnyvale-Santa Clara tops U.S. Metropolitan Statistical Areas in economic value created per unit of water consumed; San Francisco-Oakland-Hayward has third highest, followed by the Los-Angeles-Long Beach-Riverside area.

California’s large metropolitan regions, especially the San Francisco-Oakland-Silicon Valley Bay Area, generate more economic value per unit of freshwater consumed than other regions in the United States. The findings result from analysis done by the Bay Area Council that compared annual water consumption data among the top 15 counties and Metropolitan Statistical Areas by gross domestic product (GDP) in the United States.

San Francisco tops U.S. counties in economic value created per unit of water consumed

The City and County of San Francisco produces $1.3 million in economic value for every acre-foot of water consumed, more than any other county in the top 15 metropolitan statistical areas, and 31 percent more value than is created by the next highest value county, Middlesex, Massachusetts. One acre-foot equals 325,851 gallons, approximately the amount of water used by 11 Californians per year. San Francisco’s water efficiency can be credited to its cluster of high value professional services and technology sectors, combined with high-density land use policies which limit outdoor irrigation (which accounts for approximately half of all domestic water use in California). During water year 2016, San Francisco residents consumed 41 gallons-per-day compared to the California statewide average 82 gallons.

The San-Jose-Sunnyvale-Santa Clara Metropolitan Statistical Area tops U.S. regions in economic value created per unit of water consumed.

The San-Jose-Sunnyvale-Santa Clara Metropolitan Statistical Area produces $504,000 in economic value for every acre-foot of water it consumes. The metro area, which includes Silicon Valley, has one of the most productive economies in the United States, and consumes about 467,000 acre-feet of water per year, less than a quarter of the average across all metropolitan statistical areas (2,217,352 acre-feet).

Methodology

We examined the top 15 Metropolitan Regions, as defined by the United States Office of Management and Budget, and ranked by gross domestic product by the United States Department of Commerce Bureau of Economic Analysis. Individual county GDP figures were sourced from Moody’s Analytics.1 County water consumption was obtained from the United

States Geological Survey (USGS) data on total public supply withdrawals and self-supplied and industrial withdrawals.2 The water data represents urban water use only (all households, commercial, and industrial), and does not include water for agriculture, livestock, or grazing. Economic value per acre-foot was determined by dividing county GDP by county water use.

Notes

1. Moody’s Analytics, Economic Data: Forecast and Historical https://www.economy.com/products/data

2. United States Geological Survey. Estimated Use of Water in the United States County-Level Data for 2010. https://water.usgs.gov/watuse/data/2010/

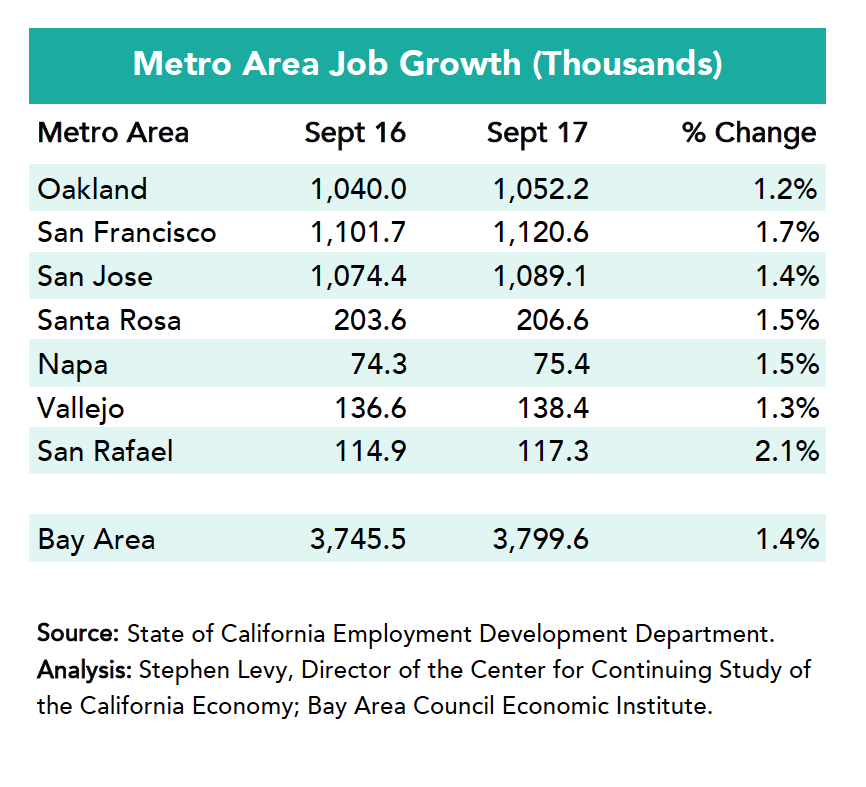

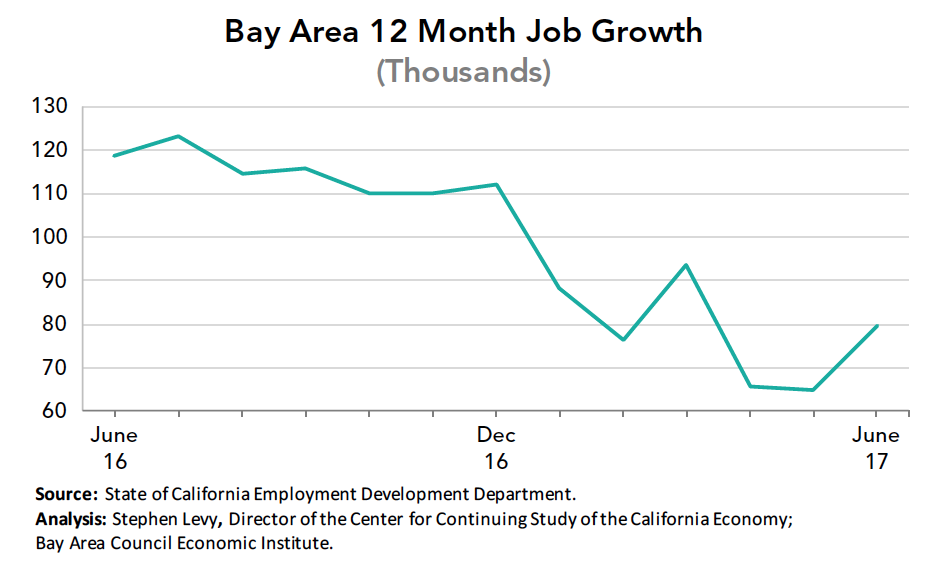

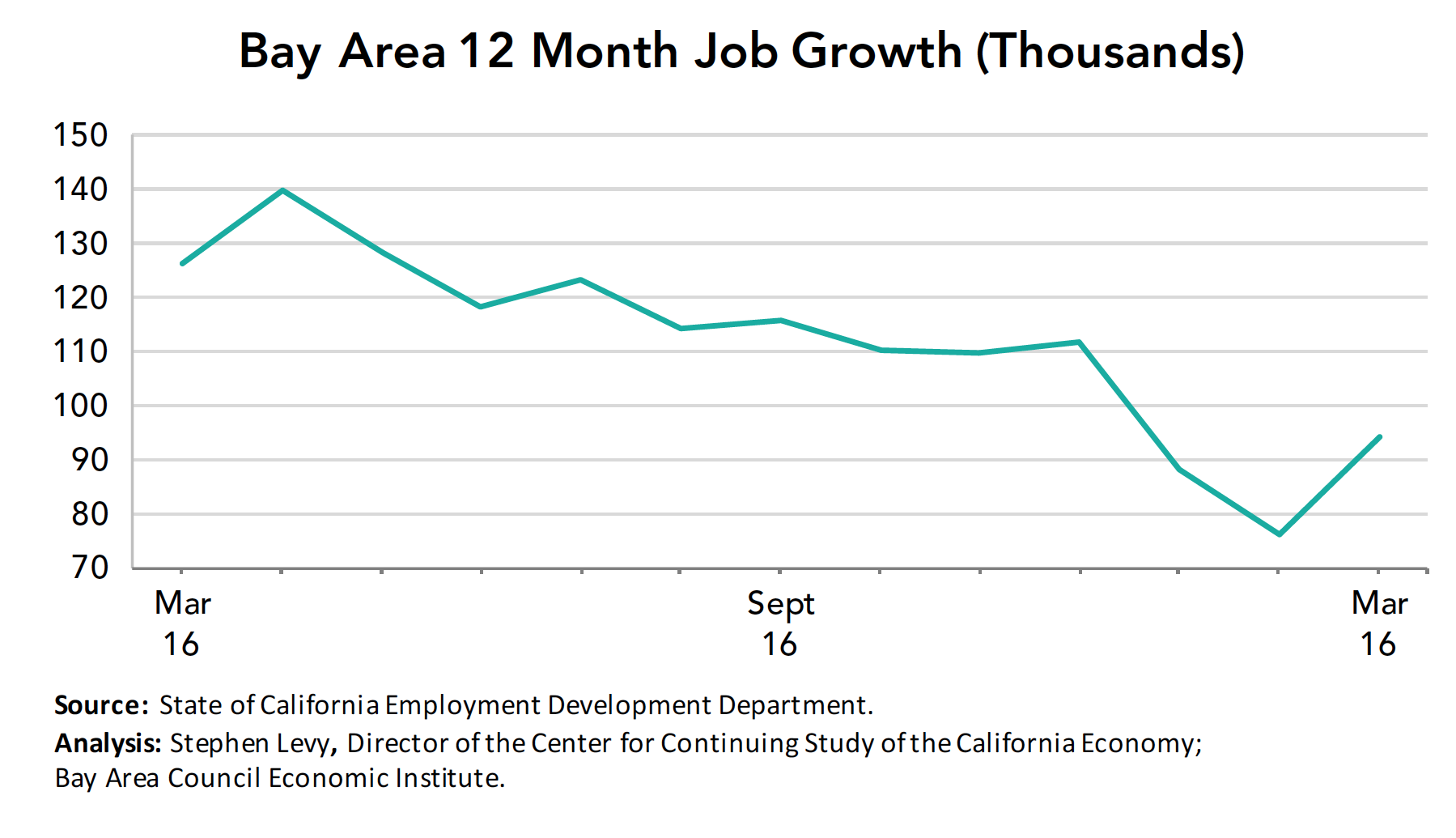

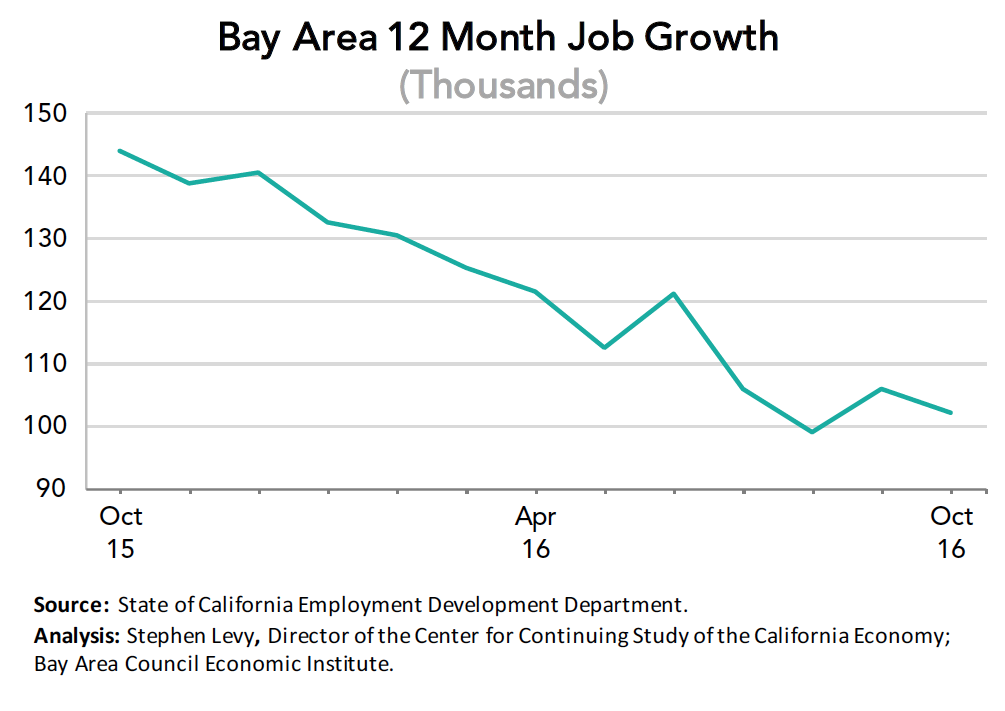

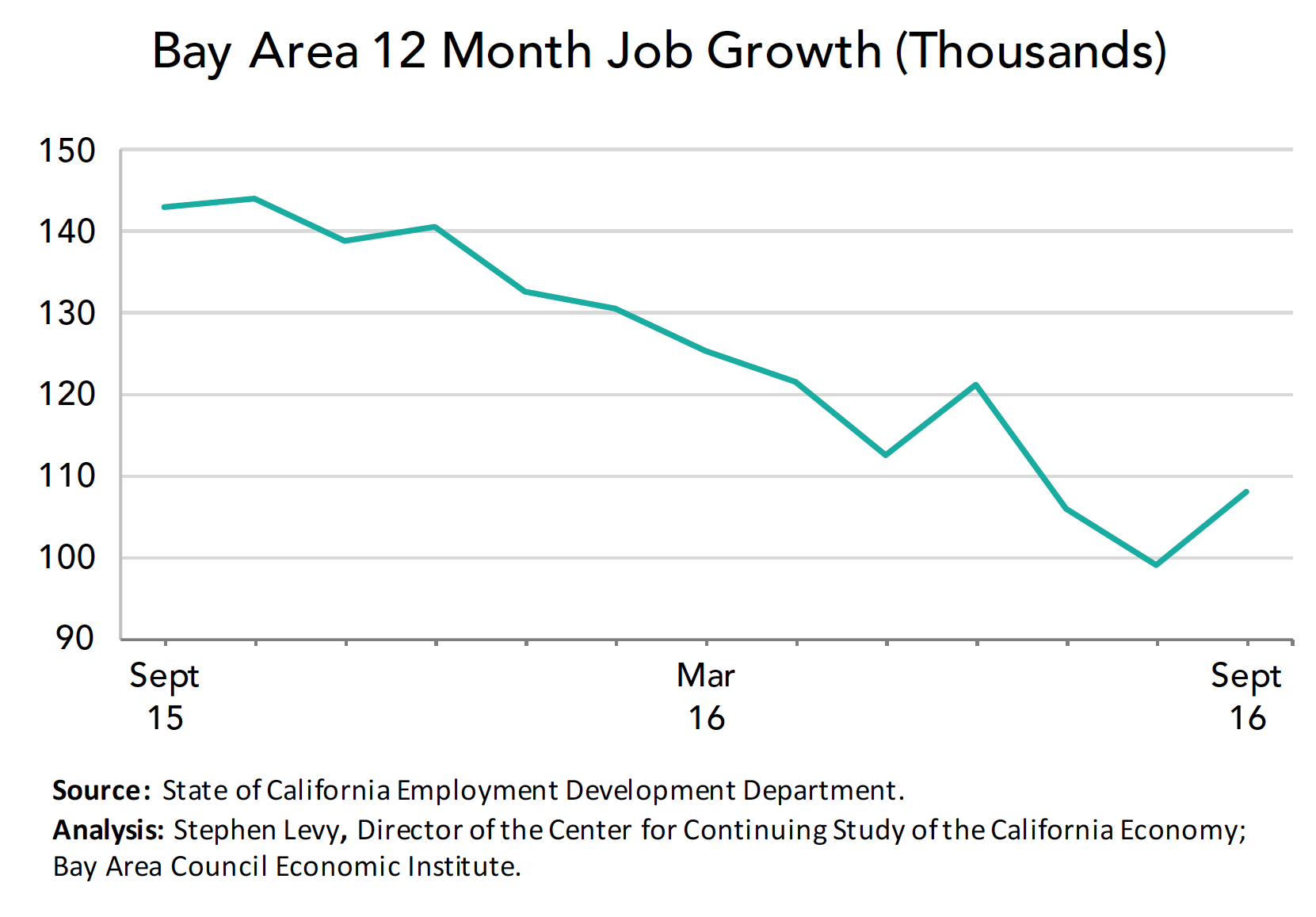

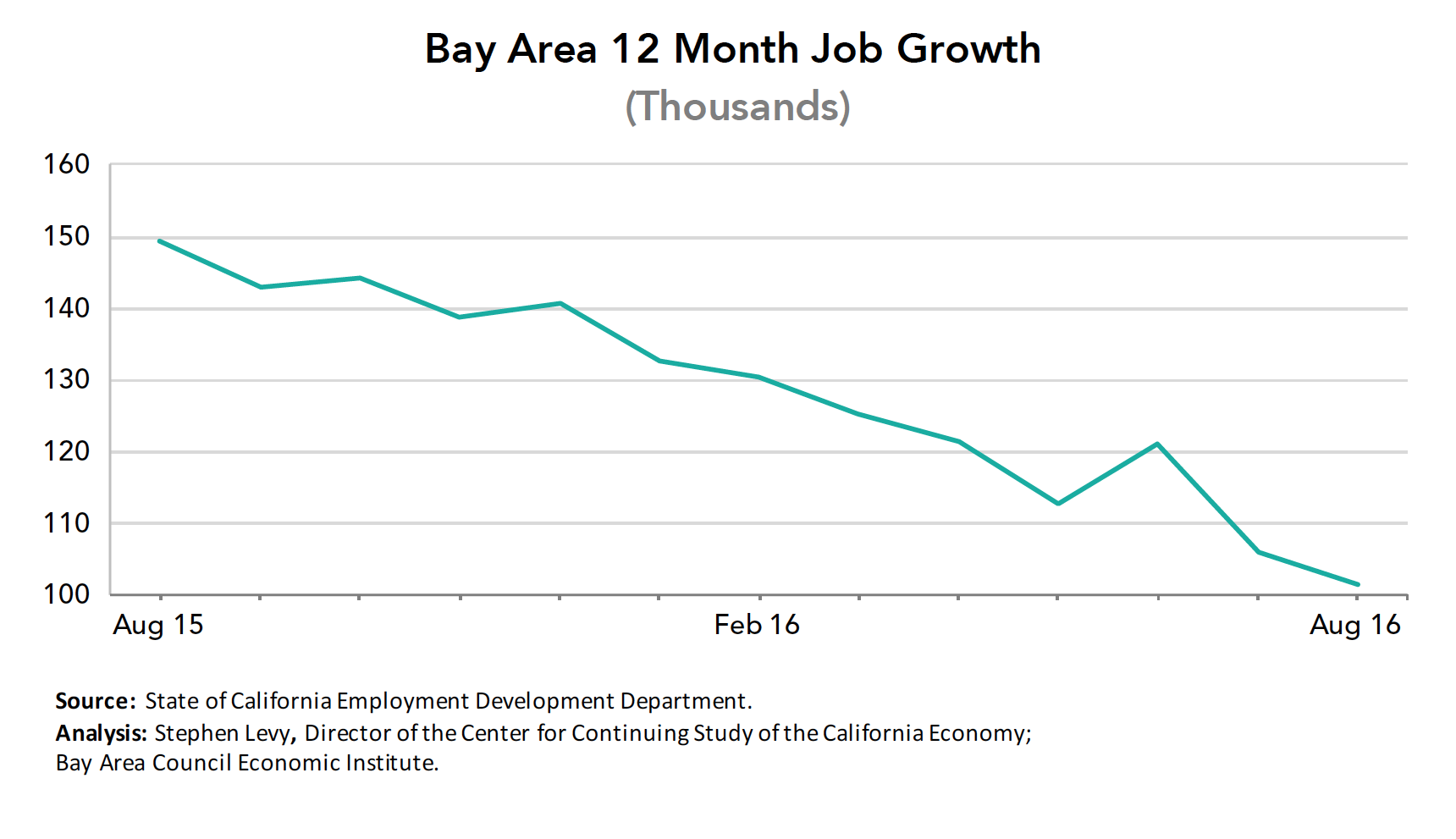

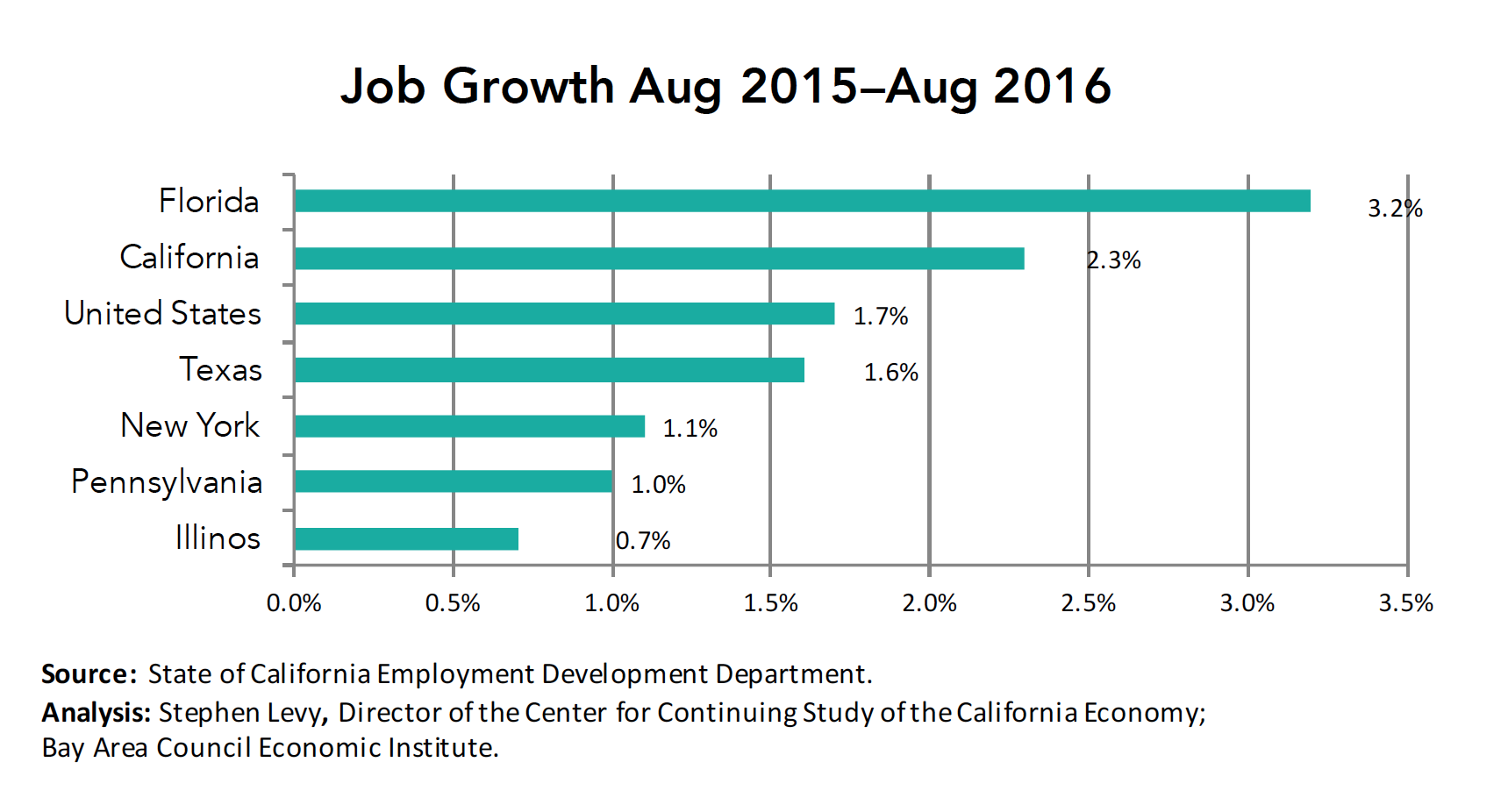

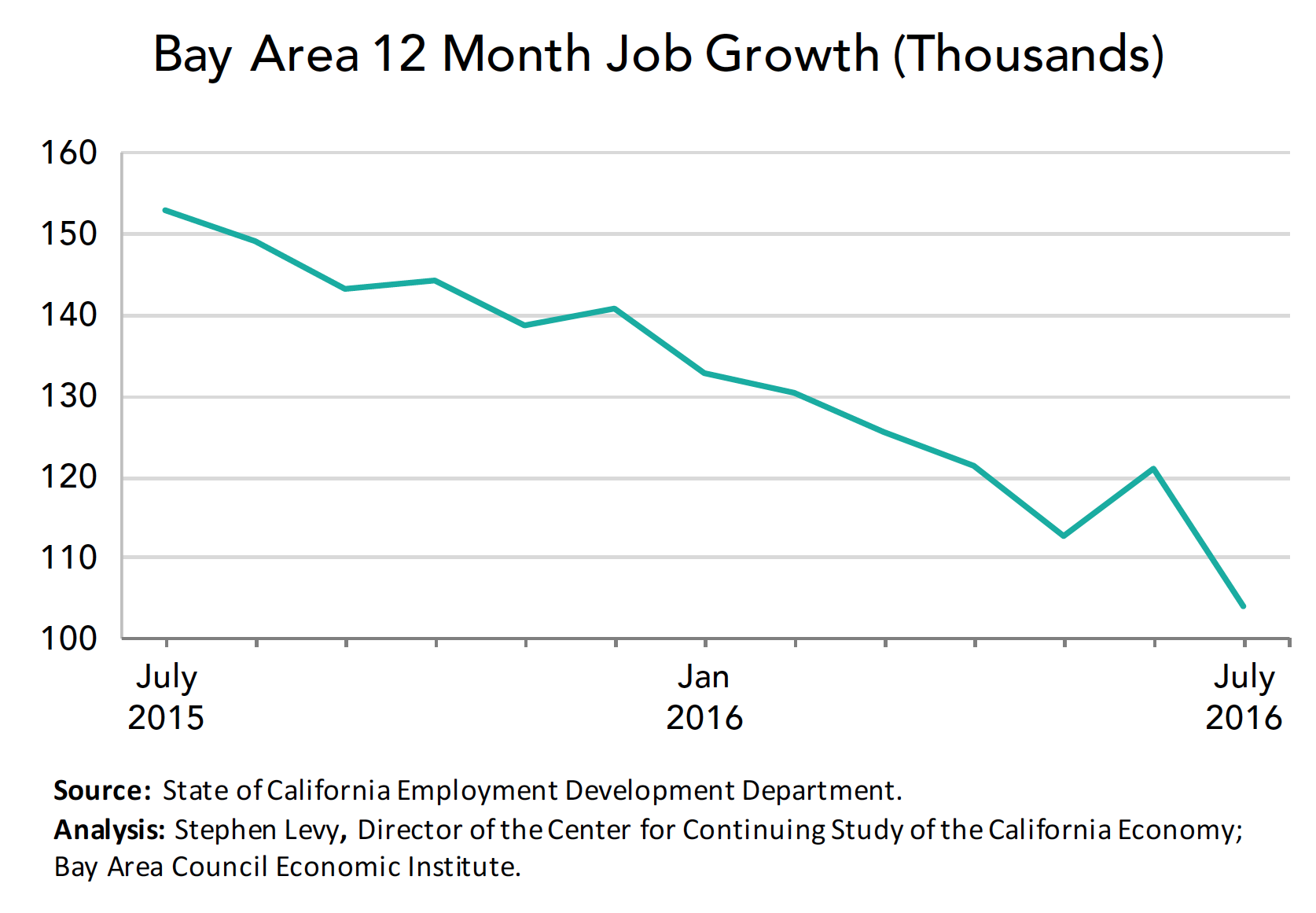

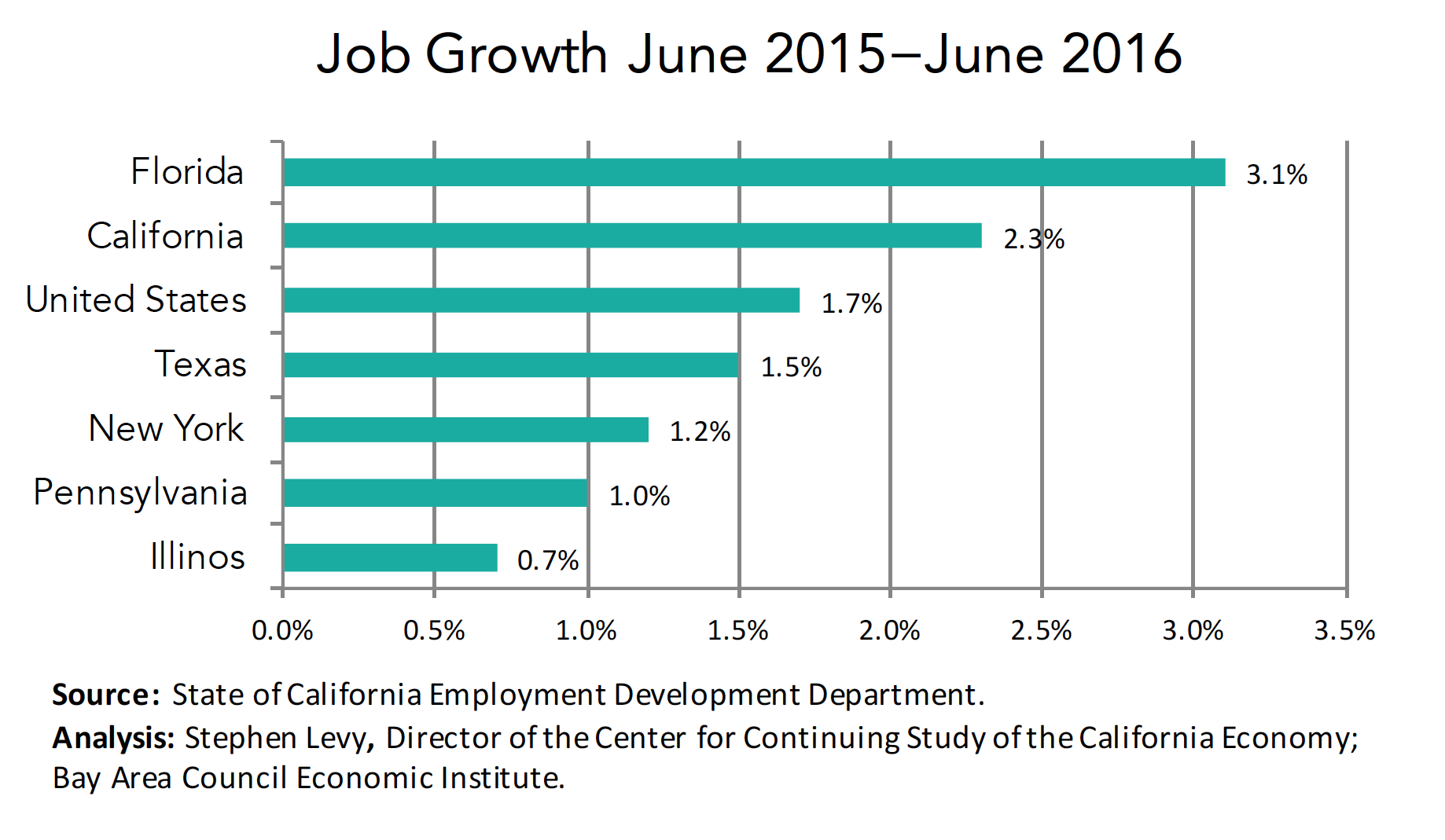

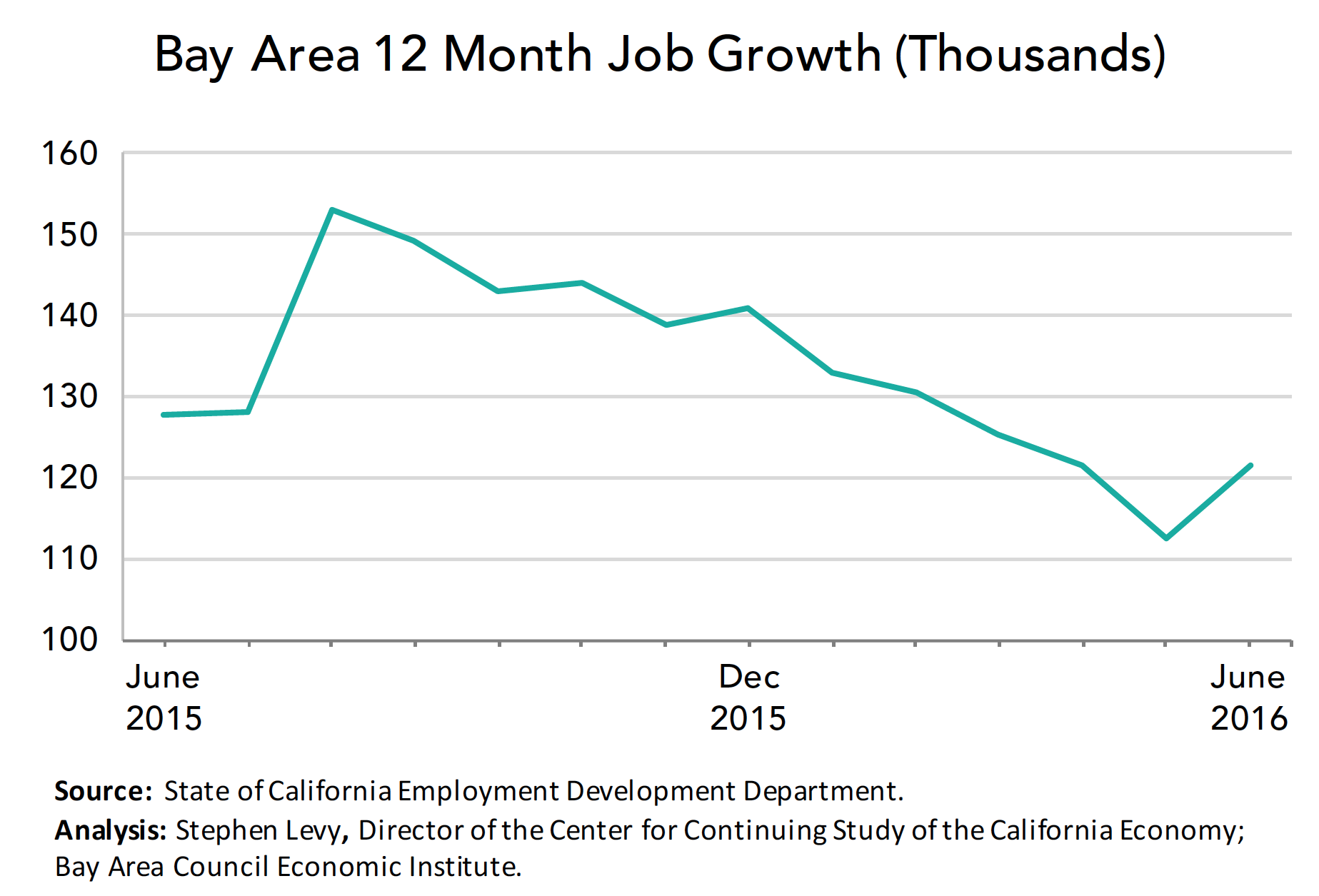

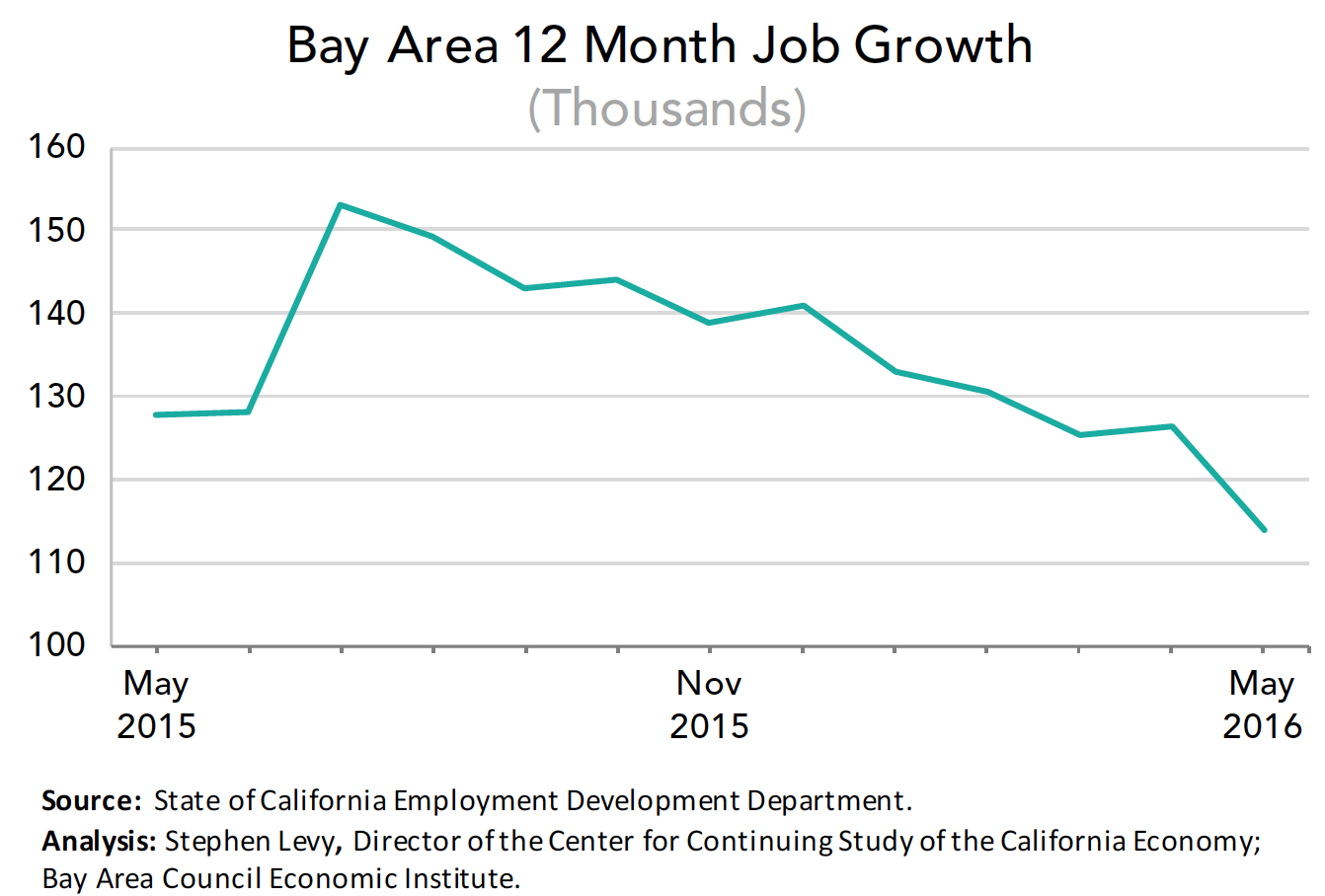

Most everyone has now read the stories about recent Bay Area job losses. It is true that job growth has slowed substantially over the past two years falling on a year over year basis by nearly two-thirds.

The Bay Area is no Longer California’s Fastest Growing Region

The Bay Area posted a 1.4% job growth rate during the past 12 months and lagged the state job growth rate for the second month in a row. The U.S. growth rate was affected last month by hurricane-related job losses.

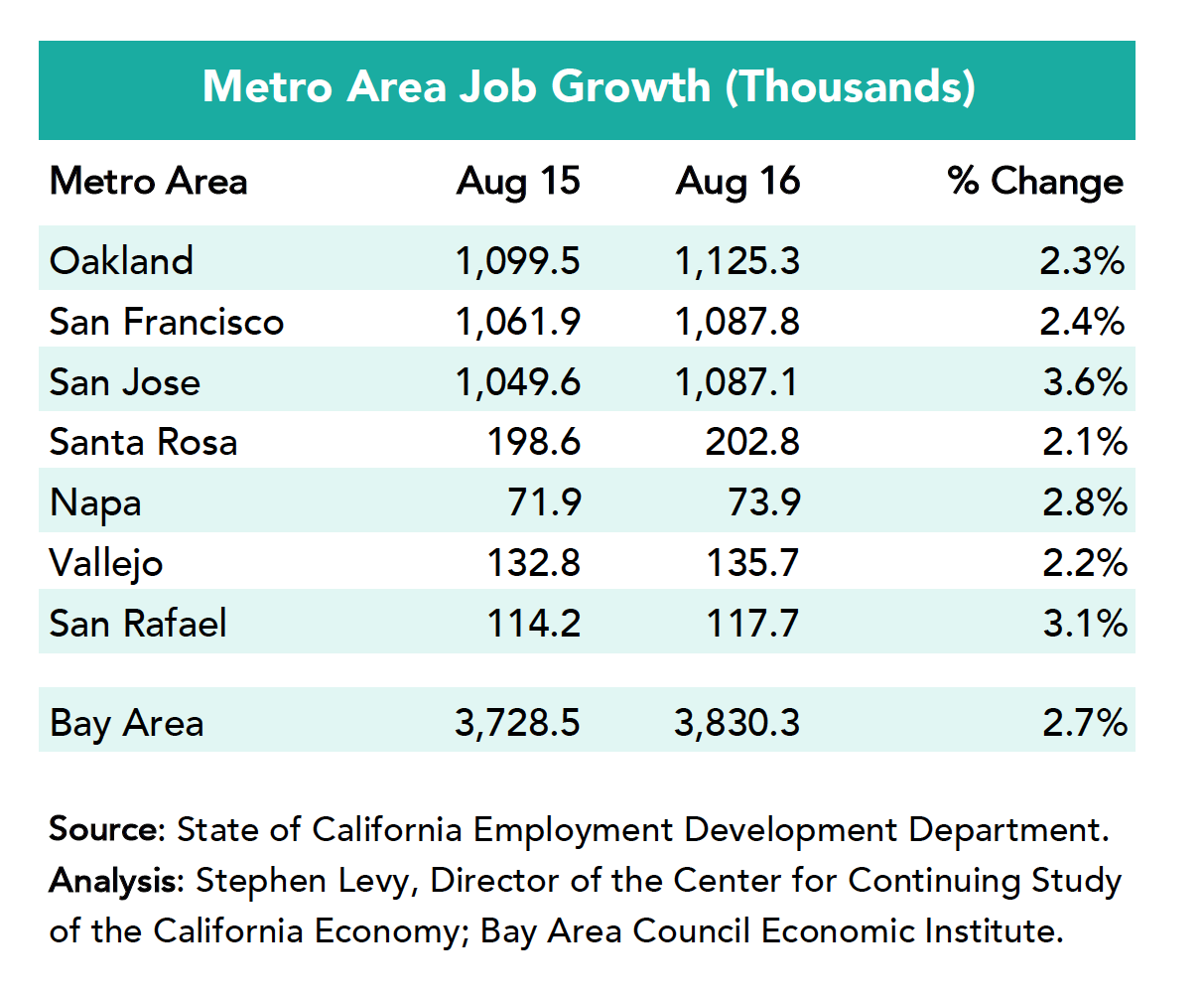

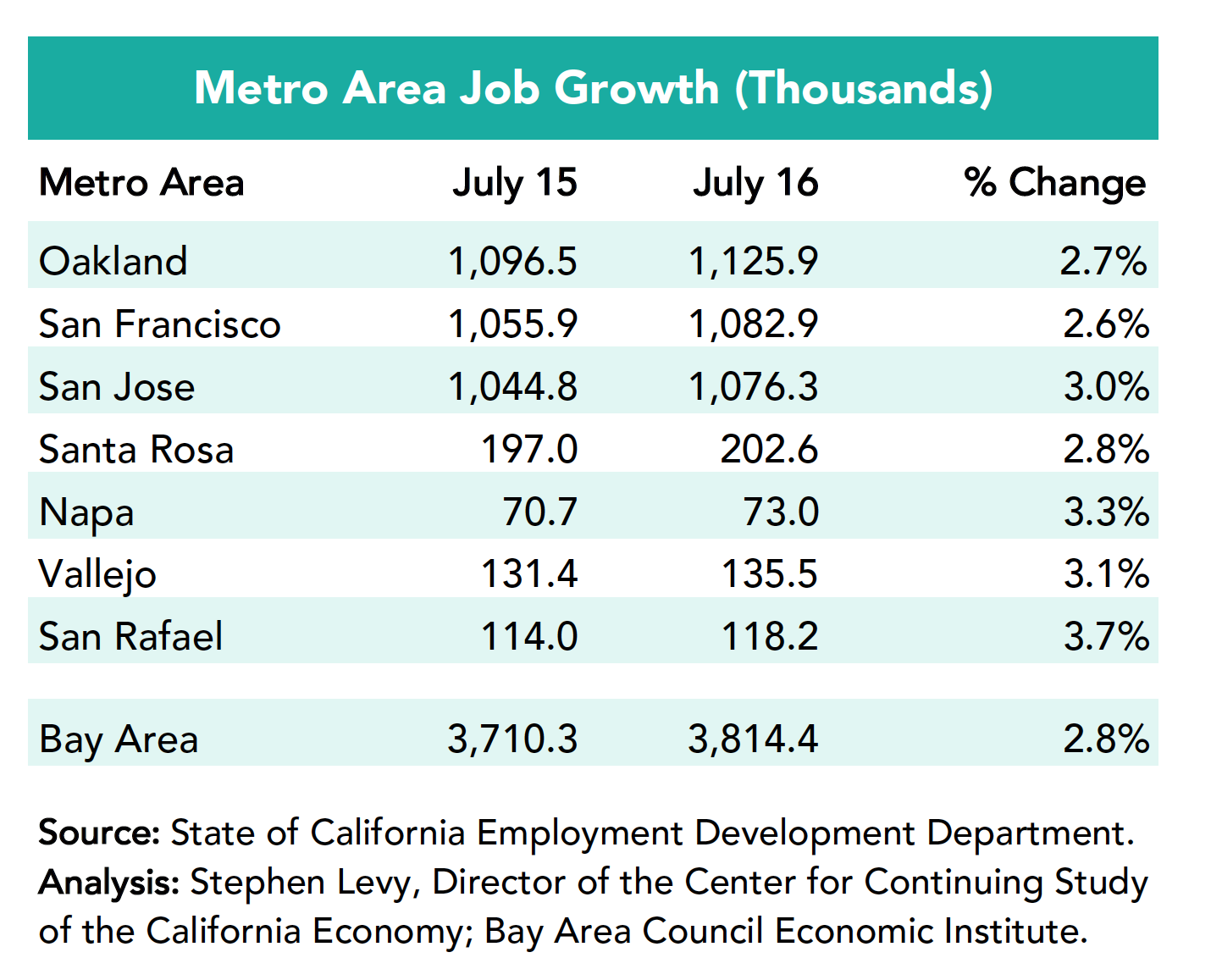

Job growth is slowing throughout the region. Year over year job growth reached a low of 55,100 in September July well below the 100,000-150,000 levels of recent years.

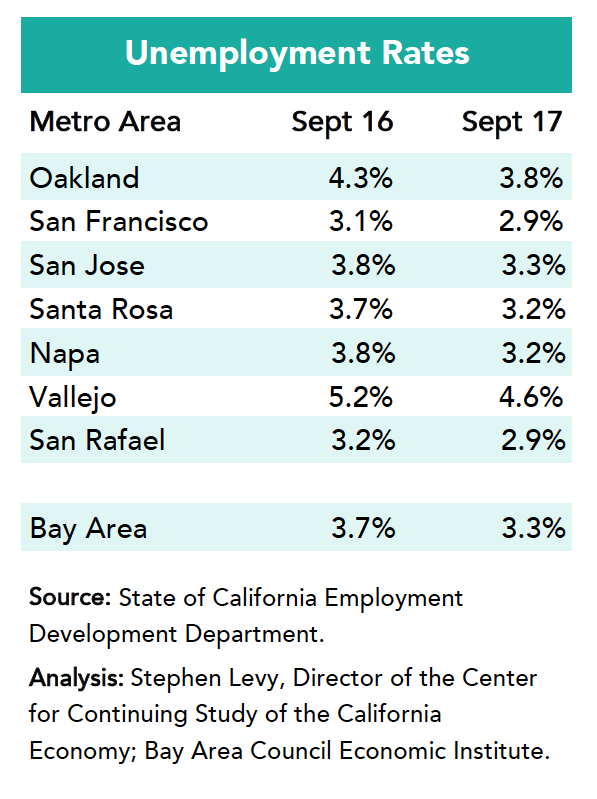

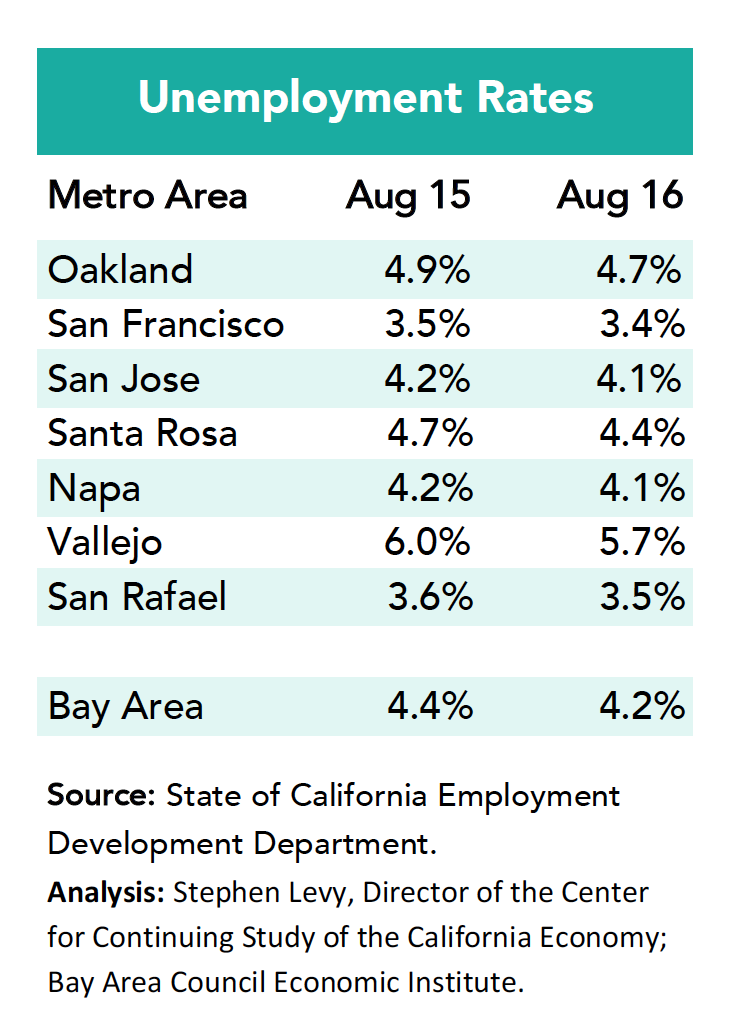

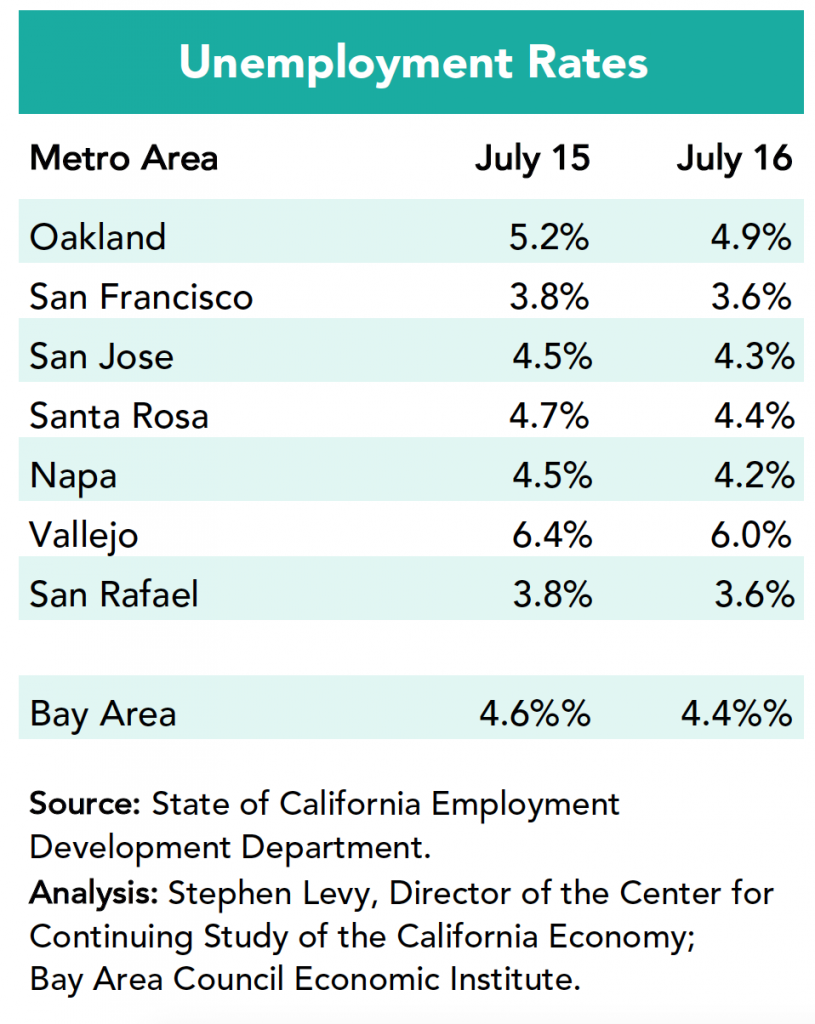

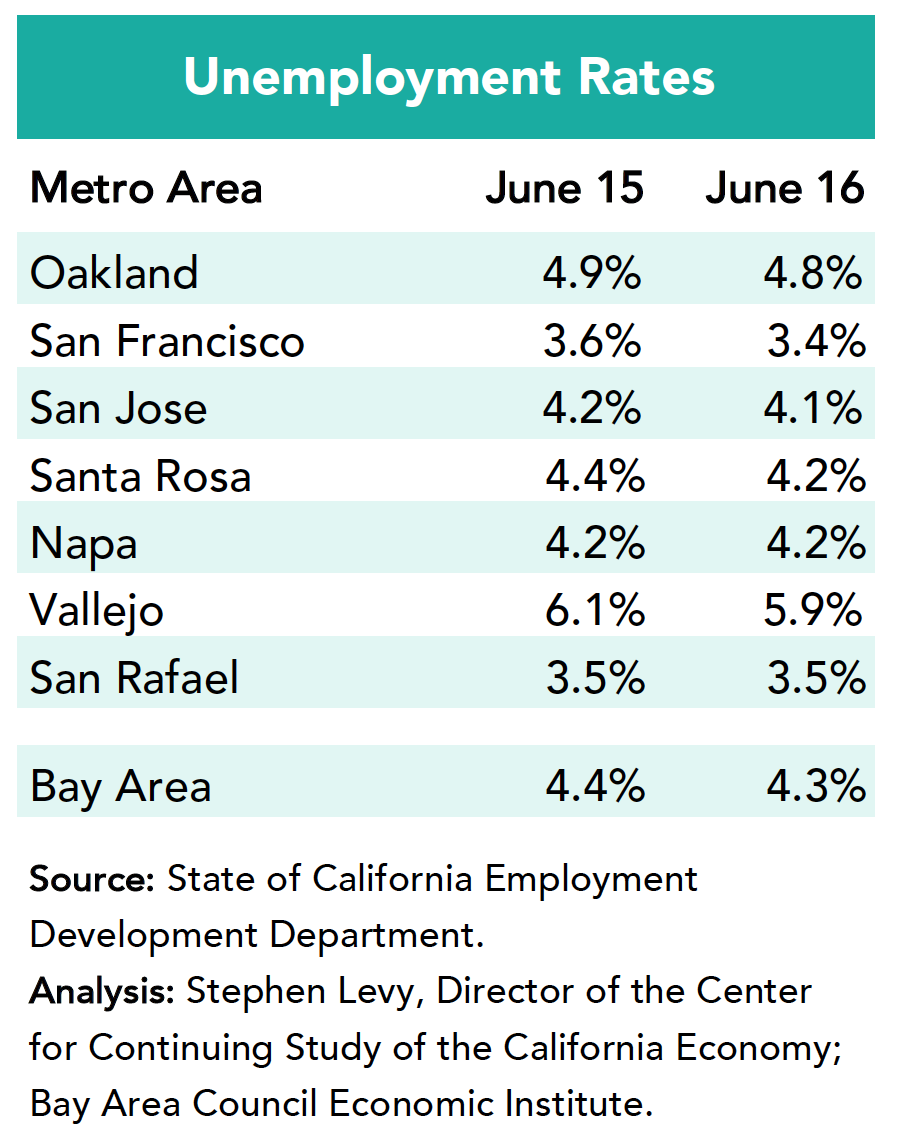

At the same time, the September data showed positive trends for labor force growth and unemployment. Unemployment rates are still falling even though rates are already low. The regional unemployment rate of 3.3% in September is the lowest since the dot.com boom. The number of unemployed residents fell from 159,500 a year ago to 145,000 last month.

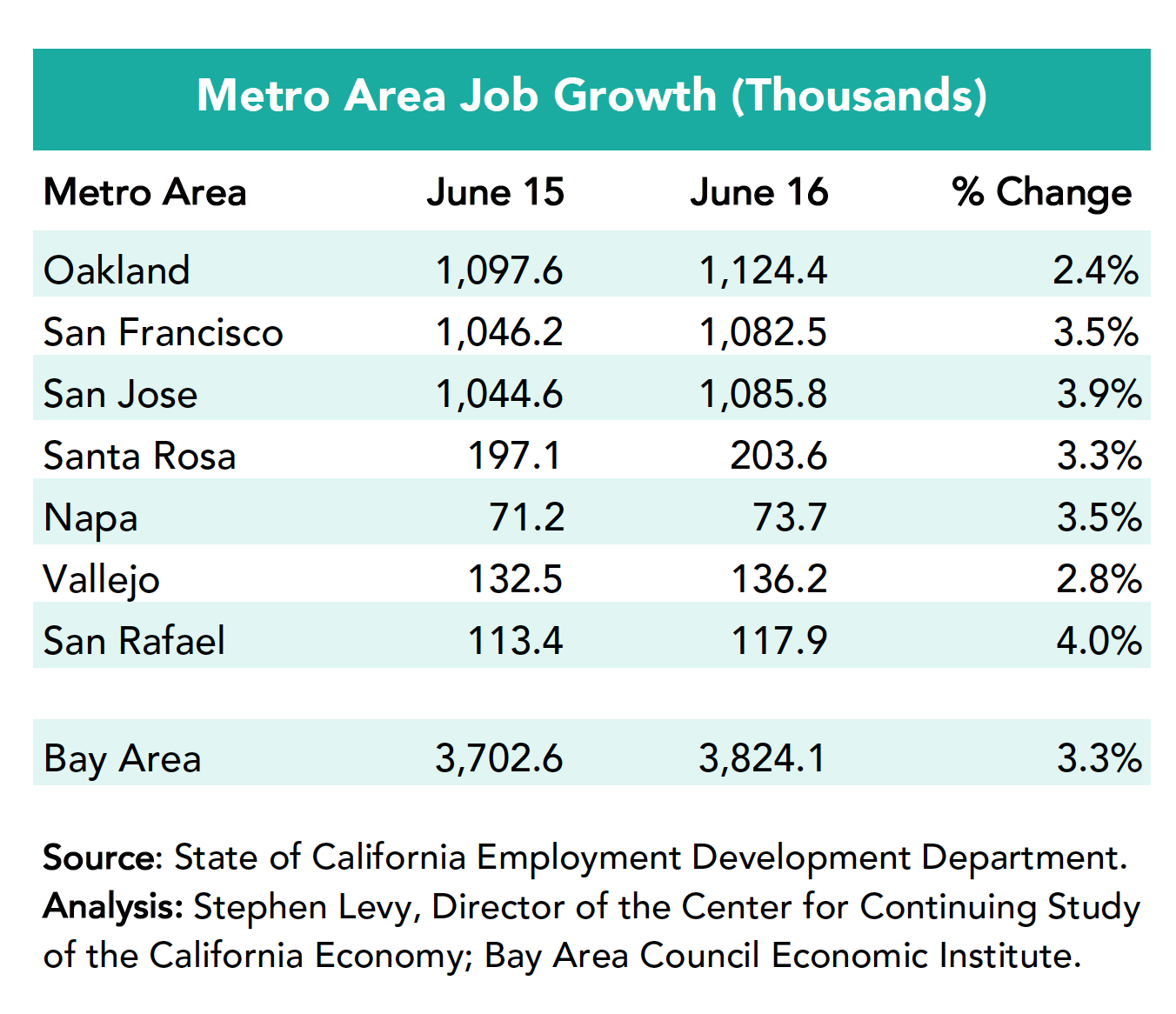

Labor force growth picked up last month and the region has added 45,000 workers (+1.1%) over the past 12 months. There are many reasons why job growth may have slowed so much. One is difficulty for workers to find housing. But there have also been a slew of layoffs resulting from consolidations. And retirements are surging as boomers are growing older.

But there are many indications that companies and communities are responding to growth challenges and planning for the future.

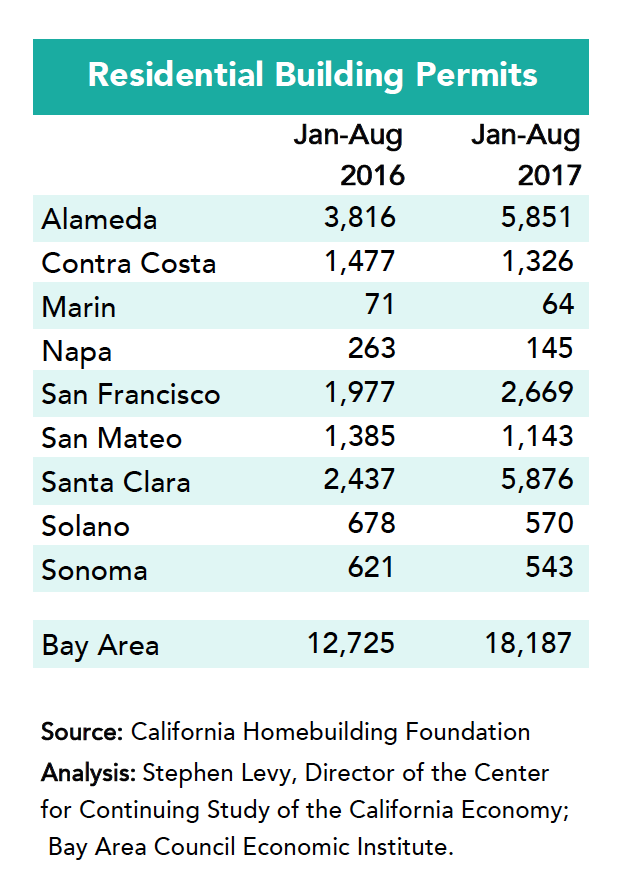

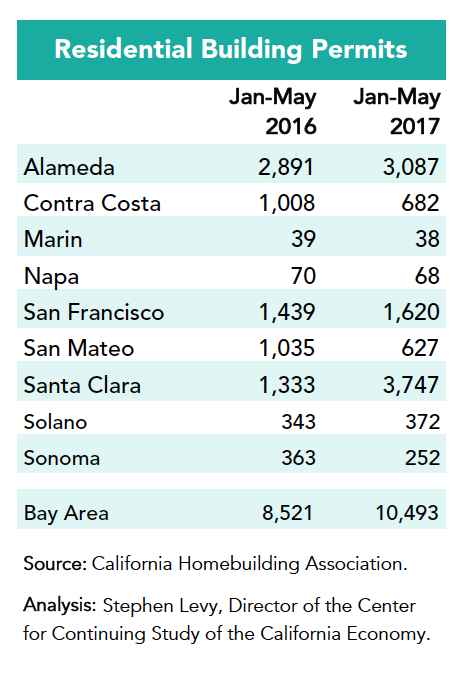

There is more positive news with regard to expanding our housing supply. Housing permits are up substantially for the first eight months of the year but more are needed. Mountain View is moving ahead with housing at North Bayshore. San Jose has bold housing proposals that coincide with the substantial Google expansions being planned. NASA is adding housing at Moffett Field. More housing is being proposed around the new BART stations and San Francisco and Oakland are moving ahead to permit more housing.

The next needed steps involve lowering the cost of building new housing, changing zoning to allow more and less expensive housing to be built and, hopefully, state funding to offset some costs of housing so that cities get the funds but some of the fees and infrastructure costs do not have to be added to the cost and price/rental rate of the new housing.

Economic Institute President Micah Weinberg, Ph.D. and Hoover Institution research fellow Lanhee J. Chen, Ph.D. co-authored an op-ed appearing on the New York Times September 19th, 2017. The piece titled “The Sanders Single-Payer Plan Is No Miracle Cure” underlines the marginal number of successful universal healthcare systems globally exposing their issues to control costs and to provide better care than systems that include private-sector insurers. The piece also examines the potential inefficiencies of Senator Sanders’ proposed single-payer healthcare bill compared to similar systems in developed nations.

In a bipartisan effort to further expose the potential inefficiencies of addressing the current complexity and concerns of healthcare in the United States with Senator Sanders’ proposal, Dr. Weinberg and Dr. Chen appeared on a segment on Fox News on September 20th, 2017. Dr. Weinberg and Dr. Chen propose a German-style insurance system as a simple, single private insurance market solution for users where insurers are regulated to produce impactful health services.

Dr. Weinberg emphasized that while the single payer bill is not the answer for the issues the nation has in regards to healthcare, the proposed Graham-Cassidy healthcare bill will generate a series of difficulties for businesses employing Americans across different states.

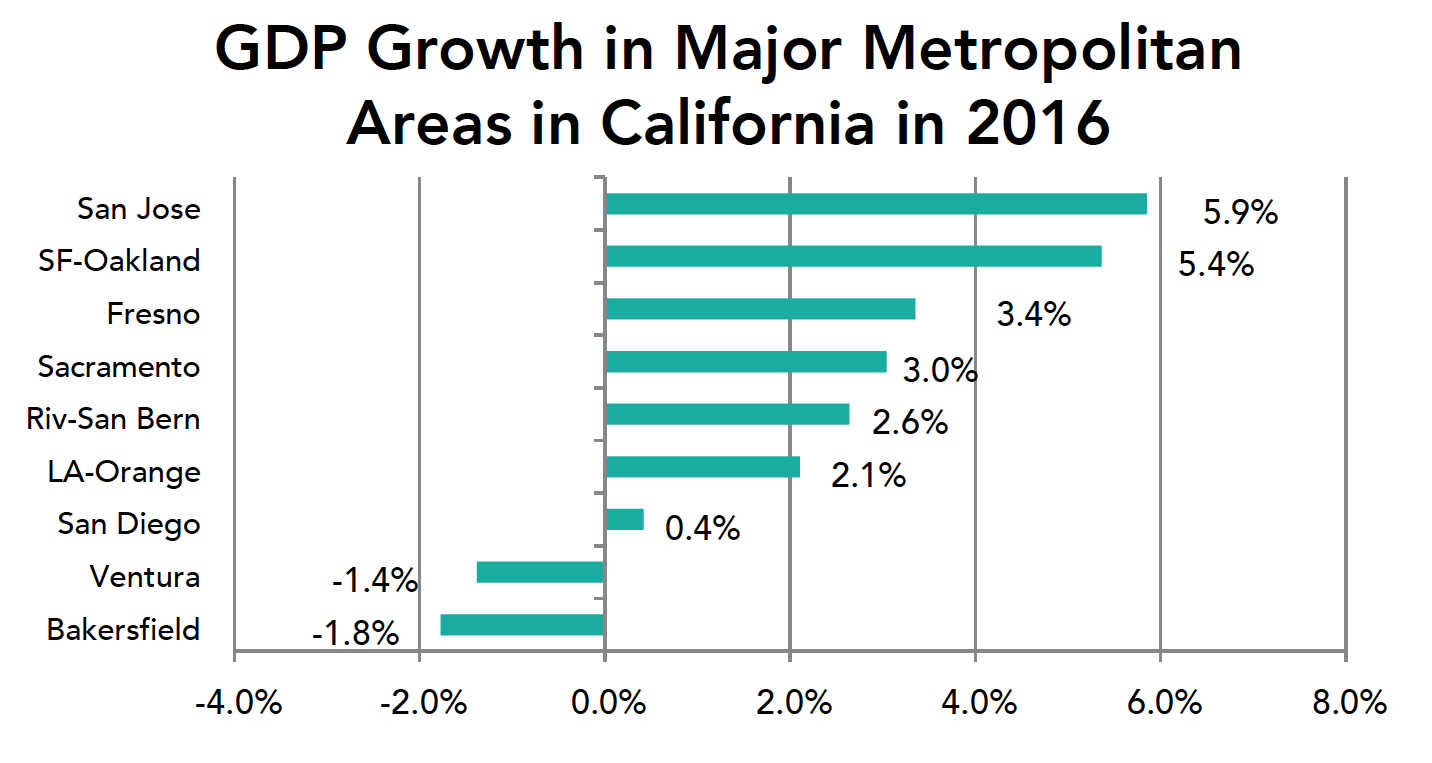

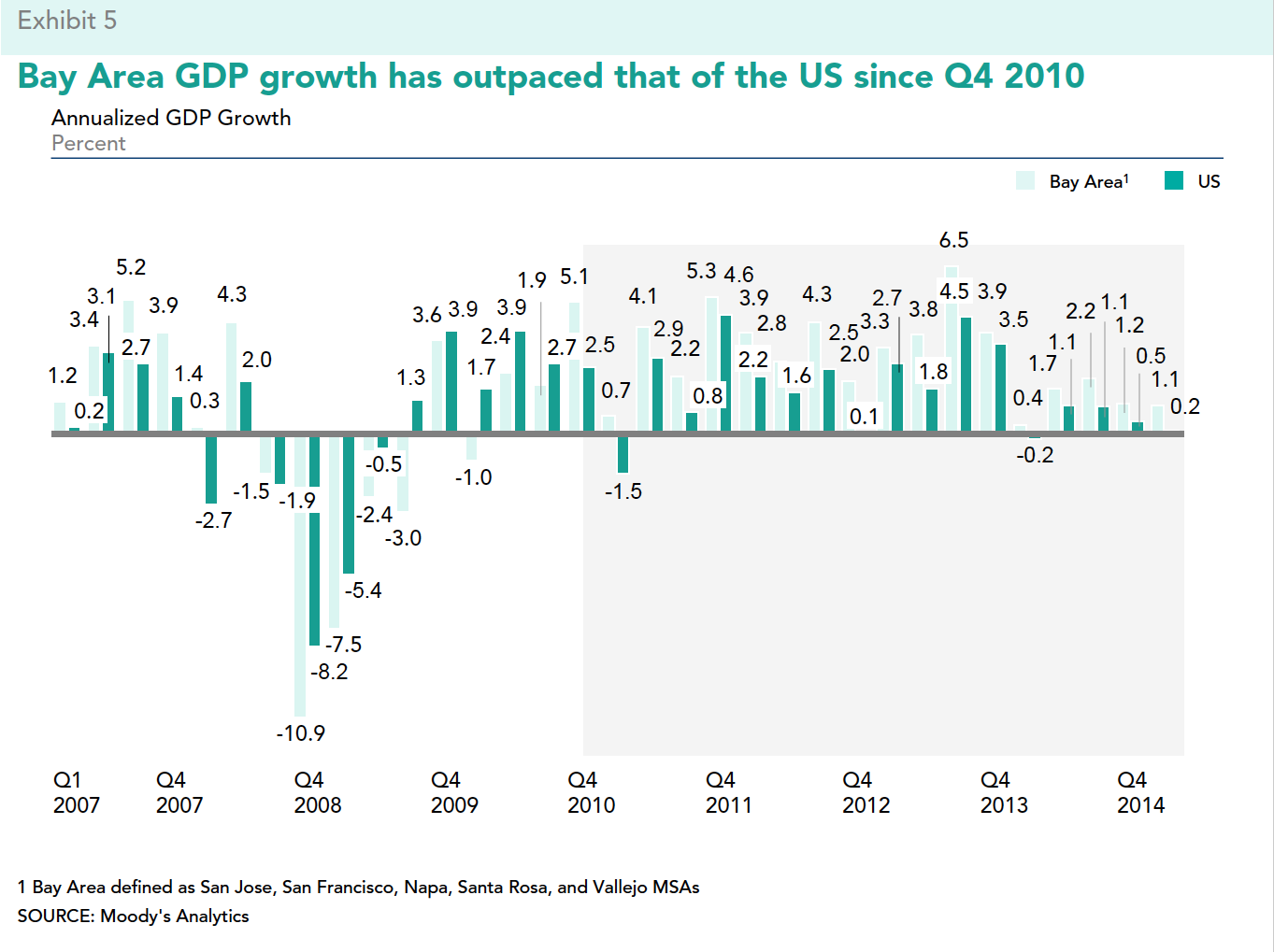

The Bay Area led California and the nation with a real (inflation-adjusted) GDP gain of 5.2% in 2016, more than 3 times faster than the national growth rate. The Sacramento region rebounded from years of slower growth to post a 3.1% real (beyond inflation) growth rate.

San Jose led all metro areas in California with a real GDP increase of 5.9% in 2016 led by gains in tech related sectors. The San Francisco-Oakland metro area was 2nd at 5.4% with gains in tech and finance.

2016 saw areas outside of the Bay Area with strong gains as these areas are now fully participating in the state’s growth. Fresno GDP grew by 3.4% led by gains in agriculture, construction, health care and government. The Bakersfield metro lagged as the oil cutbacks restrained growth.

The Sacramento metro area was led by gains in finance and professional services. The Ventura and San Diego metro areas lagged as a result of major declines in manufacturing GDP.

The Riverside-San Bernardino metro area was led by gains in construction, finance and health care that offset losses in manufacturing. The LA-Orange metro area was led by gains in information, which includes motion pictures and Internet Services.

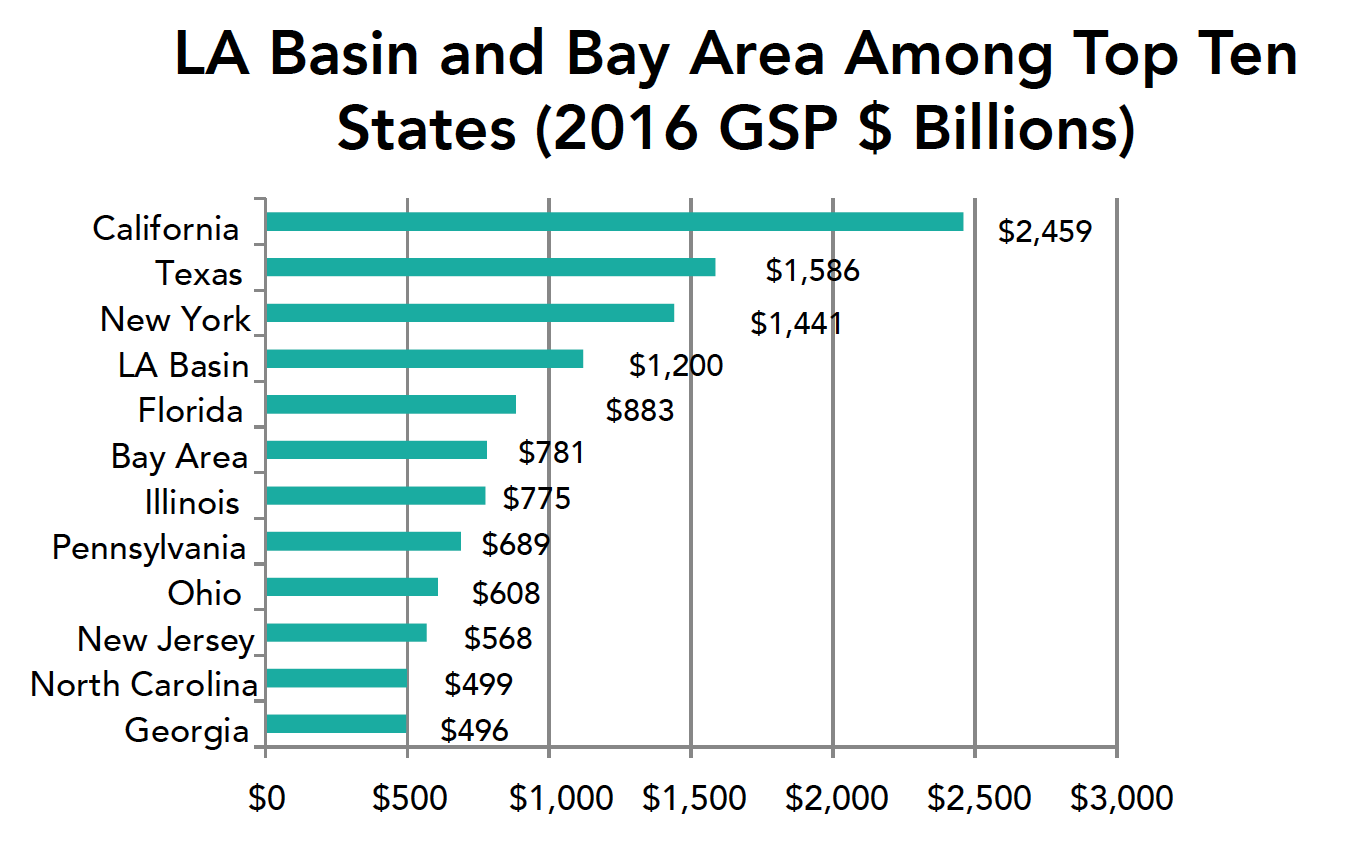

The LA Basin and Bay Area rank high in comparison to most states.

The five county LA Basin economy ranks behind only California, Texas and New York in 2016 with a $1.2 trillion dollar economy. The nine county Bay Area economy would rank 5th among all states (up from 6th last year) with a $781 billion dollar economy measured by the value of goods and services produced in each area.

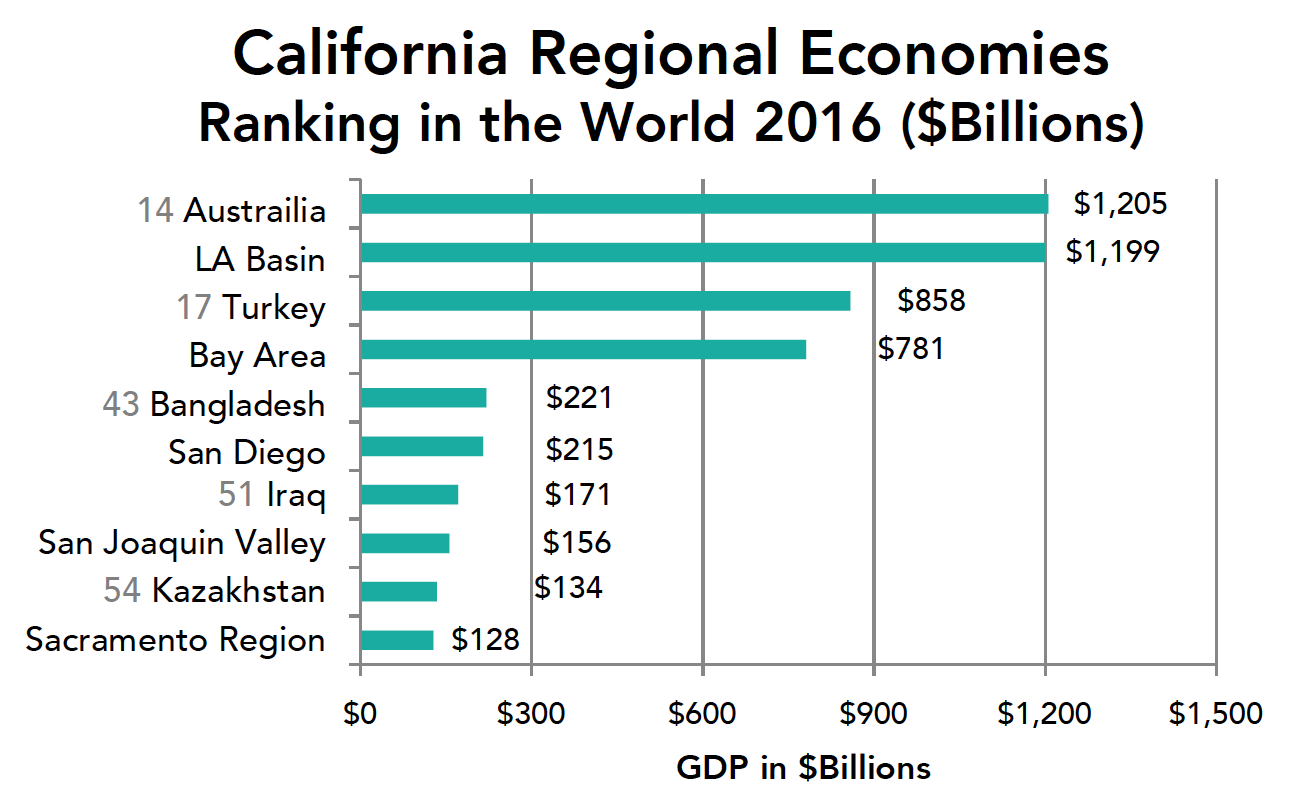

Where do California Regions Rank Worldwide?

The LA Basin economy would rank 15th (up from 16th last year) in terms of the output of goods and services behind Australia and ahead of Mexico. The Bay Area would rank 18th behind Turkey and ahead of the Netherlands. San Diego County would rank 44th behind Bangladesh and ahead of Portugal. The eight county San Joaquin Valley would rank 52nd behind Iraq and ahead of Algeria. And the six county Sacramento region would rank 55th behind Kazakhstan and ahead of Hungary. California and the regions were not counted as countries in these rankings. See the below on page 4.

2017 Update and Commentary

Job growth has slowed in the Bay Area and statewide so far in 2017. But job growth continues to spread to areas previously left behind including the Inland Empire, Butte, and many San Joaquin Valley counties.

So it is very likely that GDP growth in the state and many regions in 2017 will be below the 2015 and 2106 levels.

The recently released ACS data remind us of two important points: 1) that though poverty is falling, it remains far above the levels we hope for and 2) that in most areas of the state it is high housing costs that push a large number of residents below the poverty level and that housing remains both an economic, equity and environmental challenge that we need to meet.

Methodology

The estimates presented above are based on 2016 advance metropolitan area estimates published by BEA in September 2017.

GDP is referred to as output or the output of goods and services in the text. GDP is used instead of GSP (gross state product) although the meanings are similar).

The LA Basin includes Los Angeles, Orange, Riverside, San Bernardino and Ventura counties. The Bay Area includes Alameda, Contra Costa, Marin, Napa, San Francisco, San Mateo, Solano and Sonoma counties. The San Diego region includes San Diego County. The San Joaquin Valley region includes Fresno, Kern, Kings, Madera, Merced, San Joaquin, Stanislaus and Tulare counties, The Sacramento region includes El Dorado, Placer, Sacramento, Sutter, Yolo and Yuba counties.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

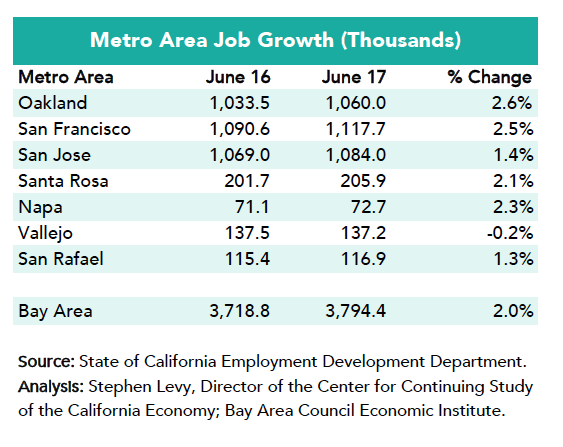

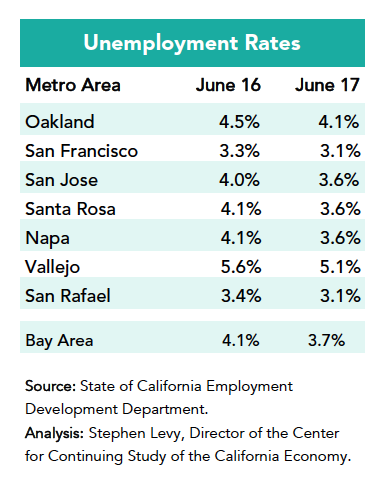

The California Employment Development Department (EDD) has released job and labor force estimates for June 2017. Here are the highlights:

Job growth in the Bay Area rebounded in June.

The region’s labor force fell over the past year with all job gains coming from a decline in the number of unemployed workers, already near record low levels.

Major companies continue to announce expansion plans, some accompanied by housing developments.

A Job Rebound Accompanied by a Shrinking Labor Force

Job growth has slowed over the past year, though June brought a strong rebound and the region again outpaces the state and nation.

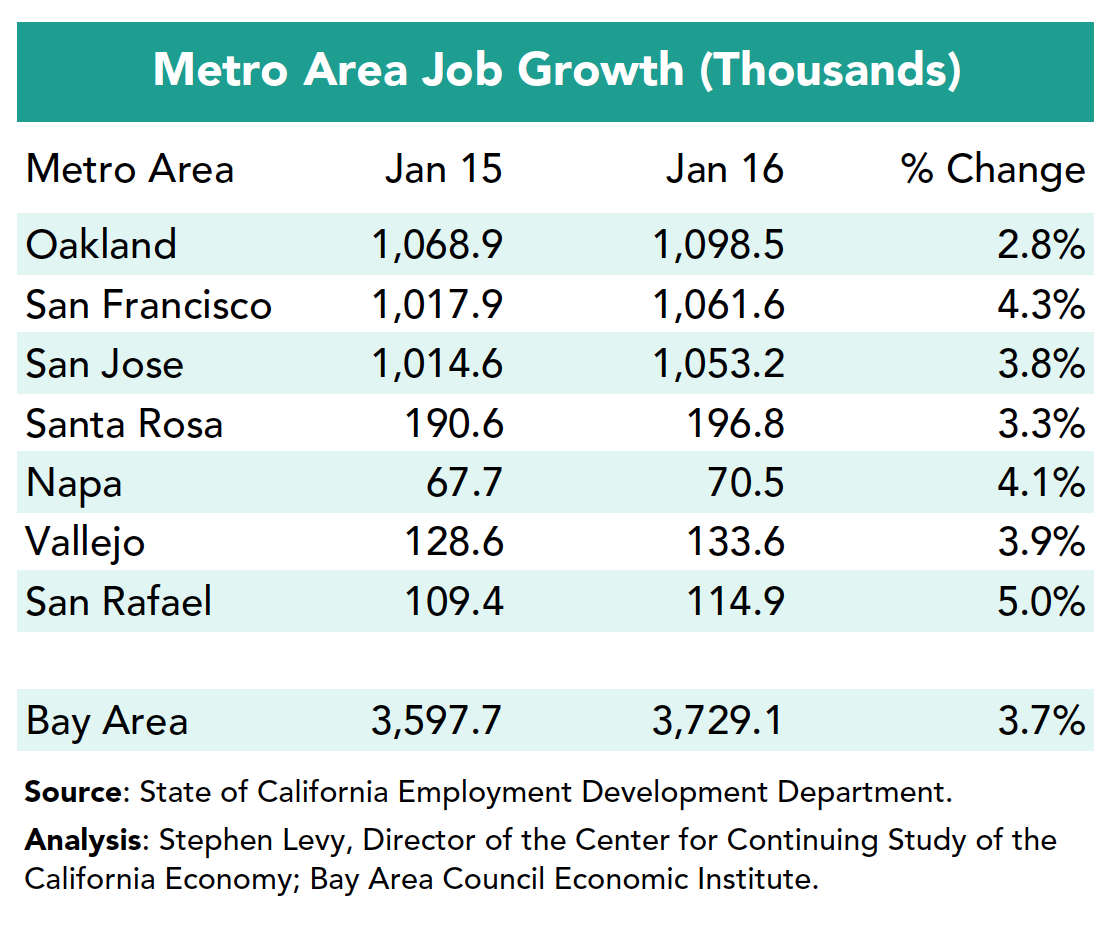

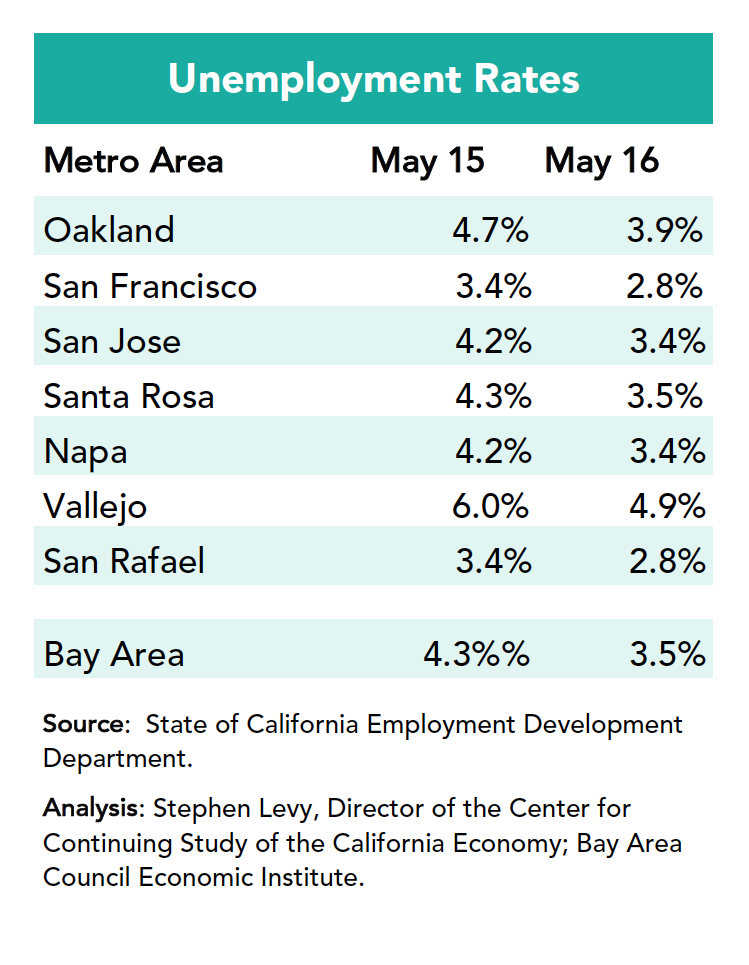

Job growth is slowing throughout the region. For the past 12 months only the Oakland, San Francisco, Santa Rosa and Napa metro areas have added jobs at a faster pace than the nation. Year over year job growth reached a low of 65,000 in May before rebounding to 79,900 in June still well below the 100,000+ levels of recent years.

At the same time unemployment rates have declined sharply throughout the region to the lowest levels since the dot.com boom. The June rates are higher than normal as a result of school closings for the summer but the year over year trends show the continuing decline.

While unemployment and unemployment rates have declined, labor force growth has shrunk with 9,700 fewer workers than a year ago. This has created a very tight labor market where finding workers has become more difficult. Job growth cannot continue without positive labor force growth, which is tied to the region’s efforts to provide more housing at a range of affordability.

Job growth levels have declined sharply since last June from near 130,000 on a year over year basis to roughly half that level before rebounding a bit in June.

But this week alone has brought positive signs for the region’s future.

Facebook announced expansion plans in Menlo Park including plans for housing and community amenities. Adobe announced plans for expansion in San Jose. San Francisco adopted a number of pro housing initiatives and approvals. South Bay communities are pursuing mixed use projects around BART stations. The state legislature will look at several housing proposals in August.

Housing permits are up for the first part of the year but more are needed.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

Last Tuesday, Economic Institute Vice President Jeff Bellisario joined by Oakland Athletics’ President Dave Kaval discussed the findings of a new Institute report on the economic impact of building a new Stadium in Oakland. The study found that over the first 10 years of operation a new baseball stadium for the Oakland Athletics would generate $3.05 billion in economic impact for the residents and businesses of the city. Building the stadium would also create 2,000 construction jobs, many of which would go to local workers and businesses under hiring agreements expected to accompany the project. The analysis breaks down the economic impact of the new stadium as follows:

$768 million from construction and related spending

$1.54 billion from game-day spending

$742 million from ballpark operations

While the location of the new stadium has not been specified, the study estimates a new stadium could increase attendance from 1.5 million (2016) to 2.55 million in its first year of operation.

This Monday, Economic Institute President Micah Weinberg discussed the importance of preserving open space in the Bay Area while addressing the housing challenges the region faces at Greenbelt Alliance’s board of director’s meeting. The conversation suggests that the Bay Area can make progress to accommodate its growing population in a way that is environmentally sustainable while preserving open spaces that are economic assets to the region.

The conversation precedes the release of the Institute’s forthcoming report Bay Area Balance: Preserving Open Space, Addressing Housing Affordability that makes the economic case for preserving open spaces and identifies opportunities for responsible development in the region. The report complements East Bay Regional Parks District’s Quantifying Our Quality of Life report, an economic analysis of open spaces in the East Bay.

Listen to the conversation below.

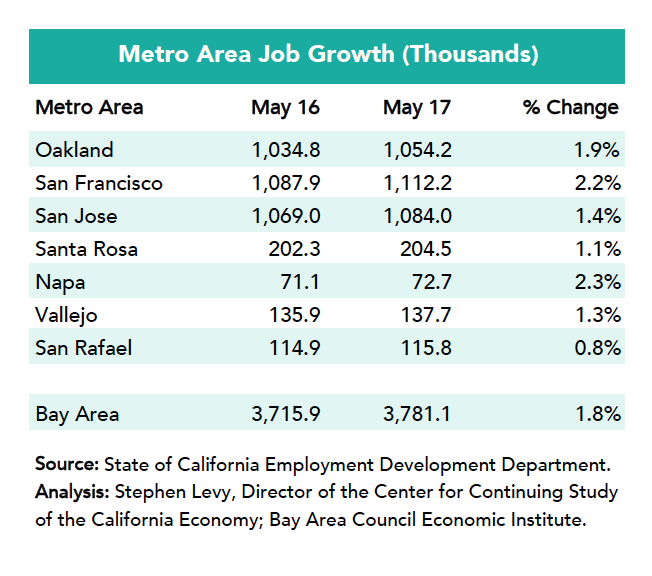

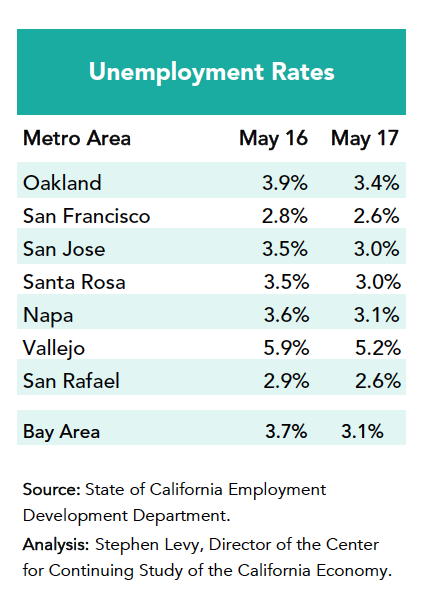

The California Employment Development Department (EDD) has released job and labor force estimates for May 2017. Here are the highlights:

Job growth in the Bay Area and state has slowed since January…

Unemployment and unemployment rates have reached the lowest levels since the dot.com boom and labor force growth has disappeared at least temporarily.

Job openings nationally are at record levels at the same time unemployment is low and labor force growth is slowing.

Before summarizing the recent data, this brief looks at the strength and vigor of the regional economy over the period since 2012.

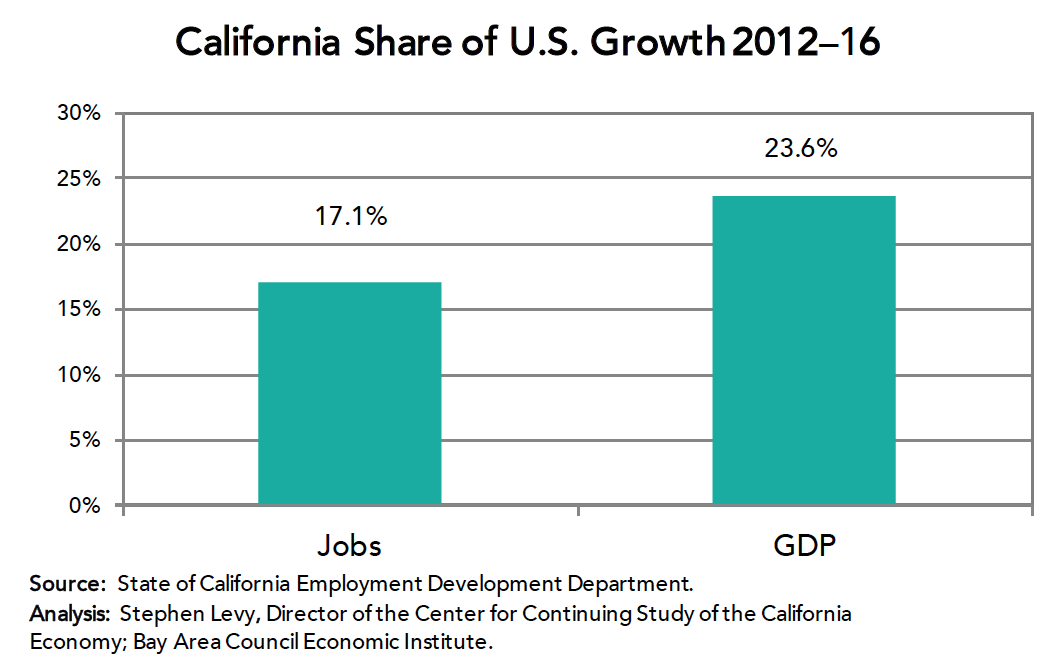

The state accounted for 17.1% of U.S. job growth and 23.6% of national GDP growth between 2012 and 2016 while representing between 11% and 12% of national jobs and population. The Bay Area with 2.5% of U.S. jobs in 2012 accounted for 4.8% of national job growth and the rest of the state also outpaced the nation in job growth. The Bay Area also accounted for an above-average share of GDP growth.

A High and Rising Share of Fast Growth Sectors

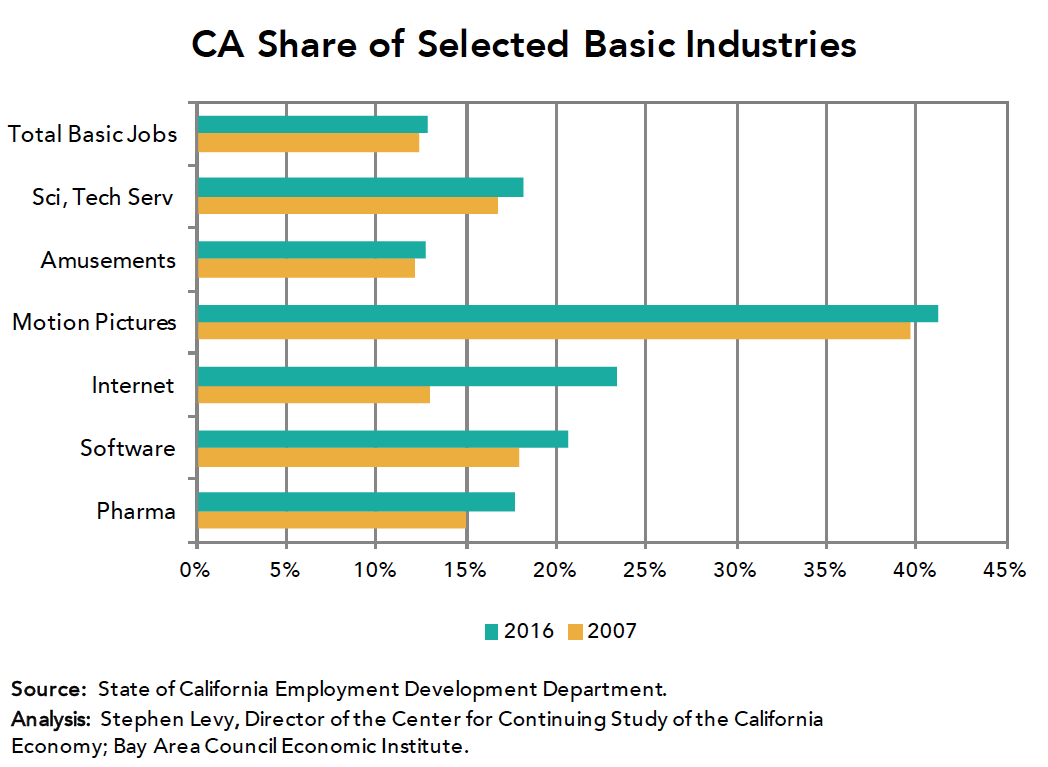

The state has a high share of fast growing basic (export oriented) sectors, many concentrated in the Bay Area and California increased its share of national jobs in many key sectors between 2007 and 2016.

These gains pushed the state’s share of total U.S. jobs to 11.8% in 2016, a record, from 11.4% in 2012.

The state and Bay Area economic strength in the face of strict air quality regulations, high and rising housing costs and state and local tax increases, lend perspective to two national policy issues.

The Bay Area this month achieved compliance with two more federal air quality standards and the Air Resources Board announced that both total and per capita GHG emissions are declining. At the same time the region is attracting company after company taking advantage of our labor force to innovate in a variety of clean tech endeavors.

These trends show that helping the environment is consistent with, and will be helped by in the long run, policies to promote energy efficiency and air quality.

The second point is that the Bay Area and state economies are critical to U.S. economic growth. That is what the 17.1% of job growth and 23.6% of GDP growth tell us. That means that policies that could hurt our economy like restrictive trade and immigration policies, will also retard national economic growth. Our economies are connected.

Looking at the Bay Area Slowdown

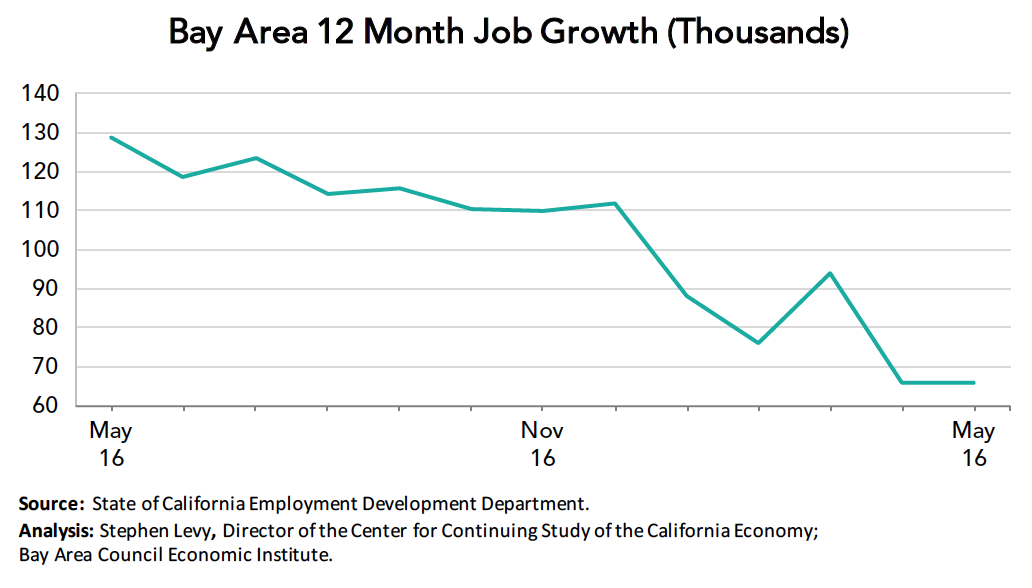

Job growth has slowed. The Bay Area still outpaces the nation in job growth in May 2017 but barely and state growth lags the nation for the first time in several years.

Job growth is slowing throughout the region. For the past 12 months only the Oakland, San Francisco and Napa metro areas have added jobs at a faster pace than the nation.

At the same time unemployment rates have declined sharply throughout the region to the lowest levels since the dot.com boom.

While unemployment and unemployment rates have declined, labor force growth has shrunk to 0 for the past 12 months. This has created a very tight labor market where finding workers has become more difficult.

Job growth levels have declined sharply since last May from near 130,000 on a year over year basis to roughly half that level.

Is the slowdown a sign of serious trouble ahead or is this a temporary bump in the road.

Job growth will slow in the nation, state and region going forward as labor force growth slows with more boomers retiring.

But this week alone has brought positive signs for the region’s future.

Google is exploring a very large (20,000 job) expansion around Diridon station in San Jose that will, if completed, bring additional housing and retail activity,

Alphabet announced plans to add 300 modular units to the Moffett Field development in a test of whether modular units can be an important part of reducing the cost of housing in the region

The federal government announced that for now “dreamers” will be allowed to learn and earn

Last week Jeff Bellisario, one of the Institute’s co-authors of the Megaregion study came to an expert panel meeting I ran for the Sacramento Area Council of Governments in preparing their upcoming regional transportation and sustainable communities plan. The meeting, with Jeff’s help, explored the possibilities for improved economic competitiveness in the two regions through better Bay Area/Sacramento region connections.

Thanks, Jeff.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

Much of the political rhetoric of the 2016 Presidential campaign focused on the winners and losers of the nation’s economic transformation over the past several decades, painting global trade and rapid technological advancements as villains stealing blue collar jobs and decimating local economies in places like Ohio, Michigan and Pennsylvania. The story, however, is far more complex and one that has huge implications for our region. The Bay Area Council and the Bay Area Council Economic Institute are delving into those complexities, and this week hosted a fascinating discussion with Ohio Congressman Tim Ryan and Silicon Valley Congressman Ro Khanna on the many and strong connections between the Bay Area and America’s heartland and the vast opportunity for deepening those connections to address concerns about economic displacement.

The conversation, which was moderated by former Economic Institute Chair and eminent UC Berkeley economist Laura D’Andrea Tyson, explored how the Bay Area’s innovation leadership can be leveraged to boost up places that are feeling left behind, the ways in which that can happen and the widespread economic benefits that it can produce. Institute president, Micah Weinberg initiated the conversation by telling the story of Alabama’s half a billion dollar investment that led to the auto manufacturing industry boom during a time in which many part suppliers in the region did not meet OSHA guidelines and standards. The industry grew by about 26,000 jobs, many of which were low-paying and dangerous. By contrast, Bay Area companies on brought 27,000 jobs with higher average wages to the region without the financial incentive Alabama-based companies received.

The Economic Institute also previewed an online tool that offers a detailed analysis of the existing jobs and economic connections between Bay Area companies and individual states and congressional districts. The tool will be formally launched in the coming weeks.

Read more about the conversation from Wired’s Nitasha Tiku.

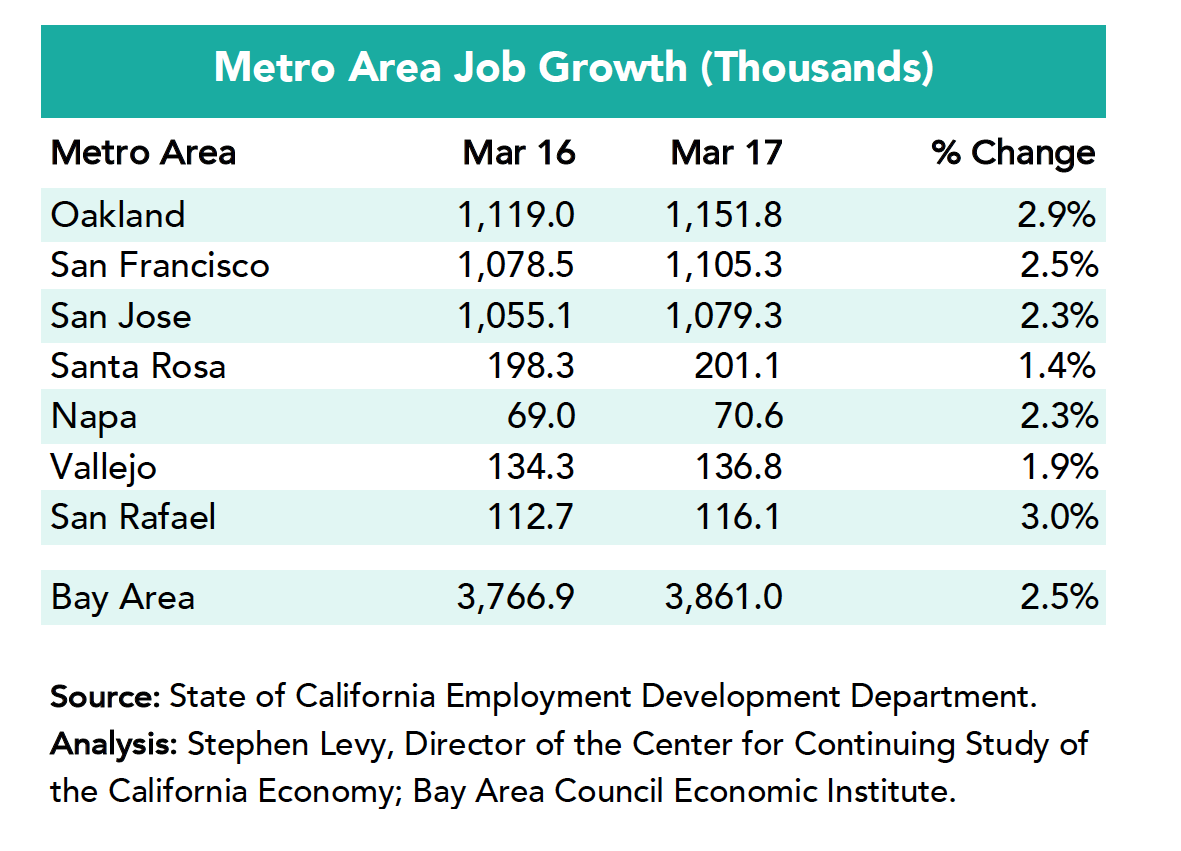

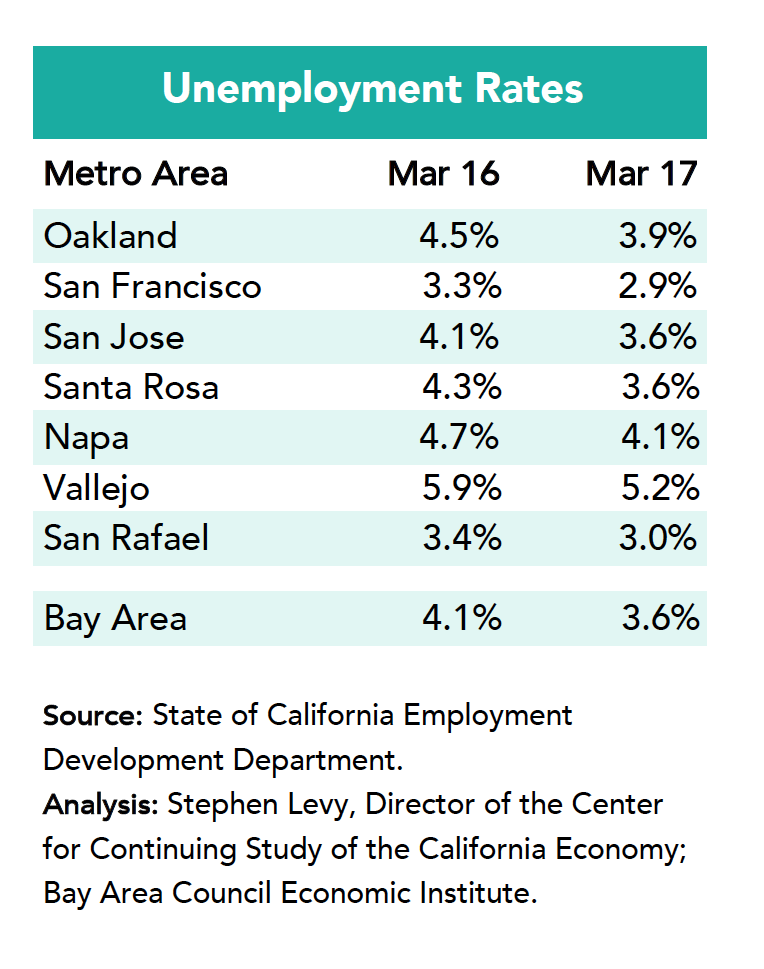

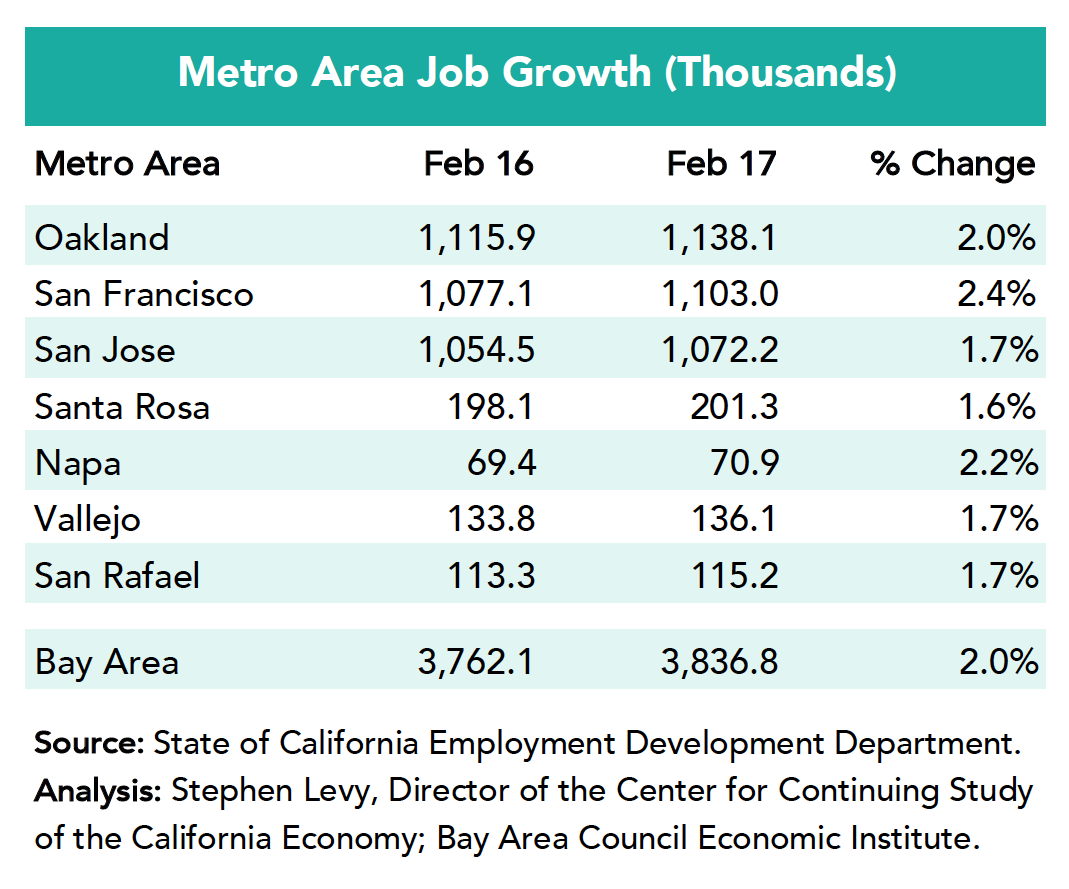

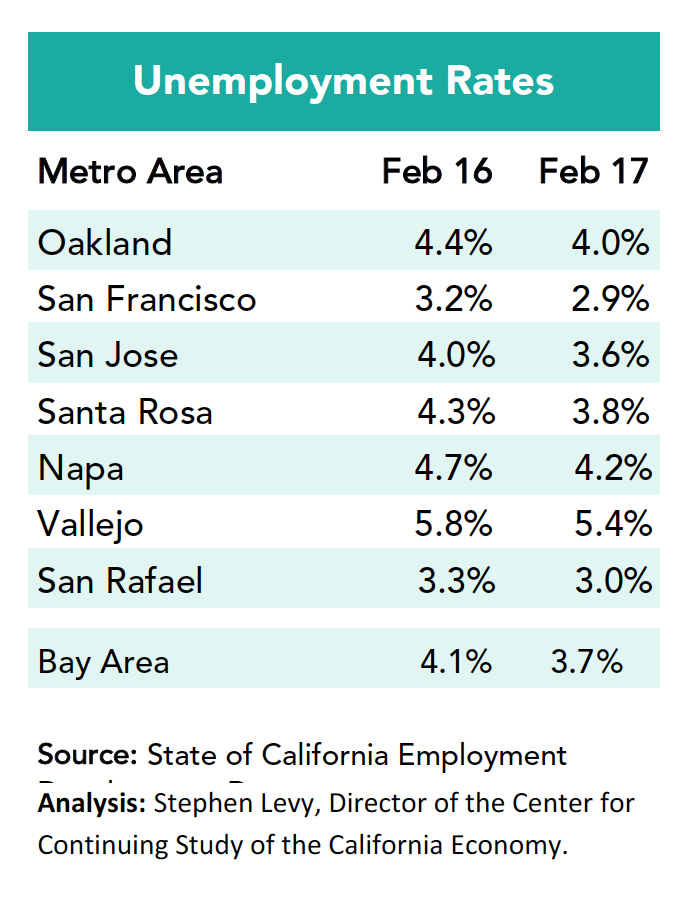

The California Employment Development Department (EDD) has released job and labor force estimates for March 2017. Here are the highlights.

Job growth picked up in March led by gains in the Oakland metro area and the region again outpaces the nation and state in job growth.

Unemployment and unemployment rates continue to decline throughout the region.

National job growth slowed in March leaving the first quarter of 2017 with conflicting job trends in the nation, state, and region.

Year over Year Job Growth Strong but Slowing

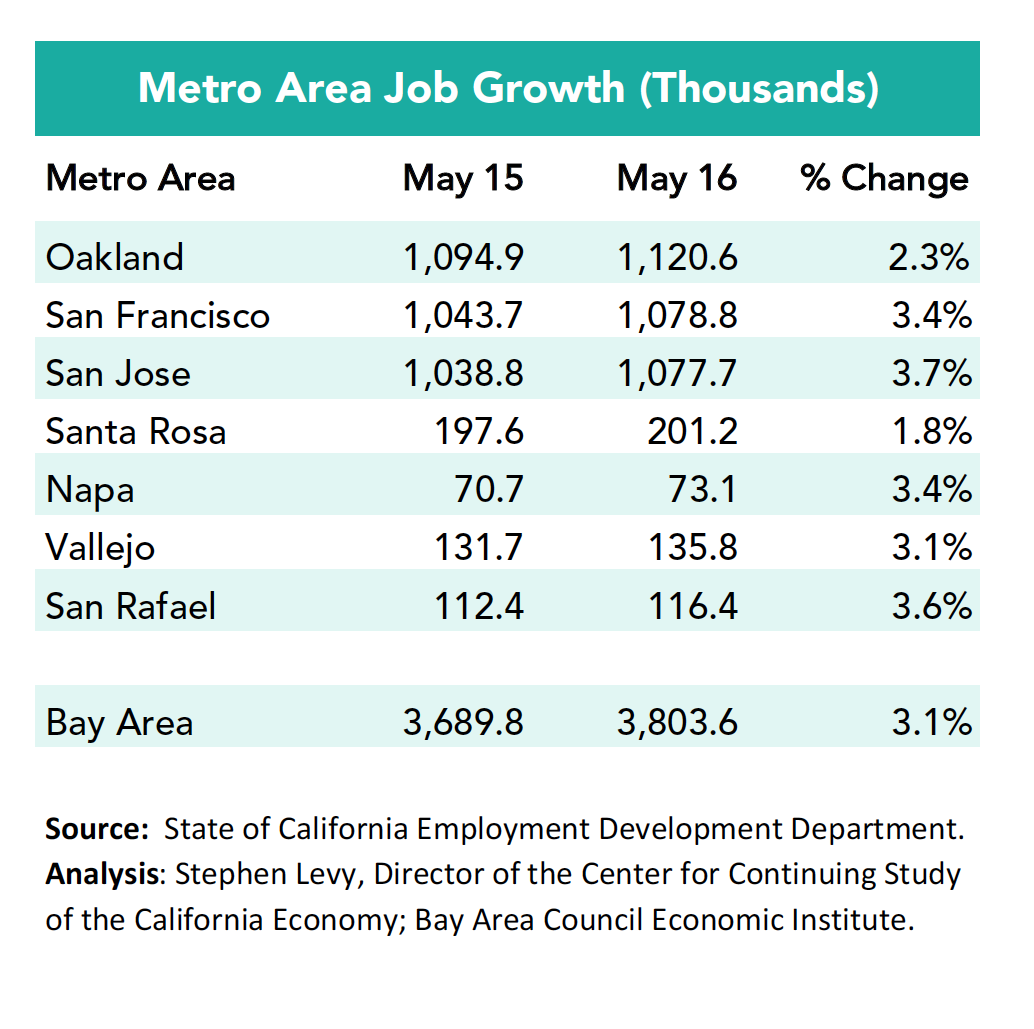

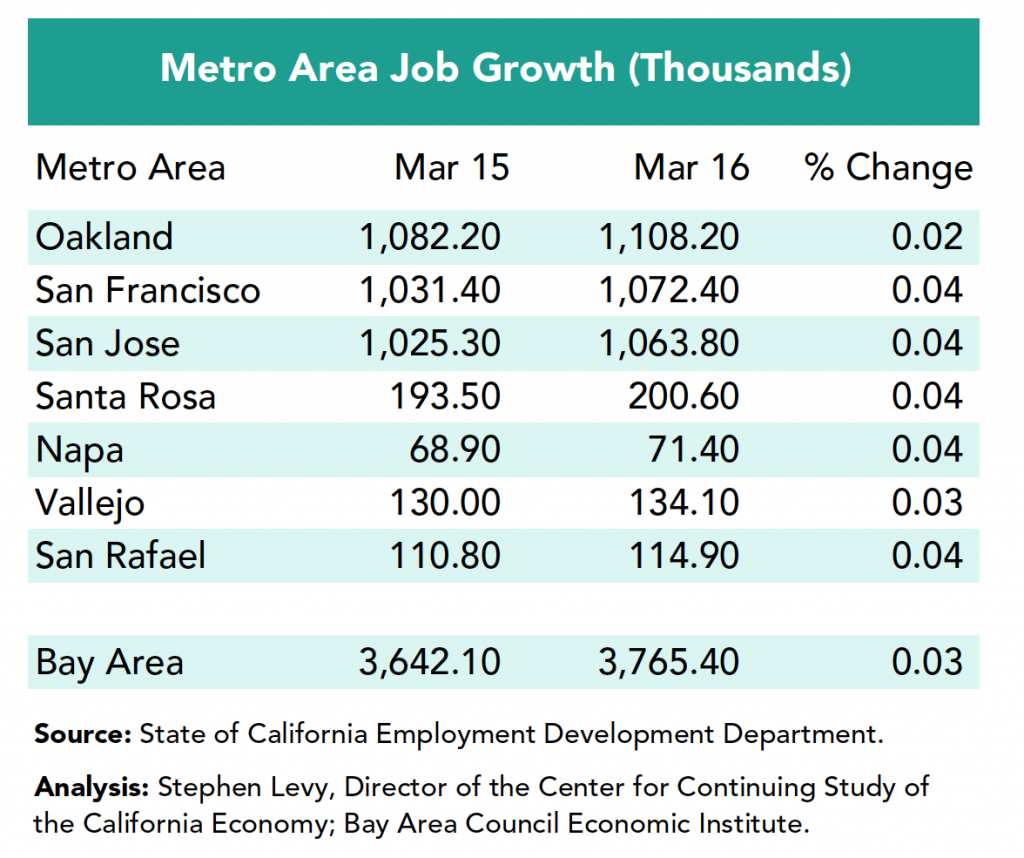

The region added 94,100 jobs between March 2016 and 2017 for a gain of 2.5% compared to 1.5% for the nation and 2.1% for California.

Year over year job growth remains equal to or above the national average in all metro areas in the region except the Santa Rosa metro area though at a much slower pace than in the past two years. The Oakland metro area has become a growth leader in the past three months as the peninsula showed strong but slowing job gains compared to a year earlier.

The March job trends erase, for the moment, fears that January and February data showed a loss of competitive advantage for the region.

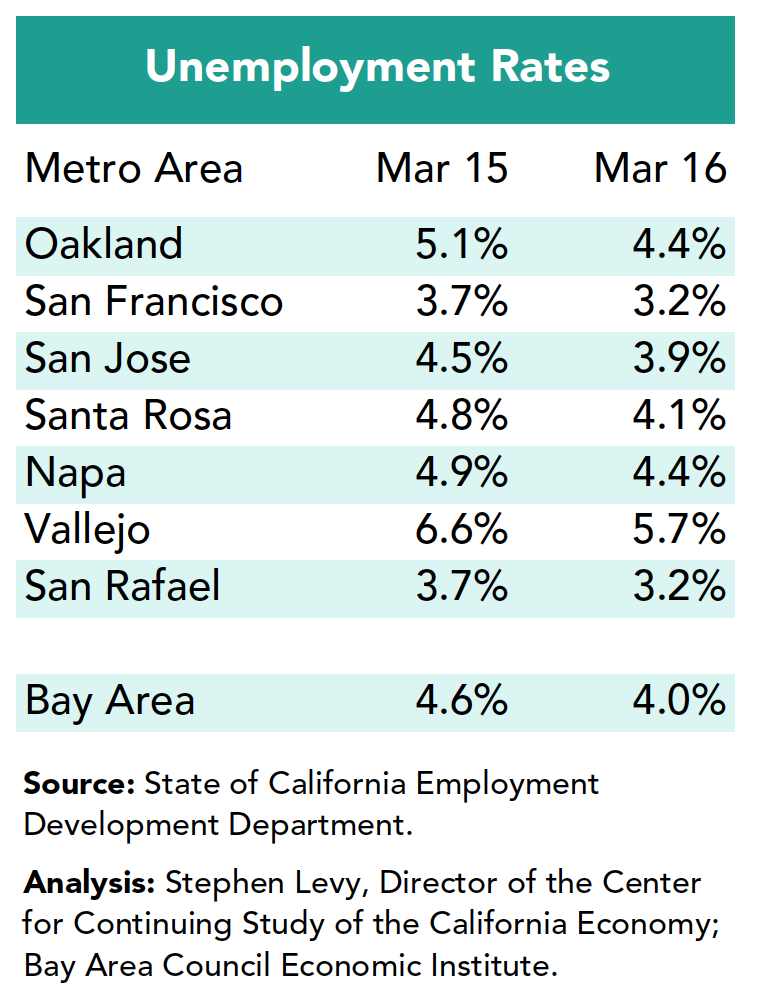

The job gains continue to push unemployment rates lower but labor force growth has slowed dramatically in recent months and is up only 0.3% over the past year. The regional unemployment rate at 3.6% is substantially lower than the national 4.5% and state 4.9% unemployment rates. Only the Vallejo metro area has an unemployment rate higher than the national rate.

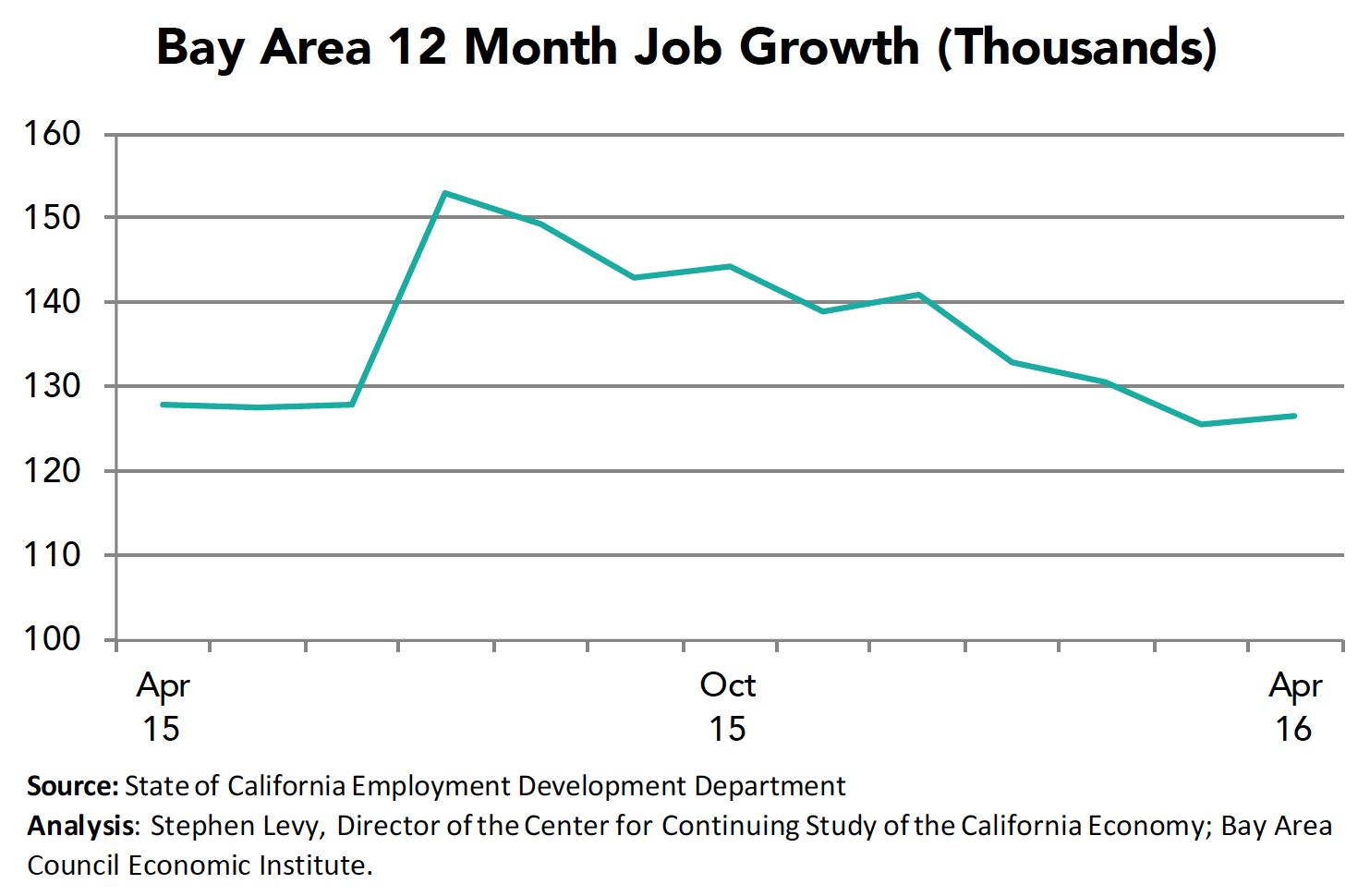

Year over year job gains bounced back up in March after declining sharply in the first two months of 2017 from mid-2016 levels. It is too soon to know if the severity of the recent declines was a one-time event or reflects ongoing challenges for the region.

The continuing job growth now that unemployment rates have fallen will bring new residents to the region as will the growing need to replace retiring workers.

All of these trends underscore the importance of policies to increase housing and make sure that housing and transportation challenges do not undermine the region’s still vibrant economic competitiveness. Bay Area residents approved many funding measures for transportation and several local measures give hope that the housing supply and affordability challenges are being increasingly recognized by residents. The Bay Area Council has identified policies that can reduce costs and other barriers to expanding housing choices in the Solving the Housing Affordability Crisis report (2016).

While more communities such as San Francisco, Redwood City and Mountain View are now approving housing developments, the region has a long way to go and regional stakeholders will also want to watch the many housing bills now in the state legislature.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

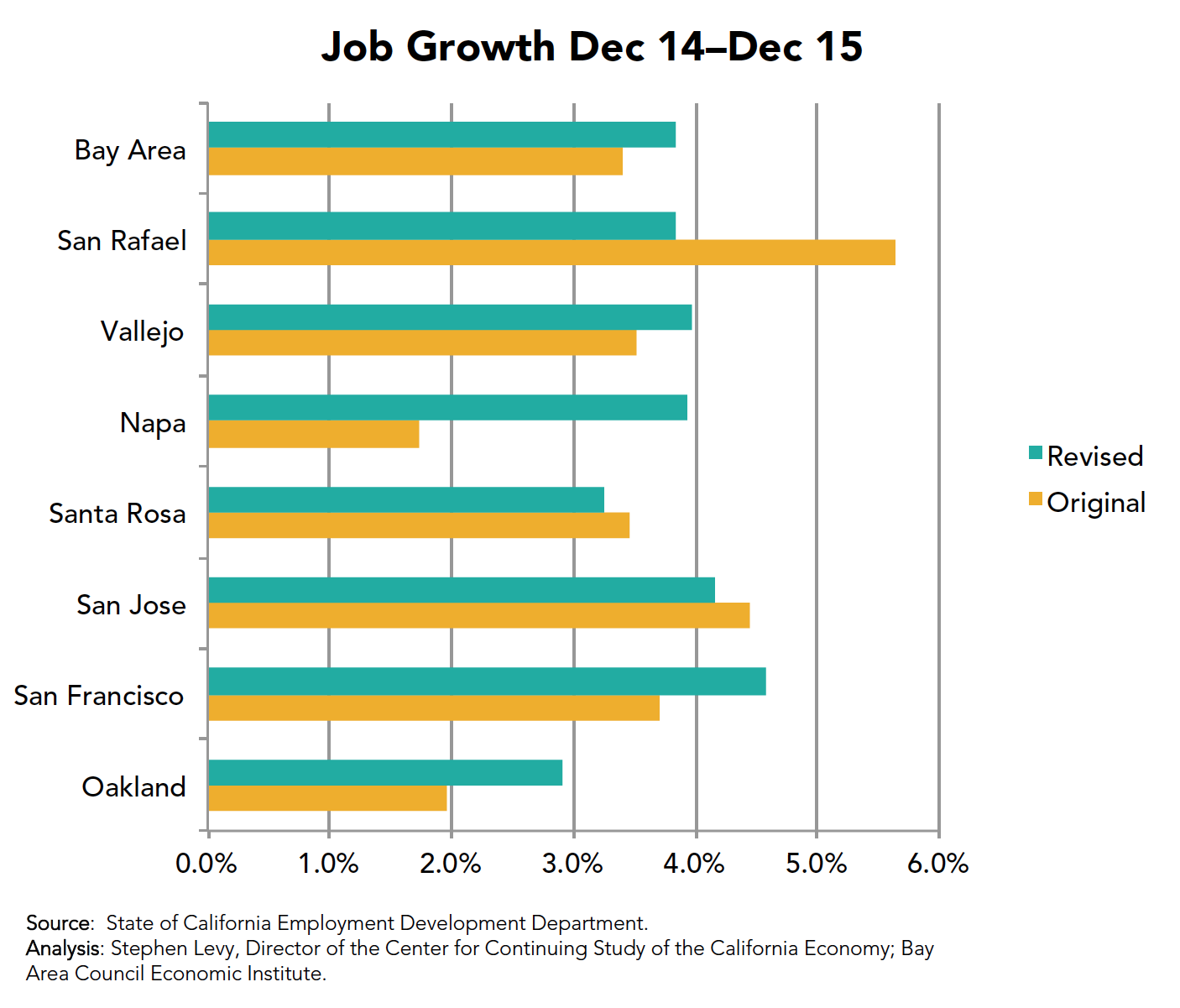

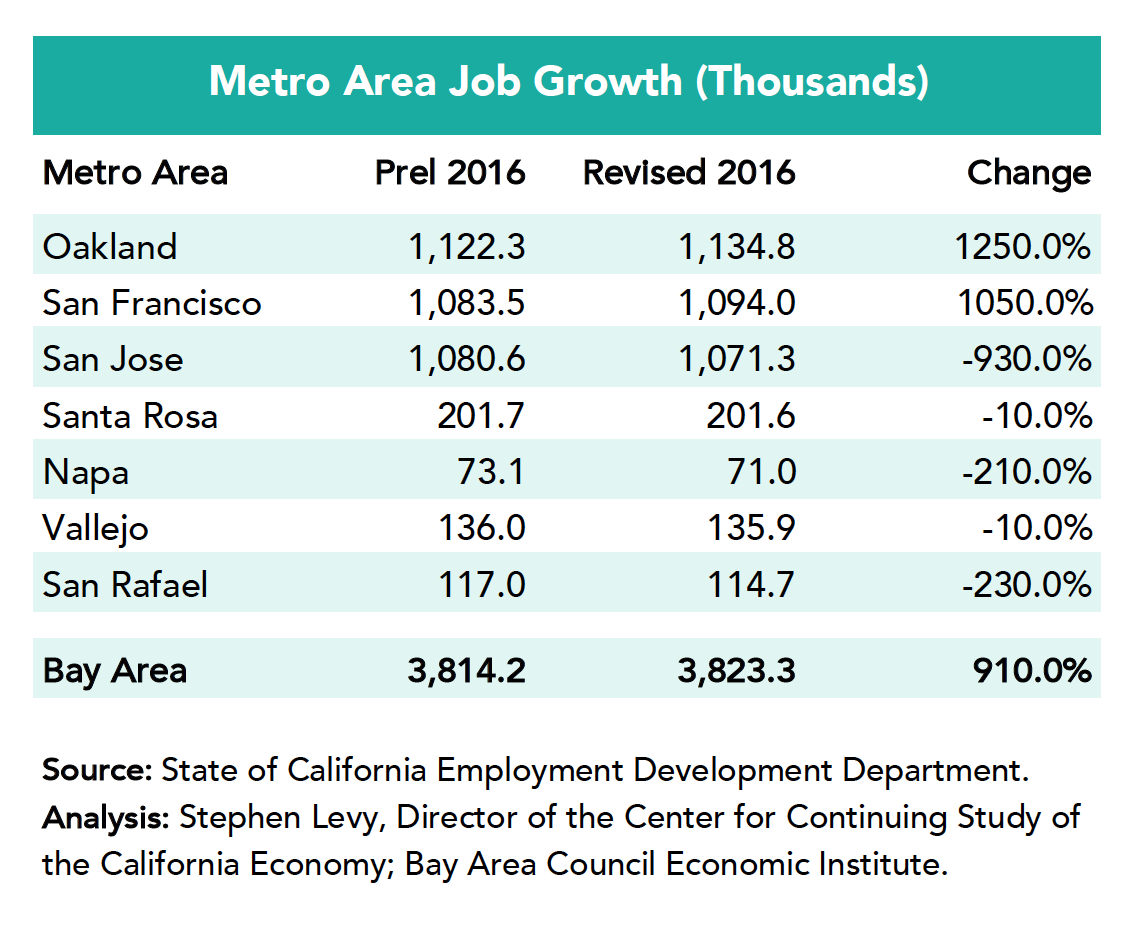

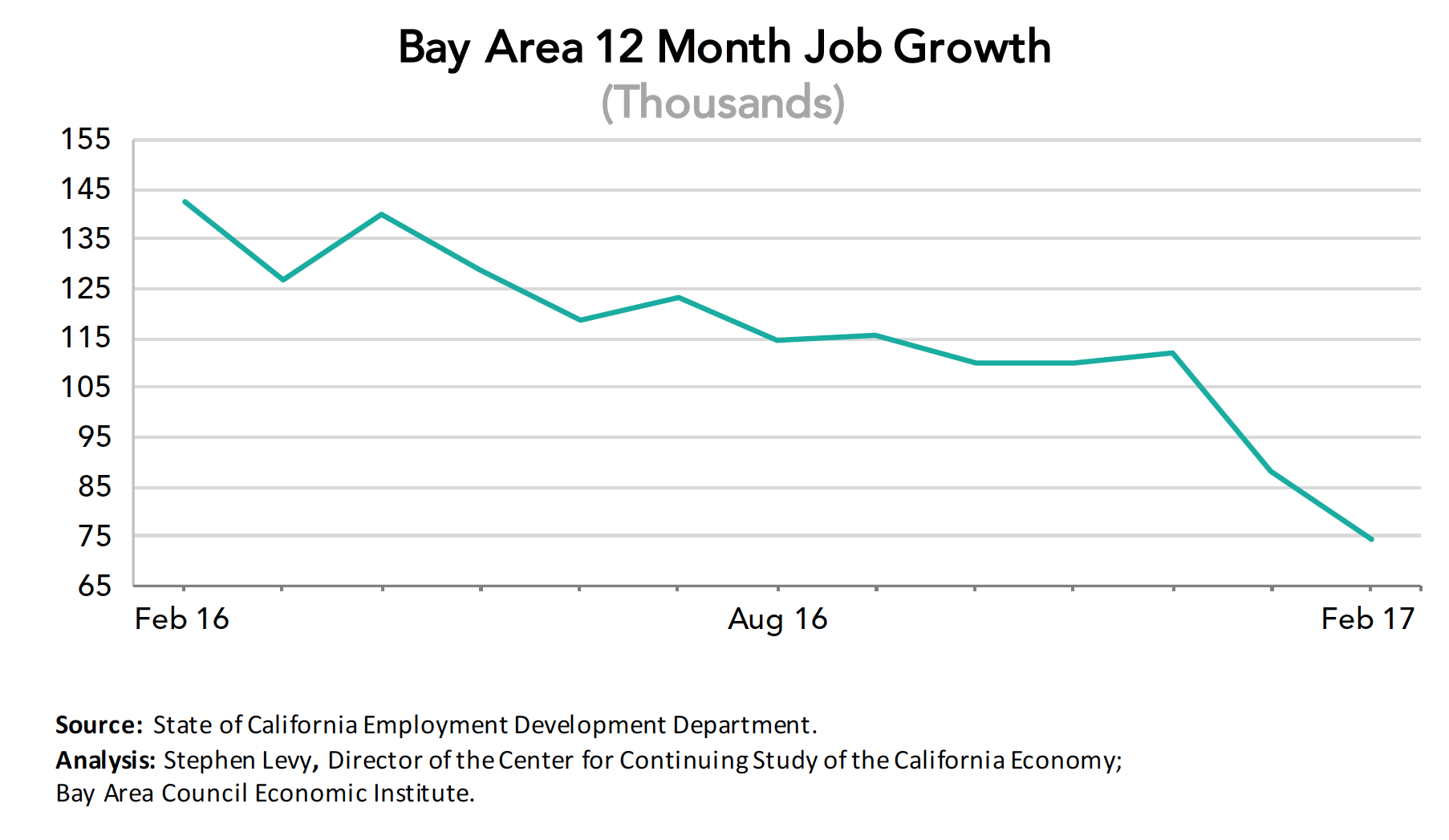

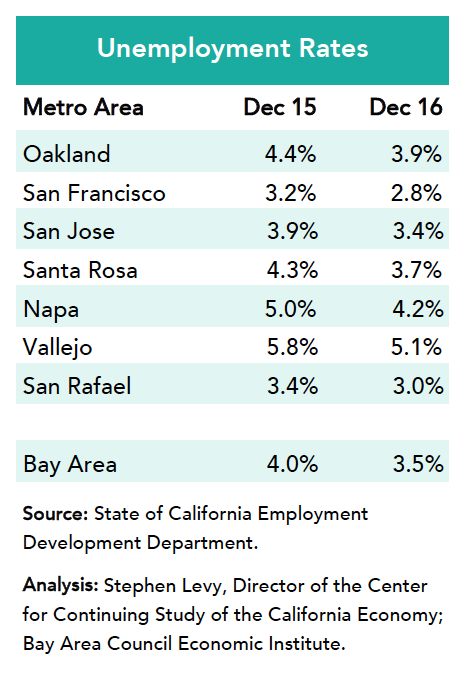

The California Employment Development Department (EDD) has released job and labor force estimates for February 2017 and revisions for 2015 and 2016. Here are the highlights.

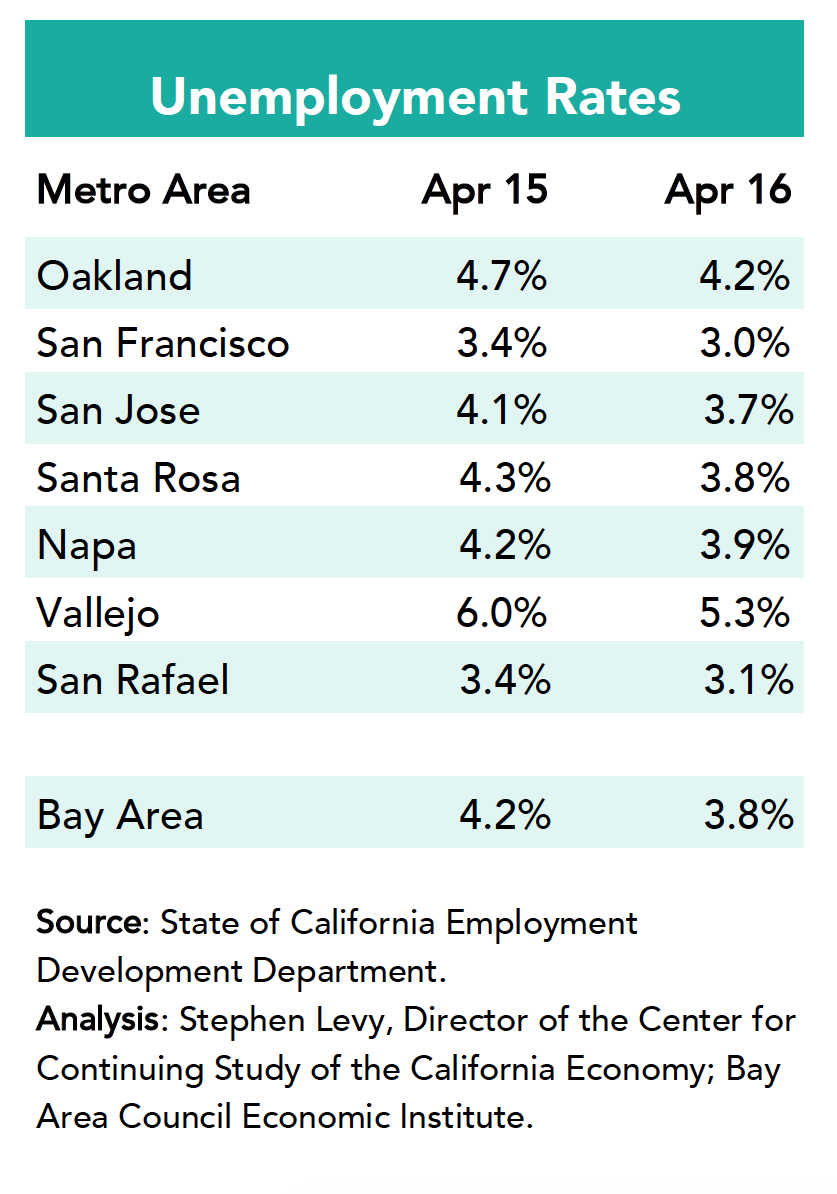

Job growth slowed in the first two months of 2017 and now only slightly outpaces the state and nation while the region’s unemployment rate remains below 4%.

The region added approximately 10,000 more jobs in 2016 than originally reported.

This week Amazon announced a 1,300 job tech oriented expansion in East Palo Alto to take advantage of the region’s skilled workforce. This builds on the move by auto companies for similar reasons.

Year over Year Job Growth Strong but Slowing

The region added 74,700 jobs between February 2016 and 2017 for a gain of 2.0% compared to 1.6% for the nation and 1.9% for California. While the January and February job numbers may be revised upwards, the pace of job growth is likely to slow in 2017 and beyond as more baby boomers retire and the pool of unemployed workers shrinks.

Year over year job growth remains equal to or above the national average in all metro areas in the region though at a much slower pace than in the past two years.

The job gains continue to push unemployment rates lower but labor force growth has slowed dramatically in recent months and is up only 0.3% over the past year.

Each year in March EDD makes revisions to the previous year’s job estimates. Overall the region gained jobs in the revision though the Oakland and SF metros gained while the San Jose metro had fewer jobs than previously reported.

Year over year job gains declined sharply in the first two months of 2017 from mid-2016 levels. It is too soon to know if the severity of the recent declines will continue.

The continuing job growth now that unemployment rates have fallen will bring new residents to the region as will the growing need to replace retiring workers.

All of these trends underscore the importance of policies to increase housing and make sure that housing and transportation challenges do not undermine the region’s still vibrant economic competitiveness. Bay Area residents approved many funding measures for transportation and several local measures give hope that the housing supply and affordability challenges are being increasingly recognized by residents. The Bay Area Council has identified policies that can reduce costs and other barriers to expanding housing choices. http://www.bayareacouncil.org/economy/by-the-numbers-solving-the-housing-affordability-crisis/.

While more communities such as San Francisco, Redwood City and Mountain View are now approving housing developments, the region has a long way to go and regional stakeholders will also want to watch the many housing bills now in the state legislature.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

This morning, Institute president Micah Weinberg participated in a segment of NPR’s Morning Edition along with reporter Stephanie O’Neill of Kaiser Health News. The segment discussed the impacts of the new Republican health care bill in California, a state where one in three residents rely on Medi-Cal for health insurance.

California was one of the states that fully embraced Obamacare to reduce the number of uninsured people. As it stands, Medi-Cal covers 14 million Californians. Of those covered, two-thirds actively participate in the labor force. Moreover, our 2016 Mainstreaming Medi-Cal report found that Medi-Cal generates $1.7 billion in increased yearly personal income in the state. A repeal of the program will have a devastating impact on the state’s economy.

Under the proposed Obamacare replacement, the Medi-Cal program would lose part of its federal funding and would be entirely cut from the federal budget by 2020. Although the actual magnitude of the impact of the proposed replacement plan is not yet determined, many people are expected to lose coverage or make the choice to drop out from Medi-Cal entirely.

Last week, upon request from California’s 14 GOP representatives, U.S. Transportation Secretary the Elaine Chao decided to delay the decision to award a $650 million federal grant to the state of California for the electrification of a Caltrain Bay Area commuter rail system. The proposed transformation would electrify the current railway system connecting San Jose and San Francisco, two of California’s major innovation and employment hubs.

The plan to electrify Caltrain’s railway system has been in the works for almost two decades, but the need to complete hasn’t been felt as urgent as now. In 2016, the Caltrain system carried over 62,000 riders per weekday, an 83% increase in ridership since 2010. Similarly, weekend ridership has increased 36% in the same period of time. This trend is expected to continue as the region’s residents and labor force increase.

Continued job growth in the region seems to be the main driver for increased ridership. The San Francisco-Redwood City-South San Francisco and San Jose-Sunnyvale-Santa Clara metropolitan regions employ close to two million people and this number is expected to rise. Just between December 2015 and 2016, the Bay Area region added 100,300 jobs, a 2.4% increase compared to 1.5% for the nation and 2.0% for the whole state. Job gains continue to push unemployment rates lower even as the labor force continues to add workers although the region is now at or close to full employment.

The Bay Area is one of the nation’s top economic drivers. In 2015 alone the Bay Area generated over $666 million in GDP, ranking 3rd in GPD nationwide, behind the New York and Los Angeles metropolitan regions. Between 2014 and 2015 alone, the region saw a 5.8% increase in GDP compared 2.5% average increase seen by all other US metro areas.

According to MTC’s Vital Signs’ regional performance profile, the average time spent in public transportation by Bay Area commuters amounted to 48.9 minutes in 2014. Caltrain’s Project 2025 estimates that completion of this project would reduce commute time for riders by 10 minutes and would encourage people to use the system, resulting in increased ridership and fewer cars on the road. Further delay of the electrification of Caltrain penalizes the thousands of Californians that travel within the region, especially those that do so for work.

The fact that the Bay Area and its hubs are significant drivers for the US economy is undeniable. Delaying Caltrain’s electrification ultimately hurts workers and the overall productivity of the region. The Bay Area will continue to grow and its transportation infrastructure needs to meet the needs of the region’s residents.

Last week, Economic Institute President Micah Weinberg participated in a panel at the Brookings’ Center for Health Policy addressing what worked and what didn’t work in Obamacare insurance markets. Dr. Weinberg pointed out that “you can’t put together competing networks in an area with only one hospital system. If we really care about competition, we need to care about competitors. The competitors we care the most about are actually not the insurance plans, but rather the providers.”

The panel discussion parallels the newly released report Study of Affordable Care Act Competitiveness in California developed by the Economic Institute in partnership with Brookings. The report examines the implementation of the Affordable Care Act in California and assesses the interplay among factors such as health care provider concentration, the choices that the state made in implementation, the underlying market dynamics, and the extent to which the structure of the federal law all contributed to creating these choices for consumers across the many diverse regions of the state.

Most of what was said about trade during the presidential campaign was wrong. Chalk it up to politics, but both candidates fed voters a line that distorts our understanding of what free trade is about and how Americans benefit. Uninformed voters might be forgiven for believing them. It’s better, though, to know the facts.

First, let’s define what this is about. Free trade agreements are partnerships between nations that agree to drop barriers — such as tariffs and quotas — to trade. Such agreements make goods and services cheaper for both parties and increase jobs and exports for both.

Let’s also be clear that California has a lot at stake. As the nation’s second-largest exporting state and a technology powerhouse, we particularly stand to benefit from provisions that open agricultural markets (California is the nation’s largest agricultural exporter) and protect intellectual property and the cross-border movement of data — issues of great importance to our tech companies.

So here are the facts:

Free trade agreements are not killing manufacturing. At $2.2 trillion, U.S. manufacturing output is at an all-time high. But output is different from employment, which has been falling for decades. That’s a result of technology and improved efficiency in production processes, not trade agreements. Analysis shows that only 13 percent of manufacturing’s job loss is linked to trade, while 87 percent is caused by automation.

Free trade agreements don’t hurt the U.S. trade balance — they help it. Taken together, the U.S. has a positive balance of trade with the 20 countries with which it has free trade agreements. The U.S. International Trade Commission estimates that in 2015 those agreements contributed a net gain of nearly $60 billion to our global trade balance. Our deficit is overwhelmingly with countries such as China, where the U.S. does not have free trade agreements.

Free trade agreements are about growing the pie. Seventy-five percent of the world’s purchasing power is outside the United States, something U.S. companies can’t ignore. These agreements open doors. Even though the United States’ 20 free trade partners account for only 6 percent of the world’s population and less than 10 percent of its economy, they purchase nearly half of U.S. manufactured exports.

Our manufactured exports also are growing faster to our free trade partners than to countries where no U.S. free trade agreement is in place. In 2015, U.S. manufacturers sent $12.7 billion more in manufactured goods to those countries than they sold to us. At the same time, the U.S. had a $639 billion manufactured trade deficit with non-free-trade countries.

Distorted views of trade, an unfortunate legacy of the election, have extended to individual agreements. Is NAFTA really a disaster for jobs and manufacturing? Then why have manufactured exports to Canada and Mexico nearly quadrupled since NAFTA entered into force? The reality is that we buy a lot from Mexico and Canada, but many of those products are assembled from U.S.-made components.

The Trans-Pacific Partnership, a proposed agreement with 11 Asia-Pacific countries, is the biggest victim of this false debate. The U.S. International Trade Commission — the most authoritative source available — estimates that with a Trans-Pacific Partnership, both exports and imports would grow, but exports would grow faster. Both agriculture and services, the area where most economic growth today is occurring, would benefit as long-standing trade barriers in Japan and other countries are reduced. These are areas where California and the Bay Area lead.

The significance of free trade agreements runs deeper. They are about writing the rules of trade. When agreements such as Trans-Pacific Partnership protect intellectual property and the free movement of data, it’s because the U.S. has fought for those principles. Other provisions provide enforceable environmental and labor protections, which are core U.S. values. Those values aren’t universal, however. China has its own trade deal on the table with 16 Asia-Pacific countries (the Regional Comprehensive Economic Partnership) which does not share those priorities.

If we abandon the Trans-Pacific Partnership but China’s deal goes forward, then U.S. companies will lose competitiveness across the region. China can’t be faulted for advancing its interests and those of its companies. We have no less a responsibility to advance ours.

So where do we go from here?

Affirm our existing trade agreements. Tweak them, maybe. But acknowledge that they’re working and important to our economy.

Stick with the basics of the proposed Trans-Pacific Partnership. Its provisions are good for both the U.S. and its partners, and should serve as the foundation for any new proposals.

Support manufacturing by fixing the tax code. At 35 percent, our corporate tax rate is the highest in the developed world and should be reduced so that it’s closer to the global norm. This will encourage more investment in the United States. Tax rates should also be adjusted to encourage repatriation of the more than $2 trillion in profits our companies have parked overseas — if it’s reinvested in infrastructure or assets like production equipment and worker training.

Support U.S. workers.Far more workers benefit from these agreements than don’t, but for those who lose the pain is real. Trade Adjustment Assistance, which provides transitional assistance to workers who lose their jobs as a result of trade, should be revisited and strengthened.

If we’re really concerned about dislocated workers, however, then our national focus should be on the disruption of traditional employment being caused by advances in technology — a process that is only beginning. Developing a national strategy to anticipate those changes should be a bipartisan priority in Congress. But don’t stop trade.

Sean Randolph is Senior Director at the Bay Area Council Economic Institute

As the world watched the inauguration of President Donald Trump, the Bay Area Council Economic Institute’s 10th Annual Economic Forecast presented by McKinsey & Company and hosted by the Federal Reserve Bank of San Francisco convened leading economists and top experts to give their economic forecast for the Bay Area, California, and the nation.

The prognosis was clear. As we usher in the new administration, we are on stable footing. Dr. Christopher Thornberg, Founding Partner of Beacon Economics and a leading expert on the California economy, presented on a set of economic indicators, showing that much of the national political rhetoric around stagnant wages, the impact of trade, and unemployment is not borne out in the economic data. Labor markets are tight and becoming tighter across most of the United States. This is particularly true in California where the housing supply problem is one of the biggest challenges to continued growth. He also assessed that, while GDP is growing relatively slowly, it is growing and economic fundamentals, such as consumer spending, remain strong. Among the challenges cited for slow growth were self-inflicted wounds and political gridlock, a weak global economy, and the shift to an information economy among others. And, while there is little chance for a recession (for now), uncertainty surrounding the new administration’s policy agenda clouds the view forward. There are broad ramifications for potential change in policy in healthcare, immigration, social insurance, trade, manufacturing, and more.

San Francisco Fed President and Council Executive Committee member John Williams offered an exclusive perspective on the U.S. economy and federal monetary policy. Williams talked about the dynamics surrounding the U.S. labor market and how the Fed is likely to gradually increase its interest rate targets over time so that the economy grows without risking a bubble. Williams emphasized how the central bank is not influenced by partisan politics, staying politically independent, data-driven and focused on its narrow goals to promote low inflation, full employment and financial stability.

Bay Area Council Economic Institute Chair and McKinsey & Company Western Region Managing Partner Kausik Rajgopal and Aspen Institute Fellow Natalie Foster explored the “Future of the Worker” in the new age of automation and the growing gig economy. In the Bay Area, the independent workforce is 30 percent of the working age population with most digital independents working in order to earn when traditional jobs falter, to provide extra income for high cost of living or to buffer uneven income streams. One of the key points discussed was how automation is focused on specific activities rather than entire jobs, and can spur more job growth.

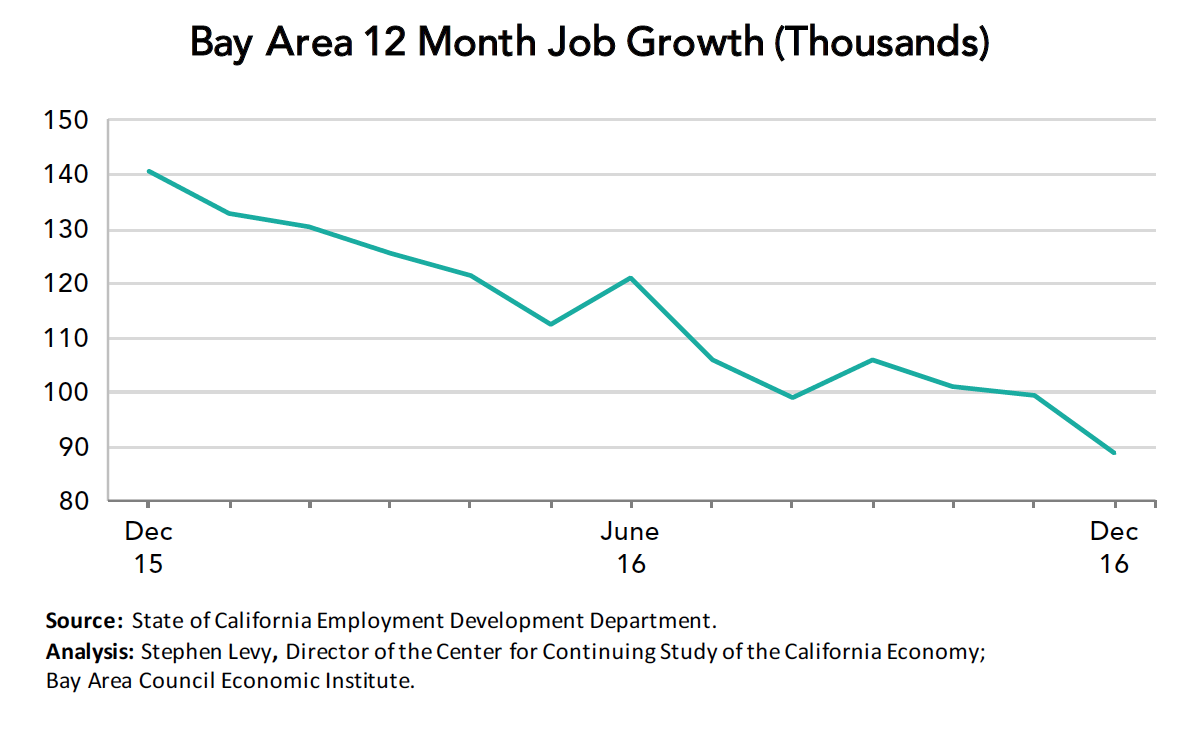

The California Employment Development Department (EDD) has released job and labor force estimates for December 2016. Here are the highlights.

Job growth slowed in December while year over year gains continue to outpace the state and nation.

Labor force growth remains strong which implies that job opportunities are strong enough to bring some workers back into the workforce.

At the same time as the labor force is surging, unemployment rates are at the lowest level since the dot.com boom.

Year over Year Job Growth Strong but Slowing

The region added 100,300 jobs between December 2015 and 2016 for a gain of 2.4% compared to 1.5% for the nation and 2.0% for California. The pace of job growth is likely to slow in 2017 and beyond as more baby boomers retire and the pool of unemployed workers shrinks but companies throughout the region continue to make plans for expansion as shown by the recent approval of the Facebook expansion in Menlo Park.

Year over year job growth remains above the national average in all but one metro area in the region.

The job gains continue to push unemployment rates lower even as the labor force continues to add workers although the region is now at or close to full employment.

While year over year job gains have declined from mid 2015 peaks, they remain in very healthy territory with no signs of a significant loss of competitive advantage. Job growth rates in 2016 are likely to be the peak going forward as baby boomer retirements are slowing labor force growth.

The continuing job growth now that unemployment rates have fallen will bring new residents to the region as will the growing need to replace retiring workers.

All of these trends underscore the importance of policies to increase housing and make sure that housing and transportation challenges do not undermine the region’s still vibrant economic competitiveness. Bay Area residents approved many funding measures for transportation and several local measures give hope that the housing supply and affordability challenges are being increasingly recognized by residents. The Bay Area Council has identified policies that can reduce costs and other barriers to expanding housing choices. Here is their analysis

Today President Trump was inaugurated.

His agenda has implications for the state and regional economy that will be explored by the Bay Area Council Economic Institute in future months. Here is a first analysis.

The region’s economy is tied to the world economy through trade, immigration and investment. All of these issues were discussed the incoming President and what happens in the coming legislative session will have major implications for the state and regional economies.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

By Keith Carson Published on January 2nd, 2017

This op-ed originally appeared in the East Bay Times

My father always taught us that while we may not always accept the opinions of others, we must respect the opinions of others. For many of us living in this complex world, this concept is becoming more challenging with each passing day.

On Jan. 20, Donald Trump will be sworn in as the 45th president of the United States. While there are a range of emotions about Trump and his presidency, not much real attention has been focused on the 61 million Americans, including nearly 4 million Californians and 215,000 residents of Alameda and Contra Costa counties, who elected him to that office.

This campaign brought to light the great divide that exists in this country, one that we suppress, dismiss and ignore, but unfortunately surfaces daily.

Annual statistics document the grave disparities that have existed and still exist in education, housing, employment, the criminal justice system, and a range of other areas.

Disproportionately these disparities have impacted black, brown, and other people of color, indigenous people, and struggling, poor whites.

While President-elect Trump openly campaigned on attacking approaches to achieve equity, his 61 million supporters felt his platform reflected their views and values. These are 61 million people who live among us, teach in our schools, protect and serve, and make important decisions in government, business, and public life.

This 61 million decide daily who will or will not get sent to jail, receive a loan, get expelled from school, or receive medical attention.

We must engage the Trump presidency and the 61 million people who voted to elect him and his vision for America. Our faith-based organizations need to honestly and transparently revisit the doctrines upon which they were founded, answering the age-old question, “Am I my brother’s/sister’s keeper?”

Our public safety institutions must critically examine the scales of Lady Justice and ask themselves, “Are we a just society?” And we local elected officials must also look in the mirror and ask, “Are we taking the strides to serve the greatest good for our communities?”

Together we must begin an authentic dialogue with one another, even with those of different opinions.

Our local faith-based and community organizations need to open their doors and initiate these conversations in earnest at the ground level.

Those of us in public leadership need to come together and identify a common agenda to unite us around our shared goals.

Doing so can highlight that despite our differences of skin color, sexual orientation, religious belief, or economic status, we have far more in common.

We share the desires of a better future for our community and to live in peace, to develop to our maximum potential, and to genuinely embrace those who may be different from us.

Keith Carson represents District 5 on the Alameda County Board of Supervisors. Carson can be reached at 1221 Oak St., Suite 536, Oakland, CA 94612, 510-272-6695 or dist5@acgov.org.

Keith Carson is part of the Economic Institute’s Board of Trustees.

Header image by AP Photo/Evan Vucci

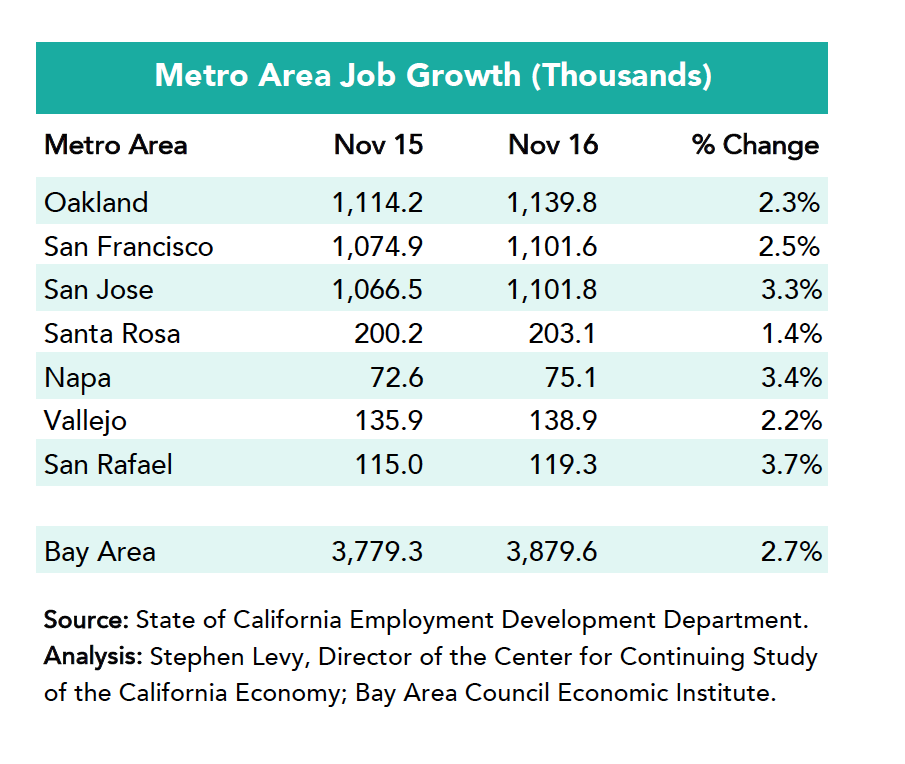

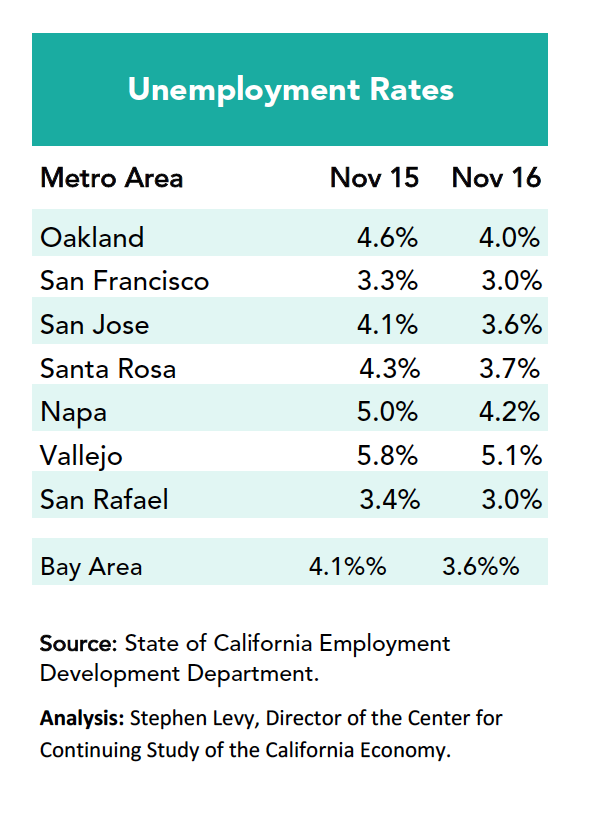

The California Employment Development Department (EDD) has released job and labor force estimates for November 2016 and the California Department of Finance has released county population estimates for 2016. Here are the highlights.

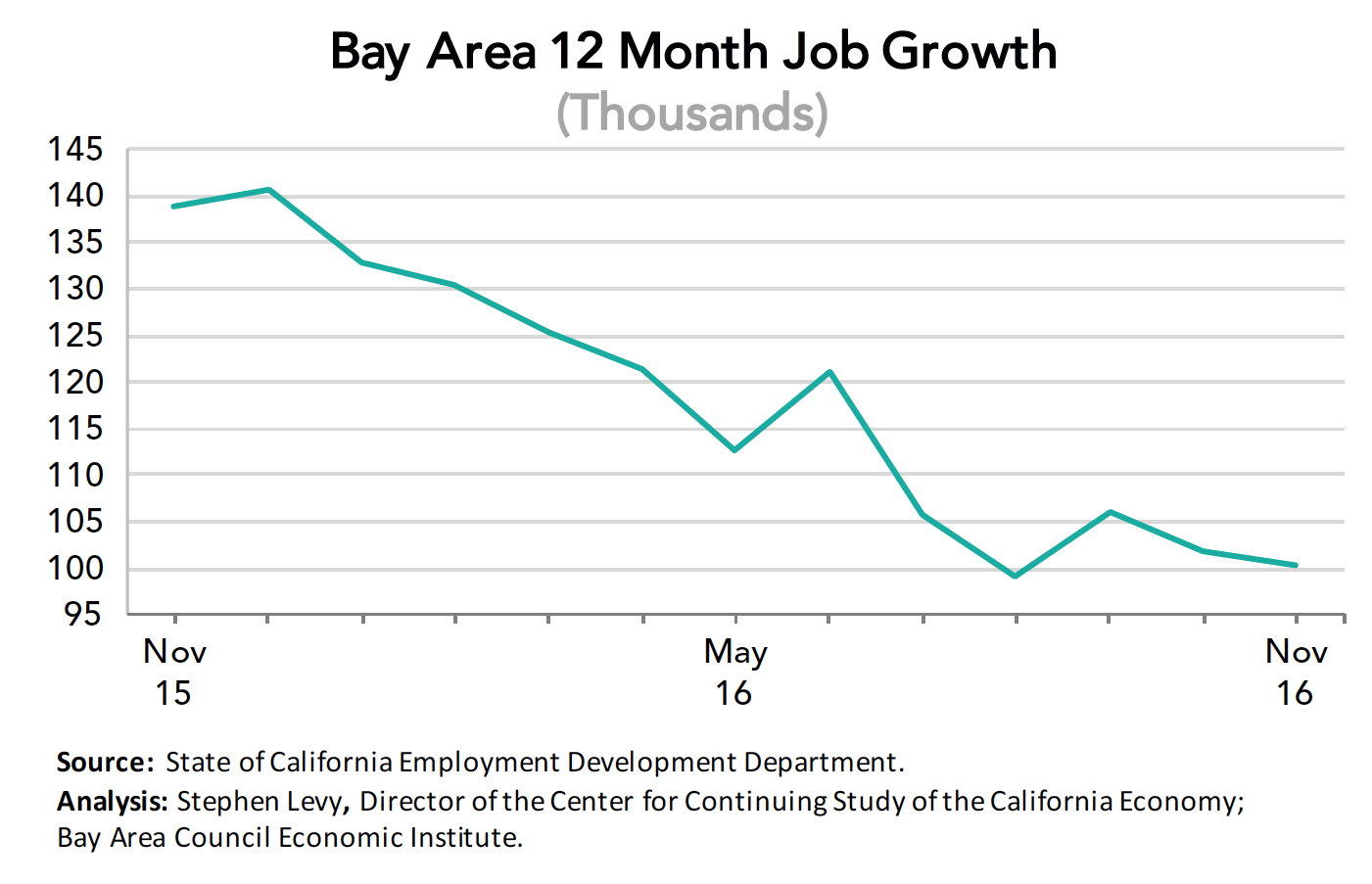

Although job growth slowed slightly in November year over year gains continue to outpace the state and nation and year over year job growth is remains above 100,000.

Labor force growth remains strong and is outpacing population growth, which implies that job opportunities are strong enough to bring some workers back into the workforce.

At the same time as the labor force is surging, unemployment rates are at the lowest level since the dot-com boom.

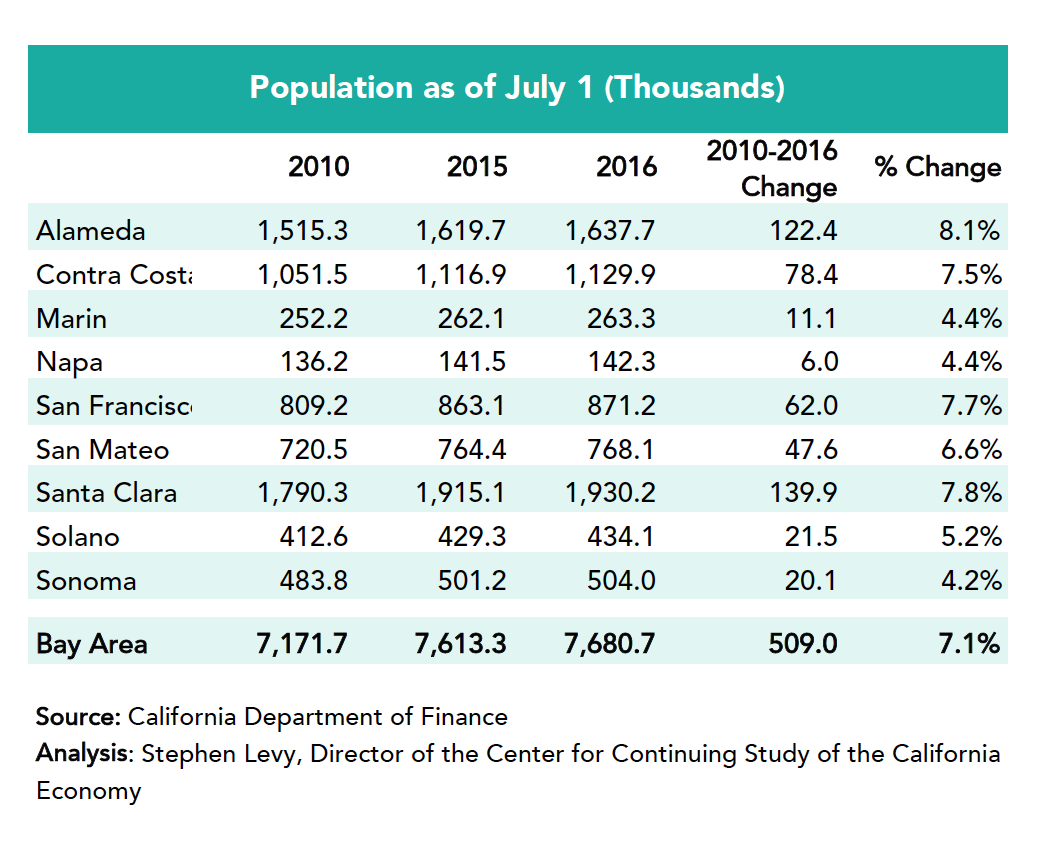

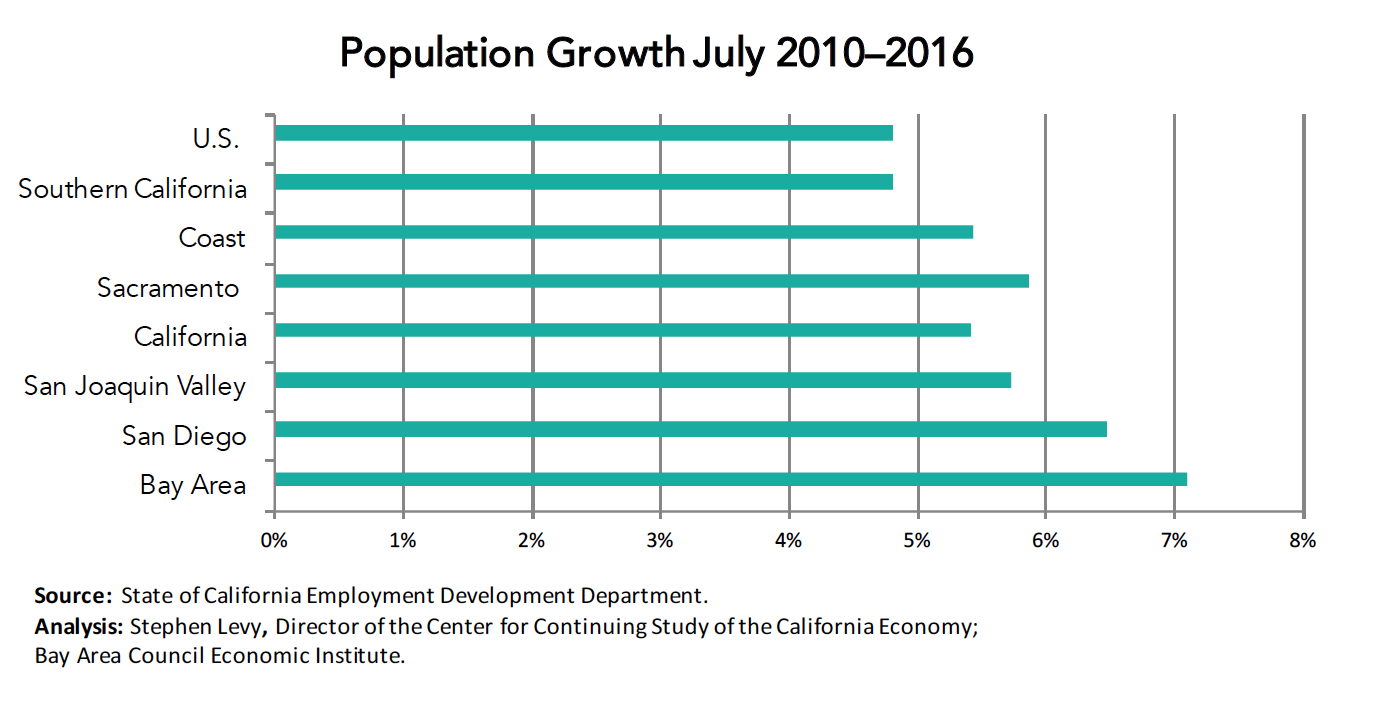

Population growth slowed in the state and region in 2016 but the Bay Area remains the fastest growing region in California measured by both jobs and population since 2010.

Year over Year Job Growth Strong but Slowing Slightly

The region added 100,300 jobs between November 2015 and 2016 for a gain of 2.7% compared to 1.6% for the nation and 2.3% for California. The pace of job growth is likely to slow in 2017 and beyond as more baby boomers retire but companies throughout the region continue to make plans for expansion as shown by the recent approval of the Facebook expansion in Menlo Park.

Year over year job growth remains above the national average in all but one metro area in the region.

The job gains continue to push unemployment rates lower even as while the labor force continues to add workers although the region is now at or close to full employment.

While year over year job gains have declined from mid 2015 peaks, they remain in very healthy territory with no signs of a significant loss of competitive advantage. Job growth rates in 2016 are likely to be the peak going forward as baby boomer retirements are slowing labor force growth.

The continuing job growth now that unemployment rates have fallen will bring new residents to the region as will the growing need to replace retiring workers.

All of these trends underscore the importance of policies to increase housing and make sure that housing and transportation challenges do not undermine the region’s still vibrant economic competitiveness. Bay Area residents approved many funding measures for transportation and several local measures give hope that the housing supply and affordability challenges are being increasingly recognized by residents. The Bay Area Council has identified policies that can reduce costs and other barriers to expanding housing choices. Read the report here.

The national election results have implications for the state and regional economy that will be explored by the Bay Area Council Economic Institute in future months. Click here to read the analysis.

Summary Population Update

The Bay Area added 67,400 residents in the year ending June 30, 2016. This is slightly less than in the previous three years. The fastest growth rates since 2010 were in Alameda (8.1%), Santa Clara (7.8%), San Francisco (7.7%) and Contra Costa (7.5%). For the first time since the Gold Rush days the Bay Area is the fastest growing region in California and also outpaced the nation in population growth. More details will come in the next update.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

Recap

Thirty-five business leaders, government officials, and real estate developers convened in San Francisco on December 8 to tackle two questions that are vexing California families, governments, and employers: In the face of surging housing demand, high housing prices, and historically low interest rates, why does California chronically under-produce housing?What can we do in the near term to unlock supply?

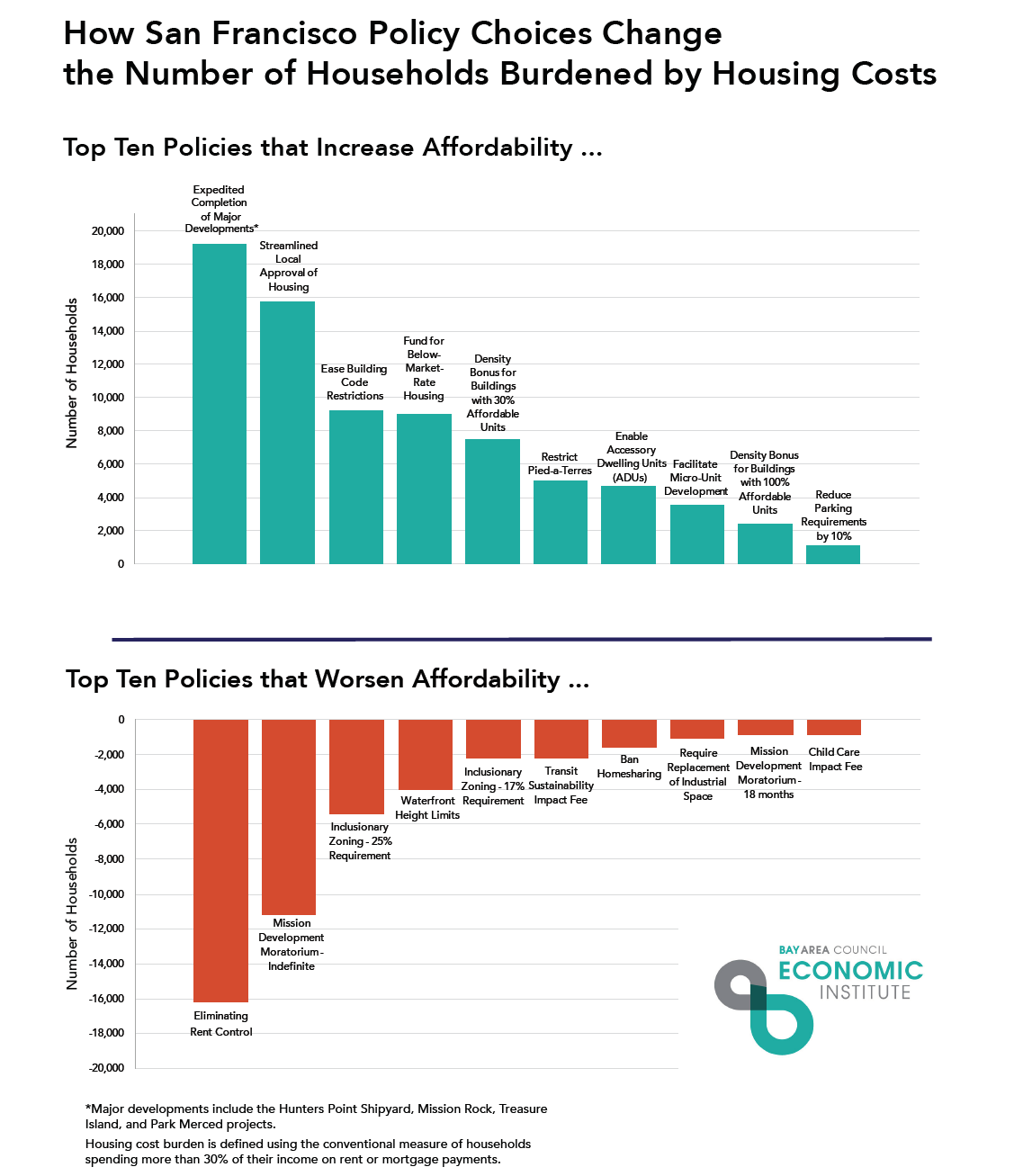

Context: California real estate prices have risen three times faster than household incomes. As a result, more than half of the state’s residents cannot afford housing. This housing affordability gap, which is particularly acute in San Francisco, hurts families, exacerbates homelessness, and damages the region’s economic competitiveness. McKinsey & Company’s 2016 California housing affordability report ranked California 49th out of 50 U.S. states for housing supply—and estimated that California needs to build 3.5 million housing units by 2025. The analysis identified physical capacity to build five million new housing units in the state—including 500,000 potential units in the inner Bay Area. According to a recent report from the Bay Area Council Economic Institute, public policy can play a critical role in unlocking supply and creating a greater degree of affordability for families. The report analyzes 20 proposed or enacted San Francisco housing policies and their impacts on affordability.

Some of the key themes discussed included:

Win hearts and minds for housing. We need storytelling, not just data. Building conviction for housing among major voting blocs—e.g., environmentalists and organized labor—is critical. “Never let a good crisis go to waste”. The state could reframe the conversation by declaring a housing crisis and the electorate would be receptive to action due to skyrocketing rents and home prices. Critical electoral groups—the middle-income workforce, seniors and millennials—are particularly affected by this crisis. A professional public relations strategy could go a long way toward winning the hearts and minds of all stakeholders.

Develop a deeper fact base on what drives or impedes housing production. For cost reasons, housing production in California skews towards single-family structures rather than mid-rise or high-rise. The economics of dense development become even more challenging when fees and other policy-driven costs are included. To stimulate infill, we need to understand compressible costs, including the cost impacts of current regulations (e.g., Title 24) and potential future regulations (e.g., Zero Net Energy, purple pipe). If the net effect of environmental regulations is to force people to relocate from California to Texas, where per capita Greenhouse Gas production is three times higher, that is not a positive outcome for the environment.

Help transit agencies accelerate transit-oriented development. BART, Valley Transit Authority, and LA Metro have announced major housing commitments on agency-owned land. Fast tracking the development of these projects will demonstrate what is possible and link densely-built housing with access to transit. California could experiment with “housing accelerators” in the highest-potential transit station areas (e.g., tax increment financing, development-impact fee relief, cap and trade funding, inclusionary zoning, minimum density requirements, eminent domain, and streamlined approvals). By bringing transit agencies, city planning officials, developers, and community advocates together to plan and build successful developments, these accelerators can become a model for other California cities.

Improve funding for housing projects. Creating new transportation/housing funding streams linked to local housing production, imposing a ceiling on development impact fees (waived for cities that meet housing targets), financing non-housing infrastructure at mega-project sites, and committing state resources to facilitate Enhanced Infrastructure Financing Districts could make a big difference.

Give local governments “political cover” to create more housing. Modeled on the Massachusetts Chapter 40B example, allow developers to appeal to a state entity if local governments block housing projects that meet stated sustainability goals.

Rethink sacred cows. Consider revisiting Proposition 13, CEQA, and local control over land use as part of a grand bargain on housing.

Experiment with policy innovations. Options include granting the California Attorney General power to enforce housing element law by suing non-compliant jurisdictions; streamlining land-use approvals for affordable housing projects and transit oriented development (TOD); empowering a state entity to prioritize state-owned land for housing; and creating “policy innovation zones” in housing hotspots.

Bay Area households have the second highest median household income in the country, nonetheless households struggle to afford their basic needs.

The Bay Area has recovered from the Great Recession faster than the rest of the nation, and has proven to be resilient to economic downturns. Labor force participation and job growth rates have surpassed those of the nation. Nonetheless, despite the region’s economic success households have not seen their income rise at a fast enough pace to keep up with the rising cost of living.

According to the Bureau of Labor Statistics, the Bay Area Consumer Price Index (CPI) reached 258.5 in 2015. The index takes into account the cost of shelter – for homeowners and renters – as well as the cost of everyday expenses such as apparel, transportation and medical care. Between 2000 and 2015, CPI saw an increase of 78.4%, one of the fastest growing cost of living for US metro areas. During the same period, the median household income in the Bay Area saw increased from $73,000 to $103,600, a 41.9% total increase 36.5 percentage points behind CPI.

To put things into a national context, the 2015 annual CPI for the whole nation was 237.01 and only saw a .1 percent increase from the previous year. On the other hand, the San Francisco-Oakland-San Jose MSA’s CPI for 2015 was 258.57 saw a 2.6 percentage growth during the same period.

While the Bay Area’s increase in CPI surpassed the nation’s by only a few percentage points, the Bay Area is one of the most expensive regions in the country with median home sale prices tripling the nation’s average. In 2015, the average home sale price in the Bay Area was $766,394, while the nation’s was $247,600. Similarly, Bay Area renters pay among the highest prices for rent in the nation with thirteen Bay Area cities ranking in the top 20 nationally. Listings for one-bedroom apartments in Palo Alto, San Francisco, and Cupertino averaged $3,423 in 2015.

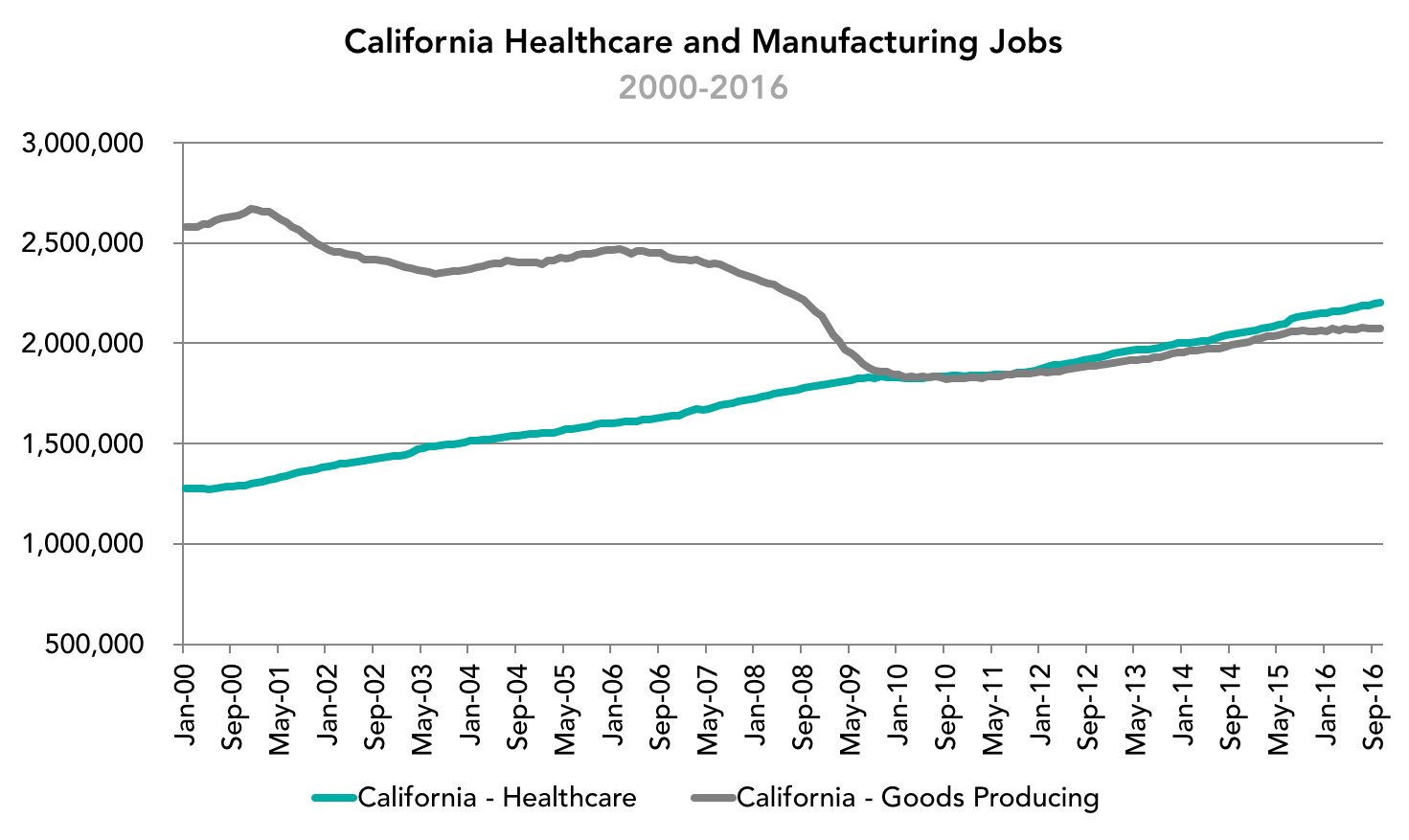

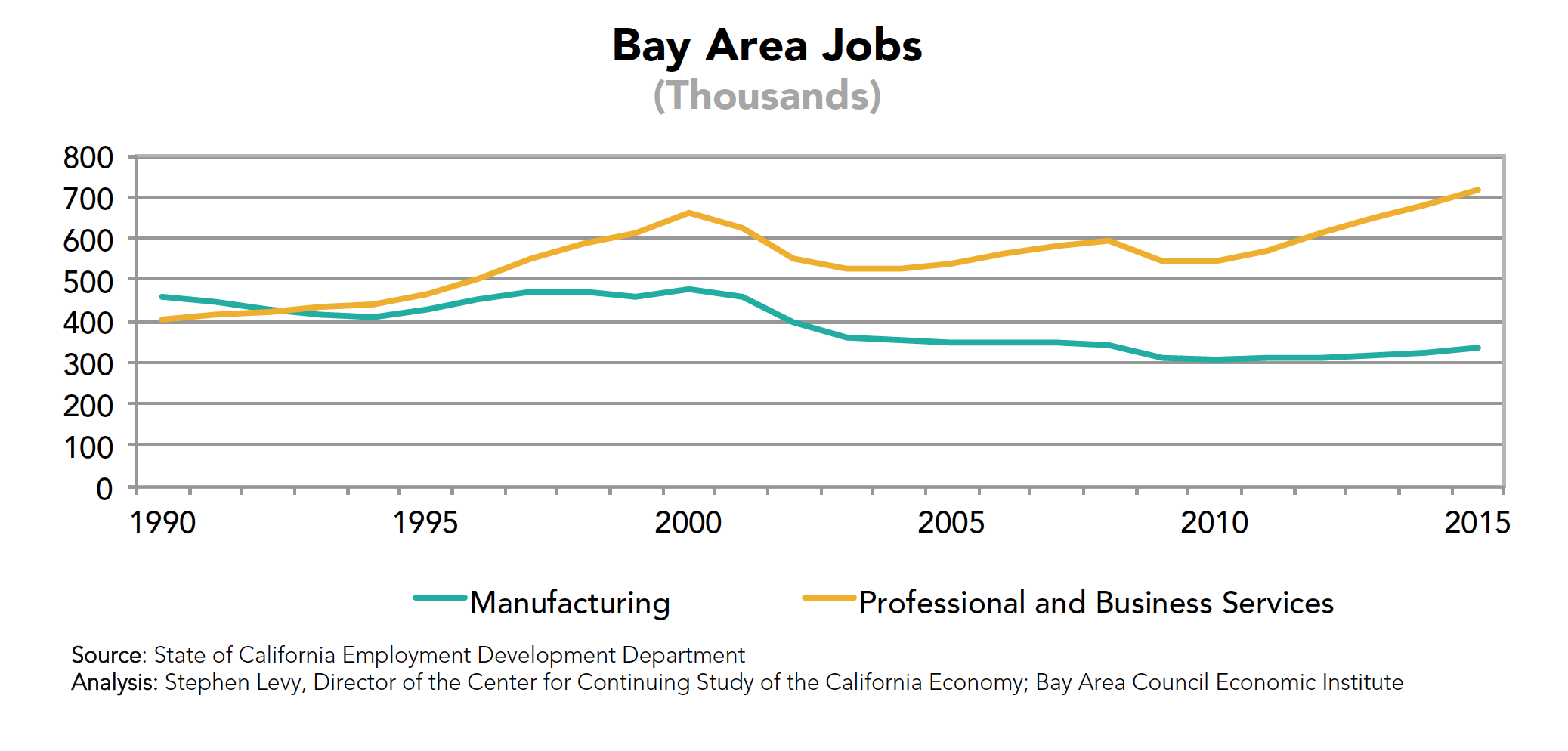

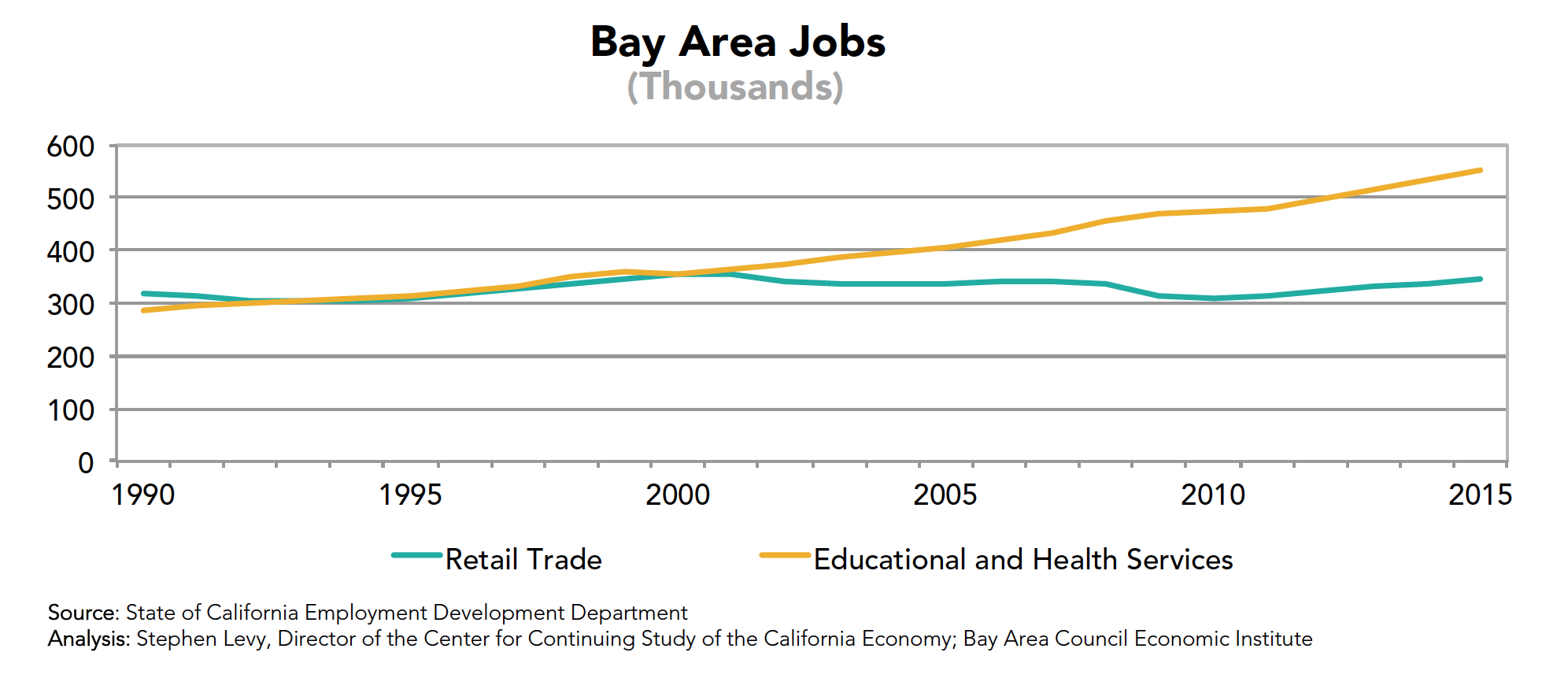

The presidential election focused on the disappearance of manufacturing jobs in the United States as well as the move to repeal the Affordable Care Act, which if it does nothing else, will dramatically decrease the amount of money the federal government spends on healthcare. A deeper dive into the relevant economic data raises important questions about these priorities at least as it relates to job creation. The chart below shows the trend for California that mirrors the trend in the nation: As manufacturing jobs declined over several decades largely driven by automation, they were replaced by healthcare jobs that are substantially more difficult to automate or offshore. There is reason to believe, therefore, that pumping more money, resources and attention into manufacturing at the expense of healthcare may be – for whatever other virtues this strategy may hold – problematic from the standpoint of job creation.

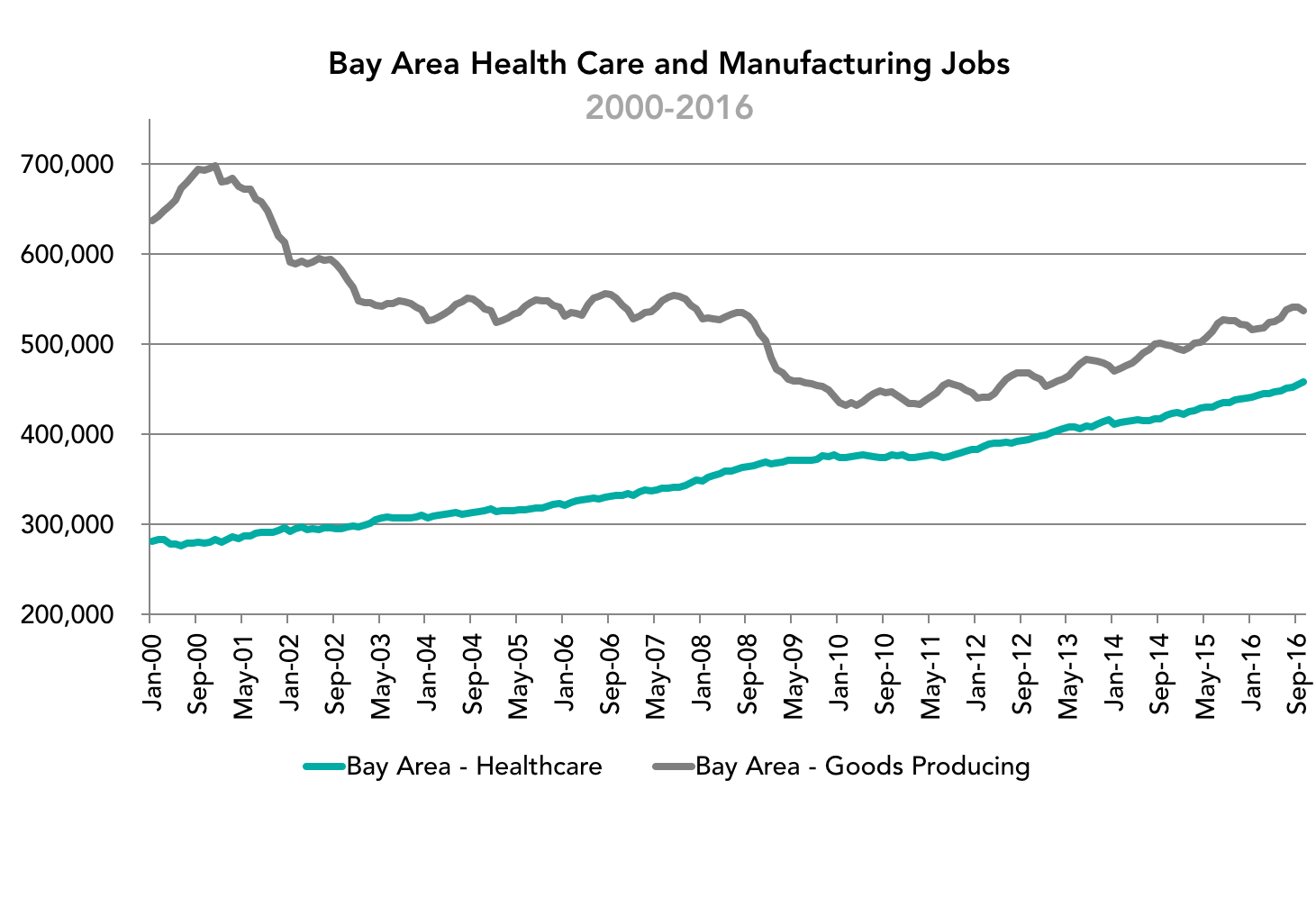

The trend in the Bay Area mirrors the trend in California and highlights the other missing piece of the conversation. Though manufacturing jobs are far below their historic peaks in the mid-20th century, there has been a slow and steady rebound of manufacturing employment in the region over the course of the past 5+ years. This is indicative of the increasing strength of the domestic economy during this time, and the emergence of export-driven high value-added manufacturing clusters in the Bay Area and throughout the nation. Pretending that manufacturing jobs are still in freefall, therefore, may lead to a belief that more aggressive anti-trade measures could prop up this sector of the economy. They would be much more likely, however, to choke off this rebound and impact not only these jobs but an economy that is producing a greater value of manufactured goods than at any other time in history.

Written by Micah Weinberg, PhD

Institute Welcomes New Chair

The Bay Area Council Economic Institute is happy to announce the appointment of Kausik Rajgopal to Chair of the Institute’s Board of Trustees. Kausik is Senior Partner and West Coast Regional Manager at McKinsey & Company, and brings extensive experience in strategy, operations, and the public sector. In addition to serving as Chair of the Economic Institute, Kausik also serves on the advisory board of Stanford University’s Center for Comparative Studies in Race and Ethnicity.

The Institute would like to thank outgoing Chair, Dr. Laura D’Andrea Tyson, for her exceptional service and ongoing commitment to the Institute and to the Bay Area. Under Dr. Tyson’s leadership the Institute released dozens of highly-influential reports and hosted thoughtful economic and public policy discussions with elected officials and thought leaders from here and abroad.

Solving The Housing Affordability Crisis:

How Policies Change the Number Of San Francisco Households Burdened by Housing Costs

On Wednesday October 19th, the Bay Area Council Economic Institute released its one of a kind Solving the Housing Affordability Crisis report, an analysis of how policies in San Francisco affect the number of households burdened by housing costs. The report compiles a list of 20 housing-related state and local policies that increase and worsen affordability in San Francisco. The analysis finds that while the city has seen an increase of 22% in employment between 2009 and 2015, it has lagged on the development of new housing, causing demand to drive up housing costs.

The report calls for state and local policymakers to consider the impact their policies have on housing affordability for individuals and families. The analysis ultimately finds that the best way to alleviate housing cost burdens is by building all types of housing.

The report was featured in an editorial piece on the San Francisco Chronicle’s Sunday paper, where it received praise for its objectiveness.

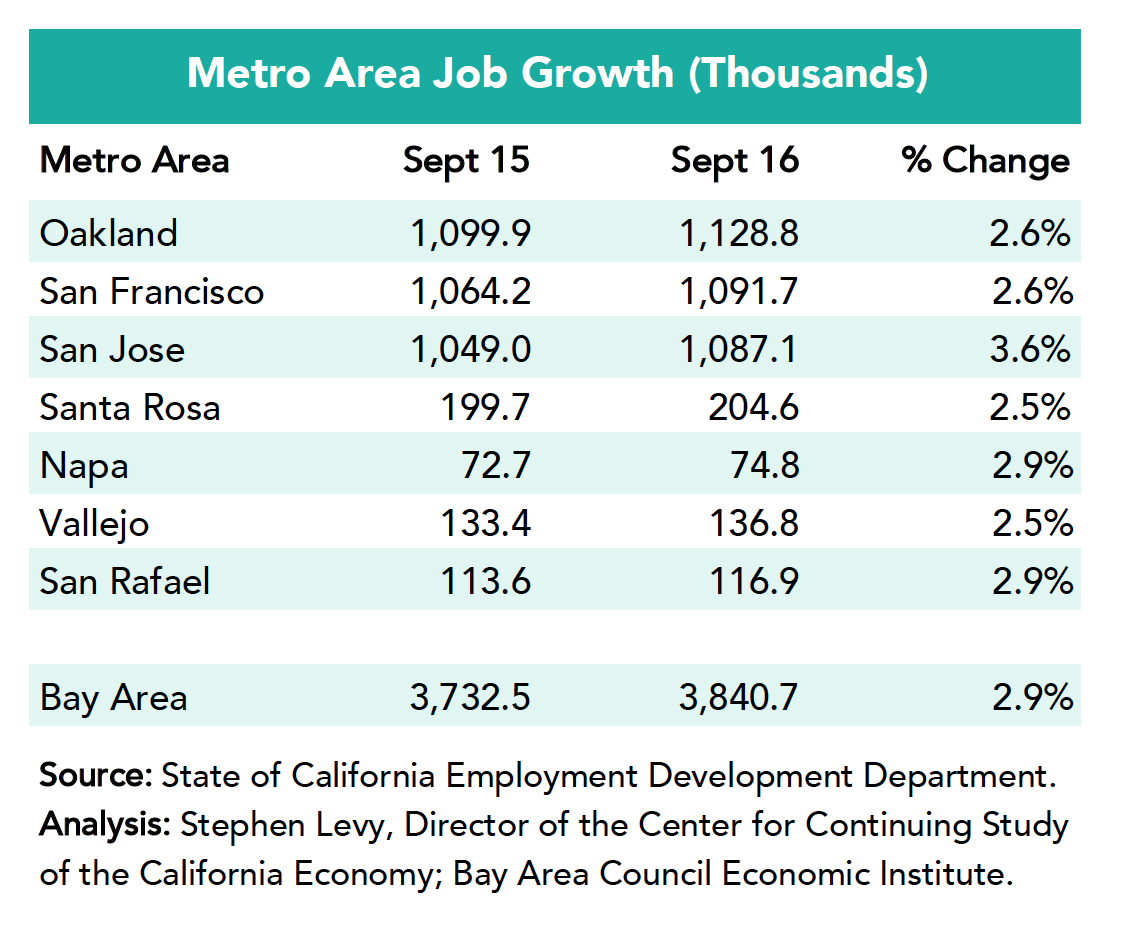

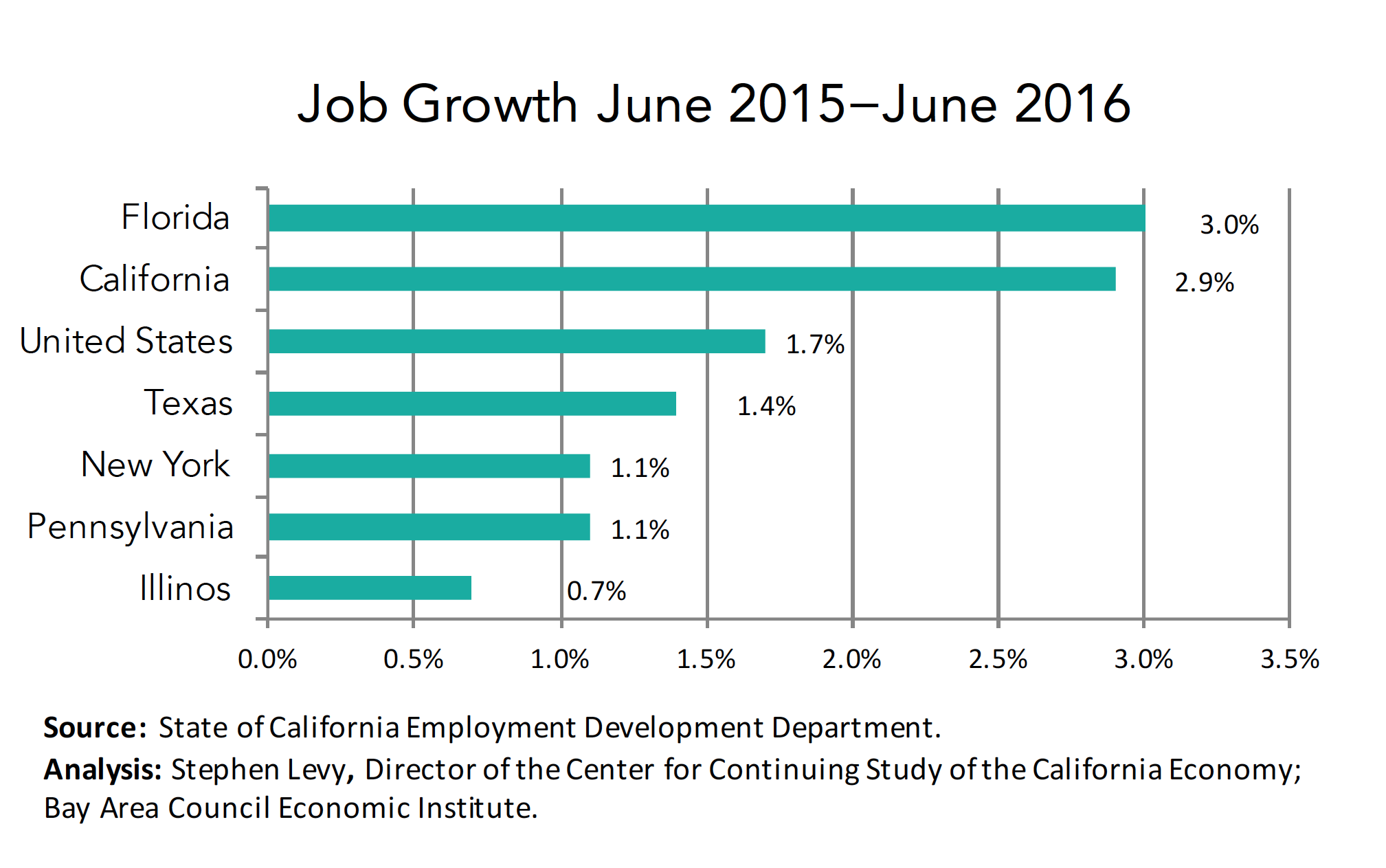

This month’s Bay Area Job Watch found that the region added 108,100 jobs between September 2015 and 2016 for a gain of 2.9% compared to 1.7% for the nation and 2.3% for California. While the pace of growth has slowed from the mid-summer 2015 highs year over year gains remain robust.

Yet the most impressive statistic in the September report is the continuing strong increase in the region’s labor force. In the past 12 months 123.800 workers have joined the labor force (+3.0%) far outpacing the 1.0% population increase. This means that economic growth is reaching more people in the region and that is good news. All of these trends underscore the importance of policies to increase housing and make sure that housing and transportation challenges do not undermine the region’s still vibrant economic competitiveness.

Upcoming Events and Report Releases

ANNUAL ECONOMIC FORECAST

January 20, 2017

8:00am – 11:00am

Federal Reserve Bank of San Francisco

Yellen Conference Center

101 Market Street

San Francisco, CA 94105

Upcoming Board Meetings

Basic Board of Directors Meeting

December 12, 2016

2:00pm – 8:00pm

University of California, San Francisco

BASIC Board of Directors and By Invitation Only

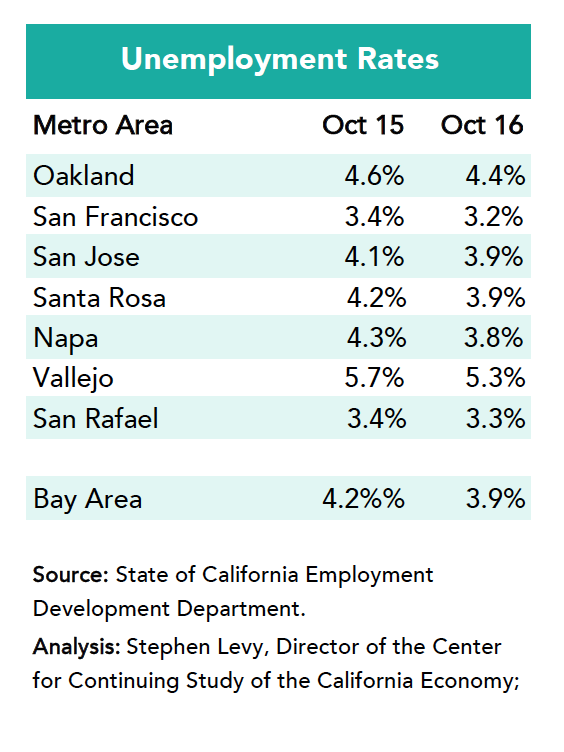

The California Employment Development Department (EDD) has released job and labor force estimates for October 2016. Here are the highlights

Possibly the most impressive statistic in the October report is the continuing strong increase in the region’s labor force. In the past 12 months 116,700 workers have joined the labor force (+2.8%) far outpacing the 1.0% population increase. While monthly labor force participation rate estimates are not available for the region, it must be true from these numbers that the region’s force participation rate has jumped while baby boomer retirements continue to put downward pressure on labor force growth.

This means that economic growth is reaching more people in the region and that is good news. Not everyone is fully participating but the trend is positive and unemployment rates remain low despite fast labor force growth.

Year Over Year Job Growth Strong but Slowing Slightly

The region added 102,000 jobs between October 2015 and 2016 for a gain of 2.7% compared to 1.7% for the nation and 2.4% for California. The pace of growth has slowed from the mid-summer 2015 highs although year over year gains remain robust.

Year over year job growth remains above the national average in all metro areas.

The job gains continue to support low unemployment rates while the labor force continues to add workers although the region is now at or close to full employment.

While year over year job gains have declined from mid 2015 peaks, they remain in very healthy territory with no signs of a significant loss of competitive advantage. Job growth rates in 2016 are likely to be the peak going forward as baby boomer retirements are slowing labor force growth.

The continuing job growth now that unemployment rates have fallen will bring new residents to the region as will the growing need to replace retiring workers.

All of these trends underscore the importance of policies to increase housing and make sure that housing and transportation challenges do not undermine the region’s still vibrant economic competitiveness. Bay Area residents approved many funding measures for transportation and several local measures give hope that the housing supply and affordability challenges are being increasingly recognized by residents.

The national election results have implications for the state and regional economy that will be explored by the Bay Area Council Economic Institute in future months.

Some of the obvious areas of concern are the negative impacts that restricting trade and immigration will have on an innovation economy.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

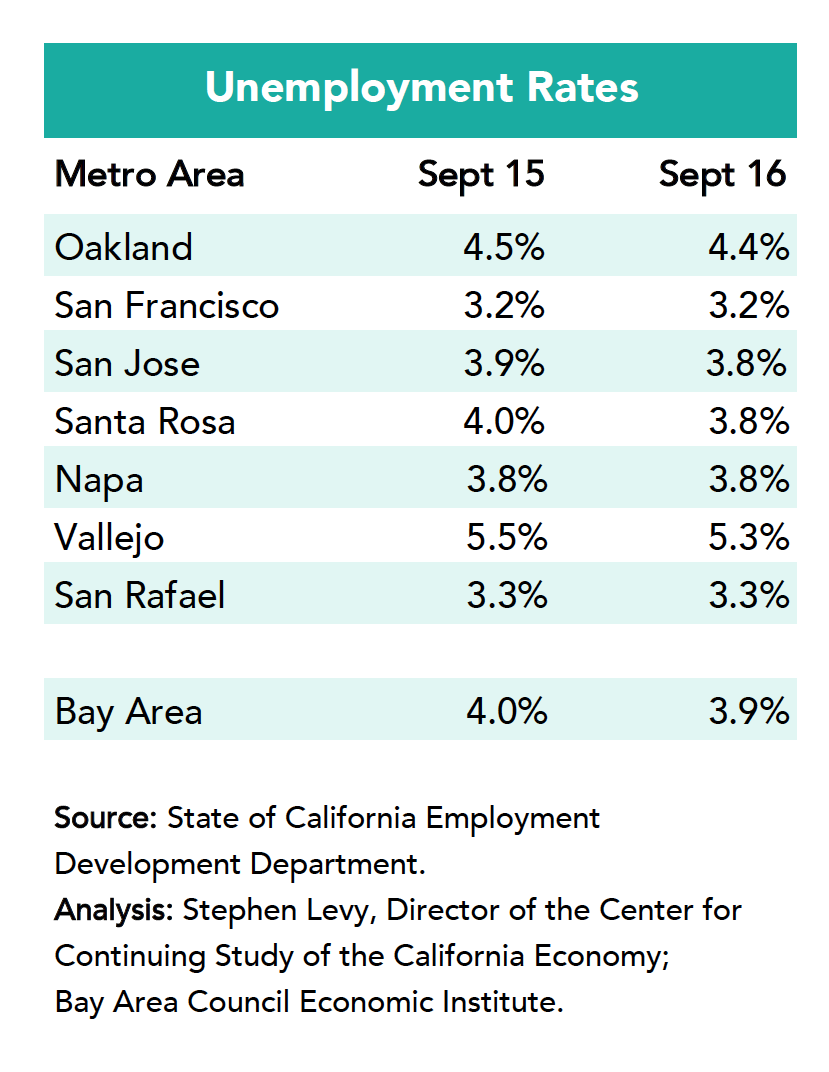

The California Employment Development Department (EDD) has released job and labor force estimates for September 2016. Here are the highlights:

Possibly the most impressive statistic in the September report is the continuing strong increase in the region’s labor force. In the past 12 months 123.800 workers have joined the labor force (+3.0%) far outpacing the 1.0% population increase. While monthly labor force participation rate estimates are not available for the region, it must be true from these numbers that the region’s force participation rate has jumped while baby boomer retirements continue to put downward pressure on labor force growth.

This means that economic growth is reaching more people in the region and that is good news. Not everyone is fully participating but the trend is positive and unemployment rates remain low despite fast labor force growth.

Year Over year Growth Increased in September

The region added 108,100 jobs between September 2015 and 2016 for a gain of 2.9% compared to 1.7% for the nation and 2.3% for California. The pace of growth has slowed from the mid-summer 2015 highs although year over year gains remain robust.

Year over year job growth picked up a bit in September as discussed above and remains far above the national average in all metro areas.

The job gains continue to reduce unemployment rates (more slowly in September) while the labor force continues to add workers although the region is now at or close to full employment.

While year over year job gains have declined slightly from mid-2015 peaks, they remain in very healthy territory with no signs of a significant loss of competitive advantage. Job growth rates in 2016 are likely to be the peak going forward as baby boomer retirements are slowing labor force growth.

The continuing job growth now that unemployment rates have fallen will bring new residents to the region as will the growing need to replace retiring workers.

All of these trends underscore the importance of policies to increase housing and make sure that housing and transportation challenges do not undermine the region’s still vibrant economic competitiveness. Bay Area residents will have many opportunities at the ballot in November to support investments in transportation and housing for low income and vulnerable residents.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

By Micah Weinberg and Derecka Mehrens Published on 9/29/2016

This piece originally appeared in The Mercury News

Santa Clara County voters have a once in a generation opportunity in November to support essential investments in transportation improvement when they decide how to vote on Measure B. This half-cent, 30-year sales tax measure will repair streets and complete the BART extension to San Jose and Santa Clara among other important investments.

If passed by two-thirds of voters, the measure will generate $6.3 billion to fund transportation projects. But in addition to this investment, there are other immense economic benefits derived from improving roads and transit in the county.

A recent study by the Bay Area Council Economic Institute found that Measure B will be a gigantic economic boon to the county, creating nearly 4,000 jobs and more than $15.4 billion in increased business output.

The good jobs Measure B will support cut across a range of industries, skills and incomes, including construction jobs, manufacturing and professional services. Local workers and businesses will be among the chief beneficiaries.

The $6.3 billion in total transportation spending over 30 years will stimulate the local economy through local contracting and support on-going operations and maintenance jobs.

Further, this funding will allow Santa Clara County to leverage additional funds for greater investment from state and federal sources and create an even greater impact. The direct spending will have ripple effects as dollars change hands and translate into new jobs and new business revenues.

To calculate the economic impacts, the Bay Area Council Economic Institute employed computer modeling widely used by federal, state, and local transportation agencies. The model considers a range of information and projections, including future population growth and travel patterns, labor and goods movement, market access and construction spending, to estimate the costs, benefits, and economic impacts that flow from them.

In addition to the many direct and indirect effects of Measure B investments, there are other economic impacts that are just as important but more difficult to quantify.

For example, San Jose has the fastest growing traffic congestion of any metropolitan area in the U.S. From 2010 to 2014, the annual number of hours of traffic delay per commuter grew from 37 to 51 hours, a 36.8 percent increase. It’s one of only two major metropolitan areas to exceed a 30 percent increase.

That growing delay creates a huge drag on worker productivity, discourages new economic investment, adds to harmful air pollution and generally diminishes our quality of life.

The immediate benefits of more efficient transportation are most easily noticed in reduced congestion, expanded transportation options and travel time savings.

The long-term benefits of infrastructure investments like this can shape the region’s economy and prepare it for continued economic growth and resiliency against future downturns, including improving access to jobs for the county’s residents, providing economic development opportunities near new transportation hubs, extending the regional labor pool available to employers and enhancing worker productivity.

Santa Clara County was the first in the state to use a sales tax to pay for local transportation infrastructure when Measure A was passed in 1976. The county has continued to use sales taxes to fund transportation – to the tune of raising $8 billion over the last 40 years. In that time, Santa Clara County has built the fastest growing economy in the United States.

In Silicon Valley, where taking risks is a way of life, investing in transportation infrastructure is almost a sure thing.

Micah Weinberg is president of the Bay Area Council Economic Institute. Derecka Mehrens is executive director of Working Partnerships USA. They wrote this for The Mercury News.

The California Employment Development Department (EDD) has released job estimates for August 2016. Here are the highlights:

Year over year growth slowing, but still strong

The region added 101,800 jobs between August 2015 and 2016 for a gain of 2.7% compared to 1.7% for the nation and 2.3% for California. The pace of growth has slowed from the mid-summer 2015 highs although year over year gains remain robust. The state jobs report showed a gain of 63,100 jobs in August but the Bay Area added only 4,000 jobs seasonally adjusted, an estimate that is likely to be revised up as it is implausible that the region added barely 5% of the state gains.

The job gains continue to reduce unemployment rates while the labor force continues to add workers.

Year over year job growth slowed in June as discussed above but remains far above the national average in all metro areas.

Possibly the most impressive statistic in the August report is the very strong increase in the region’s labor force. In the past 12 months 92,400 workers have joined the labor force (+2.2%) far outpacing the 1.0% population increase. While monthly labor force participation rate estimates are not available, it must be true from these numbers that the region’s force participation rate has jumped while the comparable state and national rates are under pressure from baby boomer retirement.

This means that economic growth is slowly reaching more people in the region and that is good news. Not everyone is fully participating but the trend is toward improvement.

While year over year job gains have declined slightly from mid 2015 peaks, they remain in very healthy territory with no signs of a significant loss of competitive advantage. Job growth rates in 2016 are likely to be the peak going forward as baby boomer retirements are slowing labor force growth.

The California job growth trends put the state near of the top of the nation’s most populous states, in part because job growth has accelerated in Southern California and parts of the Central Valley including San Joaquin County adjacent to the Bay Area and also in Fresno County.

The continuing job growth now that unemployment rates have fallen will bring new residents to the region as will the growing need to replace retiring workers.

All of these trends underscore the importance of policies to increase housing and make sure that housing and transportation challenges do not undermine the region’s still vibrant economic competitiveness.

These economic updates are authored by Stephen Levy, Director of the Center for Continuing Study of the California Economy, and a member of the Bay Area Council Economic Institute board.

This month, the U.S. Bureau of Economic Analysis released 2015 GDP estimates for metropolitan areas in the nation. An analysis by Stephen Levy from the Center for Continuing Study of the California Economy found that all major regions in California came ahead of the nation in real GPD growth, but the Bay Area lead both the state and the nation with a real GDP gain of 5.8% (inflation adjusted). The Bay Area’s $721 billion dollar economy would land it 6th among the top ten states measured by the value of goods and services produced in each state. Globally, the Bay Area would rank 16th just behind Mexico and ahead of Indonesia.

The San Jose-Sunnyvale-Santa Clara and San Francisco-Oakland metropolitan areas led all metro areas in California in real GDP growth in 2015 with an increase of 8.9% and 4.1%, respectively. Part of San Jose-Sunnyvale-Santa Clara metro area’s economic success is attributed to its continuous growth in the technology sector, which ultimately made it the 2nd fastest growing metropolitan region in the nation between 2014 and 2015.

Overall, Califonia continues leading the nation with $2,459 billion dollars in real GDP in 2015 as all regions in the state outpaced the nation.

By Sean Randolph and Mark Pisano Published on 9/19/2016

This piece originally appeared in the Capitol Weekly

They blew it. Fifteen months ago, Governor Brown called the Legislature into special session to find new ways to pay for the state’s aging transportation system.

A huge coalition—from highway and transit groups to trucking associations and business and labor organizations—asked the Legislature to put money into the system and improve accountability and results, citing clear benefits for jobs, economic development, and the environment.

Nothing happened.

Some hearings were held and a few tax proposals were considered, none on the scale needed to do the job. None were voted on, and the special session recessed last week with a whimper.

It’s time to move in a new direction—away from Sacramento’s political gridlock and toward a regional approach to governing and funding California’s transportation systems.

Until we do, it’s clear California’s deteriorating roads and aging transit systems will only get worse—continuing to be a drag on the economy. The Legislature focused this year on one part of the problem: the state’s $59 billion backlog in road maintenance. CA Fwd recently concluded that our transportation systems, from highways and bridges to airports and local roads, will require almost 10 times that much—$530 billion—to safely maintain and operate over the next 10 years. With the main source of state revenue—the gas tax—failing to keep pace with demand, public agencies have less than half the funds they need to pay for it. The state’s total transportation funding shortfall? Nearly $300 billion and climbing.

The source of this problem isn’t just funding or Sacramento politics: It’s an obsolete governance system—one that, for decades, funneled large amounts of federal money, matched with state dollars, to road, highway, and transit projects. With federal money drying up, state money is proving inadequate, and our leaders can’t seem to find innovative solutions.

While the state fiddles, local governments are taking action—and it’s at the local and regional level that the next generation of transportation solutions must be devised.

Taxpayers in 21 counties already pay for a sizable portion of their own transportation systems. These so-called “self-help” counties have approved $4 billion a year in local sales tax measures for everything from highway tunnels and transit extensions to local roads.

Those numbers are about to get a lot bigger.